International Journal of Business and Management Invention

ISSN (Online): 2319 8028, ISSN (Print): 2319 801X

www.ijbmi.org Volume 2 Issue 10 October. 2013 PP.12-17

The Accounting Information Quality And The Accounting

Information System Quality Through The Organizational

Structure : A Survey Of The Baitulmal Wattamwil (BMT) In

West Java Indonesia

Sri Dewi Anggadini

1

,Doctoral Student Accounting Department, Faculty of Economics and Business, Padjadjaran University

Bandung, West Java, Indonesia

ABSTRACT : The purpose of the study is to measure the influences of accounting information system quality

on the accounting information quality through observing the organizational structure. The study uses

descriptive and verificative analysis method and involves forty seven (47) Baitulmal Wattamwil (BMT) in West

Java Indonesia, those are applied accounting information system. The result of the study shows that the

organizational structure have significant influence on the accounting information system quality. Besides, the

accounting information system quality has an impact on the accounting information quality as well.

KEYWORDS : organizational structure, accounting information system quality, accounting information

quality.

I.

INTRODUCTION

An organization takes into account that providing qualified information is the key to achieve

competitive achievement (Suri, 2005) in market competition (Mc. Leod, 2007:34), leverage is very helpful for

the organization to make a fast and precise decision, competed with its competitors (Laudon and Laudon,

2012:14). Accounting information quality allows information users, in this case organizations, in making

valuable decisions, called usefulness decisions (Shipper and Vincent, 2003: 98). Further, Laudon and Laudon

(2012:48) states if the information in the organization has good quality, the organization will run well.

Otherwise low quality of information is a threat to the survival of the organization. Therefore information

quality is crucial for the sustainability of an organization (Laudon and Laudon, 2012:50).Discussing on criteria

of accounting information quality, McLeod (2007: 43) determines that the accounting information quality is the

information considered to be accurate, timely, relevant, and complete. Accounting information quality is

generated by the quality of accounting information system (Laudon and Laudon, 2012: 7). No accounting

information quality without quality of accounting information system (Sacer et al., 2006:62). Accounting

information system is a tool used by management in organizations to give added value that results a competitive

advantage (Stair and Reynolds, 2010:6).

The issues arising on phenomenon on accounting information quality are, the less-optimum condition

for quality of information technology (Agus Martowardojo, 2010), such a badly-documented report in BUMN

(governments incubator business) requiring management of information system to access data (Dahlan Iskan,

2012) and some problems in making an accountable and transparent financial management (Hadi Poernomo,

2012), the unwell-programmed recovery of law and national accounting system leads public sectors and

business to the insignificant progression of the development of report accountability and transparency (Anwar

Nasution, 2007). Unfortunately, the condition is also occurred in Baitulmal Wattamwil (BMT). The prior

observation shows that the ineffective management of information system leads to the problems arisen because

of information system. It is assumed that unqualified accounting system may cause unqualified accounting

information system (Sacer et al., 2006: 62). Sacer et al. (2006: 61) and Zimerman et al. (1995) argue that

accounting information system produces accounting information. Accounting information system is a sequence

or integration of sub systems or units both physically and non-physically which are interrelated and correlated

congruously to manage data transactions from financial issue to financial information (Azhar Susanto, 2008:72).

In line with Sacer, OBrien (2008: 10) argues that accounting information system consists of brainware,

information technology (including hardware, software and communication network) and database which collect,

manipulate, and distribute information within organization.

www.ijbmi.org

12 | Page

The Accounting Information Quality And The

The information system should cover the knowledge of the way people work and of social practice

involved in the system (Indeje and Zheng, 2010: 4). One of main factors that has to be considered in that point is

organizational structure (Laudon and Laudon, 2012: 109). In this sense, information system involves an

important component, that is a man (Claver et al., 2007), and Fontaine (2007) argues that organizational

structure is the most crucial components of all business strategy, it is of the essence that an organizing is

resources, specifically human resources. In that case, it is clear that information system is a part related to

organizational structure ; information system and organization are interrelated and inter-influenced (Laudon and

Laudon, 2012: 19). Arguing to the issue, the focus of the study is explicitly formulated as the concept that the

accounting information quality is believed to be influenced by the accounting information system quality

influenced by the organizational structure. Adopted from Ang et al. (2001), the study also argues the influence

of information technology usage as organizational structure, organizational size, managerial IT knowledge, top

management supports, financial resources, goal alignment, and budgeting method.

II.

