S-ar putea să vă placă și

- Assignment Questions SapmDocument2 paginiAssignment Questions SapmKeerthini SadashivaÎncă nu există evaluări

- 7891FinalGr1paper2ManagementAccountingandFinancilAnalys PDFDocument32 pagini7891FinalGr1paper2ManagementAccountingandFinancilAnalys PDFPrasanna SharmaÎncă nu există evaluări

- Mqp1 10mba Mbafm02 AmDocument4 paginiMqp1 10mba Mbafm02 AmDipesh JainÎncă nu există evaluări

- List of Favourite SFM Examination QuestionsDocument12 paginiList of Favourite SFM Examination QuestionsAnkit RastogiÎncă nu există evaluări

- Finance RTP Cap-II June 2016Document37 paginiFinance RTP Cap-II June 2016Artha sarokarÎncă nu există evaluări

- 18542final Old Sugg Paper Nov09 2Document14 pagini18542final Old Sugg Paper Nov09 2Atish SahooÎncă nu există evaluări

- Investment Planning and Portfolio ManagementDocument3 paginiInvestment Planning and Portfolio ManagementTark Raj BhattÎncă nu există evaluări

- Financial Management-I Term End Examinations: 31 Stdev 14.30 10.91 Beta 0.26 CORRR 0.1988Document7 paginiFinancial Management-I Term End Examinations: 31 Stdev 14.30 10.91 Beta 0.26 CORRR 0.1988EshanMishraÎncă nu există evaluări

- Financial ManagementDocument3 paginiFinancial ManagementMRRYNIMAVATÎncă nu există evaluări

- Exercise-Chapter 2 and 3: P Q P Q P Q A B C D FDocument4 paginiExercise-Chapter 2 and 3: P Q P Q P Q A B C D FPrum Longdy100% (4)

- Nmims Moolyankan Quiz 2011Document13 paginiNmims Moolyankan Quiz 2011Ivani BoraÎncă nu există evaluări

- CS Final - Financial Tresurs and Forex Management - June 2004Document4 paginiCS Final - Financial Tresurs and Forex Management - June 2004Rushikesh DeshmukhÎncă nu există evaluări

- Portfolio Theory - Additional Problems 1Document3 paginiPortfolio Theory - Additional Problems 1Hambeca PHÎncă nu există evaluări

- Questions For Group 1: S.B.Khatri-FM-AIMDocument6 paginiQuestions For Group 1: S.B.Khatri-FM-AIMAbhishek singhÎncă nu există evaluări

- Pen & Paper Final Group I SFM April 10 Test 1Document4 paginiPen & Paper Final Group I SFM April 10 Test 1rbhadauria_1Încă nu există evaluări

- Questions For Group 1: S.B.Khatri-FM-AIMDocument6 paginiQuestions For Group 1: S.B.Khatri-FM-AIMAbhishek singhÎncă nu există evaluări

- IMT 09 Security Analysis & Portfolio Management M2Document4 paginiIMT 09 Security Analysis & Portfolio Management M2solvedcareÎncă nu există evaluări

- Project Risk Analysis Assignment Xi 2011Document3 paginiProject Risk Analysis Assignment Xi 2011Piyush SikariaÎncă nu există evaluări

- Capital Budgeting Illustrative NumericalsDocument6 paginiCapital Budgeting Illustrative NumericalsPriyanka Dargad100% (1)

- Financial, Treasury and Forex ManagementDocument8 paginiFinancial, Treasury and Forex ManagementnikhilÎncă nu există evaluări

- Tutorial 3 For FM-IDocument5 paginiTutorial 3 For FM-IarishthegreatÎncă nu există evaluări

- Accf 2204Document7 paginiAccf 2204Avi StrikyÎncă nu există evaluări

- Sem IV (Internal 2010)Document15 paginiSem IV (Internal 2010)anandpatel2991Încă nu există evaluări

- Cost CalculationlDocument5 paginiCost CalculationlIshan ShingneÎncă nu există evaluări

- ACC501 Mega File SolvedDocument1.045 paginiACC501 Mega File SolvedOwais KhanÎncă nu există evaluări

- Choose The Most Appropriate Answer Among The Given ChoicesDocument17 paginiChoose The Most Appropriate Answer Among The Given Choicesrehmania78644Încă nu există evaluări

- Tutorial I, II, III, IV QuestionsDocument15 paginiTutorial I, II, III, IV QuestionsAninda DuttaÎncă nu există evaluări

