S-ar putea să vă placă și

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)De la EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Evaluare: 4.5 din 5 stele4.5/5 (5)

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)De la EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)Încă nu există evaluări

- CFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)De la EverandCFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Evaluare: 5 din 5 stele5/5 (1)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)De la EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Evaluare: 5 din 5 stele5/5 (1)

- Midterm 1 (HK1 2018-19) KeyDocument69 paginiMidterm 1 (HK1 2018-19) KeyĐặng Khánh LinhÎncă nu există evaluări

- Final Testbank For Tax 4001Document74 paginiFinal Testbank For Tax 4001ceimeen50% (2)

- Taxation Chapter 5 - 8Document117 paginiTaxation Chapter 5 - 8Hồng Hạnh NguyễnÎncă nu există evaluări

- Binder1 PDFDocument5 paginiBinder1 PDFSaad Raza KhanÎncă nu există evaluări

- Invoice: Order Details Billing SummaryDocument2 paginiInvoice: Order Details Billing SummaryOussama AkkariÎncă nu există evaluări

- Fsa Questions FBNDocument34 paginiFsa Questions FBNsprykizyÎncă nu există evaluări

- Tax Ch6 QuizDocument13 paginiTax Ch6 QuizJoshua Alan Braden0% (1)

- Full Download Finance Applications and Theory 4th Edition Cornett Test Bank PDF Full ChapterDocument36 paginiFull Download Finance Applications and Theory 4th Edition Cornett Test Bank PDF Full Chaptercategory.torskhwbgd100% (16)

- Finance Applications and Theory 4th Edition Cornett Test BankDocument21 paginiFinance Applications and Theory 4th Edition Cornett Test Bankkilter.murk0nj3mx100% (35)

- MC Problems QuesDocument11 paginiMC Problems QuesJustine Mae AgapitoÎncă nu există evaluări

- AICPA - CPA Reg 2017Document12 paginiAICPA - CPA Reg 2017Gene'sÎncă nu există evaluări

- Financial Accounting & Reporting Final Examination: Name: Date: Professor: Section: ScoreDocument17 paginiFinancial Accounting & Reporting Final Examination: Name: Date: Professor: Section: ScoreMaryjoy NemenoÎncă nu există evaluări

- Before We Begin RevisedDocument2 paginiBefore We Begin RevisedBaburam AdÎncă nu există evaluări

- Fall10mid1 ProbandsolnDocument8 paginiFall10mid1 Probandsolnivanata72Încă nu există evaluări

- Bài tập ôn tập chapter 4 Ms.TrangDocument8 paginiBài tập ôn tập chapter 4 Ms.TrangNgọc Trung Học 20Încă nu există evaluări

- ACCOUNTING COMPETENCY EXAM SAMPLEDocument12 paginiACCOUNTING COMPETENCY EXAM SAMPLEAmber AJÎncă nu există evaluări

- Practice Final (New Material Only)Document12 paginiPractice Final (New Material Only)Bree JiangÎncă nu există evaluări

- CAE 2 Financial Accounting and Reporting: Lyceum-Northwestern UniversityDocument15 paginiCAE 2 Financial Accounting and Reporting: Lyceum-Northwestern UniversityAmie Jane MirandaÎncă nu există evaluări

- Objective Questions of AccountingDocument8 paginiObjective Questions of Accountingshobhitgoel0% (1)

- Acc Exam 1Document21 paginiAcc Exam 1binalamitÎncă nu există evaluări

- Chapter 01 02 Selected MCQsDocument7 paginiChapter 01 02 Selected MCQsLe Hong Phuc (K17 HCM)Încă nu există evaluări

- Income Tax Fundamentals 2013 31St Edition Whittenburg Test Bank Full Chapter PDFDocument67 paginiIncome Tax Fundamentals 2013 31St Edition Whittenburg Test Bank Full Chapter PDFjohndorothy0h3u100% (11)

- Income Tax Fundamentals 2013 31st Edition Whittenburg Test BankDocument46 paginiIncome Tax Fundamentals 2013 31st Edition Whittenburg Test Bankhoatuyenbm5k100% (24)

- Lyceum-Northwestern University: Income Statement Balance Sheet Debit Credit Debit CreditDocument12 paginiLyceum-Northwestern University: Income Statement Balance Sheet Debit Credit Debit CreditAmie Jane Miranda0% (1)

- ACF L 4 ExamDocument5 paginiACF L 4 ExamJemal SeidÎncă nu există evaluări

- Microsoft Word - FINA5340 Practice Question 1 Spring 2019Document10 paginiMicrosoft Word - FINA5340 Practice Question 1 Spring 2019Mai PhamÎncă nu există evaluări

- Test Bank For Fundamental Financial Accounting Concepts 8th Edition EdmondsDocument29 paginiTest Bank For Fundamental Financial Accounting Concepts 8th Edition Edmondsooezoapunitory.xkgyo4100% (35)

