S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

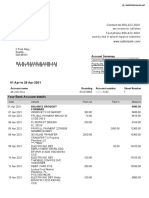

- Sutton Bank StatementDocument2 paginiSutton Bank StatementNadiia AvetisianÎncă nu există evaluări

- Airbus A3XX: Developing The World's Largest Commercial JetDocument31 paginiAirbus A3XX: Developing The World's Largest Commercial JetRishi Bajaj100% (1)

- Market Visit Ing ReportDocument3 paginiMarket Visit Ing ReportMr. JahirÎncă nu există evaluări

- Garuda Indonesia Vs Others, Winning The Price WarDocument16 paginiGaruda Indonesia Vs Others, Winning The Price Waryandhie570% (1)

- Updated PJBF PresentationDocument16 paginiUpdated PJBF PresentationMuhammad FaisalÎncă nu există evaluări

- Tata Vistara - Agency PitchDocument27 paginiTata Vistara - Agency PitchNishant Prakash0% (1)

- Special Economic ZoneDocument7 paginiSpecial Economic ZoneAnonymous cRMw8feac8Încă nu există evaluări

- Eco Sem 6 Course Outline 2022-23Document4 paginiEco Sem 6 Course Outline 2022-23Hetvi ShahÎncă nu există evaluări

- Financial AnalysisDocument2 paginiFinancial AnalysisDemi Jamie LaygoÎncă nu există evaluări

- KONTRAK KERJA 2 BahasaDocument12 paginiKONTRAK KERJA 2 BahasaStanley RusliÎncă nu există evaluări

- AP Macro 2008 Audit VersionDocument24 paginiAP Macro 2008 Audit Versionvi ViÎncă nu există evaluări

- TYS 2007 To 2019 AnswersDocument380 paginiTYS 2007 To 2019 Answersshakthee sivakumarÎncă nu există evaluări

- BANK 3009 CVRM Workshop 1 ExercisesDocument3 paginiBANK 3009 CVRM Workshop 1 Exercisesjon PalÎncă nu există evaluări

- Five Year PlanDocument5 paginiFive Year PlanrakshaksinghaiÎncă nu există evaluări

- Annexure - VI Deed of Hypothecation (To Be Executed On Non Judicial Stamp Paper of Appropriate Value)Document3 paginiAnnexure - VI Deed of Hypothecation (To Be Executed On Non Judicial Stamp Paper of Appropriate Value)Deepesh MittalÎncă nu există evaluări

- Management Control System: Session 8 Budget Preparation OCTOBER 15, 2012 Jakarta, IndonesiaDocument31 paginiManagement Control System: Session 8 Budget Preparation OCTOBER 15, 2012 Jakarta, IndonesiaLinda TanÎncă nu există evaluări

- The Simple Keynesian ModelDocument9 paginiThe Simple Keynesian ModelRudraraj MalikÎncă nu există evaluări

- BioplasticDocument5 paginiBioplasticclaire bernadaÎncă nu există evaluări

- S.B. No. 824: First Regular SessionDocument5 paginiS.B. No. 824: First Regular SessionKevin TayagÎncă nu există evaluări

- UAS MS NathanaelCahya 115190307Document2 paginiUAS MS NathanaelCahya 115190307Nathanael CahyaÎncă nu există evaluări

- Terms and Conditions of Carriage enDocument32 paginiTerms and Conditions of Carriage enMuhammad AsifÎncă nu există evaluări

- Property Location Within Abroa D Within Outside Withi N Outside Real Properties X X Personal Properties Tangible X X Intangible X X XDocument4 paginiProperty Location Within Abroa D Within Outside Withi N Outside Real Properties X X Personal Properties Tangible X X Intangible X X XMarie Tes LocsinÎncă nu există evaluări

- San Clemente VillagesDocument2 paginiSan Clemente VillagesHarichandan PÎncă nu există evaluări

- Understanding EntrepreneurshipDocument277 paginiUnderstanding Entrepreneurshiphannaatnafu100% (1)

- Levels ReactingDocument17 paginiLevels Reactingvlad_adrian_775% (8)

- QM - Chapter 4 (MCQ'S)Document15 paginiQM - Chapter 4 (MCQ'S)arslanÎncă nu există evaluări

- Awnser KeyDocument3 paginiAwnser KeyChristopher FulbrightÎncă nu există evaluări

- HR PoliciesDocument129 paginiHR PoliciesAjeet ThounaojamÎncă nu există evaluări

- Folder Gründen in Wien Englisch Web 6-10-17Document6 paginiFolder Gründen in Wien Englisch Web 6-10-17rodicabaltaÎncă nu există evaluări

- Chapter 6-Household BehaviorDocument19 paginiChapter 6-Household BehaviorJAGATHESANÎncă nu există evaluări