S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Network Selection Criterion For Ubiquitous Communication Provisioning in Smart Cities - 2018Document34 paginiNetwork Selection Criterion For Ubiquitous Communication Provisioning in Smart Cities - 2018haidine_DDBonnÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Sustainability 11 01912 v3Document22 paginiSustainability 11 01912 v3haidine_DDBonnÎncă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Quality Attributes in Edge Computing For IoT - A Systematic Mapping Study - March2021Document20 paginiQuality Attributes in Edge Computing For IoT - A Systematic Mapping Study - March2021haidine_DDBonnÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Quality Attributes in Edge Computing For IoT - A Systematic Mapping Study - March2021Document20 paginiQuality Attributes in Edge Computing For IoT - A Systematic Mapping Study - March2021haidine_DDBonnÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- OPNET - Location Based Performance of WiMAX Network For QoS With Optimal BSDocument11 paginiOPNET - Location Based Performance of WiMAX Network For QoS With Optimal BShaidine_DDBonnÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Emerging Trends in Wireless Infrastructure RND June-2022 W Rohd46Document51 paginiEmerging Trends in Wireless Infrastructure RND June-2022 W Rohd46haidine_DDBonnÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Release 0.4: Operations Requirements For The Next Generation of Mobile NetworksDocument24 paginiRelease 0.4: Operations Requirements For The Next Generation of Mobile Networksfixme1960Încă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- China Mobile CRAN White Paper v26 2014Document61 paginiChina Mobile CRAN White Paper v26 2014haidine_DDBonnÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Radio Mobile Program Operating GuideDocument79 paginiRadio Mobile Program Operating GuideuserCCCÎncă nu există evaluări

- NGMN 5G White Paper V1 March-2015 NGMN AllianceDocument125 paginiNGMN 5G White Paper V1 March-2015 NGMN Alliancehaidine_DDBonnÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Top 10 Considerations For A Successful 4G LTE EPC Deployment - Cisco - 2013Document17 paginiTop 10 Considerations For A Successful 4G LTE EPC Deployment - Cisco - 2013haidine_DDBonnÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Wireless Backhaul Can Ease Transition To Fibre - SenzaFiliConsultingDocument11 paginiWireless Backhaul Can Ease Transition To Fibre - SenzaFiliConsultinghaidine_DDBonnÎncă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Planning & Construction of LTE Networks - Ucell - 8Document33 paginiPlanning & Construction of LTE Networks - Ucell - 8haidine_DDBonnÎncă nu există evaluări

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- CELTIC Initiative "Telecommunication Solutions" - Celtic Commune d5 1 FinalDocument59 paginiCELTIC Initiative "Telecommunication Solutions" - Celtic Commune d5 1 Finalhaidine_DDBonnÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- KauppinenDocument10 paginiKauppinenamalthejusÎncă nu există evaluări

- Capesso Symena LTE Network DesignDocument18 paginiCapesso Symena LTE Network Designhaidine_DDBonnÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Frequency Assignment and Mathematics For Comm SystemsDocument63 paginiFrequency Assignment and Mathematics For Comm Systemshaidine_DDBonnÎncă nu există evaluări

- A Broadband Network Cost ModelDocument22 paginiA Broadband Network Cost Modelhaidine_DDBonnÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Building A Next-Generation Mobile Operator BusinessDocument22 paginiBuilding A Next-Generation Mobile Operator Businesshaidine_DDBonnÎncă nu există evaluări

- Lecture2 - Network Design and SecurityDocument27 paginiLecture2 - Network Design and Securityhaidine_DDBonnÎncă nu există evaluări

- LS For Resource Constrained Assignment ProblemDocument17 paginiLS For Resource Constrained Assignment Problemhaidine_DDBonnÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Wireless Services Catalog 2013Document32 paginiWireless Services Catalog 2013haidine_DDBonnÎncă nu există evaluări

- 4G Mobile Broadband Evolution-Rel 10 Rel 11 and Beyond October 2012 PDFDocument234 pagini4G Mobile Broadband Evolution-Rel 10 Rel 11 and Beyond October 2012 PDFKike Vergara PalmaÎncă nu există evaluări

- File To UploadDocument8 paginiFile To Uploadhaidine_DDBonnÎncă nu există evaluări

- Kopie Von Giving An Oral PresentationDocument1 paginăKopie Von Giving An Oral Presentationhaidine_DDBonnÎncă nu există evaluări

- Network Desgin Part1Document13 paginiNetwork Desgin Part1Thomas GarzaÎncă nu există evaluări

- Chapter 5 Network Planning Wireless CDMADocument42 paginiChapter 5 Network Planning Wireless CDMAhaidine_DDBonnÎncă nu există evaluări

- Upload Data ManagementDocument1 paginăUpload Data Managementhaidine_DDBonnÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- EC Mandate M441 - Smart Metering StandardsDocument4 paginiEC Mandate M441 - Smart Metering Standardshaidine_DDBonnÎncă nu există evaluări

- ALCATEL Onetouch 2005 2005d Quick Guide EnglishDocument2 paginiALCATEL Onetouch 2005 2005d Quick Guide EnglishSrdjan StefanovÎncă nu există evaluări

- MSC AerospaceDocument4 paginiMSC AerospaceskhurramqÎncă nu există evaluări

- Manuale RDC - ENDocument45 paginiManuale RDC - ENYiannis SteletarisÎncă nu există evaluări