- Full Download Test Bank For Fundamental Financial Accounting Concepts 8th Edition Edmonds PDF Full ChapterDocument36 paginiFull Download Test Bank For Fundamental Financial Accounting Concepts 8th Edition Edmonds PDF Full Chapternicholaswright18082003jsa100% (18)

- 6352 Pract Exam Part 1Document5 pagini6352 Pract Exam Part 1iluvumiÎncă nu există evaluări

- DHS Accountancy 2021Document30 paginiDHS Accountancy 2021Kuenga Geltshen100% (2)

- Financial Accounting Canadian 4th Edition Libby Test BankDocument59 paginiFinancial Accounting Canadian 4th Edition Libby Test BankBrianWilsonqekdn100% (14)

- Recitation Quiz 1Document5 paginiRecitation Quiz 1BlairEmrallafÎncă nu există evaluări

- Practice Final (New Material Only) SOLUTIONSDocument13 paginiPractice Final (New Material Only) SOLUTIONSBree JiangÎncă nu există evaluări

- Gross Income and DeductionsDocument6 paginiGross Income and DeductionsIvan Fausto OranteÎncă nu există evaluări

- Practice Final Exam ReviewDocument200 paginiPractice Final Exam ReviewChad Vincent B. BollosaÎncă nu există evaluări

- Finance 323 - FinalDocument14 paginiFinance 323 - FinalSounak Srimanti SahaÎncă nu există evaluări

- ACCT 202 PQ4 SPR 18Document9 paginiACCT 202 PQ4 SPR 18catacutantriciamae13Încă nu există evaluări

- Sample Exam Ch2Document12 paginiSample Exam Ch2wikidoggÎncă nu există evaluări

- Practice Test II TrueFalse Indicate Whether The Statement Is TrueDocument15 paginiPractice Test II TrueFalse Indicate Whether The Statement Is TrueKhushboo BadayaÎncă nu există evaluări

- Income Tax Fundamentals 2012 30Th Edition Whittenburg Test Bank Full Chapter PDFDocument67 paginiIncome Tax Fundamentals 2012 30Th Edition Whittenburg Test Bank Full Chapter PDFjohndorothy0h3u100% (6)

- 2018-I PD5Document6 pagini2018-I PD5magicÎncă nu există evaluări

- Abs3 TheoryDocument31 paginiAbs3 TheoryHassenÎncă nu există evaluări

- TN+TLDocument21 paginiTN+TL2121013027Încă nu există evaluări

- Ch4 MC1,2Document5 paginiCh4 MC1,2ChaituÎncă nu există evaluări

- Fundamental Financial Accounting Concepts 8th Edition Edmonds Test Bank DownloadDocument147 paginiFundamental Financial Accounting Concepts 8th Edition Edmonds Test Bank DownloadKeith Meacham100% (23)

- Oshwal College: Association of Chartered Certified Accountants (ACCA) Foundation Level FA2 Maintaining Financial RecordsDocument6 paginiOshwal College: Association of Chartered Certified Accountants (ACCA) Foundation Level FA2 Maintaining Financial RecordsKhushi SinghÎncă nu există evaluări

- Group Work #1 With SolutionsDocument3 paginiGroup Work #1 With SolutionsShadi MorakabatiÎncă nu există evaluări

- Accounts Practice Answers Tutorial 1Document8 paginiAccounts Practice Answers Tutorial 1PGP 2023Încă nu există evaluări

- FAR CPA Exam Practice QuestionsDocument8 paginiFAR CPA Exam Practice QuestionsDarlene JacaÎncă nu există evaluări

- PA - T NG H P TestbankDocument86 paginiPA - T NG H P TestbankBích Phan Ngô NgọcÎncă nu există evaluări

- Practice Exam 1Document14 paginiPractice Exam 1borisdpunÎncă nu există evaluări

- PACE Sample ExamDocument13 paginiPACE Sample ExamjhouvanÎncă nu există evaluări

- BookkeepingDocument20 paginiBookkeepingzhanel bekenovaÎncă nu există evaluări

- Income Tax Fundamentals 2019 37Th Edition Whittenburg Test Bank Full Chapter PDFDocument36 paginiIncome Tax Fundamentals 2019 37Th Edition Whittenburg Test Bank Full Chapter PDFacrania.dekle.z2kajy100% (7)

- Intermediate Financial Accounting Model DirDocument14 paginiIntermediate Financial Accounting Model Dirmelkamu tesfayÎncă nu există evaluări

- PILOT TEST 2023Document6 paginiPILOT TEST 2023bapeboiz1510Încă nu există evaluări

- Quiz ch1 2Document5 paginiQuiz ch1 2loveshareÎncă nu există evaluări

- Economic & Budget Forecast Workbook: Economic workbook with worksheetDe la EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetÎncă nu există evaluări