REVIEW OF LITERATUR

2.1 Accounting Information Quality

Information quality is multidimensional. This means that organization must use multiple measures to

evaluate the quality of their information. Schiper and Vincent (2003: 99) explain that accounting information

quality may be defined as a complex concept covering relevancy of accounting information value, accounting

conservatism, and management profit. McLeod (2007:86) explain that information should be available for

problem solving before crisis situasions develop or opportunities are lost. The user should be to obtain

information that describes what is happening now, in addition to what happened in the past. Information that

arrives the decision is made has no value. The dimension and indicators of information quality used in this study

are adopted from theories argued by Xu, et al. (2003: 461), Mc. Leod (2007: 35) and Romney and Steinbart

(2012:6). The dimension and indicators are illustrated by accurate (ideally, all information should be accurate,

however features that contribute to system accuracy add to the of an information syste), timeline (information

should be available for decision making before crisis situation develop or oppurtunities are lost), relevant

(information has relevancy when it pertains to the problem at hand. The user should be able to select the

data that are needed without wading trough a volume of unrelated facts), and complete (users should be able to

obtain information that presents a complete picture of a particular problem or solution. However, systems

should not drown users in a sea of information) ( Hilton, 2000:551; Mc. Leod, 2007:35 ; serta Romney, et

al, 2012:6 ; Kieso, et al, 2012:44-47 ; OBrien, et al, 2008:364 ; Eppler, 2003: 68).

2.2.Accounting Information System Quality

An accounting information system is a system that collects records, stores, and processes data to

produce information for decision makers (Romney et al, 2012: 6). Adding to previous statement, Azhar Susanto

(2008: 72) describes accounting information system, basically, is integration of some transactional management

system. Thus, accounting information system may be defined as a group or integration of sub systems /

components both physical and non-physical which are interrelated and interrelationship congruously to operate

data transactions related to financial issue into financial information. Furhthermore, OBrien (2008), Romney

and Steinbart (2012), Azhar Susanto (2008), state that the accounting information system has components

consisting of hardware, software, brainware, procedures, database, and network communication technology.

According to Stair and Reynolds (2010:57), an accounting information system quality is usually flexible,

efficient, accessible, and timely. The term "quality" can mean success (DeLone and McLean, 1992 & 2003;

Seddon, 1997; Fred Davis, 1989), or effectiveness (Gelinas, 2012), or user satisfaction (Stair & Reynoalds,

2010), and / or include the term quality (Sacer et al, 2006:62) itself. DeLone and McLeans model is one of the

information system success models. These authors aimed to synthesize the previous research on information

system success and present a more coherent basis for future research (DeLone and McLean, 2003). In their

model, DeLone and McLean (1992) proposed that the success of information systems is determined by the

information system quality (the technical quality of the system) and the output quality of the information

system (the quality of information produced). These dimensions influence the use level and user response to

the information system (user satisfaction). As a result, the user attitude (individual impact) and organizational

performance (organizational impact) are influenced (Azhar Susanto, 2008:374 ; Sacer et al, 2006:6 ; DeLone,

et al, 2003 ; Stacie Petter, 2008 ; Ralph, et al, 2010:57 ; Laudon, et al, 2012:548 ; Todd, 2005:85)

2.3.Organizational Structure

Organizational structure is the formal system of task and authority relationships that control how

people coordinate their actions and use resources to achieve organizational goals (Jones Gareth, 2010:29).

Organizational structure is formally dictated on how jobs and tasks are distributed and coordinated between

individuals and groups within the company. One way of getting a feel for an organizational structure is by

www.ijbmi.org

13 | Page

The Accounting Information Quality And The

looking at an organizational chart. An organizational chart is a drawing that represents every job in the

organization and the formal reporting relationships between those jobs. It helps organizational members and

outsiders understand and comprehend how work is structures within the company (Colquit et al, 2011: 257).

The dimension and indicator of organizational structure used in the study are: work specialization which is

dividing work activities into separate job task (Robbins and Coulter, 2009:201 ; Colquitt et al., 2011:528;

Robbins and Judge, 2011:214; Schermerhorn et al., 2005:384; Gibson et al., 2006); span of control is the

number of employees a manager can efficiently and effectively manage (Robbins and Coulter, 2009:203 ;

Colquitt et al., 2011:528; Schermerhorn et al., 2005:386; Robbins and Judge, 2011:214; Gibson et al., 2006);

chain of command is the line of authority extending from upper organizational levels to lower levels, which

clarifies who reports to whom (Robbins and Coulter, 2009:203 ; Colquitt et al., 2011:528; Robbins and Judge,

2011:214); formalization refers to how standardized an organizations jobs are and the extend to which

employee behaviour is guided by rules and procedures (Robbins and Coulter, 2009:205 ; Colquitt et al.,

2011:528; Robbins and Judge, 2011:214; Schermerhorn et al., 2005:390); delegation (centralization and

decentralization), centralization is the degree to which decisions making takes place at upper levels of the

organization, on the other hand, the more that lower level employees provide input or actually make decisions,

the more decentralization there is. (Robbins and Coulter, 2009:204 ; Colquitt et al., 2011:528; Robbins and

Judge, 2011:214; Gibson et al., 2006; Schermerhorn et al., 2005:392).

III.

