S-ar putea să vă placă și

- TaxationBarQ26A TaxRemediesDocument32 paginiTaxationBarQ26A TaxRemediesjuneson agustinÎncă nu există evaluări

- Election Cases Land Registration Cases Cadastral Naturalization Insolvency Proceedings Other Cases Not Provided ForDocument139 paginiElection Cases Land Registration Cases Cadastral Naturalization Insolvency Proceedings Other Cases Not Provided ForIvan LeeÎncă nu există evaluări

- 2016 Tax 2 Bar Q&ADocument3 pagini2016 Tax 2 Bar Q&Achristine100% (1)

- Dasco Vs PhiltrancoDocument14 paginiDasco Vs PhiltrancocyhaaangelaaaÎncă nu există evaluări

- Remedies Under The Tax Code of 1997Document7 paginiRemedies Under The Tax Code of 1997mnyngÎncă nu există evaluări

- Toshiba Vs CIRDocument3 paginiToshiba Vs CIRKim Patrick DayosÎncă nu există evaluări

- Remedies For National Taxes Period Reckoning DayDocument4 paginiRemedies For National Taxes Period Reckoning DayAnn SaturayÎncă nu există evaluări

- How To Create A CorporationDocument2 paginiHow To Create A Corporationicecyst888Încă nu există evaluări

- 7 ABS-CBN Broadcasting Corp. v. NazarenoDocument27 pagini7 ABS-CBN Broadcasting Corp. v. NazarenoCristelle FenisÎncă nu există evaluări

- CIR Vs MenguitoDocument1 paginăCIR Vs MenguitokoeyÎncă nu există evaluări

- FRIA DoctrinesDocument4 paginiFRIA DoctrinesFG FGÎncă nu există evaluări

- Dario VS MisonDocument2 paginiDario VS MisonJose Ramir Layese100% (1)

- Contex Corporation vs. CIR Persons LiableDocument16 paginiContex Corporation vs. CIR Persons LiableEvan NervezaÎncă nu există evaluări

- LOZADA Vs MENDOZA - LASHERASDocument3 paginiLOZADA Vs MENDOZA - LASHERASMARRYROSE LASHERASÎncă nu există evaluări

- Enriquez Security Services, Inc. vs. CabotajeDocument5 paginiEnriquez Security Services, Inc. vs. CabotajeAaron CariñoÎncă nu există evaluări

- Aoi Walang ForeverDocument6 paginiAoi Walang ForeverJuris PoetÎncă nu există evaluări

- Caltex (Phils.), Inc. v. PNOC Shipping and Transport Corp., 498 SCRA 400 (2006)Document29 paginiCaltex (Phils.), Inc. v. PNOC Shipping and Transport Corp., 498 SCRA 400 (2006)inno KalÎncă nu există evaluări

- Cruz v. Dalisay DigestDocument1 paginăCruz v. Dalisay DigestKimberly SisonÎncă nu există evaluări

- Petitioner vs. vs. Respondent: Second DivisionDocument7 paginiPetitioner vs. vs. Respondent: Second DivisionJuleen Evette MallariÎncă nu există evaluări

- Jurisdiction of Cta Enbanc and DivisionDocument12 paginiJurisdiction of Cta Enbanc and DivisionJune Karl CepidaÎncă nu există evaluări

- People Vs Carlos, 47 Phil 626Document5 paginiPeople Vs Carlos, 47 Phil 626flornatsÎncă nu există evaluări

- 23.) KiamcoDocument2 pagini23.) KiamcoChelle OngÎncă nu există evaluări

- Ra 10607 PDFDocument68 paginiRa 10607 PDFMae Jansen Doroneo100% (1)

- Corporation-Law Digest Compiled PDFDocument71 paginiCorporation-Law Digest Compiled PDFAlpha BetaÎncă nu există evaluări

- Taxation Law 1991Document10 paginiTaxation Law 1991Jc GalamgamÎncă nu există evaluări

- Taxation Case Digest2Document242 paginiTaxation Case Digest2Kevin LavinaÎncă nu există evaluări

- Module 7 Chapter 9 Input VATDocument7 paginiModule 7 Chapter 9 Input VATChris SumandeÎncă nu există evaluări

- Marubeni Corp Vs CIRDocument2 paginiMarubeni Corp Vs CIRKara AgliboÎncă nu există evaluări

- Mercantile Law 2014Document11 paginiMercantile Law 2014TariljaYentlBestreÎncă nu există evaluări