- Jurnal PajakDocument43 paginiJurnal PajakIndahÎncă nu există evaluări

- The Cash Transactions and Cash Balances of Banner Inc ForDocument1 paginăThe Cash Transactions and Cash Balances of Banner Inc Foramit raajÎncă nu există evaluări

- Forex Service Charges: Exports Bills Purchased /Discounted/NegotiatedDocument9 paginiForex Service Charges: Exports Bills Purchased /Discounted/NegotiatedSameer GhogaleÎncă nu există evaluări

- Application EstampDocument1 paginăApplication Estampvijay_vbvÎncă nu există evaluări

- Chapter 22Document61 paginiChapter 22Tim LeeÎncă nu există evaluări

- CIR Vs YMCADocument2 paginiCIR Vs YMCAGianna de JesusÎncă nu există evaluări

- 365) - The Income Tax Rate Is 40%. Additional Expenses Are Estimated As FollowsDocument3 pagini365) - The Income Tax Rate Is 40%. Additional Expenses Are Estimated As FollowsMihir HareetÎncă nu există evaluări

- Solved Whaleco Acquired All of The Common Stock of Minnowco EarlyDocument1 paginăSolved Whaleco Acquired All of The Common Stock of Minnowco EarlyAnbu jaromiaÎncă nu există evaluări

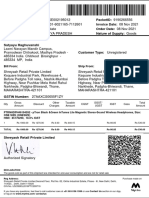

- Tax Invoice: Original For RecipientDocument3 paginiTax Invoice: Original For RecipientS V ENTERPRISESÎncă nu există evaluări

- FASTag - Statement1032014763720200501124625793 - OW PDFDocument4 paginiFASTag - Statement1032014763720200501124625793 - OW PDFNarasimha SandakaÎncă nu există evaluări

- Floating Rate Saving BondDocument6 paginiFloating Rate Saving Bondmanoj barokaÎncă nu există evaluări

- Direct Tax Interview Questions For ArticleshipDocument15 paginiDirect Tax Interview Questions For ArticleshipAayush GamingÎncă nu există evaluări

- Inv 407306401237Document2 paginiInv 407306401237hesima4637 bodeem.comÎncă nu există evaluări

- Lic Ecs Mandate Form EnglishDocument3 paginiLic Ecs Mandate Form EnglishpajipitarÎncă nu există evaluări

- BFCI FINAL ENGAGEMENT PROPOSAL Silver FernDocument2 paginiBFCI FINAL ENGAGEMENT PROPOSAL Silver FernGeram ConcepcionÎncă nu există evaluări

- Tugas Mike P5-3ADocument6 paginiTugas Mike P5-3Awinda dwi lestariÎncă nu există evaluări

- CIR V CA and GCLDocument2 paginiCIR V CA and GCLWilliam SantosÎncă nu există evaluări

- Statement of Account As at 16 July 2023: For Adjust Alignment Issue, Didn't RemoveDocument2 paginiStatement of Account As at 16 July 2023: For Adjust Alignment Issue, Didn't RemovekakakkawaiiÎncă nu există evaluări

- Income Under The Head of SalaryDocument2 paginiIncome Under The Head of Salarykajal100% (1)

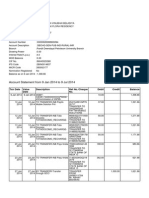

- Account Statement SummaryDocument5 paginiAccount Statement SummaryManthan BeladiyaÎncă nu există evaluări

- M/Chip Functional Architecture For Debit and Credit: Applies To: SummaryDocument12 paginiM/Chip Functional Architecture For Debit and Credit: Applies To: SummaryAbiy MulugetaÎncă nu există evaluări

- Manipalcigna Prohealth Group Insurance PolicyDocument3 paginiManipalcigna Prohealth Group Insurance PolicykeviletuoÎncă nu există evaluări

- Tax invoice for headphonesDocument1 paginăTax invoice for headphonesSachin FfÎncă nu există evaluări

- Final Exam-Basic AccountingDocument2 paginiFinal Exam-Basic AccountingNoel Buenafe JrÎncă nu există evaluări

- BIR RulingDocument3 paginiBIR RulingyakyakxxÎncă nu există evaluări

- Philippine Geothermal, Inc. vs. Commissioner of Internal Revenue, 465 SCRA 308 (2005)Document2 paginiPhilippine Geothermal, Inc. vs. Commissioner of Internal Revenue, 465 SCRA 308 (2005)VerlynMayThereseCaroÎncă nu există evaluări

- On January 1 2014 Alicia Masingale Established Leopard Realty WhichDocument1 paginăOn January 1 2014 Alicia Masingale Established Leopard Realty WhichAmit PandeyÎncă nu există evaluări