S-ar putea să vă placă și

- ADR Aribitrage Opportunities For DummiesDocument29 paginiADR Aribitrage Opportunities For DummiesEd McManus100% (1)

- Final Paper RDDocument16 paginiFinal Paper RDapi-253561960Încă nu există evaluări

- The New York Stock Exchange and Public Opinion Remarks at Annual Dinner, Association of Stock Exchange Brokers, Held at the Astor Hotel, New York, January 24, 1917De la EverandThe New York Stock Exchange and Public Opinion Remarks at Annual Dinner, Association of Stock Exchange Brokers, Held at the Astor Hotel, New York, January 24, 1917Încă nu există evaluări

- Celebration at The: See Interview This MagazineDocument5 paginiCelebration at The: See Interview This MagazineSam SamÎncă nu există evaluări

- Freedom of Contracts-Emerging IssuesDocument22 paginiFreedom of Contracts-Emerging Issuesyashvardhan guptaÎncă nu există evaluări

- The Meaning of MoneyDocument6 paginiThe Meaning of MoneyChristopher Michael Quigley100% (1)

- Gocardless Direct Debit GuideDocument53 paginiGocardless Direct Debit GuideGregory CarterÎncă nu există evaluări

- Zeitgeist: Addendum: The Final CutDocument18 paginiZeitgeist: Addendum: The Final CutTimothyÎncă nu există evaluări

- Fiction of LawDocument8 paginiFiction of LawFukyiro PinionÎncă nu există evaluări

- TA GlossaryDocument8 paginiTA GlossaryJJÎncă nu există evaluări

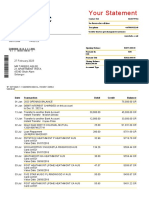

- 1 This First Bank: Sample Account Statement and BalancingDocument2 pagini1 This First Bank: Sample Account Statement and BalancingQuenie De la CruzÎncă nu există evaluări

- Capital Accumalation and Wealth Building Index - PHPDocument278 paginiCapital Accumalation and Wealth Building Index - PHPGeorge Bailey50% (2)

- Corporate Finance in LawDocument19 paginiCorporate Finance in LawcmtinvÎncă nu există evaluări

- Disposal of Unserviceable AssetsDocument6 paginiDisposal of Unserviceable AssetsJOHAYNIEÎncă nu există evaluări

- Maxim Prohibited Directly Also Indirectly TreatiesDocument533 paginiMaxim Prohibited Directly Also Indirectly TreatiesKevin HaddockÎncă nu există evaluări

- Simon Cash Machine1Document12 paginiSimon Cash Machine1TerryÎncă nu există evaluări

- Nepotism in The Arab World An Institutional Theory PerspectiveDocument29 paginiNepotism in The Arab World An Institutional Theory PerspectiveElena SanduÎncă nu există evaluări

- Oath of OfficeDocument2 paginiOath of OfficeDavidSDekalbÎncă nu există evaluări

- Day Saints, Which I Have Just Discovered Was Written by Charles Mackay, Because We NowDocument88 paginiDay Saints, Which I Have Just Discovered Was Written by Charles Mackay, Because We NowHoward HillÎncă nu există evaluări

- Key Financial Terms and RatiosDocument16 paginiKey Financial Terms and RatiosShravan KumarÎncă nu există evaluări

- Mcq's MergedDocument720 paginiMcq's MergedPruthil MonpariyaÎncă nu există evaluări

- High Probability Chart Reading John Murphy PDFDocument4 paginiHigh Probability Chart Reading John Murphy PDFomarÎncă nu există evaluări

- The Philatelic AtlasDocument190 paginiThe Philatelic AtlasVictor UribeÎncă nu există evaluări

- Nison Trading PrinciplesDocument1 paginăNison Trading PrinciplesLUCKY CHOPRAÎncă nu există evaluări

- Cuius Est SolumDocument1 paginăCuius Est SolumowinohÎncă nu există evaluări

- Dirty Little Secrets of Your 401(K): What the “big Money Boys” Don’t Want You to KnowDe la EverandDirty Little Secrets of Your 401(K): What the “big Money Boys” Don’t Want You to KnowÎncă nu există evaluări

- SHILLER, Robert J. (1984) Stock Prices and Social DynamicsDocument54 paginiSHILLER, Robert J. (1984) Stock Prices and Social DynamicsDouglas de Medeiros FrancoÎncă nu există evaluări

- John Coates The Hour Between Dogand Wolf 269Document25 paginiJohn Coates The Hour Between Dogand Wolf 269hakan hamidÎncă nu există evaluări