- Tax Rev Midterms CoverageDocument11 paginiTax Rev Midterms CoverageRegi Mabilangan ArceoÎncă nu există evaluări

- Santosa B. Datuman vs. First Cosmopolitan Manpower and Promotion Services, Inc.Document9 paginiSantosa B. Datuman vs. First Cosmopolitan Manpower and Promotion Services, Inc.Angel UrbanoÎncă nu există evaluări

- Summary of Significant SC Decisions (April May June 2011)Document2 paginiSummary of Significant SC Decisions (April May June 2011)elmersgluethebombÎncă nu există evaluări

- Legal Ethics Bar Exams 2015 PointersDocument46 paginiLegal Ethics Bar Exams 2015 PointersMariline LeeÎncă nu există evaluări

- Tabunting Pawnshop V CirDocument2 paginiTabunting Pawnshop V CirNezte VirtudazoÎncă nu există evaluări

- Securities Regulations Code ("SRC") - Ra 8799Document25 paginiSecurities Regulations Code ("SRC") - Ra 8799Shiela MarieÎncă nu există evaluări

- Republic VS Asiapro Coop DigestDocument4 paginiRepublic VS Asiapro Coop DigestKath LimÎncă nu există evaluări

- R.A. 1125 Creating The Court of Tax AppealsDocument6 paginiR.A. 1125 Creating The Court of Tax AppealsJose Van TanÎncă nu există evaluări

- Rule 2 Case Digest PDFDocument43 paginiRule 2 Case Digest PDFHomer CasauayÎncă nu există evaluări

- EDI-Staffbuilders International, Inc. Expertise Search InternationalDocument4 paginiEDI-Staffbuilders International, Inc. Expertise Search InternationalGerard Relucio OroÎncă nu există evaluări

- Certification Election - Bureau of Labor RelationsDocument3 paginiCertification Election - Bureau of Labor RelationsNiruh Kyle AntaticoÎncă nu există evaluări

- Civ Pro Introduction InigoDocument7 paginiCiv Pro Introduction InigoMyrna ValledorÎncă nu există evaluări

- VAT Digest PDFDocument31 paginiVAT Digest PDFangelicaÎncă nu există evaluări

- Gosiaco v. Ching and Casta, GR 173807, April 16, 2009 FactsDocument2 paginiGosiaco v. Ching and Casta, GR 173807, April 16, 2009 FactsRoselle LagamayoÎncă nu există evaluări

- Cir vs. Team Sual CorporationDocument12 paginiCir vs. Team Sual CorporationRhevÎncă nu există evaluări

- RMC No 67-2012Document5 paginiRMC No 67-2012evilminionsattackÎncă nu există evaluări

- Taxation CasesDocument94 paginiTaxation CasesMichael jay sarmientoÎncă nu există evaluări

- Mabuhay Holdings v. SEMBCORPDocument39 paginiMabuhay Holdings v. SEMBCORPYvainÎncă nu există evaluări

- Partnership Agency and Trust (Article 1767-1827)Document1 paginăPartnership Agency and Trust (Article 1767-1827)Cyra de LemosÎncă nu există evaluări

- Corp-General Credit V AlsonsDocument10 paginiCorp-General Credit V AlsonsAnonymous OVr4N9MsÎncă nu există evaluări

- Sample Judicial AffidavitDocument3 paginiSample Judicial AffidavitRoland Bon IntudÎncă nu există evaluări

- New Trial or Reconsideration: Rule 37Document38 paginiNew Trial or Reconsideration: Rule 37Angelica Joyce DyÎncă nu există evaluări

- Brotherhood Labor Unity Movement VS NLRCDocument2 paginiBrotherhood Labor Unity Movement VS NLRCBalaod Maricor100% (1)

- Magalona vs. Pesayco, GR No. L-39607, February 6, 1934 (59 Phil 453) PDFDocument2 paginiMagalona vs. Pesayco, GR No. L-39607, February 6, 1934 (59 Phil 453) PDFJohanna VidadÎncă nu există evaluări

- Case DigestDocument9 paginiCase DigestLea Angelica RiofloridoÎncă nu există evaluări

- Hayden Kho Sr. Vs Dolores Nagbanua, Et. Al. G.R. No. 237246. July 29, 2019Document10 paginiHayden Kho Sr. Vs Dolores Nagbanua, Et. Al. G.R. No. 237246. July 29, 2019Mysh PDÎncă nu există evaluări

