S-ar putea să vă placă și

- Chart of Entity ComparisonDocument4 paginiChart of Entity ComparisonDee BeldÎncă nu există evaluări

- Agency and Partnership GuideDocument3 paginiAgency and Partnership GuidetoddmbakerÎncă nu există evaluări

- Closely Held Business Org and Agency DutiesDocument85 paginiClosely Held Business Org and Agency DutiesnabarrowÎncă nu există evaluări

- Business OrganizationsDocument71 paginiBusiness Organizationsjdadas100% (2)

- Community Property Final Outline - ADDocument62 paginiCommunity Property Final Outline - ADAlexandra DelatorreÎncă nu există evaluări

- Corporations OutlineDocument35 paginiCorporations OutlineSteve AdamsonÎncă nu există evaluări

- BA Outline - OKellyDocument69 paginiBA Outline - OKellylshahÎncă nu există evaluări

- 2 - BA Attack OutlineDocument41 pagini2 - BA Attack OutlineJenna AliaÎncă nu există evaluări

- BA - FreerDocument121 paginiBA - FreerEugene Yanul100% (1)

- Business Organizations OutlineDocument71 paginiBusiness Organizations Outlineesquire2014fl100% (3)

- Business Associations Agency OutlineDocument43 paginiBusiness Associations Agency OutlineLarry Rogers100% (2)

- Business Organizations - Agency and AuthorityDocument65 paginiBusiness Organizations - Agency and AuthorityNas YasinÎncă nu există evaluări

- Community Property Outline-SUMMARYDocument7 paginiCommunity Property Outline-SUMMARYfredtv100% (1)

- Corporations Outline Partnoy PalmiterDocument20 paginiCorporations Outline Partnoy PalmiterMatt ToothacreÎncă nu există evaluări

- Checklist PRDocument8 paginiChecklist PRDouglas GromackÎncă nu există evaluări

- FlowchartsDocument6 paginiFlowchartsesanchezfloat100% (1)

- Professional Responsibilities LawyerDocument3 paginiProfessional Responsibilities LawyerRooter CoxÎncă nu există evaluări

- Agency and Business Organization DutiesDocument5 paginiAgency and Business Organization DutiesSam Hughes100% (1)

- Business Associations - Template 2 (Australia)Document14 paginiBusiness Associations - Template 2 (Australia)Marten NguyenÎncă nu există evaluări

- Business Associations Spring 2003 Grimes: QuestionsDocument70 paginiBusiness Associations Spring 2003 Grimes: QuestionsCelebSightings100% (1)

- Remedies Outline CutDocument2 paginiRemedies Outline CutErica Chavez100% (1)

- Business Associations Attack OutlineDocument65 paginiBusiness Associations Attack OutlineWaylon Fields86% (7)

- BA Outline - FinalDocument32 paginiBA Outline - FinalNathan Yost100% (1)

- Business Associations OutlineDocument30 paginiBusiness Associations OutlineClaudia GalanÎncă nu există evaluări

- Choose Business Structure & Tax TreatmentDocument74 paginiChoose Business Structure & Tax TreatmentRonnie Barcena Jr.Încă nu există evaluări

- Business Associations OutlineDocument36 paginiBusiness Associations OutlineAlex StratasÎncă nu există evaluări

- Agency and Partnership BasicsDocument27 paginiAgency and Partnership BasicsRory FarrellÎncă nu există evaluări

- Agency Relationships & LiabilityDocument75 paginiAgency Relationships & LiabilityjryanandersonÎncă nu există evaluări

- Federal Income Tax (Wells)Document30 paginiFederal Income Tax (Wells)Bear100% (2)

- Wills and Estates Cheat Sheet: by ViaDocument4 paginiWills and Estates Cheat Sheet: by ViaMartin LaiÎncă nu există evaluări

- Negligence, Intentional Torts, and Property Damage ExplainedDocument2 paginiNegligence, Intentional Torts, and Property Damage Explaineddeenydoll4125Încă nu există evaluări

- Business Associations Outline - Klein, 3rd EdDocument75 paginiBusiness Associations Outline - Klein, 3rd Edjanklewich100% (2)

