S-ar putea să vă placă și

- Digital Transformation In Banking A Complete Guide - 2020 EditionDe la EverandDigital Transformation In Banking A Complete Guide - 2020 EditionÎncă nu există evaluări

- Fintech 100Document112 paginiFintech 100Meghana VyasÎncă nu există evaluări

- Core Banking System Strategy A Complete Guide - 2020 EditionDe la EverandCore Banking System Strategy A Complete Guide - 2020 EditionÎncă nu există evaluări

- CASHU MerchantDocument20 paginiCASHU MerchantAKASHÎncă nu există evaluări

- Summary of Louis C. Gerken & Wesley A. Whittaker's The Little Book of Venture Capital InvestingDe la EverandSummary of Louis C. Gerken & Wesley A. Whittaker's The Little Book of Venture Capital InvestingÎncă nu există evaluări

- Analysis of Unsecured LoanDocument65 paginiAnalysis of Unsecured LoanJeremy TaylorÎncă nu există evaluări

- Wealth Management in the New Economy: Investor Strategies for Growing, Protecting and Transferring WealthDe la EverandWealth Management in the New Economy: Investor Strategies for Growing, Protecting and Transferring WealthÎncă nu există evaluări

- Banking As A Whole: Investment Bank Commercial BankingDocument50 paginiBanking As A Whole: Investment Bank Commercial Bankingsalva89830% (1)

- Global Opportunity Analysis and Industry Forecast: Payment FacilitatorDocument7 paginiGlobal Opportunity Analysis and Industry Forecast: Payment FacilitatorDavid ChowÎncă nu există evaluări

- Report of the Inter-agency Task Force on Financing for Development 2020: Financing for Sustainable Development ReportDe la EverandReport of the Inter-agency Task Force on Financing for Development 2020: Financing for Sustainable Development ReportÎncă nu există evaluări

- Hsu - Sara - Li - Jianjun China - S Fintech Explosion - Disruption - Innovation - and Survival Columbia UnivDocument361 paginiHsu - Sara - Li - Jianjun China - S Fintech Explosion - Disruption - Innovation - and Survival Columbia UnivNguyễn Đức Tuấn100% (1)

- Digital Financial Services in the Pacific: Experiences and Regulatory IssuesDe la EverandDigital Financial Services in the Pacific: Experiences and Regulatory IssuesÎncă nu există evaluări

- Vijay Shekhar SharmaDocument21 paginiVijay Shekhar SharmaManan Chandarana100% (1)

- Uk Payment Markets SUMMARY 2020: June 2020Document8 paginiUk Payment Markets SUMMARY 2020: June 2020Ankit GuptaÎncă nu există evaluări

- Scaling Ethereum Applications and Cross-Chain Finance @stse Harmony - One/talkDocument11 paginiScaling Ethereum Applications and Cross-Chain Finance @stse Harmony - One/talkstargeizerÎncă nu există evaluări

- Ali PayDocument4 paginiAli PayAhmed GulÎncă nu există evaluări

- Fintech in Asia Pacific: Digital Payment Platforms: October 2019Document42 paginiFintech in Asia Pacific: Digital Payment Platforms: October 2019VaishnaviRaviÎncă nu există evaluări

- Electronic Retail Payment Systems: User Acceptability and Payment Problems in GhanaDocument66 paginiElectronic Retail Payment Systems: User Acceptability and Payment Problems in Ghanaafnankhan1100% (1)

- Payment Systems: Presented To: Dr. Talha Salam Rohab Shafiq l18-3100 Muneeb Suhail l18-3082 Sana Mehr l18-3123Document14 paginiPayment Systems: Presented To: Dr. Talha Salam Rohab Shafiq l18-3100 Muneeb Suhail l18-3082 Sana Mehr l18-3123Muneeb SohailÎncă nu există evaluări

- SmartMoney Digital Payments Strategy in IndiaDocument11 paginiSmartMoney Digital Payments Strategy in IndiaTushar SoniÎncă nu există evaluări

- Collaborating To Win in Canada's Fintech Ecosystem: Accenture 2021 Canadian Fintech ReportDocument71 paginiCollaborating To Win in Canada's Fintech Ecosystem: Accenture 2021 Canadian Fintech ReportRogaes EnpédiÎncă nu există evaluări