- Medical Plaza Makati Condominium Corp vs. Cullen, 709 SCRA 110, G.R. No. 181416 Nov 11, 2013Document19 paginiMedical Plaza Makati Condominium Corp vs. Cullen, 709 SCRA 110, G.R. No. 181416 Nov 11, 2013Galilee RomasantaÎncă nu există evaluări

- TAXATION LAW REVIEW. Sababan. 2008 Ed. PPG 181-200: A.The Remedies of The GovernmentDocument9 paginiTAXATION LAW REVIEW. Sababan. 2008 Ed. PPG 181-200: A.The Remedies of The GovernmentRein DrewÎncă nu există evaluări

- TAX REMEDIES UNDER THE NIRC PowerDocument5 paginiTAX REMEDIES UNDER THE NIRC PowerjonahÎncă nu există evaluări

- Tax 2 (Remedies & CTA Jurisdiction)Document13 paginiTax 2 (Remedies & CTA Jurisdiction)Monice RiveraÎncă nu există evaluări

- 2020 Reme TPDocument24 pagini2020 Reme TPManuel VillanuevaÎncă nu există evaluări

- Tariff Protest Cases: Ollector of Ustoms UlingDocument1 paginăTariff Protest Cases: Ollector of Ustoms UlingNayadÎncă nu există evaluări

- Strike Procedure Labor Relations Law PhilippinesDocument1 paginăStrike Procedure Labor Relations Law Philippinespurplelady22Încă nu există evaluări

- Tariff Seizure & Forefiture Cases: EizureDocument1 paginăTariff Seizure & Forefiture Cases: EizureNayadÎncă nu există evaluări

- Real Property Protest Assessment (Land Value) Real Property Protest Assessment (Collection of RPT)Document1 paginăReal Property Protest Assessment (Land Value) Real Property Protest Assessment (Collection of RPT)NayadÎncă nu există evaluări

- Tax+Remedy+ +refund Tax+CreditDocument1 paginăTax+Remedy+ +refund Tax+CreditEdwin PadilloÎncă nu există evaluări

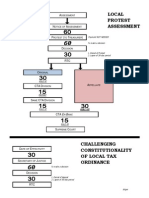

- Local Protest Assessment: SsessmentDocument1 paginăLocal Protest Assessment: SsessmentEAP11705790Încă nu există evaluări

- Tax RemedyDocument1 paginăTax RemedyNayadÎncă nu există evaluări

- Remedial Law Review Atty. Tranquil Salvador - Special ProceedingsDocument4 paginiRemedial Law Review Atty. Tranquil Salvador - Special ProceedingsNayadÎncă nu există evaluări

- GuideDocument7 paginiGuideNayadÎncă nu există evaluări

- Erratum: Sec. 188, Publication of Tax Ordinances and Revenue MeasuresDocument1 paginăErratum: Sec. 188, Publication of Tax Ordinances and Revenue MeasuresNayadÎncă nu există evaluări

- Guidelines On Estate and Donor's TaxDocument14 paginiGuidelines On Estate and Donor's Taxkatreena ysabelle89% (9)

- Guide Notes On Local Government TaxationDocument27 paginiGuide Notes On Local Government TaxationNayadÎncă nu există evaluări

- DeanDocument6 paginiDeanNayadÎncă nu există evaluări

- Aria Pocket Guide 2007Document8 paginiAria Pocket Guide 2007AsmphLibrary OrtigasÎncă nu există evaluări

- Children's Rights ReviewerDocument40 paginiChildren's Rights ReviewerNayad100% (1)

- Admin Law PointersDocument16 paginiAdmin Law PointersNayadÎncă nu există evaluări

- Instructions For Form 943: Pager/SgmlDocument4 paginiInstructions For Form 943: Pager/SgmlIRSÎncă nu există evaluări

- MCQ On Finals TaxesDocument7 paginiMCQ On Finals TaxesRandy ManzanoÎncă nu există evaluări

- 71 Ing Bank VSDocument2 pagini71 Ing Bank VSManuel Villanueva100% (1)

- IRS Form W-9Document4 paginiIRS Form W-9Gary S. Wolfe100% (1)

- KEY WORDS Income Taxation 2Document19 paginiKEY WORDS Income Taxation 2Buddy Brylle YbanezÎncă nu există evaluări

- Topic Wise Taxation Icap Past Papers (Pak) of C.ADocument30 paginiTopic Wise Taxation Icap Past Papers (Pak) of C.AIrfan33% (3)

