S-ar putea să vă placă și

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Revenue and Expenditure CycleDocument13 paginiRevenue and Expenditure CycleKent NiceÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Revenue and Expenditure CycleDocument13 paginiRevenue and Expenditure CycleKent NiceÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Revenue and Expenditure CycleDocument13 paginiRevenue and Expenditure CycleKent NiceÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Topic 1 Decision Analysis Chapter 3Document54 paginiTopic 1 Decision Analysis Chapter 3Kent Nice100% (4)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- Topic 1 Decision Analysis Chapter 3Document54 paginiTopic 1 Decision Analysis Chapter 3Kent Nice100% (4)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Global WarmingDocument5 paginiGlobal WarmingKent NiceÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Bpi v. de CosterDocument2 paginiBpi v. de CosterRuperto A. Alfafara III100% (2)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Prudential Guarantee and Assurance Inc., vs. Trans-Asia Shipping Lines Inc, G.R. No. 151890 June 20, 2006 (Full Text and Digest)Document14 paginiPrudential Guarantee and Assurance Inc., vs. Trans-Asia Shipping Lines Inc, G.R. No. 151890 June 20, 2006 (Full Text and Digest)RhoddickMagrataÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Impact of GST On LogisticsDocument18 paginiImpact of GST On LogisticsSharath ReddyÎncă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- COmplaint Management System by RBIDocument2 paginiCOmplaint Management System by RBIsudhir guptaÎncă nu există evaluări

- Nadi Chamber of Commerce & Industry (NCCI) Asia Development Bank 52nd Annual Meeting MagazineDocument19 paginiNadi Chamber of Commerce & Industry (NCCI) Asia Development Bank 52nd Annual Meeting MagazineNadi Chamber of Commerce and IndustryÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Housing Finance in BangladeshDocument13 paginiHousing Finance in BangladeshShah Muhammed Bodrul HasanÎncă nu există evaluări

- TV 1 V 25Document33 paginiTV 1 V 25ahmadhatakeÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Monitoring Harian JuniDocument229 paginiMonitoring Harian JuniFitri AniÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Copia de Default of Credit Card ClientsDocument2.196 paginiCopia de Default of Credit Card Clientsricardipineda80Încă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- SHFL Posting With AddressDocument8 paginiSHFL Posting With AddressPrachi diwateÎncă nu există evaluări

- Debt Recovery Management of SBIDocument12 paginiDebt Recovery Management of SBIDipanjan DasÎncă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- StatementDocument2 paginiStatementliangill1Încă nu există evaluări

- Analysis of Credit Proposal For Corporate Banking Division of BRAC Bank LimitedDocument66 paginiAnalysis of Credit Proposal For Corporate Banking Division of BRAC Bank LimitedGere TassewÎncă nu există evaluări

- Chapter 29. Powers Authority of The Commissioner of Internal RevenueDocument5 paginiChapter 29. Powers Authority of The Commissioner of Internal RevenuePrincess Edelyn CastorÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Mortgage Comparison WorksheetDocument3 paginiMortgage Comparison WorksheetNancy SuárezÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Oriental Insurance Company LimitedDocument3 paginiThe Oriental Insurance Company Limitedpooja boraÎncă nu există evaluări

- Anti-Money Laundering (AML) - Cases Involving Capital Market ParticipantsDocument3 paginiAnti-Money Laundering (AML) - Cases Involving Capital Market ParticipantsVia Commerce Sdn BhdÎncă nu există evaluări

- Accounting BasicsDocument42 paginiAccounting Basicssowmithra4uÎncă nu există evaluări

- Indemsure - Processes and Procedures PDFDocument95 paginiIndemsure - Processes and Procedures PDFYudi SuyantoÎncă nu există evaluări

- Bank ReconciliationDocument2 paginiBank Reconciliationapi-3727562Încă nu există evaluări

- The ManagerDocument1 paginăThe ManagerKhaled SherifÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Taxation - Questions Sepr 2012Document17 paginiTaxation - Questions Sepr 2012kannadhassÎncă nu există evaluări

- 138 NI ACT DissertationDocument98 pagini138 NI ACT DissertationSahil Chawla71% (7)

- Simple and Compound InterestDocument2 paginiSimple and Compound InterestJeffrey Del MundoÎncă nu există evaluări

- Manipur Bank Branches ListDocument17 paginiManipur Bank Branches ListKhundrakpam SatyabartaÎncă nu există evaluări

- CTT January 18 ExamDocument5 paginiCTT January 18 ExamAie GeraldinoÎncă nu există evaluări

- Liberty Secure Travel Plan Details: Cover Sum InsuredDocument1 paginăLiberty Secure Travel Plan Details: Cover Sum InsuredMeghaÎncă nu există evaluări

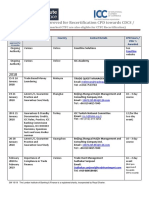

- 2018/19 - Courses Approved For Recertification CPD Towards CDCSDocument29 pagini2018/19 - Courses Approved For Recertification CPD Towards CDCSMunshi Masudur RahamanÎncă nu există evaluări

- Form No.: Form No.: Issue Date: Form No.: Issue Date: Program: Program: Due Date: Program: Due Date: Semester: Semester: Expiry Date: Semester: Expiry Date: Due Date: Issue DateDocument1 paginăForm No.: Form No.: Issue Date: Form No.: Issue Date: Program: Program: Due Date: Program: Due Date: Semester: Semester: Expiry Date: Semester: Expiry Date: Due Date: Issue Dateowaisyaqoob29Încă nu există evaluări

- Ibs Bandar Tenggara SC 1 31/12/21Document20 paginiIbs Bandar Tenggara SC 1 31/12/21Ary PotterÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)