S-ar putea să vă placă și

- "Quasi-Contract": Law of Contracts-1Document21 pagini"Quasi-Contract": Law of Contracts-1Muhammad MahatabÎncă nu există evaluări

- Contract ProjectDocument7 paginiContract ProjectPragalbh Bhardwaj0% (1)

- Freedon of Profession, Occupation, Trade or BusinessDocument58 paginiFreedon of Profession, Occupation, Trade or BusinessKumail fatimaÎncă nu există evaluări

- Legal Status of Animals, Unborn Person & Dead ManDocument12 paginiLegal Status of Animals, Unborn Person & Dead ManHare Krishna RevolutionÎncă nu există evaluări

- Saima Gous Tort ProjectDocument15 paginiSaima Gous Tort ProjectShadabÎncă nu există evaluări

- Contract of GuaranteeDocument6 paginiContract of GuaranteeKumari PiyaÎncă nu există evaluări

- Synopsis Meaning Void Marriages Voidable Marriages Difference Between Void and Voidable Marriages Legitimacy of Children Case Laws ConclusionDocument5 paginiSynopsis Meaning Void Marriages Voidable Marriages Difference Between Void and Voidable Marriages Legitimacy of Children Case Laws ConclusionSiddhesh Kamat AzrekarÎncă nu există evaluări

- Wagering Agreement & Contingent Contract PDFDocument9 paginiWagering Agreement & Contingent Contract PDFSamrat DashÎncă nu există evaluări

- A Critical Analysis of The Shah Bano CasDocument7 paginiA Critical Analysis of The Shah Bano Casvijaya choudharyÎncă nu există evaluări

- History ProjectDocument17 paginiHistory ProjectGAURI JHAÎncă nu există evaluări

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDocument29 paginiDamodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaArabinda SahooÎncă nu există evaluări

- Stridhan ProjectDocument13 paginiStridhan ProjectTanraj SinghÎncă nu există evaluări

- Model Q The Partnership Act 1932Document17 paginiModel Q The Partnership Act 1932api-226230529Încă nu există evaluări

- Hindu Law Notes 5 PDF FreeDocument122 paginiHindu Law Notes 5 PDF Freehoney DhingraÎncă nu există evaluări

- Relations in Nature of Marriage and Legal WedlockDocument11 paginiRelations in Nature of Marriage and Legal WedlockSagar KamraniÎncă nu există evaluări

- Succession To StridhanDocument19 paginiSuccession To StridhanAnirudh GoelÎncă nu există evaluări

- Hindu Joint Family and Coparcenary - An AnalysisDocument9 paginiHindu Joint Family and Coparcenary - An Analysisbelievable or unbelievableÎncă nu există evaluări

- Judicial Views On Conditional Legislation - Effects and Implication-An OverviewDocument16 paginiJudicial Views On Conditional Legislation - Effects and Implication-An OverviewGaurav AryaÎncă nu există evaluări

- Agreement in Restraint of MarriageDocument10 paginiAgreement in Restraint of MarriageRajat KaushikÎncă nu există evaluări

- Motor Vehicles TribunalsDocument21 paginiMotor Vehicles TribunalsVivek GurnaniÎncă nu există evaluări

- Section 125 CRPC PDFDocument5 paginiSection 125 CRPC PDFSaurabh YadavÎncă nu există evaluări

- Maintenance Under CRPCDocument12 paginiMaintenance Under CRPCShubham Phophalia100% (1)

- Kautilyas Arthasastra and Its Impact On Indian Judicial System History ProjectDocument23 paginiKautilyas Arthasastra and Its Impact On Indian Judicial System History ProjectMuppana NikhilaÎncă nu există evaluări

- Schools of Hindu LawDocument3 paginiSchools of Hindu Lawrahulhaina100% (1)

- SEM 7 PRAKASH KUMAR - Law of Evidence - Roll 102 - Section B PDFDocument18 paginiSEM 7 PRAKASH KUMAR - Law of Evidence - Roll 102 - Section B PDFPrakash Kumar100% (1)

