S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- New Management AKDocument282 paginiNew Management AKKhalid Aziz50% (2)

- Level III of CFA Program Mock Exam 3 June, 2019 Revision 1Document65 paginiLevel III of CFA Program Mock Exam 3 June, 2019 Revision 1Yohan CruzÎncă nu există evaluări

- Syllabus of M.A. Eco KUDocument12 paginiSyllabus of M.A. Eco KUPlatonicÎncă nu există evaluări

- Specimen AccountsDocument12 paginiSpecimen AccountsPlatonicÎncă nu există evaluări

- Past Examination Papers M.A. Eco PUDocument5 paginiPast Examination Papers M.A. Eco PUPlatonicÎncă nu există evaluări

- Karachi - A Picture BookDocument280 paginiKarachi - A Picture BookPlatonicÎncă nu există evaluări

- Life of Waheed Murad (In Urdu)Document48 paginiLife of Waheed Murad (In Urdu)Platonic0% (1)

- Study & Examination SkillsDocument29 paginiStudy & Examination SkillsPlatonicÎncă nu există evaluări

- Waheed Murad Urdu Article by Fareed Ashraf GhaziDocument4 paginiWaheed Murad Urdu Article by Fareed Ashraf GhaziPlatonicÎncă nu există evaluări

- Salma and Waheed MuradDocument3 paginiSalma and Waheed MuradPlatonicÎncă nu există evaluări

- Reading For Study - CIPFADocument25 paginiReading For Study - CIPFAPlatonicÎncă nu există evaluări

- Life of Waheed Murad (In English)Document36 paginiLife of Waheed Murad (In English)PlatonicÎncă nu există evaluări

- Online Accounting TutorialDocument140 paginiOnline Accounting TutorialPlatonic100% (1)

- Specimen of Share CertificateDocument3 paginiSpecimen of Share CertificatePlatonic33% (3)

- Stress Management - CIPFADocument22 paginiStress Management - CIPFAPlatonicÎncă nu există evaluări

- ACCA Advanced Corporate Reporting 2001Document79 paginiACCA Advanced Corporate Reporting 2001PlatonicÎncă nu există evaluări

- Time Management - CIPFADocument26 paginiTime Management - CIPFAPlatonicÎncă nu există evaluări

- ACCA Advanced Corporate Reporting 2005Document763 paginiACCA Advanced Corporate Reporting 2005Platonic100% (2)

- Companies Rules Volume IVDocument561 paginiCompanies Rules Volume IVPlatonicÎncă nu există evaluări

- Learning Styles - CIPFADocument28 paginiLearning Styles - CIPFAPlatonicÎncă nu există evaluări

- Business LawDocument529 paginiBusiness LawPlatonicÎncă nu există evaluări

- Classroom Atlas by Rand McNallyDocument103 paginiClassroom Atlas by Rand McNallyPlatonicÎncă nu există evaluări

- Brewer Dictionary of Phrase & FablesDocument2.411 paginiBrewer Dictionary of Phrase & FablesPlatonicÎncă nu există evaluări

- Companies Rules Volume VDocument699 paginiCompanies Rules Volume VPlatonicÎncă nu există evaluări

- Companies Rules Volume IIIDocument413 paginiCompanies Rules Volume IIIPlatonicÎncă nu există evaluări

- Important Problems in AccountingDocument225 paginiImportant Problems in AccountingPlatonic100% (3)

- Companies Rules Volume VIDocument473 paginiCompanies Rules Volume VIPlatonicÎncă nu există evaluări

- Companies Ordinance, 1984Document423 paginiCompanies Ordinance, 1984PlatonicÎncă nu există evaluări

- Companies Rules Volume IIDocument585 paginiCompanies Rules Volume IIPlatonicÎncă nu există evaluări

- Companies Ordinance 1984Document421 paginiCompanies Ordinance 1984PlatonicÎncă nu există evaluări

- Companies Rules Volume IDocument503 paginiCompanies Rules Volume IPlatonicÎncă nu există evaluări

- Customer Management Procedure A Study On Some Private Commercial Banks of BangladeshDocument118 paginiCustomer Management Procedure A Study On Some Private Commercial Banks of BangladeshSharifMahmudÎncă nu există evaluări

- Business Owner TGV Factsheet Jun 19Document1 paginăBusiness Owner TGV Factsheet Jun 19Abdullah18Încă nu există evaluări

- Module 13 - BusCom - Forex. - StudentsDocument13 paginiModule 13 - BusCom - Forex. - StudentsLuisito CorreaÎncă nu există evaluări

- Understanding Bank Credit AnalysisDocument116 paginiUnderstanding Bank Credit AnalysisSekar Murugan100% (2)