- A Framework For Comparison: ResearchDocument75 paginiA Framework For Comparison: Researchbriton336Încă nu există evaluări

- How To Build A Great Mobile ProductDocument15 paginiHow To Build A Great Mobile ProductBRYAND CHEÎncă nu există evaluări

- Bancassurance Report FinalDocument152 paginiBancassurance Report FinalMohammed BenaliÎncă nu există evaluări

- Fintech Collection Report 2021 - TransUnionDocument22 paginiFintech Collection Report 2021 - TransUnionArnelit PhilipÎncă nu există evaluări

- Digital Banking: Time To Rebuild Your Organization (Part III of III)Document14 paginiDigital Banking: Time To Rebuild Your Organization (Part III of III)CognizantÎncă nu există evaluări

- Coss Whitepaper v3Document50 paginiCoss Whitepaper v3ioanabrinzasÎncă nu există evaluări

- 0 RiskScreen Full BrocDocument12 pagini0 RiskScreen Full BrocmyraataÎncă nu există evaluări

- Payments in The Wild PWC Fintech SurveyDocument20 paginiPayments in The Wild PWC Fintech SurveyCrowdfundInsiderÎncă nu există evaluări

- Britannica 03Document9 paginiBritannica 03Sanket BorhadeÎncă nu există evaluări

- Top 100 Leading Global Fintech Report by KPMGDocument112 paginiTop 100 Leading Global Fintech Report by KPMGNofriza Nindiyasari0% (1)

- CB Insights Venture Report Q2 2021Document190 paginiCB Insights Venture Report Q2 2021BrentjaciowÎncă nu există evaluări

- I Used Acorns, Robinhood, and Stash For 2 Years. This Is What I Learned and EarnedDocument8 paginiI Used Acorns, Robinhood, and Stash For 2 Years. This Is What I Learned and Earnedbarakasake300Încă nu există evaluări

- Ms500se PDFDocument5 paginiMs500se PDFEduardo NazarioÎncă nu există evaluări

- How To Better Understand Your Customers Using ContextDocument20 paginiHow To Better Understand Your Customers Using ContextAmitÎncă nu există evaluări

- Wechat Mini Program Playbook For PDFDocument58 paginiWechat Mini Program Playbook For PDFAbel 2LItÎncă nu există evaluări

- Technology in Retail LendingDocument31 paginiTechnology in Retail LendingRedSunÎncă nu există evaluări

- Fintech, Lending and Payment InnovationDocument19 paginiFintech, Lending and Payment InnovationAvengers HeroesÎncă nu există evaluări

- Innovation in Banking Sector in IndiaDocument16 paginiInnovation in Banking Sector in IndiaKishor CoolÎncă nu există evaluări

- CB Insights Banks in Fintech BriefingDocument60 paginiCB Insights Banks in Fintech BriefingHaider RazaÎncă nu există evaluări

- PWC Consumer Lending RadarDocument34 paginiPWC Consumer Lending RadarNaveen TandanÎncă nu există evaluări

- FINTECH in Myanmar PDFDocument4 paginiFINTECH in Myanmar PDFRiza Zausa CuarteroÎncă nu există evaluări

- GS Reasonable DoubtDocument5 paginiGS Reasonable DoubtZerohedgeÎncă nu există evaluări

- Illuminating The Dark Age of Blockchain AlgorandDocument40 paginiIlluminating The Dark Age of Blockchain AlgorandChris DEÎncă nu există evaluări

- Manual For Conducting Market AssessmentDocument62 paginiManual For Conducting Market AssessmentSonya ShannonÎncă nu există evaluări

- How To Become A VTU Airtime DistributorDocument8 paginiHow To Become A VTU Airtime Distributortunlaji100% (1)

- Global Cryptocurrency Mergers and Acquisition and Fundraising Report February 2022Document25 paginiGlobal Cryptocurrency Mergers and Acquisition and Fundraising Report February 2022Sarahi CaballeroÎncă nu există evaluări

- Roland Berger Retail Banking SurveyDocument28 paginiRoland Berger Retail Banking SurveyRicky100% (1)

- Corporate Turnaround TheoryDocument4 paginiCorporate Turnaround TheoryabeeraÎncă nu există evaluări

