S-ar putea să vă placă și

- Macaura V Northern Assurance Company LTD PDFDocument9 paginiMacaura V Northern Assurance Company LTD PDFVishalÎncă nu există evaluări

- Residence of The CompanyDocument51 paginiResidence of The CompanygauravÎncă nu există evaluări

- Mistaken Identity ContractsDocument2 paginiMistaken Identity ContractsMayank SenÎncă nu există evaluări

- Daimler Co LTD Vs Continental Tyre and Rubber Co LTDDocument1 paginăDaimler Co LTD Vs Continental Tyre and Rubber Co LTDyohaan john0% (1)

- Daimler Co. v. Continental TyreDocument27 paginiDaimler Co. v. Continental TyreVishal Anand100% (1)

- Case Summary 2 (Corporate Management 1-2Document4 paginiCase Summary 2 (Corporate Management 1-2Subodh MalkarÎncă nu există evaluări

- Commissioner Of Income-Tax v. Jayalakshmi Rice And Oil Mills Contractor Co (38Document2 paginiCommissioner Of Income-Tax v. Jayalakshmi Rice And Oil Mills Contractor Co (38Sai Malavika Tulugu0% (1)

- Landmark CCI Order Finds Cement Companies Guilty of Price FixingDocument9 paginiLandmark CCI Order Finds Cement Companies Guilty of Price FixingAkshita choubey100% (1)

- KREDITBANK CASSEL G.M.B.H. v. SCHENKERS, LIMITED. (1925Document10 paginiKREDITBANK CASSEL G.M.B.H. v. SCHENKERS, LIMITED. (1925Ashley KoÎncă nu există evaluări

- Morgan Stanley Mutual Fund Vs Kartrik DasDocument15 paginiMorgan Stanley Mutual Fund Vs Kartrik DasChaitanya Sharma100% (1)

- Satyabrata Ghose vs. Mugneeram Bangur & Co.Document21 paginiSatyabrata Ghose vs. Mugneeram Bangur & Co.Aditi BanerjeeÎncă nu există evaluări

- Lloyd Vs Grace SmithDocument3 paginiLloyd Vs Grace SmithAkshay Bhasin60% (5)

- Case Briefs 2Document4 paginiCase Briefs 2Rachit TiwariÎncă nu există evaluări

- Builder Association of India V Cement Manufacturers Association Cement Cartelisation CaseDocument7 paginiBuilder Association of India V Cement Manufacturers Association Cement Cartelisation CaseVaibhav50% (2)

- CT Case AnalysisDocument16 paginiCT Case AnalysisAchal Mittal0% (1)

- H Dakin & Co LTD V LeeDocument13 paginiH Dakin & Co LTD V LeeKori RuslanÎncă nu există evaluări

- Chanakya National Law University, Patna: Project Topic: Morgan Stanley Mutual Fund Vs Kartick DasDocument4 paginiChanakya National Law University, Patna: Project Topic: Morgan Stanley Mutual Fund Vs Kartick Dashuma gousÎncă nu există evaluări

- Section 11 ApplicationDocument11 paginiSection 11 Applicationudit mehtaÎncă nu există evaluări

- Case Comment Gannon Dunkerley v. State of MadrasDocument12 paginiCase Comment Gannon Dunkerley v. State of MadrasNitish Joshi100% (1)

- Sale of Goods Act 1930 Smart Notes PDFDocument32 paginiSale of Goods Act 1930 Smart Notes PDFLAZY TWEETY100% (1)

- Erlanger V New Sombrero Phosphate CompanyDocument4 paginiErlanger V New Sombrero Phosphate CompanyAsare William50% (2)

- Case Analysis of Administrative Law (Himmat Lal Shah V Commissioner of PoliceDocument18 paginiCase Analysis of Administrative Law (Himmat Lal Shah V Commissioner of PoliceShubham PhophaliaÎncă nu există evaluări

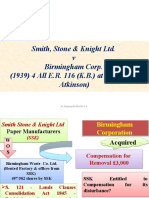

- 10 Smith, Stone & Knight Ltd.Document37 pagini10 Smith, Stone & Knight Ltd.gauravÎncă nu există evaluări

- English Assignment On Lord DenningDocument11 paginiEnglish Assignment On Lord DenningWONDERFULDAYSÎncă nu există evaluări

- United Spirit PVT LTD Vs Kanchan Udyog LTDDocument10 paginiUnited Spirit PVT LTD Vs Kanchan Udyog LTDDivya AggarwalÎncă nu există evaluări

- Standard Chartered vs. CustodianDocument6 paginiStandard Chartered vs. CustodianPranshu VatsÎncă nu există evaluări

- CASE ANALYSIS ON BHARAT GLASS TUBE LIMITED VDocument2 paginiCASE ANALYSIS ON BHARAT GLASS TUBE LIMITED VvishnuÎncă nu există evaluări

- Mithoolal Nayak Vs Lic: Facts in BriefDocument4 paginiMithoolal Nayak Vs Lic: Facts in BriefrajÎncă nu există evaluări