- Corporations Bar OutlineDocument4 paginiCorporations Bar OutlineJohn RisvoldÎncă nu există evaluări

- BUSINESS ASSOCIATIONS OUTLINEDocument117 paginiBUSINESS ASSOCIATIONS OUTLINEDarren Christman100% (1)

- PR OutlineDocument34 paginiPR OutlineroseyboppÎncă nu există evaluări

- Business Organization Chart AssignmentDocument4 paginiBusiness Organization Chart AssignmentTosha BrownÎncă nu există evaluări

- Flowchart - Negligence (Occupier's Liability) : Issue 1: Did The Defendant Owe The Plaintiff A Duty of Care?Document4 paginiFlowchart - Negligence (Occupier's Liability) : Issue 1: Did The Defendant Owe The Plaintiff A Duty of Care?NDÎncă nu există evaluări

- Intro: Legal Knowledge Skill Thoroughness PreparationDocument2 paginiIntro: Legal Knowledge Skill Thoroughness PreparationHaifaÎncă nu există evaluări

- BA OutlineDocument17 paginiBA OutlineCarrie AndersonÎncă nu există evaluări

- Business Associations Outline: Agency Law and LiabilitiesDocument75 paginiBusiness Associations Outline: Agency Law and LiabilitiesMissy Meyer100% (1)

- I. Who Is An Agent?: Gorton v. Doty (1937)Document109 paginiI. Who Is An Agent?: Gorton v. Doty (1937)Erick VelizÎncă nu există evaluări

- BusOrgTemplates 1 2Document48 paginiBusOrgTemplates 1 2Sam Hughes100% (1)

- Acing BA OutlineDocument64 paginiAcing BA OutlineStephanie PayanoÎncă nu există evaluări

- Corporation Law Flow Chart (MBCADocument1 paginăCorporation Law Flow Chart (MBCAMegan Lindsay Ruffin100% (4)

- When Does the UCC Apply? – Key Factors and TestsDocument49 paginiWhen Does the UCC Apply? – Key Factors and TestsLaura C100% (1)

- Business Organizations OutlineDocument29 paginiBusiness Organizations OutlineMissy Meyer100% (1)

- Property Attack Outline Eslund Spring 2011Document22 paginiProperty Attack Outline Eslund Spring 2011Patricia Torres TorresÎncă nu există evaluări

- Final Civil Procedure Outline!Document7 paginiFinal Civil Procedure Outline!Kate BroderickÎncă nu există evaluări

- Corporations Agency PartnershipDocument61 paginiCorporations Agency PartnershipDan StewartÎncă nu există evaluări

- Torts 1 Rule StatementsDocument8 paginiTorts 1 Rule StatementsNija Anise Bastfield100% (3)

- Partnership Formation and RightsDocument4 paginiPartnership Formation and Rightsalexander100% (2)

- Forming a Corporation and Understanding Corporate StructureDocument7 paginiForming a Corporation and Understanding Corporate StructureParker BushÎncă nu există evaluări

- PR ChecklistDocument4 paginiPR Checklistjm9887100% (1)

- Corps - Clarke - Short OutlineDocument14 paginiCorps - Clarke - Short OutlineLal LegalÎncă nu există evaluări

- Real Covenants vs. Equitable ServitudesDocument1 paginăReal Covenants vs. Equitable ServitudesJeffrey StevensonÎncă nu există evaluări

- Contracts Mnemonics and Definitions: Mnemonics, #2De la EverandContracts Mnemonics and Definitions: Mnemonics, #2Încă nu există evaluări

- Business Structure Comparison Chart: Document 1109ADocument3 paginiBusiness Structure Comparison Chart: Document 1109ASameera Sri VidurangaÎncă nu există evaluări

- Guide to Starting a Business in the PhilippinesDocument6 paginiGuide to Starting a Business in the PhilippinesLoue CommsÎncă nu există evaluări

- DLA Piper Guide To Going Global Corporate United StatesDocument15 paginiDLA Piper Guide To Going Global Corporate United StatesGarima JainÎncă nu există evaluări