- In Tech We Trust: A Report From The Economist Intelligence UnitDocument34 paginiIn Tech We Trust: A Report From The Economist Intelligence UnitAbhishekÎncă nu există evaluări

- Public SME Financing and FILP System in JapanDocument36 paginiPublic SME Financing and FILP System in JapanADBI EventsÎncă nu există evaluări

- The Development of Indonesia FintechDocument5 paginiThe Development of Indonesia FintechRisky F Setyo MaulanaÎncă nu există evaluări

- Cooperation Agreement Asic CSSF 4 OctoberDocument6 paginiCooperation Agreement Asic CSSF 4 OctoberCrowdfundInsiderÎncă nu există evaluări

- 2020 Queens Awards Enterprise Press BookDocument126 pagini2020 Queens Awards Enterprise Press BookCrowdfundInsiderÎncă nu există evaluări

- UK Cryptoassets Taskforce Final Report Final WebDocument58 paginiUK Cryptoassets Taskforce Final Report Final WebCrowdfundInsiderÎncă nu există evaluări

- Monzo Annual Report 2019Document92 paginiMonzo Annual Report 2019CrowdfundInsider100% (2)

- House of Commons Treasury Committee Crypto AssetsDocument53 paginiHouse of Commons Treasury Committee Crypto AssetsCrowdfundInsider100% (1)

- 2020 Queens Awards Enterprise Press BookDocument126 pagini2020 Queens Awards Enterprise Press BookCrowdfundInsiderÎncă nu există evaluări

- Bank of Canada Staff Working Paper :document de Travail Du Personnel 2018 - 34 Incentive Compatibility On The Blockchainswp2018-34Document19 paginiBank of Canada Staff Working Paper :document de Travail Du Personnel 2018 - 34 Incentive Compatibility On The Blockchainswp2018-34CrowdfundInsiderÎncă nu există evaluări

- OCC Fintech Charter Manual: Considering-charter-Applications-fintechDocument20 paginiOCC Fintech Charter Manual: Considering-charter-Applications-fintechCrowdfundInsiderÎncă nu există evaluări

- Annual Report and Consolidated Financial Statements For The Year Ended 31 March 2018Document47 paginiAnnual Report and Consolidated Financial Statements For The Year Ended 31 March 2018CrowdfundInsiderÎncă nu există evaluări

- Token Alliance Whitepaper WEB FINALDocument108 paginiToken Alliance Whitepaper WEB FINALCrowdfundInsiderÎncă nu există evaluări

- A Financial System That Creates Economic Opportunities Nonbank Financi...Document222 paginiA Financial System That Creates Economic Opportunities Nonbank Financi...CrowdfundInsiderÎncă nu există evaluări

- Cryptocurrencies and The Economics of Money - Speech by Hyun Song Shin Economic Adviser and Head of Research BISDocument5 paginiCryptocurrencies and The Economics of Money - Speech by Hyun Song Shin Economic Adviser and Head of Research BISCrowdfundInsiderÎncă nu există evaluări

- Annual Report and Consolidated Financial Statements For The Year Ended 31 March 2018Document47 paginiAnnual Report and Consolidated Financial Statements For The Year Ended 31 March 2018CrowdfundInsiderÎncă nu există evaluări

- Crowdcube 2018 Q2 Shareholder Update 2Document11 paginiCrowdcube 2018 Q2 Shareholder Update 2CrowdfundInsiderÎncă nu există evaluări

- EBA Report On Prudential Risks and Opportunities Arising For Institutions From FintechDocument56 paginiEBA Report On Prudential Risks and Opportunities Arising For Institutions From FintechCrowdfundInsiderÎncă nu există evaluări

- Bitcoin Foundation Letter To Congressman Cleaver 5.1.18Document7 paginiBitcoin Foundation Letter To Congressman Cleaver 5.1.18CrowdfundInsiderÎncă nu există evaluări

- Speech by Dr. Veerathai Santiprabhob Governor of The Bank of Thailand July 2018Document6 paginiSpeech by Dr. Veerathai Santiprabhob Governor of The Bank of Thailand July 2018CrowdfundInsiderÎncă nu există evaluări

