S-ar putea să vă placă și

- 10 Steps To Invest in Equity - SFLBDocument3 pagini10 Steps To Invest in Equity - SFLBSudhir AnandÎncă nu există evaluări

- Annavonreitz-Pay To USDocument3 paginiAnnavonreitz-Pay To USaplawÎncă nu există evaluări

- From Calamity to Stability: Harnessing the Wisdom of Past Financial Crises to Build a Stable and Resilient Global Financial SystemDe la EverandFrom Calamity to Stability: Harnessing the Wisdom of Past Financial Crises to Build a Stable and Resilient Global Financial SystemÎncă nu există evaluări

- LTD CasesDocument4 paginiLTD CasestearsomeÎncă nu există evaluări

- IPSDocument6 paginiIPSAjay KumarÎncă nu există evaluări

- Risk and Return AnalysisDocument38 paginiRisk and Return AnalysisAshwini Pawar100% (1)

- UntitledDocument1.339 paginiUntitledIanÎncă nu există evaluări

- UpdateDocument6 paginiUpdatemtwang100% (1)

- Zztreasury Research - Daily - Global and Asia FX - April 29 2013Document2 paginiZztreasury Research - Daily - Global and Asia FX - April 29 2013r3iherÎncă nu există evaluări

- AmBank FX Daily OutlookDocument3 paginiAmBank FX Daily Outlookr3iherÎncă nu există evaluări

- RHB-OSK Malaysia DIVA Fund-PhsDocument5 paginiRHB-OSK Malaysia DIVA Fund-PhsNur Hidayah JalilÎncă nu există evaluări

- IDirect RBIActions Feb16Document4 paginiIDirect RBIActions Feb16umaganÎncă nu există evaluări

- Interest Rates InflationDocument3 paginiInterest Rates InflationHans WidjajaÎncă nu există evaluări

- Treasury Research News Bulletin - 27 November 2013Document2 paginiTreasury Research News Bulletin - 27 November 2013r3iherÎncă nu există evaluări

- Market Insight Q3FY12 RBI Policy Review Jan12Document3 paginiMarket Insight Q3FY12 RBI Policy Review Jan12poojarajeswariÎncă nu există evaluări

- Initiating Coverage Ruchi Soya Industries LTDDocument20 paginiInitiating Coverage Ruchi Soya Industries LTDShruti SharmaÎncă nu există evaluări

- Sharekhan's Top SIP Fund PicksDocument4 paginiSharekhan's Top SIP Fund PicksrajdeeppawarÎncă nu există evaluări

- Shriram Transport Finance: Recommendation: Buy CMP: Inr 1376 Allocation: 10%Document2 paginiShriram Transport Finance: Recommendation: Buy CMP: Inr 1376 Allocation: 10%genid.ssÎncă nu există evaluări

- HDFC Children's Gift Fund - Savings Plan - : Nature of Scheme Inception Date Option/PlanDocument5 paginiHDFC Children's Gift Fund - Savings Plan - : Nature of Scheme Inception Date Option/Plansandeepkumar404Încă nu există evaluări

- Blog - Fed Watch Nifty FiftyDocument3 paginiBlog - Fed Watch Nifty FiftyOwm Close CorporationÎncă nu există evaluări

- Debt StrategyDocument10 paginiDebt StrategysnehaaggarwalÎncă nu există evaluări

- Sunlife Balanced Fund KFDDocument4 paginiSunlife Balanced Fund KFDPaolo Antonio EscalonaÎncă nu există evaluări

- Stocks On The MoveDocument9 paginiStocks On The MoveGauriGanÎncă nu există evaluări

- July Monthly LetterDocument3 paginiJuly Monthly LetterTheLernerGroupÎncă nu există evaluări

- Project Report ON Study ofDocument78 paginiProject Report ON Study ofSana MoidÎncă nu există evaluări

- Opportunities in Times of Adversity!: Event UpdateDocument3 paginiOpportunities in Times of Adversity!: Event UpdateJanani SubramanianÎncă nu există evaluări

- Stock To Watch:: Nifty ChartDocument3 paginiStock To Watch:: Nifty ChartKavitha RavikumarÎncă nu există evaluări

- DaburIndia ICICI 130412Document2 paginiDaburIndia ICICI 130412Vipul BhatiaÎncă nu există evaluări

- Investor / Analyst Presentation (Company Update)Document48 paginiInvestor / Analyst Presentation (Company Update)Shyam SunderÎncă nu există evaluări

- Innovative Investments in MalaysiaDocument30 paginiInnovative Investments in MalaysiaNavin RajagopalanÎncă nu există evaluări

- 4 December Affluence RegDocument12 pagini4 December Affluence Regapi-279593513Încă nu există evaluări