- 2020 Guide to Small Business Tax PlanningDe la Everand2020 Guide to Small Business Tax PlanningÎncă nu există evaluări

- Short Form LLC Member Admission AgreementDocument3 paginiShort Form LLC Member Admission AgreementJPF100% (3)

- Comprehensive Agreement Between Companies To Preserve Trade Secrets While Discussing Possible Transaction Between ThemDocument4 paginiComprehensive Agreement Between Companies To Preserve Trade Secrets While Discussing Possible Transaction Between ThemJPFÎncă nu există evaluări

- Purchase Order Short FormDocument4 paginiPurchase Order Short FormJPFÎncă nu există evaluări

- Preferred Stock Purchase AgreementDocument18 paginiPreferred Stock Purchase AgreementJPFÎncă nu există evaluări

- Security Agreement All Assets of Personal PropertyDocument17 paginiSecurity Agreement All Assets of Personal PropertyJPF100% (6)

- Investment AgreementDocument42 paginiInvestment AgreementJPFÎncă nu există evaluări

- New Corporation QuestionaireDocument25 paginiNew Corporation QuestionaireJPFÎncă nu există evaluări

- Sale of All Assets of LLCDocument12 paginiSale of All Assets of LLCJPFÎncă nu există evaluări

- Private Placement QuestionaireDocument27 paginiPrivate Placement QuestionaireJPFÎncă nu există evaluări

- Intellectual Property Asset AcqusitionDocument7 paginiIntellectual Property Asset AcqusitionJPFÎncă nu există evaluări

- Redemption and Termination AgreementDocument4 paginiRedemption and Termination AgreementJPFÎncă nu există evaluări

- Termination Agreement - General Form.: (Signature of Employee)Document1 paginăTermination Agreement - General Form.: (Signature of Employee)JPFÎncă nu există evaluări

- Option To Purchase AssetsDocument3 paginiOption To Purchase AssetsJPFÎncă nu există evaluări

- Telecomuting AgreementDocument2 paginiTelecomuting AgreementJPFÎncă nu există evaluări

- Landscape AgreementDocument5 paginiLandscape AgreementJPFÎncă nu există evaluări

- Partnershi Conv To LLC AgrtDocument2 paginiPartnershi Conv To LLC AgrtJPFÎncă nu există evaluări

- Fernandes Firm Minute BookDocument8 paginiFernandes Firm Minute BookJPFÎncă nu există evaluări

- Choice of Entity For ScribdDocument8 paginiChoice of Entity For ScribdJPFÎncă nu există evaluări

- Fernandes Law Private Placement Client MemoDocument9 paginiFernandes Law Private Placement Client MemoJPFÎncă nu există evaluări

- LLC Memo For Client CompleteDocument4 paginiLLC Memo For Client CompleteJPF100% (1)

- Form: Distribution Agreement With CommentaryDocument15 paginiForm: Distribution Agreement With CommentaryJPF100% (1)

- Asset Protection PlanDocument36 paginiAsset Protection PlanJPF100% (2)

- Mutual Confi AgrtDocument4 paginiMutual Confi AgrtJPFÎncă nu există evaluări

- Angel Investing Basic Captial StructureDocument1 paginăAngel Investing Basic Captial StructureJPFÎncă nu există evaluări

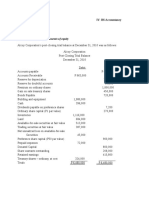

- Accounting For CorporationsDocument2 paginiAccounting For CorporationsMaila LoquincioÎncă nu există evaluări

- SBEC Q&A - Part-ADocument164 paginiSBEC Q&A - Part-AMohammad ZaynÎncă nu există evaluări

- Guide to Incorporating a CompanyDocument11 paginiGuide to Incorporating a CompanyAparna JaymohanÎncă nu există evaluări

- Corpo Reviewer MidtermsDocument10 paginiCorpo Reviewer MidtermscrisÎncă nu există evaluări

- Declaration Form For Non-Individual Account Opening - V2 - FinalDocument2 paginiDeclaration Form For Non-Individual Account Opening - V2 - FinalAhleescia LyisÎncă nu există evaluări