- Luxury Housing Development in Ethiopia's CapitalDocument13 paginiLuxury Housing Development in Ethiopia's CapitalDawit Solomon67% (3)

- Economic Policy 1991Document20 paginiEconomic Policy 1991Anusha Palakurthy100% (1)

- Accounting Standards For Deferred TaxDocument17 paginiAccounting Standards For Deferred TaxRishi AgnihotriÎncă nu există evaluări

- Index Investing & Financial Independence For Expats: Getting Started GuideDocument54 paginiIndex Investing & Financial Independence For Expats: Getting Started GuideAmr Mustafa ToradÎncă nu există evaluări

- LOI - Shipper & ConsigneeDocument2 paginiLOI - Shipper & ConsigneeFelipe Arango100% (1)

- Xi - Accounting: PrivateDocument15 paginiXi - Accounting: PrivateAdnan SajidÎncă nu există evaluări

- IAS 38 Summary - Accounting for Intangible AssetsDocument6 paginiIAS 38 Summary - Accounting for Intangible AssetsRey Jr AlipisÎncă nu există evaluări

- Profitero On March With 9m War Chest - Ireland - The Sunday TimesDocument4 paginiProfitero On March With 9m War Chest - Ireland - The Sunday TimesVladÎncă nu există evaluări

- University of CebuDocument5 paginiUniversity of CebuLouelie Jean AlfornonÎncă nu există evaluări

- Ratio Alalysis Jersey ProjectDocument64 paginiRatio Alalysis Jersey ProjectAnonymous 22GBLsme1Încă nu există evaluări

- Authority To Negotiate and Offer To SellDocument6 paginiAuthority To Negotiate and Offer To SellKeekay Palacio100% (1)

- Confrontation With The Banking CartelTwitter3.23.19Document24 paginiConfrontation With The Banking CartelTwitter3.23.19karen hudes100% (1)

- Accounting Under Ideal ConditionDocument53 paginiAccounting Under Ideal ConditionHideoYoshidaÎncă nu există evaluări

- Adv 1 - 6 - Intercompany Profit Transactions - Plant Assets - Handout #1Document12 paginiAdv 1 - 6 - Intercompany Profit Transactions - Plant Assets - Handout #1ria fransiscaieÎncă nu există evaluări

- BAR Exam Taxation Questions 1994-2006 by TopicDocument86 paginiBAR Exam Taxation Questions 1994-2006 by TopicNoel Alberto OmandapÎncă nu există evaluări

- A Report On Business Plan of Birishiri Resort ProjectDocument50 paginiA Report On Business Plan of Birishiri Resort ProjectJahed Nil100% (4)

- Turn Around Strategy of Air IndiaDocument33 paginiTurn Around Strategy of Air IndiaUvesh MevawalaÎncă nu există evaluări

- ABM - Fundamentals of ABM 2 CGDocument6 paginiABM - Fundamentals of ABM 2 CGKassandra KayÎncă nu există evaluări

- Fina 2360 Fall 2015 Fall Midterm KeyDocument19 paginiFina 2360 Fall 2015 Fall Midterm KeyShafkat RezaÎncă nu există evaluări

- Putting Intelligent Insights To WorkDocument12 paginiPutting Intelligent Insights To WorkDeloitte Analytics100% (1)

- Lecture 10 - Prospective Analysis - ForecastingDocument15 paginiLecture 10 - Prospective Analysis - ForecastingTrang Bùi Hà100% (1)

- How To Forecast Markets - A Departing Top JPMorgan Strategist Reveals What He Learned After 30 YearsDocument7 paginiHow To Forecast Markets - A Departing Top JPMorgan Strategist Reveals What He Learned After 30 Yearseliforu100% (1)

- Via E-Mail To Rule-Comments@sec - Gov: ASSOCIATION YEAR 2010-2011 ChairDocument7 paginiVia E-Mail To Rule-Comments@sec - Gov: ASSOCIATION YEAR 2010-2011 ChairMarketsWikiÎncă nu există evaluări

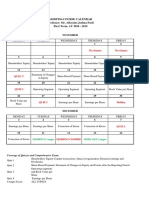

- Modfin4 Course Calendar First Term, AY 2018 - 2019 Professor: Mr. Alloysius Joshua ParilDocument1 paginăModfin4 Course Calendar First Term, AY 2018 - 2019 Professor: Mr. Alloysius Joshua ParilRedÎncă nu există evaluări

- Tea Blending Unit: Profile No.: 58 NIC Code: 10791Document6 paginiTea Blending Unit: Profile No.: 58 NIC Code: 10791P Agarwal0% (1)