THEORETICAL FRAMEWORK

3.1 Organizational Structure and Accounting Information System Quality

Accounting information system is influenced by organizational structure. Scott (2001:6) stated the

organizations structure is effect on information system. Hierarchical organizational structure that contain a

basic framework information system was built, because the system is built to circulate information in

accordance with the information in a hierarchical organizational structure. The greater the organizational

structure of the layer hierarchy will increasingly complex information systems are built, in addition to the span

of control within the organizational structure also affects information system. Laudon, et al (2012:23) explain

that other features of organizations include their business processes, organization culture, organizational politics,

surrounding environments, organizational structures, goals, constituencies and leadership style. All of these

features affect the kind of information systems used by organizations. This is supported by the result of study

Stacie, et al (2008); Mc Leod, et al (2007); Yarmohammadzadeh, et al (2011). Following the results of their

studies, the organizational structure significantly contributes to the effectiveness of accounting information

system.

3.3 Accounting Information System Quality and Accounting Information Quality

The accounting information quality is influenced by the accounting information system quality.

Wongsim, et al (2011) stated that information quality dimensions have a positive relationship with accounting

information system adoption processes. Furthermore, information quality dimensions play a vital role in the

process of AIS adoption. Next, Sacer, et al (2006) explain that the connection between an AIS and business

reporting on the basis of characteristic of quality information. The same with Onaolapo (2012) explain that

benefits of accounting information system can be evaluated by its impacts on improvement of decision making

process, quality of accounting information, performance evaluation, internal controls and facilitating companys

transactions. The purpose of an accounting information system is to produce financial statements designated for

both external and internal users (Scott, 2001). This is supported by the result of the study showing that

accounting information system enhances the truth of financial statements (Salehi et al., 2010). Thus, it is

concluded that there is a relationship between accounting information system to report on the basis of

information quality characteristics (Sacer et al., 2006). Nicolaou (2000) states, that the effectiveness of the

accounting information system is measured by the satisfaction of the decision makers on the information quality

produced by the accounting information system quality.

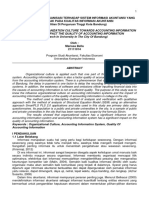

Study Models and Hypothesis

Based on the prior literature discussion, the conceptual model is shown in figure below :

www.ijbmi.org

14 | Page

The Accounting Information Quality And The

Organizational Structure

Accounting

Information System

Quality

(Colquitt et al., 2011:528; dan Judge,

2011:522; Gibson et al., 2001;;

Schermerhorn et al., 2005:392 ; McShane

et al, 2010:390)

(McDelon dan McLean, 1992 ; Straub et

al, 1995 ; Gelderman, 1988 ; Romney

and Steinbart, 2012:6 ; Azhar

Susanto,2008 ; Laudon dan Laudon,

2008 ; Bodnar and Hopwood , 2004:3)

H1

(Laudon, 2007:19; Taylan,2010 ;

Meade, 2002 ; Mahdi, 2011 ; Bodnar,

2010:23 ; Doll, 2001 ; Laudon, 2010:23

; Scott, 2001:6 ; Nagappan,2009:1 ;

Doms, 2004; Claver, 2001 ; Wanyama,

2010 ; Ismail, 2007 ; Yarmohammad,

2011 ; Fred, 2012

Accounting

Information

Quality

H2

( OBrien, 2008 : 261; Mc.

Leod & Schell (2007:35) ;

Shipper (2003) ; Kahn et al

(2002)

(Azhar,2009:6;Shebab,2004;McLeod,20

07:14;Ludon,2007:14;Wongsin,2011;Iva

na,2006;Ponte,2000;Onaolapo,2012;Ali,

2011;Siamak,2012

Figure 1 : Theoretical framework of the study

To sum up, the study is aimed to determine the causal relationship between variables through tested hypothesis.

Hypothesis 1

: The accounting information system quality is significantly influenced by organizational

structure.

Hypothesis 2

: The accounting information quality is significantly influenced by accounting information

system quality.

IV.

METHODOLOGY

The research objects are the organizational structure, the accounting information quality and the

accounting information system quality. Research methodology used in this study is method of survey with

questionnaires as a tool. The units of analysis of the study are forty seven (47) Baitulmal Wattamwil (BMT) in

West Java Indonesia. The study focuses on applying accounting information system quality and survey

conducted on the units of analysis. Numbers of questionnaires are distributed to each company, one copy for

one company. Respondents of this study are the leaders of management companies of the Baitulmal Wattamwil

(BMT). The questionnaires are manipulated based on indicators using a Likerts summated rating. The

questionnaires use closed questions format serving answered choices for variables that have clear indicators

measured. Data analysis conducted in this study is descriptive and verificative. The

answers

from

the

respondents were treated as data and processed by statistical measures. The sincerity of the respondents

answers is crucial; therefore, the data were tested through a test of validity and reliability. Then, in order to

analyze the data statistically, the ordinal data must be transformed into interval data using the successive interval

method. The data will be analized is by using path analysis with consideration of the pattern of relationships

between variables that are correlative, causality and recursive. Each hypothesis to be tested by a statistical t test :

Ho is rejected if t account > t critical, = 0.05 level.