- Eco 2 ProjectDocument23 paginiEco 2 Projectprince bhaiÎncă nu există evaluări

- Rajasthan High Court Judgment DT August 10, 2015, Declared The Jain Practice of SantharaDocument46 paginiRajasthan High Court Judgment DT August 10, 2015, Declared The Jain Practice of SantharaLatest Laws TeamÎncă nu există evaluări

- Contract of IndemnityDocument40 paginiContract of IndemnityAditya D Tanwar100% (1)

- Moot Petitioner 2019 SDocument35 paginiMoot Petitioner 2019 SSonal AgarwalÎncă nu există evaluări

- Contract Project Final SiddhantDocument19 paginiContract Project Final SiddhantKonark SinghÎncă nu există evaluări

- Research Paper On Restitution in Void and Voidable ContractsDocument12 paginiResearch Paper On Restitution in Void and Voidable ContractsAvinash KumarÎncă nu există evaluări

- Assignment On Contract Law 1Document17 paginiAssignment On Contract Law 1Aashi watsÎncă nu există evaluări

- Law of Torts - KLE Law Academy NotesDocument133 paginiLaw of Torts - KLE Law Academy NotesSupriya UpadhyayulaÎncă nu există evaluări

- Torts Case CommentDocument10 paginiTorts Case Commenttarun chhapolaÎncă nu există evaluări

- Central University of South Bihar: School of Law and Governance Family Law-IDocument14 paginiCentral University of South Bihar: School of Law and Governance Family Law-Ikumar PritamÎncă nu există evaluări

- Property Law-II ProjectDocument19 paginiProperty Law-II ProjectVanshita GuptaÎncă nu există evaluări

- Family Law Analysis Muthuniar CaseDocument5 paginiFamily Law Analysis Muthuniar CaseJayant ChoudharyÎncă nu există evaluări

- Family Law - Property of A Hindu WomanDocument14 paginiFamily Law - Property of A Hindu Womankriti bhatnagarÎncă nu există evaluări

- Contract 1Document27 paginiContract 1ShreyaÎncă nu există evaluări

- School of Law, Narsee Monjee Institute of Management Studies, BangaloreDocument9 paginiSchool of Law, Narsee Monjee Institute of Management Studies, BangaloreSAURABH SINGHÎncă nu există evaluări

- Family CasesDocument8 paginiFamily CasesPankaj Rathi100% (1)

- Sem 5 Legal Language.Document27 paginiSem 5 Legal Language.Rohan LopezÎncă nu există evaluări

- Essentials of The Specific Relief ACT, 1963Document34 paginiEssentials of The Specific Relief ACT, 1963Abhimanyu SinghÎncă nu există evaluări

- Chapter-Vii Fundamental Freedom of Trade and Commerce in India and RestrictionsDocument38 paginiChapter-Vii Fundamental Freedom of Trade and Commerce in India and RestrictionsIshita GoyalÎncă nu există evaluări

- 2nd Year Family Law Assignment On Muslim MarriagesDocument12 pagini2nd Year Family Law Assignment On Muslim MarriagesDeeveegeeÎncă nu există evaluări

- "Suicide Is Sin, Santhara Is ReligionDocument11 pagini"Suicide Is Sin, Santhara Is Religionarushi agarwalÎncă nu există evaluări

- Aman Pro TortsDocument26 paginiAman Pro TortsShivam PatelÎncă nu există evaluări

- Vicarious Liability 2Document37 paginiVicarious Liability 2natalia malikÎncă nu există evaluări

- Kishore Da 1 PDocument28 paginiKishore Da 1 PKalpita SahaÎncă nu există evaluări

- Muslim Women MaintenanceDocument3 paginiMuslim Women MaintenanceAmber ChaturvediÎncă nu există evaluări

- Whether Judiciary Is StateDocument21 paginiWhether Judiciary Is StateDeeshaÎncă nu există evaluări

- Case Law 2nd SemDocument17 paginiCase Law 2nd SemsimranÎncă nu există evaluări

- ConsiderationDocument31 paginiConsiderationadityaÎncă nu există evaluări

- Constitution Article 16Document21 paginiConstitution Article 16RachitÎncă nu există evaluări

- Consti 2 ProjDocument19 paginiConsti 2 ProjSai Malavika TuluguÎncă nu există evaluări