- Workmen Compensation Retainer FormDocument2 paginiWorkmen Compensation Retainer FormJonh BairdÎncă nu există evaluări

- About IRS Form W-8BENDocument43 paginiAbout IRS Form W-8BENkreativ Mindz100% (20)

- PAYE Return SampleDocument42 paginiPAYE Return Sampleoyesigye DennisÎncă nu există evaluări

- 1604-Cf 2013 Global EcoDocument1 pagină1604-Cf 2013 Global Ecostringwinds101Încă nu există evaluări

- Revenue Regulations No. 3-98 - Fringe Benefit TaxDocument14 paginiRevenue Regulations No. 3-98 - Fringe Benefit TaxRaiza Radoc100% (1)

- Certificate of Creditable Tax Withheld at SourceDocument2 paginiCertificate of Creditable Tax Withheld at SourceMaricar Lelaine SecretarioÎncă nu există evaluări

- Problem 1 Current Liability Entries and Adjustments: InstructionsDocument6 paginiProblem 1 Current Liability Entries and Adjustments: Instructionsbeeeeee100% (1)

- Meaning of Royalties and Fees For Technical ServicesDocument13 paginiMeaning of Royalties and Fees For Technical ServicesTripathi OjÎncă nu există evaluări

- 2002 ISDA Master AgreementDocument36 pagini2002 ISDA Master AgreementturbbbÎncă nu există evaluări

- MIRA Annual Report 2013 - English PDFDocument47 paginiMIRA Annual Report 2013 - English PDFNaee ARÎncă nu există evaluări

- Taxation Law Case DigestsDocument514 paginiTaxation Law Case DigestsCzarina Bantay67% (3)

- Register of Cash in Bank and Other Related Financial TransactionsDocument1 paginăRegister of Cash in Bank and Other Related Financial TransactionsRodelLaborÎncă nu există evaluări

- 113 Module 1 - INTODUCTORY NOTES AND TRADE PAYABLES AND ACCRUED LIABILITIESDocument4 pagini113 Module 1 - INTODUCTORY NOTES AND TRADE PAYABLES AND ACCRUED LIABILITIESRay SanzeninÎncă nu există evaluări

- HISD - Hardship Withdrawal Guidelines Documentation DTD 8-03-09Document8 paginiHISD - Hardship Withdrawal Guidelines Documentation DTD 8-03-09Vaibhav SinghÎncă nu există evaluări

- 6 - Nyk-Filjapan Shipping Corporation v. CIRDocument21 pagini6 - Nyk-Filjapan Shipping Corporation v. CIRCarlota VillaromanÎncă nu există evaluări

- Topic: Tax Refunds Commissioner of Internal Revenue V. Univation Motor Philippines, Inc. (Formerly Nissan Motor Philippines)Document2 paginiTopic: Tax Refunds Commissioner of Internal Revenue V. Univation Motor Philippines, Inc. (Formerly Nissan Motor Philippines)Joshua Erik MadriaÎncă nu există evaluări

- Attorneys Fees in LaborDocument23 paginiAttorneys Fees in LaborJanette SumagaysayÎncă nu există evaluări

- TRAIN Law (PWC Philippines)Document16 paginiTRAIN Law (PWC Philippines)Rose Ann Juleth Licayan100% (1)

- p4012 PDFDocument208 paginip4012 PDFninmonk999Încă nu există evaluări

- Polycab Final ReportDocument97 paginiPolycab Final ReportAnjali PandeÎncă nu există evaluări

- Case DigestDocument4 paginiCase DigestGabriel Jhick SaliwanÎncă nu există evaluări

- TaxDocument4 paginiTaximoymitoÎncă nu există evaluări

- PCL Chap 2 en Ca PDFDocument45 paginiPCL Chap 2 en Ca PDFRenso Ramirez JimenezÎncă nu există evaluări

- Maplebear, Inc. 50 Beale Street, 6th Floor San Francisco, CA 94105 1,604.65Document2 paginiMaplebear, Inc. 50 Beale Street, 6th Floor San Francisco, CA 94105 1,604.65YoSoyOscarMesaÎncă nu există evaluări

- A Student's Guide to Law School: What Counts, What Helps, and What MattersDe la EverandA Student's Guide to Law School: What Counts, What Helps, and What MattersEvaluare: 5 din 5 stele5/5 (4)

- The Absolute Beginner's Guide to Cross-ExaminationDe la EverandThe Absolute Beginner's Guide to Cross-ExaminationÎncă nu există evaluări