- Company Management: Appointment of Directors Under Companies Act 2013Document21 paginiCompany Management: Appointment of Directors Under Companies Act 2013RAVI RAUSHAN JHAÎncă nu există evaluări

- Legal AspectDocument12 paginiLegal AspectVhin BaldonÎncă nu există evaluări

- LLP AssignmentDocument17 paginiLLP Assignmentakarawal100% (1)

- Incorporation MoA AoADocument26 paginiIncorporation MoA AoAFarhanÎncă nu există evaluări

- 2019legislation - Revised Corporation Code Comparative Matrix - As of March 22 2019 PDFDocument121 pagini2019legislation - Revised Corporation Code Comparative Matrix - As of March 22 2019 PDFJohn Lloyd MacuñatÎncă nu există evaluări

- By LawsDocument22 paginiBy Lawsrhelmes67% (3)

- Accounting for shareholders' equity and share capitalDocument9 paginiAccounting for shareholders' equity and share capitalNimfa SantiagoÎncă nu există evaluări

- Company Law: Abhishek Reddy Aditya Tolasaria Amrita Philip Anil Lyngdoh Bhavik AmbaniDocument25 paginiCompany Law: Abhishek Reddy Aditya Tolasaria Amrita Philip Anil Lyngdoh Bhavik AmbaniBhavik AmbaniÎncă nu există evaluări

- Corporation - FBN SampleDocument1 paginăCorporation - FBN SampleOliver EnriqueÎncă nu există evaluări

- Effect of Incorporation - Companies Act 1965Document14 paginiEffect of Incorporation - Companies Act 1965Nur Afiza Tali67% (6)

- A. On November 27, The Board of Directors of India Star Company Declared A $.35 Per ShareDocument109 paginiA. On November 27, The Board of Directors of India Star Company Declared A $.35 Per ShareChris Jay LatibanÎncă nu există evaluări

- Poro Company audit comparative data from 2002-2006Document2 paginiPoro Company audit comparative data from 2002-2006Mark Michael Legaspi100% (1)

- Forms Of Business Organizations ExplainedDocument17 paginiForms Of Business Organizations Explainedanon_855990044Încă nu există evaluări

- Company Law Principles and ConceptsDocument143 paginiCompany Law Principles and ConceptsAbhi Joshi100% (1)

- Corporation Law: Atty. Divina's Highlights of The Revised Corporation Code (Zoom Lecture and Book)Document14 paginiCorporation Law: Atty. Divina's Highlights of The Revised Corporation Code (Zoom Lecture and Book)Joesil DianneÎncă nu există evaluări

- CS Executive Company Law Revision NotesDocument84 paginiCS Executive Company Law Revision NotesNaman Jain100% (1)

- Finecobank Spa: (Belonging To Banking Group)Document2 paginiFinecobank Spa: (Belonging To Banking Group)shashwatÎncă nu există evaluări

- ALS 2008 PartnershipDocument19 paginiALS 2008 PartnershipBilly EstanislaoÎncă nu există evaluări

- Shareholders Vs Stakeholders CapitalismDocument76 paginiShareholders Vs Stakeholders Capitalismsiagian_josh100% (1)

- Differentiating The Forms of Business Organization and Giving Examples of Forms of Business OrganizationsDocument24 paginiDifferentiating The Forms of Business Organization and Giving Examples of Forms of Business OrganizationsJohn Fort Edwin AmoraÎncă nu există evaluări

- Law On Business Organization Midterm ExamDocument1 paginăLaw On Business Organization Midterm ExamNikki Bucatcat100% (1)

- 2007-2013 Bar Questions On Corporation LawsDocument8 pagini2007-2013 Bar Questions On Corporation LawsHazel Martinii Panganiban100% (1)

- Audit of EquityDocument44 paginiAudit of EquityJoseph Lacuerda43% (7)

- Business Organisation: BBA I SemDocument49 paginiBusiness Organisation: BBA I SemAnchal LuthraÎncă nu există evaluări

- Ch11 Corporation AccountingDocument101 paginiCh11 Corporation AccountingLoksa Restu Sianturi100% (1)