S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Mutual Fund Holdings in DHFLDocument7 paginiMutual Fund Holdings in DHFLShyam SunderÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- JUSTDIAL Mutual Fund HoldingsDocument2 paginiJUSTDIAL Mutual Fund HoldingsShyam SunderÎncă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Settlement Order in Respect of R.R. Corporate Securities LimitedDocument2 paginiSettlement Order in Respect of R.R. Corporate Securities LimitedShyam SunderÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- Financial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Document4 paginiFinancial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Shyam SunderÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- PR - Exit Order in Respect of Spice & Oilseeds Exchange Limited (Soel)Document1 paginăPR - Exit Order in Respect of Spice & Oilseeds Exchange Limited (Soel)Shyam SunderÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Financial Results For June 30, 2014 (Audited) (Result)Document3 paginiFinancial Results For June 30, 2014 (Audited) (Result)Shyam SunderÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Settlement Order in Respect of Bikaner Wooltex Pvt. Limited in The Matter of Sangam Advisors LimitedDocument2 paginiSettlement Order in Respect of Bikaner Wooltex Pvt. Limited in The Matter of Sangam Advisors LimitedShyam SunderÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- HINDUNILVR: Hindustan Unilever LimitedDocument1 paginăHINDUNILVR: Hindustan Unilever LimitedShyam SunderÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Order of Hon'ble Supreme Court in The Matter of The SaharasDocument6 paginiOrder of Hon'ble Supreme Court in The Matter of The SaharasShyam SunderÎncă nu există evaluări

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- Exit Order in Respect of The Spice and Oilseeds Exchange Limited, SangliDocument5 paginiExit Order in Respect of The Spice and Oilseeds Exchange Limited, SangliShyam SunderÎncă nu există evaluări

- Financial Results, Limited Review Report For December 31, 2015 (Result)Document4 paginiFinancial Results, Limited Review Report For December 31, 2015 (Result)Shyam SunderÎncă nu există evaluări

- Standalone Financial Results, Auditors Report For March 31, 2016 (Result)Document5 paginiStandalone Financial Results, Auditors Report For March 31, 2016 (Result)Shyam SunderÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Financial Results For Mar 31, 2014 (Result)Document2 paginiFinancial Results For Mar 31, 2014 (Result)Shyam SunderÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Financial Results & Limited Review Report For June 30, 2015 (Standalone) (Result)Document3 paginiFinancial Results & Limited Review Report For June 30, 2015 (Standalone) (Result)Shyam SunderÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Financial Results For June 30, 2013 (Audited) (Result)Document2 paginiFinancial Results For June 30, 2013 (Audited) (Result)Shyam SunderÎncă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Financial Results For September 30, 2013 (Result)Document2 paginiFinancial Results For September 30, 2013 (Result)Shyam SunderÎncă nu există evaluări

- PDF Processed With Cutepdf Evaluation EditionDocument3 paginiPDF Processed With Cutepdf Evaluation EditionShyam SunderÎncă nu există evaluări

- Financial Results For Dec 31, 2013 (Result)Document4 paginiFinancial Results For Dec 31, 2013 (Result)Shyam Sunder0% (1)

- Standalone Financial Results For September 30, 2016 (Result)Document3 paginiStandalone Financial Results For September 30, 2016 (Result)Shyam SunderÎncă nu există evaluări

- Standalone Financial Results For June 30, 2016 (Result)Document2 paginiStandalone Financial Results For June 30, 2016 (Result)Shyam SunderÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Document3 paginiStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- Standalone Financial Results For March 31, 2016 (Result)Document11 paginiStandalone Financial Results For March 31, 2016 (Result)Shyam SunderÎncă nu există evaluări

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Document4 paginiStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderÎncă nu există evaluări

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document5 paginiStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document3 paginiStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderÎncă nu există evaluări

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document4 paginiStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderÎncă nu există evaluări

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Document4 paginiStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderÎncă nu există evaluări

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Document4 paginiStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Transcript of The Investors / Analysts Con Call (Company Update)Document15 paginiTranscript of The Investors / Analysts Con Call (Company Update)Shyam SunderÎncă nu există evaluări

- Investor Presentation For December 31, 2016 (Company Update)Document27 paginiInvestor Presentation For December 31, 2016 (Company Update)Shyam SunderÎncă nu există evaluări

- Sebi Sensex Nifty Bse NseDocument47 paginiSebi Sensex Nifty Bse NseKushal WaliaÎncă nu există evaluări

