S-ar putea să vă placă și

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Challenges: Need One Bank Licensing Policy, But Several Bank LicensingpoliciesDocument8 paginiChallenges: Need One Bank Licensing Policy, But Several Bank LicensingpoliciesAbhinav WaliaÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Britannia Nutrichoice Case StudyDocument18 paginiBritannia Nutrichoice Case StudyAbhinav WaliaÎncă nu există evaluări

- Magic Quadrants & Critical Capabilities - Gartner Inc. (HTTP-::WWW - Gartner.com:technology:research:methodologies:magicquadrants - JSP#G)Document9 paginiMagic Quadrants & Critical Capabilities - Gartner Inc. (HTTP-::WWW - Gartner.com:technology:research:methodologies:magicquadrants - JSP#G)Naida KukuruzovićÎncă nu există evaluări

- PWC Insurance BrokerageDocument28 paginiPWC Insurance BrokerageAbhinav Walia100% (1)

- PWC Insurance BrokerageDocument28 paginiPWC Insurance BrokerageAbhinav Walia100% (1)

- IOT-Module 1 PDFDocument73 paginiIOT-Module 1 PDFM.A rajaÎncă nu există evaluări

- SIGFOX Whitepaper PDFDocument17 paginiSIGFOX Whitepaper PDFSerge StasovÎncă nu există evaluări

- Treadway Tier CompanyDocument11 paginiTreadway Tier CompanyAbhinav WaliaÎncă nu există evaluări

- ZyngaDocument29 paginiZyngaAbhinav WaliaÎncă nu există evaluări

- Sec B Group 7A LupinDocument22 paginiSec B Group 7A LupinKamalapati BeheraÎncă nu există evaluări

- The Indian Tractor Industry - Bumpy Road AheadDocument3 paginiThe Indian Tractor Industry - Bumpy Road AheadSanjana AcharyaÎncă nu există evaluări

- SB Whitepaper AutomotivecrmDocument8 paginiSB Whitepaper AutomotivecrmAbhinav WaliaÎncă nu există evaluări

- Tractors Article Sep14Document7 paginiTractors Article Sep14Abhinav WaliaÎncă nu există evaluări

- Imp Facts About BiscuitsDocument2 paginiImp Facts About BiscuitsAbhinav WaliaÎncă nu există evaluări

- CRM 8068 - enDocument2 paginiCRM 8068 - enAbhinav WaliaÎncă nu există evaluări

- Corporate Heads: Industry Company Name DesignationDocument2 paginiCorporate Heads: Industry Company Name DesignationAbhinav WaliaÎncă nu există evaluări

- White Lable ATMSDocument5 paginiWhite Lable ATMSAbhinav WaliaÎncă nu există evaluări

- Small To Big Marketing Makes It Possible: The Basics of Rural MarketingDocument2 paginiSmall To Big Marketing Makes It Possible: The Basics of Rural MarketingAbhinav WaliaÎncă nu există evaluări

- ContentServer - Sales Forecast For The Indian Tractor Industry For The FY 2012-13Document19 paginiContentServer - Sales Forecast For The Indian Tractor Industry For The FY 2012-13Abhinav WaliaÎncă nu există evaluări

- Small To Big Marketing Makes It Possible: The Basics of Rural MarketingDocument2 paginiSmall To Big Marketing Makes It Possible: The Basics of Rural MarketingAbhinav WaliaÎncă nu există evaluări

- Rural Finance Issues and ChallengesDocument12 paginiRural Finance Issues and ChallengesAbhinav Walia100% (1)

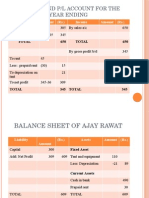

- Trading and P/L Account For The Year Ending: Expense Amount (RS.) Income Amount (RS.)Document2 paginiTrading and P/L Account For The Year Ending: Expense Amount (RS.) Income Amount (RS.)Abhinav WaliaÎncă nu există evaluări

- Corporate PresentationDocument45 paginiCorporate PresentationAbhinav WaliaÎncă nu există evaluări

- ContentServer - 3 COMPANY PROFILE Escorts Limited 2014Document9 paginiContentServer - 3 COMPANY PROFILE Escorts Limited 2014Abhinav WaliaÎncă nu există evaluări

- GK 1Document6 paginiGK 1Kushagra AgarwalÎncă nu există evaluări

- Chronology of Independent IndiaDocument10 paginiChronology of Independent IndiaAbhinav WaliaÎncă nu există evaluări

- Corporate PresentationDocument45 paginiCorporate PresentationAbhinav WaliaÎncă nu există evaluări

- MrsDocument8 paginiMrsalien888Încă nu există evaluări

- Connection and Protection in The Digital AgeDocument123 paginiConnection and Protection in The Digital AgejrturlaÎncă nu există evaluări