V.

CONCLUSSION

The model developed in this study may explain the influences of the organizational structure on the

accounting information system quality and the accounting information quality. The results of this study later, is

specifically will show that the organizational structure implemented in Baitulmal Wattamwil (BMT) have

significant effects on the accounting information system quality. Finally, the accounting information system

quality gives influence to the accounting information quality. It means that, to reach accounting information

quality, Baitulmal Wattamwil (BMT) must be supported by qualified accounting information system.

Accordingly, the financial statements of the Baitulmal Wattamwil (BMT) can be provided in accordance with

high quality standards.

www.ijbmi.org

15 | Page

The Accounting Information Quality And The

REFERENCES

[1]

[2]

[3]

[4]

[5]

[6]

[7]

[8]

[9]

[10]

[11]

[12]

[13]

[14]

[15]

[16]

[17]

[18]

[19]

[20]

[21]

[22]

[23]

[24]

[25]

[26]

[27]

[28]

[29]

[30]

[31]

[32]

[33]

[34]

[35]

[36]

[37]

[38]

[39]

[40]

[41]

Agus Martowardojo. (2010). Agus Marto Beberkan Kelemahan di Ditjen Pajak. www.buletininfo.com.

Ali Alzoubi. (2011). The Effectiveness of The Accounting Information Systems Under The Enterprise Resources Planning (ERP).

Research Journal of Finance and Accounting. Vo. 2. No. 11. Pp. 10-19.

Ang, C.L Davies, M. A., Finlay, P.N. (2001). An Empirical Model of IT Usage in The Malaysian Public Sector. Journal of

Strategic Information Systems, 10, 159-174.

Anwar Nasution.(2007). BPK : Krisis Keuangan Global Harus Jadi Pelajaran. www.tempo.co.

Azhar Susanto. (2008). Sistem Informasi Akuntansi, Struktur-Pengendalian-Resiko-Pengembangan. Bandung : Lingga Jaya.

Bodnar, George H, Hopwood William S. (2010). Accounting Information System. Prentice Hall, Inc New Jersey.

Colquit, Jason A., Lepine, Jeffery A., Wesson, Michael J. (2011). Organizational behavior: Improving Performance and

Commitment in the Workplace. New York: McGraw Hill/Irwin. International Edition.

Dahlan Iskan. (2012). Dahlan : Dokumen BUMN Banyak Yang Bermasalah. http://antaranews.com.

DeLone, W. H and McLean, E. R. (1992). Information System Success : The Quest of The Dependent Variable. Information

Systems Research. Vol. 3. Pp. 60-95.

DeLone, W. H and McLean, E. R. (2003). The DeLone and McLean Model of Information System Succes : A Ten Years Update.

Journal of Management Information System. 19(4). Pp. 3-30.

Doll, Wiliam and Xiadong Deng. (2001). The Collaborative Use of Information Technology : End User Participation and System

Succes. Information Resources Management Journals. ABI/INFORM Global.

Doms, M. E. Jarmin R. S and Klimerk, S. D. (2004). Information Technology Invesment anfd Firm Performance in U.S Retail

Trade. Economics of Innovation and New Technology. 13. 7. 596-613.

Eppler, M. J. (2003). Managing Information Quality: Increasing the Value of Information in Knowledge-Intensive Products and

Processes. Heidelberg/New York: Springer.

Fontaine, Craig W. (2007). Organizational Structure: A Critical Factor for Organizational effectiveness and Employee

Satisfaction. First Annual Conference on Organizational Effectiveness, Chicago, IL. Northeastern University.

Fred C. Lunenburg. (2012). Organizational Structure : Mintbergs Framework. International Journal of Scholarly Academic

Intellectual Diversity.

Fred Davis. (1989). Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS

Quartely, 13, September, Pp. 319-340

Claver, E., Llopis, J., Gonzalez, MR. (2001). The Performance of Information Systems through Organizational Culture. ua.

Emeraldinsight.com.aqf

Gibson, J. L., et al. (2006). Organizations Behevior, Structure, Processes (13th ed). New York: McGraw-Hill.

Gelinas U, A. Oram & W. Wriggins. (1990). Accounting Information Systems. Boston: Pwskent Publishing Company.

Gelinas, Ulric J, Dull, Richard B, Wheeler, Patrick R. (2012). Accounting Information System. 9 Th Edition. South Western

Cengage Learning. USA.

Gelderman, M. (1998). The Relation Between User Satisfaction, Usage of Information Systems and Performance. Information and

Management. 34. Pp. 11-18.

Gibson, J. L., Ivanicevic, J. M., Donelly, J. H., & Konopaske, Robert. (2006). Organizations Behevior, Structure, Processes

(13th ed). New York: McGraw-Hill.