- Essential Guide to Workplace Investigations, The: A Step-By-Step Guide to Handling Employee Complaints & ProblemsDe la EverandEssential Guide to Workplace Investigations, The: A Step-By-Step Guide to Handling Employee Complaints & ProblemsEvaluare: 3 din 5 stele3/5 (2)

- Legal Writing in Plain English: A Text with ExercisesDe la EverandLegal Writing in Plain English: A Text with ExercisesEvaluare: 3 din 5 stele3/5 (2)

- The Power of Our Supreme Court: How Supreme Court Cases Shape DemocracyDe la EverandThe Power of Our Supreme Court: How Supreme Court Cases Shape DemocracyEvaluare: 5 din 5 stele5/5 (2)

- Legal Writing: QuickStudy Laminated Reference GuideDe la EverandLegal Writing: QuickStudy Laminated Reference GuideÎncă nu există evaluări

- Legal Forms for Starting & Running a Small Business: 65 Essential Agreements, Contracts, Leases & LettersDe la EverandLegal Forms for Starting & Running a Small Business: 65 Essential Agreements, Contracts, Leases & LettersÎncă nu există evaluări

- Federal Income Tax: a QuickStudy Digital Law ReferenceDe la EverandFederal Income Tax: a QuickStudy Digital Law ReferenceÎncă nu există evaluări

- Form Your Own Limited Liability Company: Create An LLC in Any StateDe la EverandForm Your Own Limited Liability Company: Create An LLC in Any StateÎncă nu există evaluări

- Commentaries on the Laws of England, Volume 1: A Facsimile of the First Edition of 1765-1769De la EverandCommentaries on the Laws of England, Volume 1: A Facsimile of the First Edition of 1765-1769Evaluare: 4 din 5 stele4/5 (6)

- Dictionary of Legal Terms: Definitions and Explanations for Non-LawyersDe la EverandDictionary of Legal Terms: Definitions and Explanations for Non-LawyersEvaluare: 5 din 5 stele5/5 (2)

- Solve Your Money Troubles: Strategies to Get Out of Debt and Stay That WayDe la EverandSolve Your Money Troubles: Strategies to Get Out of Debt and Stay That WayEvaluare: 4 din 5 stele4/5 (8)

- Legal Forms for Everyone: Leases, Home Sales, Avoiding Probate, Living Wills, Trusts, Divorce, Copyrights, and Much MoreDe la EverandLegal Forms for Everyone: Leases, Home Sales, Avoiding Probate, Living Wills, Trusts, Divorce, Copyrights, and Much MoreEvaluare: 3.5 din 5 stele3.5/5 (2)

- Legal Guide for Starting & Running a Small BusinessDe la EverandLegal Guide for Starting & Running a Small BusinessEvaluare: 4.5 din 5 stele4.5/5 (9)

- Torts: QuickStudy Laminated Reference GuideDe la EverandTorts: QuickStudy Laminated Reference GuideEvaluare: 5 din 5 stele5/5 (1)

- LLC or Corporation?: Choose the Right Form for Your BusinessDe la EverandLLC or Corporation?: Choose the Right Form for Your BusinessEvaluare: 3.5 din 5 stele3.5/5 (4)

- Employment Law: a Quickstudy Digital Law ReferenceDe la EverandEmployment Law: a Quickstudy Digital Law ReferenceEvaluare: 1 din 5 stele1/5 (1)

- Nolo's Deposition Handbook: The Essential Guide for Anyone Facing or Conducting a DepositionDe la EverandNolo's Deposition Handbook: The Essential Guide for Anyone Facing or Conducting a DepositionEvaluare: 5 din 5 stele5/5 (1)

- So You Want to be a Lawyer: The Ultimate Guide to Getting into and Succeeding in Law SchoolDe la EverandSo You Want to be a Lawyer: The Ultimate Guide to Getting into and Succeeding in Law SchoolÎncă nu există evaluări

- Legal Research: a QuickStudy Laminated Law ReferenceDe la EverandLegal Research: a QuickStudy Laminated Law ReferenceÎncă nu există evaluări

- Legal Writing in Plain English, Third Edition: A Text with ExercisesDe la EverandLegal Writing in Plain English, Third Edition: A Text with ExercisesÎncă nu există evaluări

- How to Make Patent Drawings: Save Thousands of Dollars and Do It With a Camera and Computer!De la EverandHow to Make Patent Drawings: Save Thousands of Dollars and Do It With a Camera and Computer!Evaluare: 5 din 5 stele5/5 (1)