- Surpeme Court at Calcutta and The East India Company.Document13 paginiSurpeme Court at Calcutta and The East India Company.Shubham Golia100% (1)

- Dear Zindagi ReflectionDocument16 paginiDear Zindagi ReflectionVikas KumarÎncă nu există evaluări

- Excise 1Document6 paginiExcise 1AditiIndraniÎncă nu există evaluări

- Statement of Purpose ITLDocument5 paginiStatement of Purpose ITLAditiIndraniÎncă nu există evaluări

- Gabcikovo-Nagymaros Dams CaseDocument11 paginiGabcikovo-Nagymaros Dams CaseAnkit AnandÎncă nu există evaluări

- Historical School 27.08.2015Document19 paginiHistorical School 27.08.2015AditiIndraniÎncă nu există evaluări

- The International Criminal Court: By: Aditi Indrani Ankit AnandDocument13 paginiThe International Criminal Court: By: Aditi Indrani Ankit AnandAditiIndraniÎncă nu există evaluări

- Muradi List of Dates.Document7 paginiMuradi List of Dates.AditiIndraniÎncă nu există evaluări

- Juris PPT 17.08.2015 NewDocument60 paginiJuris PPT 17.08.2015 NewAditiIndraniÎncă nu există evaluări

- Maternity Benefit Act 1961: Presented By: Niharika Singh Parul Bhatia Richa Nidhi Sagar Gupta Navdeep SamaDocument21 paginiMaternity Benefit Act 1961: Presented By: Niharika Singh Parul Bhatia Richa Nidhi Sagar Gupta Navdeep SamaBhoomika SahuÎncă nu există evaluări

- Client Counseling Exercise: RD TH RDDocument3 paginiClient Counseling Exercise: RD TH RDAditiIndraniÎncă nu există evaluări

- Bonded Labour System (Abolition) ActDocument18 paginiBonded Labour System (Abolition) ActAditiIndraniÎncă nu există evaluări

- BibliographyDocument1 paginăBibliographyAditiIndraniÎncă nu există evaluări

- Sudha Devi CaseDocument15 paginiSudha Devi CaseAditiIndraniÎncă nu există evaluări

- Genocide CaseDocument30 paginiGenocide CaseAditiIndraniÎncă nu există evaluări

- TEAM CODE: JM15-05 5 Jamia Millia National Moot Court Competition 2015Document36 paginiTEAM CODE: JM15-05 5 Jamia Millia National Moot Court Competition 2015AditiIndraniÎncă nu există evaluări

- Recognition of States Is A Matter of Po PDFDocument14 paginiRecognition of States Is A Matter of Po PDFAditiIndraniÎncă nu există evaluări

- India S Practice and Policy of Recognition of States and GovernmentsDocument24 paginiIndia S Practice and Policy of Recognition of States and GovernmentsAnkit AnandÎncă nu există evaluări

- Employees' State Insurance Act, 1948Document48 paginiEmployees' State Insurance Act, 1948AditiIndraniÎncă nu există evaluări

- II. 008. Summary - Norwegian Fisheries CaseDocument3 paginiII. 008. Summary - Norwegian Fisheries CaseMaria Jennifer Yumul BorbonÎncă nu există evaluări

- Legal Concept of Recognition of States in International ArenaDocument11 paginiLegal Concept of Recognition of States in International ArenaAnkit AnandÎncă nu există evaluări

- Legal Person Juris IIDocument31 paginiLegal Person Juris IIAditiIndraniÎncă nu există evaluări

- Demographic DividendDocument57 paginiDemographic DividendAditiIndraniÎncă nu există evaluări

- Magna CartaDocument35 paginiMagna CartaAditiIndraniÎncă nu există evaluări

- Project Report PIL Morality in International Law: Name: Aditi Indrani 2013004Document12 paginiProject Report PIL Morality in International Law: Name: Aditi Indrani 2013004AditiIndraniÎncă nu există evaluări

- Kautilyas ArthashastraDocument10 paginiKautilyas ArthashastraAditiIndraniÎncă nu există evaluări

- 1773regulatingactwithcase 130430042333 Phpapp01Document29 pagini1773regulatingactwithcase 130430042333 Phpapp01Ananya Gupta100% (1)