Hadi Poernomo. (2012). Sumatera Utara : BPK Sepakat Bangun Sistem E-Audit. http://indonesia.go.id.

Indeje, Wanyama G., dan Zheng, Qin. (2010). Organizational Culture and Information Systems Implementation: A Structuration

Theory Perspective. Working Papers on Information Systems ISSN 1535-6078 10(27). http://sprouts.aisnet.org/10-27

Ismail, Adel Al-Alawi, Nayla Yousif Al-Marzookqi, Yasmeen Fraidoon Mohammed. (2007). Organizational Culture and

Knowledge Sharing : Critical Success Factors. Journal of Knowledge Management.

Ivana Mamic Sacer, Katarina Zager, Boris Tusek. (2006). Accounting Information Systems Qualityas The Groundfor Quality

Business Reporting. IADIS International Conferencee-Commerce 2006

Jones, Gareth. (2010). Organizational Theory, Design and Change. Sixth Edition. Pearson Education. Inc. Upper Saddle River.

New Jersey.

Kahn, B. K., Strong, D. M., & Wang, R. Y. (2002).Information Quality Benchmarks: Product and Service Performance.

Communications of the ACM, 45(4ve), 185.

Kieso, Donald E., et al. (2012). Intermediate Accounting. 14th Edition. UK: John Willey and Sons, Inc.

Laudon, Kenneth C., et al.. (2012). Management Information Systems : Managing The Digital Firm. 12th Edition. NJ : Prentice

Hall.

Mahdi Salehi, Vahab Rostami and Abdolkarim Mogadam. (2010). Usefulness of Accounting Information System in Emerging

Economy : Empirical Evidence of Iran. International Journal of Economics and Finance Vo. 2, No. 2.

Mahdi, Salehi, and Abdipour, Abdoreza. (2011). A Study of The Barriers of Implementation of Accounting Information System:

Case of Listed Companies in Tehran Stock Exchange.

Mc. Leod, Raymond and Schell, George P. (2007). Management Information System. Tenth Edition. Upper Saddle River New

Jersey 07458 : Pearson/Prentice Hall.

McShane and Von Glinov. (2010). Organizational Behaviour. Fifth Edition. McGraw-Hill International Edition.

Meade, L. and A. Presley. (2002). R and D Project Selection Using The Analytic Network Process. IEEE Transactions on

Engineering Management. 49. 1-8.

Nagappan et al. (2009). The Influence of Organizational Structure on Software Quality : an Empirical Case Study

leeexplore.ieee.org/iel5/481410.

Nicolaou Andreas I. (2000). A Contingency Model of Perceived Effectiveness in Accounting Information Systems:

Organizational Coordination and Control Effects. International Journal of Accounting Information Systems, Vol:1, Issue 2,

September 200, p 91-105.

OBrien , James A., et al. (2008). Management Information System. Eight Edition. NY: McGraw-Hill.

Onaolapo A.A and Odetayo T.A. (2012). Effect of Accounting Information System on Organisational Effectiveness : A Case Study

of Selected Construction Companies in Ibadan Nigeria. American Journal of Business and Management. Vol. 1. No. 4. 2012.

183-189.

Ramlah Hussein, Norshidah Mohamed, Nor Shahriza Abdul Karim, Abdul Rahman Ahlan. (2009). The Influences

Organizational Factors on Information System Succes in E-Government Agencies in Malaysia. The Electronic Journal of

Information System in Developing Countries. http://www.ejisdc.org.

Robbins, Stephen P., et al. (2009). Management. 9th Edition. Pearson Education. Prentice Hall.

www.ijbmi.org

16 | Page

The Accounting Information Quality And The

[42]

[43]

[44]

[45]

[46]

[47]

[48]

[49]

[50]

[51]

[52]

[53]

[54]

[55]

[56]

[57]

[58]

[59]

Robbins, Stephen, et al. (2011). Organizational Behaviour. 14th Edition. Pearson Education. Prentice Hall.

Romney, Marshall B., dan Steinbart, paul J. (2012). Accounting Information Systems. Global Edition. Twelfth Edition. England:

Pearson Education Limited

Sacer, Ivana M., Zager K., and Tusek B. (2006). Accounting Information Systems Quality as The Ground For Quality Business

Reporting. IADIS International Conference e-commerce, ISBN :972-8924-23-2.

Schermerhorn, John R., et al. (2005). Organizational Behavior. John wiley & Sons, Inc.

Scott, George M. (2001). Principles of Management Information System. New York : McGraw-Hill,Inc

Seddon, P.B. (1997). Information System Research, Vol. 8 No. 3, Pp. 240-253Shipper, K and Vincent, L. (2003). Earning

Quality. Accounting Horizons, Supplemen, 97-110.Stacie Petter, William DeLone, Ephraim McLean. (2008). Measuring

information system succes : models, dimension, measures, and Interrelationships. European Journal of Information System.