- Final Auditing Question Paper - May - 2008Document5 paginiFinal Auditing Question Paper - May - 2008Khristine CaserialÎncă nu există evaluări

- Financial Treasury and Forex Management: NoteDocument7 paginiFinancial Treasury and Forex Management: Notesks0865Încă nu există evaluări

- End Term ExamDocument4 paginiEnd Term ExamKeshav Sehgal0% (2)

- 2830203-Security Analysis and Portfolio ManagementDocument2 pagini2830203-Security Analysis and Portfolio ManagementbhumikajasaniÎncă nu există evaluări

- Investment+Planning+Module (1)Document137 paginiInvestment+Planning+Module (1)jayaram_polaris100% (1)

- Exam Financial ManagementDocument5 paginiExam Financial ManagementMaha MansoorÎncă nu există evaluări

- Assignment 01 QuestionsDocument3 paginiAssignment 01 QuestionsHanlin ShaoÎncă nu există evaluări

- FIN2001 Exam - 2021feb - FormoodleDocument7 paginiFIN2001 Exam - 2021feb - Formoodletanren010727Încă nu există evaluări

- Finance Pq1Document33 paginiFinance Pq1pakhok3Încă nu există evaluări

- Financial Management Assg-1Document6 paginiFinancial Management Assg-1Udhay ShankarÎncă nu există evaluări

- HW5 S10Document6 paginiHW5 S10danbrownda0% (1)

- MainExam 2018 PDFDocument12 paginiMainExam 2018 PDFAnonymous hGNXxMÎncă nu există evaluări

- Underline The Final Answers: ONLY If Any Question Lacks Information, State Your Reasonable Assumption and ProceedDocument4 paginiUnderline The Final Answers: ONLY If Any Question Lacks Information, State Your Reasonable Assumption and ProceedAbhishek GhoshÎncă nu există evaluări

- ACC501 Mid Term Preparation FileDocument28 paginiACC501 Mid Term Preparation FileMujtaba AhmadÎncă nu există evaluări

- Assignment#2Document3 paginiAssignment#2Wuhao KoÎncă nu există evaluări

- Selected BKM Exercises 1 - v2Document19 paginiSelected BKM Exercises 1 - v2Mattia CampigottoÎncă nu există evaluări

- BSF 1102 - Principles of Finance - November 2022Document6 paginiBSF 1102 - Principles of Finance - November 2022JulianÎncă nu există evaluări

- Advanced Financial Management: Thursday 10 June 2010Document10 paginiAdvanced Financial Management: Thursday 10 June 2010Waleed MinhasÎncă nu există evaluări

- Financial Management: Friday 9 December 2011Document8 paginiFinancial Management: Friday 9 December 2011Hussain MeskinzadaÎncă nu există evaluări

- Question Paper of FM (1) - 1637643755Document3 paginiQuestion Paper of FM (1) - 1637643755srijana pathakÎncă nu există evaluări

- Financial Management Mba Question PaperDocument4 paginiFinancial Management Mba Question Paperpalak2407Încă nu există evaluări

- SFMDocument29 paginiSFMShrinivas PrabhuneÎncă nu există evaluări

- Open Book: Financial Statement Analysis AKT304-MNJ62Document3 paginiOpen Book: Financial Statement Analysis AKT304-MNJ62Riska IinÎncă nu există evaluări

- Investment Planning (Finally Done)Document146 paginiInvestment Planning (Finally Done)api-3814557100% (2)

- SolutionDocument6 paginiSolutionaskdgasÎncă nu există evaluări

- 2.BMMF5103 FINAL EXAM Formated-Moderated 1-2013Document9 pagini2.BMMF5103 FINAL EXAM Formated-Moderated 1-2013theatresonicÎncă nu există evaluări

- Revision Question 2023.11.21Document5 paginiRevision Question 2023.11.21rbaambaÎncă nu există evaluări

- Gujarat Technological UniversityDocument3 paginiGujarat Technological UniversityAmul PatelÎncă nu există evaluări

- Accounting For ManagersDocument6 paginiAccounting For ManagerskartikbhaiÎncă nu există evaluări

- Practical QuestionsDocument6 paginiPractical Questionsshantanu_malviya_1100% (1)

- Risk and ReturnDocument2 paginiRisk and ReturnKhondaker RafsanjaniÎncă nu există evaluări

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)De la EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Evaluare: 4.5 din 5 stele4.5/5 (5)

- Rieview of Literature For Derivatives ProjectDocument42 paginiRieview of Literature For Derivatives Projectcozycap82% (22)