- Key Outcomes of The World Radiocommunication Conference 2019Document56 paginiKey Outcomes of The World Radiocommunication Conference 2019Mwaisa BangaÎncă nu există evaluări

- GE Lns-Smart Connected OperationsDocument29 paginiGE Lns-Smart Connected OperationsMichael Parohinog GregasÎncă nu există evaluări

- Senior Vice President Sales in New York City NY Resume Mary PaganoDocument2 paginiSenior Vice President Sales in New York City NY Resume Mary PaganoMaryPaganoÎncă nu există evaluări

- Chapter 4 IOT of Emerging TechnologyDocument19 paginiChapter 4 IOT of Emerging TechnologyAddisalem GanfureÎncă nu există evaluări

- Introduction To Iot - Part I: Dr. Sudip MisraDocument23 paginiIntroduction To Iot - Part I: Dr. Sudip MisraabdulmuqueemÎncă nu există evaluări

- Bosch Software Innovations Iot Whitepaper StrategyDocument22 paginiBosch Software Innovations Iot Whitepaper Strategyramnadh803181Încă nu există evaluări

- A Survey On Iot Security: Application Areas, Security Threats, and Solution ArchitecturesDocument24 paginiA Survey On Iot Security: Application Areas, Security Threats, and Solution ArchitecturesManojkumar KothandapaniÎncă nu există evaluări

- An Exploration About Frameworks Based On Green Internet of ThingsDocument5 paginiAn Exploration About Frameworks Based On Green Internet of ThingsProjects MÎncă nu există evaluări

- GSMA IoT Device Connection Efficiency Guidelines TS.34 v5.0Document80 paginiGSMA IoT Device Connection Efficiency Guidelines TS.34 v5.0Fernando HrabinaÎncă nu există evaluări

- A Survey On Real Time Bus Monitoring SystemDocument4 paginiA Survey On Real Time Bus Monitoring SystemAnonymous CUPykm6DZÎncă nu există evaluări

- R20 M.Tech DSDocument64 paginiR20 M.Tech DSPrasanna KumarÎncă nu există evaluări

- Eca3G Introduction Paper Edit Eng Feb08 2019Document16 paginiEca3G Introduction Paper Edit Eng Feb08 2019JohanÎncă nu există evaluări

- Shigeto HIRAGURI: KeywordsDocument5 paginiShigeto HIRAGURI: KeywordsNdee PitsiÎncă nu există evaluări

- Independent Learning Task 4: Guidelines in Reading A Text CriticallyDocument2 paginiIndependent Learning Task 4: Guidelines in Reading A Text CriticallyNur-Aliya ModerikaÎncă nu există evaluări

- IoT Study MaterialDocument8 paginiIoT Study MaterialxyzÎncă nu există evaluări

- 5G Technology Elements For Future Internet of ThingsDocument26 pagini5G Technology Elements For Future Internet of ThingsFahad IbrarÎncă nu există evaluări

- LMU-330™GPRS /HSPA Series: Experience The AdvantageDocument2 paginiLMU-330™GPRS /HSPA Series: Experience The AdvantageJean RamírezÎncă nu există evaluări

- Business Communicaton Project TelenorDocument49 paginiBusiness Communicaton Project TelenorAamir Raza67% (3)

- Investing Internet of Things Iot Spotlight On DairyDocument24 paginiInvesting Internet of Things Iot Spotlight On DairyAnand KiranÎncă nu există evaluări

- 4 - Internet of Things (IoT)Document92 pagini4 - Internet of Things (IoT)Kirubel DessieÎncă nu există evaluări

- White Paper EnOcean Product IntegrationDocument8 paginiWhite Paper EnOcean Product Integrationfernando_mart859243Încă nu există evaluări

- Using AutomationML and Graph-Based Design Languages For Automatic Generation of Digital Twins of Cyber-Physical SystemsDocument8 paginiUsing AutomationML and Graph-Based Design Languages For Automatic Generation of Digital Twins of Cyber-Physical SystemsJosip StjepandicÎncă nu există evaluări

- Nokia GSM Connectivity Terminal and Nokia 12 GSM Module: Properties Reference GuideDocument63 paginiNokia GSM Connectivity Terminal and Nokia 12 GSM Module: Properties Reference GuideEug. Sam.Încă nu există evaluări

- M100451 Aplicom A1 Product FamilyDocument2 paginiM100451 Aplicom A1 Product FamilyCesar BenavidesÎncă nu există evaluări

- Smartcities 04 00041 v2Document16 paginiSmartcities 04 00041 v2Георги НасковÎncă nu există evaluări

- New Open Elective IoTDocument1 paginăNew Open Elective IoTManikanta RobbiÎncă nu există evaluări