Siamak Nejadhosseini Soudani. (2012). The Uselfulness of An Accountng Information System for Effective Organizational

Performance. International Journal of Economics and Finance. Vol. 4. No. 5. May 2012. Pp. 136-143.

Stair M, and George W. Reynolds. (2010). Principles of Information Systems, Course Technology, 9 th ed., Editions. NY: McGraw-Hill.

Straub et al. (1995). Measuring System Usage : Implications for IS Theory Testing. Management Science. 41 (8). Pp. 1328-1342.

Suri, Gunmala. (2005). Organizational Culture in ICT Implementation and Knowledge Management in Spanish and Indian

Universities: A Conceptual Model. Computer Society of India . www.csi-sigegof.org/3/1_280_3.pdf

Taylan, Osman, PhD. (2010). The Effect of Information Systems on Enterprise Transformation and Organizational Behavior.

Canadian Journal on Data, Information and Knowledge Engineering Vol. 1, No. 1

Todd. (2005). A Theoritical Integration of User Satisfaction and Technology Acceptance. Information Sytems Research. Vol.16, No.1, March

2005, pp.85-102. ISSN 1047-7047

Wanyama G. Indeje and Qin Zheng. (2010). Organization Culture and Information Systems Implementation : A Structuration

Theory Perspective. Sprouts : Working Papers on Information Systems.

Wongsim, M., & Gao, J. (2011). Exploring Information Quality in Accounting Information System Adoption. IBIMA Publishing,

2011(2011), 1-12.

Xu, Hongjiang. Nord G.D. and Lin, B (2003). Key Issues Accounting Information Quality Management : Australian Case

Studies. Industrial Management and Data System.

Yarmohammad Zahed. (2011). The Analysis of The Relationship Between Organizational Structure and Information Technology

(IT) : And The Barriers to Its Establishment at The University of Isfahan from The Faculty Members Viewpoints.

Yarmohammadzadeh, Peyman, Alammeh Sayyed Mohsen, Ghalavandi Hassan, Farhang Aboulghassim, Ajdari Zaman. (2011).

The Analysis of The Relationship between Organizational Structure and Information Technology (IT) : And The Barriers to Its

Establishment at The University of Isfahan from The Faculty Members Viewpoints. Higher Education Studies.

Zimmerman JL. (1995). Accounting for Decision Making and Control. Chicago : Irwin.

www.ijbmi.org

17 | Page

S-ar putea să vă placă și

- 5659 7766 1 PBDocument6 pagini5659 7766 1 PBFajar RamadhanÎncă nu există evaluări

- Data Governance: Building a Foundation for Data ExcellenceDe la EverandData Governance: Building a Foundation for Data ExcellenceÎncă nu există evaluări

- Accoun NG and Finance Review: Yenni CarolinaDocument6 paginiAccoun NG and Finance Review: Yenni CarolinaJulia MirhanÎncă nu există evaluări

- The Quality of Accounting Information and The Quality of Accounting Information Systems Through The Internal Control SystemDocument14 paginiThe Quality of Accounting Information and The Quality of Accounting Information Systems Through The Internal Control SystemJuang MandbestÎncă nu există evaluări

- Fitrios2016FactorsThatInfluenceAISImplement AIQIJSTRDocument8 paginiFitrios2016FactorsThatInfluenceAISImplement AIQIJSTRVanesa Amalia DuatiÎncă nu există evaluări

- FITRIOSDocument8 paginiFITRIOSsoniaÎncă nu există evaluări

- Determining Business Intelligence Usage SuccessDocument23 paginiDetermining Business Intelligence Usage SuccessAnonymous Gl4IRRjzNÎncă nu există evaluări

- Factors Affecting The Quality of AccountDocument8 paginiFactors Affecting The Quality of Accounthanlgcs180659Încă nu există evaluări

- Jurnal 2 Selesai (PDF - Io)Document8 paginiJurnal 2 Selesai (PDF - Io)Ilhamputra287Încă nu există evaluări

- Quality Services 1Document4 paginiQuality Services 1Rwnw CorahuaÎncă nu există evaluări

- INFLUENCE OF USER ABILITY ON THE QUALITY OF AIS - MeiryaniDocument11 paginiINFLUENCE OF USER ABILITY ON THE QUALITY OF AIS - MeiryaniJang JubÎncă nu există evaluări

- Analysis of Factors Affecting The SuccesDocument8 paginiAnalysis of Factors Affecting The Succeshanlgcs180659Încă nu există evaluări

- Cause and Effect of Accounting Information SystemDocument8 paginiCause and Effect of Accounting Information SystemAsfa AsfiaÎncă nu există evaluări

- 270182192Document18 pagini270182192Angela CabanaÎncă nu există evaluări

- 90dd PDFDocument5 pagini90dd PDFMarjorie Zara CustodioÎncă nu există evaluări

- The Impact of Automated EmployeesDocument12 paginiThe Impact of Automated EmployeesMarie Laurice BadillaÎncă nu există evaluări