- Anticipatory Bail Law in IndiaDocument12 paginiAnticipatory Bail Law in IndiaAditiIndraniÎncă nu există evaluări

- Loveless PDFDocument61 paginiLoveless PDFAditiIndraniÎncă nu există evaluări

- Balance B/F 0.00 Payments/RefundsDocument2 paginiBalance B/F 0.00 Payments/RefundssharonÎncă nu există evaluări

- Mid (Zara)Document4 paginiMid (Zara)hbuzdarÎncă nu există evaluări

- Mananquil, Julieta P. - Jeths JefrenDocument12 paginiMananquil, Julieta P. - Jeths JefrenMarissa Bucad GomezÎncă nu există evaluări

- Lira District Report of The Auditor General 2015 PDFDocument59 paginiLira District Report of The Auditor General 2015 PDFlutos2Încă nu există evaluări

- 02012020fin RT4 PDFDocument1 pagină02012020fin RT4 PDFPAO TPT PAO TPTÎncă nu există evaluări

- Pas 26Document2 paginiPas 26AnneÎncă nu există evaluări

- 35 Financial Management FM 71 Imp Questions With Solution For CA Ipcc MsDocument90 pagini35 Financial Management FM 71 Imp Questions With Solution For CA Ipcc Msmysorevishnu75% (8)

- CH 6Document32 paginiCH 6Zead MahmoodÎncă nu există evaluări

- JAIIB Legal Sample Questions by MuruganDocument63 paginiJAIIB Legal Sample Questions by MuruganRizz Ahammad80% (5)

- Risk Capital Management 31 Dec 2011Document181 paginiRisk Capital Management 31 Dec 2011G117Încă nu există evaluări

- Ja TinderDocument6 paginiJa TinderHitlisted VasuÎncă nu există evaluări

- Business Intelligence and BankingDocument12 paginiBusiness Intelligence and BankingniklasÎncă nu există evaluări

- 26nov2022 - 30jan2023Document12 pagini26nov2022 - 30jan2023Srishti SharmaÎncă nu există evaluări

- Rex B. Banggawan, CPA, MBA: Business & Trasfer Tax Solutions Manual True or False: Part 1Document5 paginiRex B. Banggawan, CPA, MBA: Business & Trasfer Tax Solutions Manual True or False: Part 1ela alan100% (2)

- 2012 05 - Project Finance Newswire - May 2012Document56 pagini2012 05 - Project Finance Newswire - May 2012api-165049160Încă nu există evaluări

- Accounting PretestDocument4 paginiAccounting PretestseymourwardÎncă nu există evaluări

- Capstone (M&a IN BANKS IN INDIA)Document13 paginiCapstone (M&a IN BANKS IN INDIA)Mandeep SinghÎncă nu există evaluări

- Nism Xvi - Commodity Derivatives Exam - Practice Test 4Document27 paginiNism Xvi - Commodity Derivatives Exam - Practice Test 4Sohel KhanÎncă nu există evaluări

- MBA 662 Financial Institutions and Investment ManagementDocument4 paginiMBA 662 Financial Institutions and Investment ManagementAli MohammedÎncă nu există evaluări

- G.R. No. 201665Document11 paginiG.R. No. 201665ailynvdsÎncă nu există evaluări

- Ah! Ventures Startup Support ServicesDocument22 paginiAh! Ventures Startup Support ServicesabhishekÎncă nu există evaluări

- Presentation On IOCL - PPT On SUMMER INTERNSHIP PROJECTDocument15 paginiPresentation On IOCL - PPT On SUMMER INTERNSHIP PROJECTMAHENDRA SHIVAJI DHENAK33% (3)

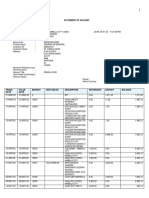

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument9 paginiStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceLoan LoanÎncă nu există evaluări

- Compare Voltas With Blue Star - EquitymasterDocument12 paginiCompare Voltas With Blue Star - Equitymasteratul.jha2545Încă nu există evaluări

- Epc and Ppa ContractsDocument12 paginiEpc and Ppa ContractsCOT Management Training InsituteÎncă nu există evaluări