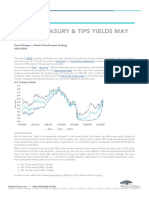

- Blog - Where Treasury TIPS Yields May Be HeadedDocument5 paginiBlog - Where Treasury TIPS Yields May Be HeadedOwm Close CorporationÎncă nu există evaluări

- Business Cycles: DR - James Manalel Professor, SMSDocument36 paginiBusiness Cycles: DR - James Manalel Professor, SMSnoorakohÎncă nu există evaluări

- State Bank of India: Play On Economic Recovery Buy MaintainedDocument4 paginiState Bank of India: Play On Economic Recovery Buy MaintainedPaul GeorgeÎncă nu există evaluări

- Monetary Policy LecDocument30 paginiMonetary Policy LecsofiaÎncă nu există evaluări

- Weekly CallDocument2 paginiWeekly Callpmishra3Încă nu există evaluări

- MF SIP Baskets: Retail ResearchDocument2 paginiMF SIP Baskets: Retail ResearchshobhaÎncă nu există evaluări

- PremiumTechnicals-Nov26 15 GammonDocument2 paginiPremiumTechnicals-Nov26 15 GammonWarren RiveraÎncă nu există evaluări

- Combined KIM For Liquid & Debt SchemesDocument15 paginiCombined KIM For Liquid & Debt SchemesSrikanth SwaÎncă nu există evaluări

- Global Macro Commentary July 14Document2 paginiGlobal Macro Commentary July 14dpbasicÎncă nu există evaluări

- 2 Federal Bank - One Pager Result Update Jan 24Document3 pagini2 Federal Bank - One Pager Result Update Jan 24raghavanseshu.seshathriÎncă nu există evaluări

- Stock To Watch:: Nifty ChartDocument3 paginiStock To Watch:: Nifty ChartKavitha RavikumarÎncă nu există evaluări

- Greaves Cotton: Upgraded To Buy With A PT of Rs160Document3 paginiGreaves Cotton: Upgraded To Buy With A PT of Rs160ajd.nanthakumarÎncă nu există evaluări

- HSL PCG "Currency Daily": 14 September, 2016Document5 paginiHSL PCG "Currency Daily": 14 September, 2016shobhaÎncă nu există evaluări

- OCTIS Asset Management: Octis Asia Pacific FundDocument3 paginiOCTIS Asset Management: Octis Asia Pacific FundoctisadminÎncă nu există evaluări

- Stable Value Strategy HSPDocument2 paginiStable Value Strategy HSPLoganBohannonÎncă nu există evaluări

- State Bank of India (STABAN) : Stress Levels More Comfortable Than PeersDocument2 paginiState Bank of India (STABAN) : Stress Levels More Comfortable Than PeersvijayÎncă nu există evaluări

- Market Outlook 27th March 2012Document4 paginiMarket Outlook 27th March 2012Angel BrokingÎncă nu există evaluări

- PLTVF Factsheet February 2014Document4 paginiPLTVF Factsheet February 2014randeepsÎncă nu există evaluări

- Stock To Watch:: Nifty ChartDocument2 paginiStock To Watch:: Nifty ChartSrinivas KaraÎncă nu există evaluări

- Option Writing (11-02-2020) - 202002111240535114872Document4 paginiOption Writing (11-02-2020) - 202002111240535114872ramajssÎncă nu există evaluări

- Strategic Analysis of SBIMFDocument19 paginiStrategic Analysis of SBIMF26amitÎncă nu există evaluări

- Some of The Important Functions of Stock Exchange/Secondary Market Are Listed BelowDocument3 paginiSome of The Important Functions of Stock Exchange/Secondary Market Are Listed BelowNadir ShahÎncă nu există evaluări

- Auto 03jun16 MoslDocument4 paginiAuto 03jun16 Moslravi285Încă nu există evaluări

- Singapore Property Companies: Singapore Industry Flash NoteDocument4 paginiSingapore Property Companies: Singapore Industry Flash NoteTerence Seah Pei ChuanÎncă nu există evaluări

- Snapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)Document2 paginiSnapshot For Straits Times Index STI (FSSTI) Straits Times Index (STI)api-237906069Încă nu există evaluări

- HSL PCG "Currency Daily": Private Client Group (PCG)Document6 paginiHSL PCG "Currency Daily": Private Client Group (PCG)umaganÎncă nu există evaluări

- MT-Daily Equity Morning Update 27 Dec 2011Document4 paginiMT-Daily Equity Morning Update 27 Dec 2011Mitesh ThackerÎncă nu există evaluări

- CIO Note Feb 6 2018Document2 paginiCIO Note Feb 6 2018Anonymous 2LowCnVdfÎncă nu există evaluări