- Effect of Management Information SystemDocument23 paginiEffect of Management Information Systemsujata bhartiÎncă nu există evaluări

- 1 s2.0 S2212567115014768 MainDocument6 pagini1 s2.0 S2212567115014768 MainTinasheÎncă nu există evaluări

- Management Information Systems and Corporate Decision - Making: A Literature ReviewDocument5 paginiManagement Information Systems and Corporate Decision - Making: A Literature Reviewvaaz205Încă nu există evaluări

- Firm Size, Business Sector and Quality of Accounting Information SystemDocument8 paginiFirm Size, Business Sector and Quality of Accounting Information SystemHoàng AnhÎncă nu există evaluări

- User Technical Capability Moderate The Effect Computer - Based Accounting Information System On Individual PerformanceDocument8 paginiUser Technical Capability Moderate The Effect Computer - Based Accounting Information System On Individual PerformanceHerna TobingÎncă nu există evaluări

- 50781-54483-1-PBDocument8 pagini50781-54483-1-PBDedhy Senjha AdhiansyahÎncă nu există evaluări

- 13-Article Text-66-1-10-20201210Document10 pagini13-Article Text-66-1-10-20201210Jam HailÎncă nu există evaluări

- Jurnal 3Document7 paginiJurnal 3Ahmad Taufik, M.Kom. UndiraÎncă nu există evaluări

- Review of LiteratureDocument11 paginiReview of LiteratureSapkota ArjunÎncă nu există evaluări

- The Effect of Information Technology On The Quality of Accounting Information System and Its Impact On The Quality of Accounting InformationDocument8 paginiThe Effect of Information Technology On The Quality of Accounting Information System and Its Impact On The Quality of Accounting InformationAlexander DeckerÎncă nu există evaluări

- Indikator Partisipàsi Pengguna 1 PDFDocument16 paginiIndikator Partisipàsi Pengguna 1 PDFansandrynÎncă nu există evaluări

- Accounting Info and Financial PerformanceDocument61 paginiAccounting Info and Financial PerformancevitalisÎncă nu există evaluări

- Jurnal Internasional IBM11!3!5523 5529XXXXXXDocument7 paginiJurnal Internasional IBM11!3!5523 5529XXXXXXLidya SÎncă nu există evaluări

- 10 5923 J Economics 20130301 06 PDFDocument5 pagini10 5923 J Economics 20130301 06 PDFSambas KesumaÎncă nu există evaluări

- Computerised Accounting Information Systems Lessons in State-Owned Enterprise in Developing Economies PDFDocument23 paginiComputerised Accounting Information Systems Lessons in State-Owned Enterprise in Developing Economies PDFjcgutz3Încă nu există evaluări

- J 1 The Usefulness of An Accounting Information System For Effective Organizational PerformanceDocument11 paginiJ 1 The Usefulness of An Accounting Information System For Effective Organizational PerformanceRizqi Irma OktaviÎncă nu există evaluări

- Article 1Document6 paginiArticle 1Nor Masidayu Binti Mat ZinÎncă nu există evaluări

- The Role of AIS Success On Accounting Information Quality: Azmi Fitriati, Naelati Tubastuvi, Subuh AnggoroDocument9 paginiThe Role of AIS Success On Accounting Information Quality: Azmi Fitriati, Naelati Tubastuvi, Subuh AnggoroThe Ijbmt100% (1)

- Evaluation of The Effectiveness of Accounting Information SystemsDocument11 paginiEvaluation of The Effectiveness of Accounting Information SystemsHA DIÎncă nu există evaluări

- 89-Article Text-123-1-10-20181028Document8 pagini89-Article Text-123-1-10-20181028Deus MalimaÎncă nu există evaluări

- Group7 Bsa 3L Importance of Accounting Information System Ais To The Management Decision MakingDocument34 paginiGroup7 Bsa 3L Importance of Accounting Information System Ais To The Management Decision MakingCristy Martin YumulÎncă nu există evaluări

- Factorsthat Affect Accounting Information System Implementationand Accounting Information Quality ASurveyin University Utara MalaysiaDocument6 paginiFactorsthat Affect Accounting Information System Implementationand Accounting Information Quality ASurveyin University Utara MalaysiaJang JubÎncă nu există evaluări

- Mis Group 6 Assignment 1Document10 paginiMis Group 6 Assignment 1Ry NielÎncă nu există evaluări

- Tinaporwal,+23 IJRG18 A07 1546Document6 paginiTinaporwal,+23 IJRG18 A07 1546Bulelwa HarrisÎncă nu există evaluări

- IJRPR3130Document6 paginiIJRPR3130Werpa PetmaluÎncă nu există evaluări

- Reconceptualising The Information System As A Service (Research in Progress)Document12 paginiReconceptualising The Information System As A Service (Research in Progress)AldimIrfaniVikriÎncă nu există evaluări