- Immunity of Trade UnionsDocument14 paginiImmunity of Trade UnionsRudra Pratap Tripathi100% (2)

- Jurisprudence 3rd SemesterDocument10 paginiJurisprudence 3rd SemesterDevansh Kumar SinghÎncă nu există evaluări

- Case Brief - Polaroid v. PolaradDocument2 paginiCase Brief - Polaroid v. PolaradYsabelleÎncă nu există evaluări

- BAYLEY v.THE MANCHESTER, SHEFFIELD, AND LINCOLNSHIRE RAILWAY COMPANY.Document16 paginiBAYLEY v.THE MANCHESTER, SHEFFIELD, AND LINCOLNSHIRE RAILWAY COMPANY.ZACHARIAH MANKIRÎncă nu există evaluări

- Lect. 2 Fixtures and ChattelsDocument9 paginiLect. 2 Fixtures and ChattelsBrianna Brown100% (2)

- TazzDocument10 paginiTazzBeebee ZainabÎncă nu există evaluări

- Corporate PersonalityDocument3 paginiCorporate PersonalitymanjushreeÎncă nu există evaluări

- Atul Mehra Vs Bank of MaharashtraDocument1 paginăAtul Mehra Vs Bank of MaharashtraAnant Khajuria50% (2)

- Continental Can CoDocument3 paginiContinental Can CoThomas JosephÎncă nu există evaluări

- Case Analysis Law Assignment BY: Ankita Jindal Mba (Ibf) 1226215101 1. Case Citation in FullDocument3 paginiCase Analysis Law Assignment BY: Ankita Jindal Mba (Ibf) 1226215101 1. Case Citation in FullSiddhant Mathur100% (2)

- T V Somanathan Administrative and Regulatory State - Oxford HandbooksDocument26 paginiT V Somanathan Administrative and Regulatory State - Oxford HandbooksDebabrataÎncă nu există evaluări

- Adams V Cape Industries PLC - 2003Document1 paginăAdams V Cape Industries PLC - 2003laiyyeen100% (4)

- Case Study on S.P. Gupta vs Union of IndiaDocument14 paginiCase Study on S.P. Gupta vs Union of IndiaTej Pratap Singh100% (1)

- Land Law LLB NotesDocument40 paginiLand Law LLB Notesdg432170% (20)

- Residential Status Problems 2021-2022-1Document5 paginiResidential Status Problems 2021-2022-120-UCO-517 AJAY KELVIN AÎncă nu există evaluări

- Banwari Lal and Ors. Vs Sukhdarshan Dayal On 12 December, 1972Document3 paginiBanwari Lal and Ors. Vs Sukhdarshan Dayal On 12 December, 1972Rohit Dwivedi33% (3)

- DDA Vs Skipper Construction LTDDocument6 paginiDDA Vs Skipper Construction LTDgaurav_11Încă nu există evaluări

- Name of The Co.Document89 paginiName of The Co.gaurav100% (1)

- M.S. Anirudhan Vs The Thomco's Bank Ltd.Document2 paginiM.S. Anirudhan Vs The Thomco's Bank Ltd.Brena Gala100% (1)

- Case of ICICI and Bank of Madura MergerDocument6 paginiCase of ICICI and Bank of Madura MergerWilliam Masterson Shah100% (3)

- Summary Fulham Football Club LTD V Cabra Estates PLC 1994 1 BCLC 363 PDFDocument5 paginiSummary Fulham Football Club LTD V Cabra Estates PLC 1994 1 BCLC 363 PDFTruc Ha ThanhÎncă nu există evaluări

- Abir Roy Kluwer CommentaryDocument196 paginiAbir Roy Kluwer CommentaryP Sivarajan P SivarajanÎncă nu există evaluări

- Design CasesDocument9 paginiDesign CaseskratiÎncă nu există evaluări

- DRT Order On Vijay Mallya CaseDocument143 paginiDRT Order On Vijay Mallya CaseAnushree JugadeÎncă nu există evaluări

- CMSR - Case Analysis 22.10.2021Document10 paginiCMSR - Case Analysis 22.10.2021prarthana rameshÎncă nu există evaluări

- Compiled Case Summary Corporate Basics 1-2Document13 paginiCompiled Case Summary Corporate Basics 1-2Priya KulkarniÎncă nu există evaluări

- Royal British rule: doctrine Bank v of Turquand constructive noticeDocument30 paginiRoyal British rule: doctrine Bank v of Turquand constructive noticedownloader10280% (5)

- Macaura V Northern Assurance Company LTDDocument9 paginiMacaura V Northern Assurance Company LTDVishalÎncă nu există evaluări

- Request Made By: Request Made On: IP: Westlaw India Delivery SummaryDocument9 paginiRequest Made By: Request Made On: IP: Westlaw India Delivery SummaryVishal AnandÎncă nu există evaluări

- Performance Breach and Frustration TutorialDocument9 paginiPerformance Breach and Frustration TutorialAdam 'Fez' FerrisÎncă nu există evaluări