- Good ThingsDocument16 paginiGood ThingsculwavesÎncă nu există evaluări

- LTDDocument3 paginiLTDAustine CamposÎncă nu există evaluări

- Series34 PrepDocument45 paginiSeries34 PrepaudifferensÎncă nu există evaluări

- 6446 The Netherlands Guide PDFDocument8 pagini6446 The Netherlands Guide PDFYakob BudimanÎncă nu există evaluări

- Bank Class Action Media ReleaseDocument2 paginiBank Class Action Media ReleaseJohn@spiritusÎncă nu există evaluări

- Release Waiver and Quitclaim - No Ee-Er RelnshipDocument2 paginiRelease Waiver and Quitclaim - No Ee-Er RelnshipmisyeldvÎncă nu există evaluări

- Dow TheoryDocument4 paginiDow TheoryRamani RajeshÎncă nu există evaluări

- 3 Firm Portfolio ExampleDocument12 pagini3 Firm Portfolio ExampleRudy Martin Bada AlayoÎncă nu există evaluări

- Contracts LawDocument17 paginiContracts LawAnklesh08Încă nu există evaluări

- Chart History of Gold Market - Updated 8.2015Document43 paginiChart History of Gold Market - Updated 8.2015Peter L. BrandtÎncă nu există evaluări

- Solution Manual For Intermediate Accounting IFRS 4th Edition by Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield Chapter 1 - 24Document70 paginiSolution Manual For Intermediate Accounting IFRS 4th Edition by Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield Chapter 1 - 24marcuskenyatta27550% (2)

- Bank Statement TareeqDocument2 paginiBank Statement TareeqIzza NabbilaÎncă nu există evaluări

- Victoria's Secret Annual ReportDocument13 paginiVictoria's Secret Annual Reportapi-373843164% (28)

- Unclaimed Balances LawDocument17 paginiUnclaimed Balances LawFritchel Mae QuicosÎncă nu există evaluări

- Thomas v. PinedaDocument11 paginiThomas v. PinedaylessinÎncă nu există evaluări

- Variant Perception Understanding-VolatilityDocument20 paginiVariant Perception Understanding-VolatilityLinda FreemanÎncă nu există evaluări

- Neuman Double Binds, Triadic Binds PDFDocument14 paginiNeuman Double Binds, Triadic Binds PDFWillem OuweltjesÎncă nu există evaluări

- Strategic Alliance v. Radstock DigestDocument9 paginiStrategic Alliance v. Radstock DigestLeighÎncă nu există evaluări

- Penny Stock PaperDocument41 paginiPenny Stock PaperSerodÎncă nu există evaluări

- Ivan BoeskyDocument2 paginiIvan BoeskySaad ZahidÎncă nu există evaluări

- CH 22Document68 paginiCH 22Aireen TanioÎncă nu există evaluări

- An Anatomy of Trading Strategies: Jennifer ConradDocument31 paginiAn Anatomy of Trading Strategies: Jennifer ConradRicardo NuñezÎncă nu există evaluări

- Permanence: 17th June 2013Document5 paginiPermanence: 17th June 2013tony caputi100% (1)

- Smiths Law of ContractsDocument617 paginiSmiths Law of Contractssastrylanka1980Încă nu există evaluări

- Boogaloo Bois Have Guns and Military Training - and Now They Want To Overthrow The GovernmentDocument11 paginiBoogaloo Bois Have Guns and Military Training - and Now They Want To Overthrow The GovernmentsiesmannÎncă nu există evaluări

- The Missing Risk Premium: Why Low Volatility Investing WorksDocument118 paginiThe Missing Risk Premium: Why Low Volatility Investing WorksMinh NguyenÎncă nu există evaluări

- Julius Evola Race As A Builder of LeadersDocument4 paginiJulius Evola Race As A Builder of LeadersΠΤΟΛΕΜΑΙΟΣ ΗΡΑΚΛΕΙΔΗΣÎncă nu există evaluări

- EuroDollar University Season2 SlideDeckDocument145 paginiEuroDollar University Season2 SlideDeckdsfgdfgdfgÎncă nu există evaluări

- Cryptocurrencies: International Regulation AND Uniformization of PracticesDocument18 paginiCryptocurrencies: International Regulation AND Uniformization of PracticesRizalien Jane BongcayaoÎncă nu există evaluări

- A List of 25 Principles of Adult Behavior by John Perry BarlowDocument2 paginiA List of 25 Principles of Adult Behavior by John Perry BarlowDJSeidel100% (1)