- Inf Quality and AkMen DSS ImplementationDocument5 paginiInf Quality and AkMen DSS ImplementationveccoÎncă nu există evaluări

- The Usefulness of An Accounting Information System For Effective Organizational PerformanceDocument11 paginiThe Usefulness of An Accounting Information System For Effective Organizational PerformanceSierra.Încă nu există evaluări

- 37-Research Paper-1161-1-10-20220717Document11 pagini37-Research Paper-1161-1-10-20220717Fir MalÎncă nu există evaluări

- I J C R B: Dr. Amir Hossein Amir Khani Dr. Ali Rostami Ali NaseriDocument14 paginiI J C R B: Dr. Amir Hossein Amir Khani Dr. Ali Rostami Ali NaseriTolulope AbiodunÎncă nu există evaluări

- 1 Chapter 1Document9 pagini1 Chapter 1Shyne MonteverdÎncă nu există evaluări

- IT InfrastructureDocument9 paginiIT InfrastructurewilberÎncă nu există evaluări

- Impact of Accounting Information Systems (AIS) On Organizational Performance A Case Study of TATA Consultancy Services (TCS) - IndiaDocument8 paginiImpact of Accounting Information Systems (AIS) On Organizational Performance A Case Study of TATA Consultancy Services (TCS) - IndiaHerna TobingÎncă nu există evaluări

- Influence of Information Systems On Organizational ResultsDocument18 paginiInfluence of Information Systems On Organizational ResultsAlessandro LangellaÎncă nu există evaluări

- Enterprise Resource Planning (ERP) Dan Knowledge Terhadap Impact Organisasi Di RiauDocument18 paginiEnterprise Resource Planning (ERP) Dan Knowledge Terhadap Impact Organisasi Di Riaujifri syamÎncă nu există evaluări

- How IT Controls Improve The Control EnvironmentDocument18 paginiHow IT Controls Improve The Control EnvironmentMichele LangÎncă nu există evaluări

- 2 Chapter 2Document14 pagini2 Chapter 2Guess what happened masterÎncă nu există evaluări

- IJABERDocument28 paginiIJABERJy MainzaÎncă nu există evaluări

- Influence of Information Systems On Organizational ResultsDocument18 paginiInfluence of Information Systems On Organizational ResultsMauser Acuña sotoÎncă nu există evaluări

- Jbptunikompp GDL Marissabel 33395 1 Unikom - M LDocument16 paginiJbptunikompp GDL Marissabel 33395 1 Unikom - M LHerly KurniatiÎncă nu există evaluări

- 2 - AlnajjarDocument19 pagini2 - AlnajjarWHILSA PUTRA MUTHIÎncă nu există evaluări

- 09 Quang Linh Huynh-PDocument13 pagini09 Quang Linh Huynh-PFahmi AbdullaÎncă nu există evaluări

- The Impact of Accounting Information System in Decision Making Process in Local Non-Governmental Organization in Ethiopia in Case of Wolaita Development Association, SNNPR, EthiopiaDocument5 paginiThe Impact of Accounting Information System in Decision Making Process in Local Non-Governmental Organization in Ethiopia in Case of Wolaita Development Association, SNNPR, EthiopiaEmesiani TobennaÎncă nu există evaluări

- Effects of Online Marketing On The Behaviour of Consumers in Selected Online Companies in Owerri, Imo State - NigeriaDocument12 paginiEffects of Online Marketing On The Behaviour of Consumers in Selected Online Companies in Owerri, Imo State - Nigeriainventionjournals100% (1)

- A Critical Survey of The MahabhartaDocument2 paginiA Critical Survey of The MahabhartainventionjournalsÎncă nu există evaluări

- Student Engagement: A Comparative Analysis of Traditional and Nontradional Students Attending Historically Black Colleges and UniversitiesDocument12 paginiStudent Engagement: A Comparative Analysis of Traditional and Nontradional Students Attending Historically Black Colleges and Universitiesinventionjournals100% (1)

- Non-Linear Analysis of Steel Frames Subjected To Seismic ForceDocument12 paginiNon-Linear Analysis of Steel Frames Subjected To Seismic ForceinventionjournalsÎncă nu există evaluări

- Effect of P-Delta Due To Different Eccentricities in Tall StructuresDocument8 paginiEffect of P-Delta Due To Different Eccentricities in Tall StructuresinventionjournalsÎncă nu există evaluări

- Immobilization and Death of Bacteria by Flora Seal Microbial SealantDocument6 paginiImmobilization and Death of Bacteria by Flora Seal Microbial SealantinventionjournalsÎncă nu există evaluări

- Inter-Caste or Inter-Religious Marriages and Honour Related Violence in IndiaDocument5 paginiInter-Caste or Inter-Religious Marriages and Honour Related Violence in IndiainventionjournalsÎncă nu există evaluări