- Forex QuizDocument17 paginiForex QuizManish KanwarÎncă nu există evaluări

- Statement of CashflowDocument2 paginiStatement of CashflowAna Marie IllutÎncă nu există evaluări

- Chapter 9-STOCK VALUATION-FIXDocument33 paginiChapter 9-STOCK VALUATION-FIXRacing FirmanÎncă nu există evaluări

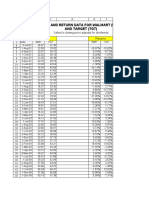

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 paginiPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahÎncă nu există evaluări

- Solutions Chap007Document13 paginiSolutions Chap007Said Ur RahmanÎncă nu există evaluări

- 3 - Cost Basis CalculatorDocument2 pagini3 - Cost Basis Calculatorsumit6singhÎncă nu există evaluări

- 2) M1 Ch2 International Parity Relationships andDocument9 pagini2) M1 Ch2 International Parity Relationships andManan SuchakÎncă nu există evaluări

- BCC620 Business Finance Management Main (JAN) E1 - JUL 2022 - ANSWER SCHEMEDocument5 paginiBCC620 Business Finance Management Main (JAN) E1 - JUL 2022 - ANSWER SCHEMERukshani RefaiÎncă nu există evaluări

- FX Training Series34 Review v3Document4 paginiFX Training Series34 Review v3eliteforextrainingÎncă nu există evaluări

- Chapter 2 - Capital Structure - Student's Copy FinalDocument78 paginiChapter 2 - Capital Structure - Student's Copy FinalJulie Mae Caling MalitÎncă nu există evaluări

- Marketing Grewal 4th Edition Solutions ManualDocument26 paginiMarketing Grewal 4th Edition Solutions ManualPeterThomasizbjf100% (77)

- Sip Proposal Sip ProposedDocument3 paginiSip Proposal Sip Proposedsaurabh agarwalÎncă nu există evaluări

- Call OptionDocument1 paginăCall OptionMustafa BhaiÎncă nu există evaluări

- Banking Chapter NineDocument46 paginiBanking Chapter NinefikremariamÎncă nu există evaluări

- MetwestDocument47 paginiMetwestJason HolmezÎncă nu există evaluări

- Capital Structure - 1Document25 paginiCapital Structure - 1bakhtiar2014Încă nu există evaluări

- Invoice - 622 #1Document2 paginiInvoice - 622 #1Serena GothÎncă nu există evaluări

- No. Requisition / Material Code / Description Quantity Unit Unit Price Disc % AmountDocument3 paginiNo. Requisition / Material Code / Description Quantity Unit Unit Price Disc % AmountMond NaÎncă nu există evaluări

- Finance For Viva PDFDocument17 paginiFinance For Viva PDFTusherÎncă nu există evaluări

- Banking Sector Yes Bank Under A Moratorium. SBI Investing CapitalDocument5 paginiBanking Sector Yes Bank Under A Moratorium. SBI Investing CapitalSingh JagdishÎncă nu există evaluări

- Comparative Analysis of HDFCDocument18 paginiComparative Analysis of HDFCgagandeepsingh86Încă nu există evaluări

- Financial Analysis and Reporting Midterm Quiz 1Document8 paginiFinancial Analysis and Reporting Midterm Quiz 1Santi SeguinÎncă nu există evaluări

- Alibaba IPO Write-UpDocument6 paginiAlibaba IPO Write-UpShashank ReddyÎncă nu există evaluări

- 10 Best Penny Stock Concepts & StrategiesDocument98 pagini10 Best Penny Stock Concepts & StrategiesRick SaldanÎncă nu există evaluări

- CFA Level 3 2012 Guideline AnswersDocument42 paginiCFA Level 3 2012 Guideline AnswersmerrylmorleyÎncă nu există evaluări

- 12 Chapter 9 - Risk Management in Banks NBFCsDocument4 pagini12 Chapter 9 - Risk Management in Banks NBFCsgarima_kukreja_dceÎncă nu există evaluări

- Marketing - Definition, Importance and FunctionsDocument7 paginiMarketing - Definition, Importance and FunctionsPakornTongsukÎncă nu există evaluări

- Study of Tax Saving Schemes in Mutual Funds Mba ProjectDocument74 paginiStudy of Tax Saving Schemes in Mutual Funds Mba ProjectSachin Gala33% (6)

- Choch Trading PlanDocument22 paginiChoch Trading PlanDario Anchava90% (10)