- Constitution CurrentDocument70 paginiConstitution CurrentRafael HelenoÎncă nu există evaluări

- The Boom of 2021Document4 paginiThe Boom of 2021Jeff McGinnÎncă nu există evaluări

- The U.S. Constitution and MoneyDocument491 paginiThe U.S. Constitution and MoneyDumitru ZburleaÎncă nu există evaluări

- Scientology Memoirs by Lisa GibsonDocument15 paginiScientology Memoirs by Lisa GibsonsirjsslutÎncă nu există evaluări

- Book of The LawDocument2 paginiBook of The LawPatan PaulÎncă nu există evaluări

- Astrosophic Principles - J Hazelrigg (1917)Document135 paginiAstrosophic Principles - J Hazelrigg (1917)KoayeÎncă nu există evaluări

- Appleby Guide To International Trusts in SeychellesDocument12 paginiAppleby Guide To International Trusts in SeychellesBianci820% (1)

- SFO Feb11Document96 paginiSFO Feb11AbgreenÎncă nu există evaluări

- ArbitrageDocument8 paginiArbitrageYankey MermelsteinÎncă nu există evaluări

- Scott Locklin - A Bestiary of Algorithmic Trading Strategies Locklin On ScienceDocument13 paginiScott Locklin - A Bestiary of Algorithmic Trading Strategies Locklin On Sciencetedcruz4presidentÎncă nu există evaluări

- D Stephens - A Game ManualDocument100 paginiD Stephens - A Game ManualP OtteÎncă nu există evaluări

- Hacienda Royale Subdivision: San Fernando, PampangaDocument11 paginiHacienda Royale Subdivision: San Fernando, PampangaRenzo GuevarraÎncă nu există evaluări

- Multinational CorporationsDocument26 paginiMultinational CorporationsHarshal ShindeÎncă nu există evaluări

- Comparing The Aicpa Code To The Global StandardDocument6 paginiComparing The Aicpa Code To The Global StandardNoveldaÎncă nu există evaluări

- Wallstreetjournal 20160125 The Wall Street JournalDocument40 paginiWallstreetjournal 20160125 The Wall Street JournalstefanoÎncă nu există evaluări

- Innocents Abroad Currencies and International Stock ReturnsDocument39 paginiInnocents Abroad Currencies and International Stock ReturnsShivaniÎncă nu există evaluări

- Why Marc Faber Is Such A BearDocument6 paginiWhy Marc Faber Is Such A BearrobintanwhÎncă nu există evaluări

- PPE - Initial Measurement - Assignment - No AnswersDocument2 paginiPPE - Initial Measurement - Assignment - No Answersemman neriÎncă nu există evaluări

- Steve Advanced Courses Part 3Document16 paginiSteve Advanced Courses Part 3Manuel NadeauÎncă nu există evaluări

- Petunjuk: Ujian Kompetensi Dasar I Program Pascasarjana Teknik Industri Universitas Sebelas MaretDocument4 paginiPetunjuk: Ujian Kompetensi Dasar I Program Pascasarjana Teknik Industri Universitas Sebelas MaretriadÎncă nu există evaluări

- Supply Side PoliciesDocument5 paginiSupply Side PoliciesVanessa KuaÎncă nu există evaluări

- Lecture 2 Tutorial SoluitionDocument3 paginiLecture 2 Tutorial SoluitionEleanor ChengÎncă nu există evaluări

- 05-30-15 SatDocument32 pagini05-30-15 SatSan Mateo Daily JournalÎncă nu există evaluări

- Case Study On Exchange Rate RiskDocument2 paginiCase Study On Exchange Rate RiskUbaid DarÎncă nu există evaluări

- Answer Sample Problems Cash1-12Document4 paginiAnswer Sample Problems Cash1-12Anonymous wwLoDau1aÎncă nu există evaluări

- 09-PCSO2019 Part2-Observations and RecommDocument40 pagini09-PCSO2019 Part2-Observations and RecommdemosreaÎncă nu există evaluări

- Money - Time Relationships and Equivalence: Name of Student/s: Dickinson, Sigienel Gabriel, Neil Patrick ADocument12 paginiMoney - Time Relationships and Equivalence: Name of Student/s: Dickinson, Sigienel Gabriel, Neil Patrick ASasuke UchichaÎncă nu există evaluări

- Tambunting v. CADocument9 paginiTambunting v. CAAlex FelicesÎncă nu există evaluări