- Rating Action:: Moody's Upgrades Indonesia's Sovereign Rating To Baa3 Outlook StableDocument5 paginiRating Action:: Moody's Upgrades Indonesia's Sovereign Rating To Baa3 Outlook StableMelyastarda SiregarÎncă nu există evaluări

- STFC PresentationDocument21 paginiSTFC Presentationamitsingla19Încă nu există evaluări

- Epaperpdf 23052011 22main Edition-Pg13-0Document1 paginăEpaperpdf 23052011 22main Edition-Pg13-0anon_534957202Încă nu există evaluări

- Equities: Nifty & DJIA - at Crucial Support LevelsDocument4 paginiEquities: Nifty & DJIA - at Crucial Support LevelsSubodh GuptaÎncă nu există evaluări

- Scratch Your BrainDocument22 paginiScratch Your BrainTrancemissionÎncă nu există evaluări

- Currency Derivatives ArbitrageDocument27 paginiCurrency Derivatives ArbitrageMinh NgọcÎncă nu există evaluări

- Reviews: Avg Antivirus For Mac: A Good Free OptionDocument5 paginiReviews: Avg Antivirus For Mac: A Good Free OptionTaaTa JimenezzÎncă nu există evaluări

- Ma2-2019 - Phan Gia BaoDocument8 paginiMa2-2019 - Phan Gia BaoBao PÎncă nu există evaluări

- Terms and Conditions (AutoRecovered)Document1 paginăTerms and Conditions (AutoRecovered)Jainah JaparÎncă nu există evaluări

- Prof Ethics T4 - 18010324103Document21 paginiProf Ethics T4 - 18010324103sashank varmaÎncă nu există evaluări

- PhptoDocument13 paginiPhptoAshley Jovel De GuzmanÎncă nu există evaluări

- Obligation VendorDocument7 paginiObligation VendorRonaRinÎncă nu există evaluări

- 2020 Contract Negotiations - Official ATU Proposal 6-25-21Document5 pagini2020 Contract Negotiations - Official ATU Proposal 6-25-21Chicago Transit Justice CoalitionÎncă nu există evaluări

- Trial and Death of Jose RizalDocument24 paginiTrial and Death of Jose RizalPatricia Denise Orquia50% (8)

- Art 13 6 People Vs EnguitoDocument9 paginiArt 13 6 People Vs EnguitoAAMCÎncă nu există evaluări

- Owler - Havells Competitors, Revenue and Employees - Owler Company ProfileDocument6 paginiOwler - Havells Competitors, Revenue and Employees - Owler Company ProfileAbhishek KumarÎncă nu există evaluări

- SLB Bydt Jar W4 - 00523 H - 6698873 - 01Document59 paginiSLB Bydt Jar W4 - 00523 H - 6698873 - 01Hector BarriosÎncă nu există evaluări

- Functions of RBIDocument8 paginiFunctions of RBIdchauhan21Încă nu există evaluări

- Extra Review Questions and Answers For Chapter 10 B. Answers To Short - Answer, Essays, and ProblemsDocument18 paginiExtra Review Questions and Answers For Chapter 10 B. Answers To Short - Answer, Essays, and Problemsshygirl7646617100% (1)

- Case Study and Mind Map Health Psychology - 2Document4 paginiCase Study and Mind Map Health Psychology - 2api-340420872Încă nu există evaluări

- AllBeats 133Document101 paginiAllBeats 133Ragnarr FergusonÎncă nu există evaluări

- AOIKenyaPower 4-12Document2 paginiAOIKenyaPower 4-12KhurshidÎncă nu există evaluări

- Representation Against CJIDocument21 paginiRepresentation Against CJIThe WireÎncă nu există evaluări

- 2014 15 PDFDocument117 pagini2014 15 PDFAvichal BhaniramkaÎncă nu există evaluări

- Tutorial Questions - Week 6Document3 paginiTutorial Questions - Week 6Arwa AhmedÎncă nu există evaluări

- J.K Shah Full Course Practice Question PaperDocument16 paginiJ.K Shah Full Course Practice Question PapermridulÎncă nu există evaluări

- Ys%, XLD M Dka S%L Iudcjd Ckrcfha .Eiü M %H: The Gazette of The Democratic Socialist Republic of Sri LankaDocument32 paginiYs%, XLD M Dka S%L Iudcjd Ckrcfha .Eiü M %H: The Gazette of The Democratic Socialist Republic of Sri LankaSanaka LogesÎncă nu există evaluări

- Home Improvement Business Exam GuideDocument10 paginiHome Improvement Business Exam GuideAl PenaÎncă nu există evaluări

- Drug MulesDocument1 paginăDrug MulesApril Ann Diwa AbadillaÎncă nu există evaluări

- Saep 134Document5 paginiSaep 134Demac SaudÎncă nu există evaluări