S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- 1001 MOVIES You Must See Before You DieDocument19 pagini1001 MOVIES You Must See Before You DieMayank100% (551)

- Win-Gallup International Global Index of Religiosity and Atheism-2012Document25 paginiWin-Gallup International Global Index of Religiosity and Atheism-2012st27383100% (12)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Uber Service AuditDocument12 paginiUber Service AuditAdeelÎncă nu există evaluări

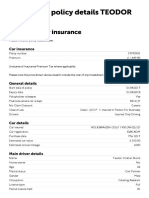

- Policy Details PageDocument2 paginiPolicy Details PageLuci PoroÎncă nu există evaluări

- A Case Study of Southwest AirlinesDocument4 paginiA Case Study of Southwest AirlinesishmaelÎncă nu există evaluări

- Practical Applications of The Wyckoff Method of Trading and InvestingDocument16 paginiPractical Applications of The Wyckoff Method of Trading and InvestingFREDERICOÎncă nu există evaluări

- FFFDocument1 paginăFFFFREDERICOÎncă nu există evaluări

- EulaDocument3 paginiEulaBrandon YorkÎncă nu există evaluări

- 25 JJDocument1 pagină25 JJFREDERICOÎncă nu există evaluări

- WYCKOFFDocument9 paginiWYCKOFFtasmanoptions67% (3)

- Henri Lepage: "Financial Crisis: The Other Vision"Document11 paginiHenri Lepage: "Financial Crisis: The Other Vision"FREDERICOÎncă nu există evaluări

- Greg Mankiw's Blog - Summer Reading ListDocument1 paginăGreg Mankiw's Blog - Summer Reading ListFREDERICOÎncă nu există evaluări

- WYCKOFF Timing Your Commitments - SandC V9.6 (224-227)Document8 paginiWYCKOFF Timing Your Commitments - SandC V9.6 (224-227)CAD16Încă nu există evaluări

- 2 Poliglotas Dão 5 Dicas para Aprender Línguas Sem Esquecê-Las - BabbelDocument6 pagini2 Poliglotas Dão 5 Dicas para Aprender Línguas Sem Esquecê-Las - BabbelFREDERICOÎncă nu există evaluări

- Wyckoff Method - Law+TestDocument6 paginiWyckoff Method - Law+Testallegre100% (3)

- Annualperformance - 11-15Document1 paginăAnnualperformance - 11-15FREDERICOÎncă nu există evaluări

- Leis de Potência, Lei de Zipf's e Distribuições de Cauda PesadaDocument40 paginiLeis de Potência, Lei de Zipf's e Distribuições de Cauda PesadaFREDERICOÎncă nu există evaluări

- Neural Network Package For Octave Users GuDocument15 paginiNeural Network Package For Octave Users GuRocio Emma Tapia AlvaÎncă nu există evaluări

- The Vi X Reality Check May 10Document4 paginiThe Vi X Reality Check May 10FREDERICOÎncă nu există evaluări

- On The Optimality of Kelly Strategies: Mark Davis and S Ebastien LleoDocument58 paginiOn The Optimality of Kelly Strategies: Mark Davis and S Ebastien LleoFREDERICOÎncă nu există evaluări

- Volatility Indexes at Cboe: Premier Barometers of Investor Sentiment and Market VolatilityDocument2 paginiVolatility Indexes at Cboe: Premier Barometers of Investor Sentiment and Market VolatilityFREDERICOÎncă nu există evaluări

- Henri Lepage: "Financial Crisis: The Other Vision"Document11 paginiHenri Lepage: "Financial Crisis: The Other Vision"FREDERICOÎncă nu există evaluări

- How to open NFO files with WordPad or NotepadDocument1 paginăHow to open NFO files with WordPad or Notepadjude_abarcaÎncă nu există evaluări

- Etd 2519Document72 paginiEtd 2519FREDERICOÎncă nu există evaluări

- Greg Mankiw's Blog - Summer Reading ListDocument1 paginăGreg Mankiw's Blog - Summer Reading ListFREDERICOÎncă nu există evaluări

- Henri Lepage: "Financial Crisis: The Other Vision"Document11 paginiHenri Lepage: "Financial Crisis: The Other Vision"FREDERICOÎncă nu există evaluări

- A New Computational Method of Input Selection For Stock Market Forecasting With Neural NetworksDocument8 paginiA New Computational Method of Input Selection For Stock Market Forecasting With Neural NetworksFREDERICOÎncă nu există evaluări

- Eastern Time Zone - Wikipedia, The Free EncyclopediaDocument5 paginiEastern Time Zone - Wikipedia, The Free EncyclopediaFREDERICOÎncă nu există evaluări

- Greg Mankiw's Blog - Summer Reading ListDocument1 paginăGreg Mankiw's Blog - Summer Reading ListFREDERICOÎncă nu există evaluări