- Sample Copy - Mphasis &finsource PDFDocument2 paginiSample Copy - Mphasis &finsource PDFSameer ShaikhÎncă nu există evaluări

- Continuous Futures Data Series For Back Testing and Technical AnalysisDocument6 paginiContinuous Futures Data Series For Back Testing and Technical AnalysisIshan SaneÎncă nu există evaluări

- (Sarvesh Dhatrak) Derivatives in Stock Market and Their Importance in HedgingDocument79 pagini(Sarvesh Dhatrak) Derivatives in Stock Market and Their Importance in Hedgingsarvesh dhatrakÎncă nu există evaluări

- GSTIN 18ABPFM4435K1ZQ: InvoiceDocument2 paginiGSTIN 18ABPFM4435K1ZQ: InvoicenirajÎncă nu există evaluări

- Business Analysis & ValuationDocument50 paginiBusiness Analysis & ValuationAimee EemiaÎncă nu există evaluări

- Sales & Marketing Agreements and ContractsDe la EverandSales & Marketing Agreements and ContractsÎncă nu există evaluări

- Profitable Photography in Digital Age: Strategies for SuccessDe la EverandProfitable Photography in Digital Age: Strategies for SuccessÎncă nu există evaluări

- Law of Contract Made Simple for LaymenDe la EverandLaw of Contract Made Simple for LaymenEvaluare: 4.5 din 5 stele4.5/5 (9)

- How to Win Your Case In Traffic Court Without a LawyerDe la EverandHow to Win Your Case In Traffic Court Without a LawyerEvaluare: 4 din 5 stele4/5 (5)

- Legal Guide to Social Media, Second Edition: Rights and Risks for Businesses, Entrepreneurs, and InfluencersDe la EverandLegal Guide to Social Media, Second Edition: Rights and Risks for Businesses, Entrepreneurs, and InfluencersEvaluare: 5 din 5 stele5/5 (1)

- A Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsDe la EverandA Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsÎncă nu există evaluări

- Contracts: The Essential Business Desk ReferenceDe la EverandContracts: The Essential Business Desk ReferenceEvaluare: 4 din 5 stele4/5 (15)

- The Certified Master Contract AdministratorDe la EverandThe Certified Master Contract AdministratorEvaluare: 5 din 5 stele5/5 (1)

- Learn the Essentials of Business Law in 15 DaysDe la EverandLearn the Essentials of Business Law in 15 DaysEvaluare: 4 din 5 stele4/5 (13)

- Technical Theater for Nontechnical People: Second EditionDe la EverandTechnical Theater for Nontechnical People: Second EditionÎncă nu există evaluări

- Crash Course Business Agreements and ContractsDe la EverandCrash Course Business Agreements and ContractsEvaluare: 3 din 5 stele3/5 (3)

- How to Win Your Case in Small Claims Court Without a LawyerDe la EverandHow to Win Your Case in Small Claims Court Without a LawyerEvaluare: 5 din 5 stele5/5 (1)

- The Small-Business Guide to Government Contracts: How to Comply with the Key Rules and Regulations . . . and Avoid Terminated Agreements, Fines, or WorseDe la EverandThe Small-Business Guide to Government Contracts: How to Comply with the Key Rules and Regulations . . . and Avoid Terminated Agreements, Fines, or WorseÎncă nu există evaluări

- Digital Technical Theater Simplified: High Tech Lighting, Audio, Video and More on a Low BudgetDe la EverandDigital Technical Theater Simplified: High Tech Lighting, Audio, Video and More on a Low BudgetÎncă nu există evaluări

- The Business of Broadway: An Insider's Guide to Working, Producing, and Investing in the World's Greatest Theatre CommunityDe la EverandThe Business of Broadway: An Insider's Guide to Working, Producing, and Investing in the World's Greatest Theatre CommunityÎncă nu există evaluări

- Contract Law for Serious Entrepreneurs: Know What the Attorneys KnowDe la EverandContract Law for Serious Entrepreneurs: Know What the Attorneys KnowEvaluare: 1 din 5 stele1/5 (1)

- Independent Film Producing: How to Produce a Low-Budget Feature FilmDe la EverandIndependent Film Producing: How to Produce a Low-Budget Feature FilmÎncă nu există evaluări