- Law Teacher Net Contract Law Page CASESDocument7 paginiLaw Teacher Net Contract Law Page CASESfel brobbsÎncă nu există evaluări

- Bisset V WilkinsonDocument8 paginiBisset V WilkinsonAkwasiÎncă nu există evaluări

- Adams V Cape Industries PLCDocument126 paginiAdams V Cape Industries PLCPui Quan YapÎncă nu există evaluări

- Hotel Jaya Puri V National Union of HotelDocument6 paginiHotel Jaya Puri V National Union of HotelPui Quan YapÎncă nu există evaluări

- Double Acres SDN BHD V Tiarasetia SDN BHDDocument31 paginiDouble Acres SDN BHD V Tiarasetia SDN BHDPui Quan YapÎncă nu există evaluări

- 6001 MS 20110309Document19 pagini6001 MS 20110309Pui Quan YapÎncă nu există evaluări

- MHL 2018Document16 paginiMHL 2018miha3la33Încă nu există evaluări

- Oblicon DigestDocument7 paginiOblicon DigestGe LatoÎncă nu există evaluări

- Actuary India Jan 2013Document32 paginiActuary India Jan 2013Rohan KunduÎncă nu există evaluări

- CimoDocument46 paginiCimomauricioh10% (1)

- HBL Installment Plan DetailsDocument4 paginiHBL Installment Plan DetailsbalochimrankhanÎncă nu există evaluări

- United India Insurance Company Limited: MR Mr. Deepak KumarDocument11 paginiUnited India Insurance Company Limited: MR Mr. Deepak KumarAnkesh Kumar SrivastavaÎncă nu există evaluări

- 2014 BigData Analytics Business Partner Case Studies 4-9-14Document59 pagini2014 BigData Analytics Business Partner Case Studies 4-9-14Dario SimbañaÎncă nu există evaluări

- Cash Disbursement 2007Document48 paginiCash Disbursement 2007api-3740993Încă nu există evaluări

- Memo Salary Deduction Facility Via AGDocument2 paginiMemo Salary Deduction Facility Via AGjaya98Încă nu există evaluări

- Axis Bank (H.R.)Document99 paginiAxis Bank (H.R.)Priya NotInterested SolankiÎncă nu există evaluări

- Automotive, Banking & Other Sectors Top Companies HR ContactsDocument15 paginiAutomotive, Banking & Other Sectors Top Companies HR ContactsMohitÎncă nu există evaluări

- M MockbarDocument11 paginiM MockbarHadjie LimÎncă nu există evaluări

- Registration PDFDocument1 paginăRegistration PDFzl0% (2)

- Socorro Water District Surigao Del Norte Executive Summary 2021Document4 paginiSocorro Water District Surigao Del Norte Executive Summary 2021Miss_AccountantÎncă nu există evaluări

- Commercial Law Memory Aid TitleDocument22 paginiCommercial Law Memory Aid TitlefrÎncă nu există evaluări

- Real Estate Sales and Purchase AgreementDocument2 paginiReal Estate Sales and Purchase AgreementAndrea A VargasÎncă nu există evaluări

- Ruchi ProjectDocument81 paginiRuchi ProjectSujeet Kumar0% (1)

- Managing Business Risks: What Is Business Risk?Document5 paginiManaging Business Risks: What Is Business Risk?Lianna RodriguezÎncă nu există evaluări

- Hotel Opening Manual IHG 2005Document119 paginiHotel Opening Manual IHG 2005Tanti.Saptarini100% (2)

- UX Project FINAL PRESENTATIONDocument34 paginiUX Project FINAL PRESENTATIONprime developersÎncă nu există evaluări

- Bike PolicyDocument2 paginiBike PolicyJagjeet SinghÎncă nu există evaluări

- Fine Arts Insurance Scope Inthe East, FinalDocument102 paginiFine Arts Insurance Scope Inthe East, FinalCody ThompsonÎncă nu există evaluări

- Nicole Reese SBA2Document1 paginăNicole Reese SBA2ColeReeseÎncă nu există evaluări

- Contract Law 1 NotesDocument20 paginiContract Law 1 NotesThe Law ClassroomÎncă nu există evaluări

- The Accounting Cycle:: Accruals and DeferralsDocument41 paginiThe Accounting Cycle:: Accruals and Deferralsmahtab_rasheedÎncă nu există evaluări

- MARINA CPC Amendment for MBCA "OLIVIA ZHANGDocument5 paginiMARINA CPC Amendment for MBCA "OLIVIA ZHANGMary Heide H. Amora100% (1)

- Comparing ULIPs and Traditional PlansDocument98 paginiComparing ULIPs and Traditional PlansAnand Singh100% (1)

- Proposal For The Issuance of An Import Documentary Credit: Beneficiary (Full Name & Address)Document4 paginiProposal For The Issuance of An Import Documentary Credit: Beneficiary (Full Name & Address)krilinX0Încă nu există evaluări

- FlexiDocument4 paginiFlexiManish Mani100% (1)

- US Internal Revenue Service: td8734Document314 paginiUS Internal Revenue Service: td8734IRSÎncă nu există evaluări