- Religion and Atheism Gallup Poll 2012Document25 paginiReligion and Atheism Gallup Poll 2012Dante Bobadilla RamírezÎncă nu există evaluări

- VJ Se RRRRRRRDocument1 paginăVJ Se RRRRRRRFREDERICOÎncă nu există evaluări

- XoekekekeDocument1 paginăXoekekekeFREDERICOÎncă nu există evaluări

- IndiGo Q2 FY22 Earnings CallDocument16 paginiIndiGo Q2 FY22 Earnings CallBhav Bhagwan HaiÎncă nu există evaluări

- Sample QuestionsDocument1 paginăSample QuestionswghiÎncă nu există evaluări

- Prospects and Challenges of The Ethiopian Commodity ExchangeDocument83 paginiProspects and Challenges of The Ethiopian Commodity Exchangeggmanche100% (5)

- 2nd Quarter First Assessment in Gen. MathDocument3 pagini2nd Quarter First Assessment in Gen. MathglaizacoseÎncă nu există evaluări

- 3.1 Income Elasticity of DemandDocument35 pagini3.1 Income Elasticity of DemandBighnesh MahapatraÎncă nu există evaluări

- Chapter 20 Measuring GDP and Economic Growth: Parkin/Bade, Economics: Canada in The Global Environment, 8eDocument40 paginiChapter 20 Measuring GDP and Economic Growth: Parkin/Bade, Economics: Canada in The Global Environment, 8ePranta SahaÎncă nu există evaluări

- Fico Imp Interview QuestionsDocument50 paginiFico Imp Interview QuestionsNaveenÎncă nu există evaluări

- Management Accounting Chapter 3 (Cost-Volume-Profit Chapter22)Document59 paginiManagement Accounting Chapter 3 (Cost-Volume-Profit Chapter22)yimerÎncă nu există evaluări

- Distribution Competitiveness GuideDocument12 paginiDistribution Competitiveness GuideEilyn PimientaÎncă nu există evaluări

- IT 2U Business Section 2 Seat 2Document120 paginiIT 2U Business Section 2 Seat 2ANee NameeÎncă nu există evaluări

- NCMSL BrochureDocument6 paginiNCMSL Brochuremaster45Încă nu există evaluări

- CBA: 'NO SEGREGATION, NO PICK-UP' POLICYDocument17 paginiCBA: 'NO SEGREGATION, NO PICK-UP' POLICYChaiÎncă nu există evaluări

- Burmah CastrolDocument13 paginiBurmah CastrolanfkrÎncă nu există evaluări

- IFM Class Examples On ECU and Gold StandardDocument2 paginiIFM Class Examples On ECU and Gold StandardFurukawa YurikoÎncă nu există evaluări

- Shah Alam Hospital Background and Possible Reasons For DelayDocument3 paginiShah Alam Hospital Background and Possible Reasons For DelayVin_Q26Încă nu există evaluări

- Kotak PMS Special Situations Value Presentation - Jan 18Document36 paginiKotak PMS Special Situations Value Presentation - Jan 18kanna275Încă nu există evaluări

- LauretaDocument2 paginiLauretaAsh Manguera50% (2)

- Marketing Management Syllabus BreakdownDocument71 paginiMarketing Management Syllabus BreakdownDarshil GalaÎncă nu există evaluări

- Cuadernillo IV Parcial Quinto Grado 2022Document1 paginăCuadernillo IV Parcial Quinto Grado 2022tumbalacasamami5365Încă nu există evaluări

- TCS Recruitment Previous Year Pattern Questions Set-9Document2 paginiTCS Recruitment Previous Year Pattern Questions Set-9QUANT ADDAÎncă nu există evaluări

- Bond ValuationDocument3 paginiBond ValuationGauravÎncă nu există evaluări

- Data For Giving His Heart More Room: Bruce Springsteen's Private FoundationsDocument63 paginiData For Giving His Heart More Room: Bruce Springsteen's Private FoundationsDavid WilsonÎncă nu există evaluări

- Group 1 LenovoDocument17 paginiGroup 1 LenovoGULAM GOUSHÎncă nu există evaluări

- 9 Micro Ch17 Presentation7e Chap09Document41 pagini9 Micro Ch17 Presentation7e Chap09Nguyễn Lê KhánhÎncă nu există evaluări

- Chapter Four: Price and Out Put Determination Under Perfect CompetitionDocument49 paginiChapter Four: Price and Out Put Determination Under Perfect Competitioneyob yohannesÎncă nu există evaluări

- Asa - Injection Mould Component Cost EstimationDocument7 paginiAsa - Injection Mould Component Cost EstimationVenkateswaran venkateswaranÎncă nu există evaluări

- Ramada Case StudyDocument2 paginiRamada Case StudySourav Sharma100% (1)