- HuiDocument5 paginiHuiShiv SinghÎncă nu există evaluări

- Full Length Paper - Role of Technology On Green BankinglDocument15 paginiFull Length Paper - Role of Technology On Green Bankinglapi-33150260Încă nu există evaluări

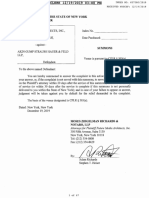

- FMA Sues Akin GumpDocument67 paginiFMA Sues Akin GumpDomainNameWireÎncă nu există evaluări

- M& A - Case Study PresentationDocument71 paginiM& A - Case Study PresentationDilip JagadÎncă nu există evaluări

- Customer Relationship Management (CRM) in Banks: Pooja GargDocument29 paginiCustomer Relationship Management (CRM) in Banks: Pooja GargManish SinghÎncă nu există evaluări

- OPPT: Individual UCC DEMAND BANK UNFREEZE TemplateDocument4 paginiOPPT: Individual UCC DEMAND BANK UNFREEZE TemplateAmerican Kabuki100% (3)

- Indian Economy QuestionsDocument25 paginiIndian Economy QuestionsPadyala SriramÎncă nu există evaluări

- The History of Banking Kerim CatovicDocument10 paginiThe History of Banking Kerim CatovicsolacevillarealÎncă nu există evaluări

- Sai Hadoop ResumeDocument5 paginiSai Hadoop ResumeSaikumar AvanigaddaÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Atm Using FingerprintDocument5 paginiAtm Using FingerprintShivaÎncă nu există evaluări

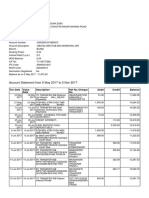

- Statement of Account Summary and Transaction DetailsDocument3 paginiStatement of Account Summary and Transaction Detailsfahad chaudhryÎncă nu există evaluări

- Indian Money Market 2019: An OverviewDocument50 paginiIndian Money Market 2019: An OverviewRavi Sahani100% (1)

- Payment Bank Impact On Digital BankingDocument78 paginiPayment Bank Impact On Digital BankingSudharshan Reddy P0% (1)

- Sally's Struthers Co. 2002-2003 financial activityDocument1 paginăSally's Struthers Co. 2002-2003 financial activityLlyod Francis LaylayÎncă nu există evaluări

- Bancassurance PDFDocument251 paginiBancassurance PDFdivyansh singh33% (3)

- Paul Thomson Search Fund Manifesto 2011 09Document25 paginiPaul Thomson Search Fund Manifesto 2011 09mitiwanaÎncă nu există evaluări

- Repo AccountingDocument11 paginiRepo AccountingRohit KhandelwalÎncă nu există evaluări

- BRD transaction reportDocument5 paginiBRD transaction reportDavid GeorgeÎncă nu există evaluări

- Global Insurance+ Review 2012 and Outlook 2013 14Document36 paginiGlobal Insurance+ Review 2012 and Outlook 2013 14Harry CerqueiraÎncă nu există evaluări

- Mba Finance Project Topics12345 PDFDocument4 paginiMba Finance Project Topics12345 PDFssanjitkumarÎncă nu există evaluări

- BPI Capital Audited Financial StatementsDocument66 paginiBPI Capital Audited Financial StatementsGes Glai-em BayabordaÎncă nu există evaluări

- Submitted To: Submitted byDocument33 paginiSubmitted To: Submitted byaanaughtyÎncă nu există evaluări

- Customer Perceptions and Knowledge of Islamic Banking in Bangladesh (38Document56 paginiCustomer Perceptions and Knowledge of Islamic Banking in Bangladesh (38Md.Azizul Islam0% (1)

- ECB European Central BankDocument12 paginiECB European Central BankHiral SoniÎncă nu există evaluări

- Supply Chain Management of First FlightDocument6 paginiSupply Chain Management of First Flightarunshukla08Încă nu există evaluări

- Yu Lim Vs YuDocument6 paginiYu Lim Vs YusandrasulitÎncă nu există evaluări

- Medfield Pharmaceuticals' Valuation and Strategic OptionsDocument9 paginiMedfield Pharmaceuticals' Valuation and Strategic OptionsvATSALAÎncă nu există evaluări

- MCQ - BankingDocument4 paginiMCQ - Bankingbhaskar51178Încă nu există evaluări

- 03 08 12 Motion To Consolidate Memorandum of Points and AuthoritiesDocument10 pagini03 08 12 Motion To Consolidate Memorandum of Points and AuthoritiesR. Castaneda100% (2)