- Business Analytics and Big Data OutlineDocument4 paginiBusiness Analytics and Big Data OutlineCream FamilyÎncă nu există evaluări

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 paginăTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Sharp CutsÎncă nu există evaluări

- Carle e Montanari at Ipack Ima - GB PDFDocument2 paginiCarle e Montanari at Ipack Ima - GB PDFRolyBernalÎncă nu există evaluări

- Complete 11 KV Assemblies Final 01-2016Document70 paginiComplete 11 KV Assemblies Final 01-2016zararÎncă nu există evaluări

- NS Lab ManualDocument11 paginiNS Lab ManualBonny PrajapatiÎncă nu există evaluări

- Ncode Designlife BrochureDocument4 paginiNcode Designlife BrochuredelaneylukeÎncă nu există evaluări

- Discrete MathDocument1 paginăDiscrete MathAngelo John R. JavinezÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Business Growth and Strategy Project FinalDocument59 paginiBusiness Growth and Strategy Project FinalSonali AgrawalÎncă nu există evaluări

- Compendio Académico UNI Álgebra-LumbrerasDocument320 paginiCompendio Académico UNI Álgebra-LumbrerasmagnoliaÎncă nu există evaluări

- Monitor Acer 7254E DELL E550Document30 paginiMonitor Acer 7254E DELL E550José Luis Sánchez DíazÎncă nu există evaluări

- LSE400S Tutorial 1Document1 paginăLSE400S Tutorial 1Willy K. Ng'etichÎncă nu există evaluări

- Lectra Fashion Brochure - pdf898Document8 paginiLectra Fashion Brochure - pdf898Kanti ModhwadiaÎncă nu există evaluări

- Mine Blast AlgorithmDocument21 paginiMine Blast Algorithmnarottam jangirÎncă nu există evaluări

- Android Enterprise Security Paper 2023Document70 paginiAndroid Enterprise Security Paper 2023caroco8182Încă nu există evaluări

- Course Details Telugu TestingDocument6 paginiCourse Details Telugu TestingMadhukar PatelÎncă nu există evaluări

- 6 Matrix Chain M UltiplicationDocument19 pagini6 Matrix Chain M UltiplicationArslan Ahmed DanishÎncă nu există evaluări

- Journal Citation Reports: Powered by Web of ScienceDocument4 paginiJournal Citation Reports: Powered by Web of ScienceMaaz AlamÎncă nu există evaluări

- Principles of Forensic PhotographyDocument57 paginiPrinciples of Forensic PhotographymiltonÎncă nu există evaluări

- Smash Up RulebookDocument12 paginiSmash Up RulebookRobert MilesÎncă nu există evaluări

- Neration of Various SignalsDocument5 paginiNeration of Various SignalsPREMKUMAR JOHNÎncă nu există evaluări

- Synopsys Tutorial v11 PDFDocument64 paginiSynopsys Tutorial v11 PDFJinu M GeorgeÎncă nu există evaluări

- BitcoinDocument2 paginiBitcoinnonsme2Încă nu există evaluări

- CP2600-OP, A20 DS 1-0-2 (Cat12 CPE)Document2 paginiCP2600-OP, A20 DS 1-0-2 (Cat12 CPE)hrga hrgaÎncă nu există evaluări

- Search Requests and Query My Hidden VideosDocument26 paginiSearch Requests and Query My Hidden VideosEMILY BASSÎncă nu există evaluări

- Presented By:-: Temperature Controlled DC FanDocument19 paginiPresented By:-: Temperature Controlled DC FanAkash HalliÎncă nu există evaluări

- JCMONDocument5 paginiJCMONDevender5194Încă nu există evaluări

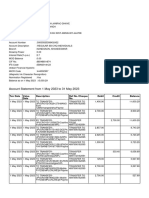

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 paginiAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027Încă nu există evaluări

- The Digital Marketing Handbook: A Step-By-Step Guide to Creating Websites That SellDe la EverandThe Digital Marketing Handbook: A Step-By-Step Guide to Creating Websites That SellEvaluare: 5 din 5 stele5/5 (6)

- Defensive Cyber Mastery: Expert Strategies for Unbeatable Personal and Business SecurityDe la EverandDefensive Cyber Mastery: Expert Strategies for Unbeatable Personal and Business SecurityEvaluare: 5 din 5 stele5/5 (1)

- The Internet Con: How to Seize the Means of ComputationDe la EverandThe Internet Con: How to Seize the Means of ComputationEvaluare: 5 din 5 stele5/5 (6)

- Grokking Algorithms: An illustrated guide for programmers and other curious peopleDe la EverandGrokking Algorithms: An illustrated guide for programmers and other curious peopleEvaluare: 4 din 5 stele4/5 (16)

- The Designer’s Guide to Figma: Master Prototyping, Collaboration, Handoff, and WorkflowDe la EverandThe Designer’s Guide to Figma: Master Prototyping, Collaboration, Handoff, and WorkflowÎncă nu există evaluări

- More Porn - Faster!: 50 Tips & Tools for Faster and More Efficient Porn BrowsingDe la EverandMore Porn - Faster!: 50 Tips & Tools for Faster and More Efficient Porn BrowsingEvaluare: 3.5 din 5 stele3.5/5 (24)