- AlliedCrowds Cryptocurrency in Emerging Markets DirectoryDocument20 paginiAlliedCrowds Cryptocurrency in Emerging Markets DirectoryCrowdfundInsiderÎncă nu există evaluări

- HR 5877 The Main Street Growth ActDocument10 paginiHR 5877 The Main Street Growth ActCrowdfundInsiderÎncă nu există evaluări

- Mueller Indictment of 12 Russian HackersDocument29 paginiMueller Indictment of 12 Russian HackersShane Vander HartÎncă nu există evaluări

- Virtual Currencies and Central Bans Monetary Policy - Challenges Ahead - European Parliament July 2018Document33 paginiVirtual Currencies and Central Bans Monetary Policy - Challenges Ahead - European Parliament July 2018CrowdfundInsiderÎncă nu există evaluări

- Ontario Securities Commissionn Inv Research 20180628 Taking-Caution-ReportDocument28 paginiOntario Securities Commissionn Inv Research 20180628 Taking-Caution-ReportCrowdfundInsiderÎncă nu există evaluări

- Initial Coin Offerings Report PWC Crypto Valley June 2018Document11 paginiInitial Coin Offerings Report PWC Crypto Valley June 2018CrowdfundInsiderÎncă nu există evaluări

- Let Entrepreneurs Raise Capital Using Finders and Private Placement Brokers by David R. BurtonDocument6 paginiLet Entrepreneurs Raise Capital Using Finders and Private Placement Brokers by David R. BurtonCrowdfundInsiderÎncă nu există evaluări

- FINRA Regulatory-Notice-18-20 Regarding Digital AssetsDocument4 paginiFINRA Regulatory-Notice-18-20 Regarding Digital AssetsCrowdfundInsiderÎncă nu există evaluări

- Funding Circle Oxford Economics Jobs Impact Report 2018Document68 paginiFunding Circle Oxford Economics Jobs Impact Report 2018CrowdfundInsiderÎncă nu există evaluări

- Robert Novy Deputy Assistant Director Office of Investigations United States Secret Service Prepared Testimony Before the United States House of Representatives Committee on Financial Services Subcommittee on Terrorism and Illicit FinanceDocument7 paginiRobert Novy Deputy Assistant Director Office of Investigations United States Secret Service Prepared Testimony Before the United States House of Representatives Committee on Financial Services Subcommittee on Terrorism and Illicit FinanceCrowdfundInsiderÎncă nu există evaluări

- Bill - 115 S 2756Document7 paginiBill - 115 S 2756CrowdfundInsiderÎncă nu există evaluări

- Testimony On "Oversight of The U.S. Securities and Exchange Commission" by Jay Clayton Chairman, U.S. Securities and Exchange Commission Before The Committee On Financial Services June 21 2018Document25 paginiTestimony On "Oversight of The U.S. Securities and Exchange Commission" by Jay Clayton Chairman, U.S. Securities and Exchange Commission Before The Committee On Financial Services June 21 2018CrowdfundInsiderÎncă nu există evaluări

- The OTCQX Advantage - Benefits For International CompaniesDocument20 paginiThe OTCQX Advantage - Benefits For International CompaniesCrowdfundInsiderÎncă nu există evaluări

- InvestmentDocument21 paginiInvestmentQUYEN NGUYEN LE TUÎncă nu există evaluări

- Solutions ACC415Document46 paginiSolutions ACC415gloriyaÎncă nu există evaluări

- The Global EconomyDocument2 paginiThe Global EconomyJean P.Încă nu există evaluări

- Write Your Answer For Part A HereDocument9 paginiWrite Your Answer For Part A HereMATHEW JACOBÎncă nu există evaluări

- Organogram - State Bank of Pakistan: Approved by The Board On October 26, 2020Document1 paginăOrganogram - State Bank of Pakistan: Approved by The Board On October 26, 2020Bilal ZaidiÎncă nu există evaluări

- Bajaj Capital Innovative Marketing Strategies Used by Bajaj Capital Towards Mutual FundsDocument95 paginiBajaj Capital Innovative Marketing Strategies Used by Bajaj Capital Towards Mutual FundsMuma's Doll50% (2)

- SBI Life - EWealth Insurance 300415 V2Document16 paginiSBI Life - EWealth Insurance 300415 V2Tejas JasaniÎncă nu există evaluări

- LeasingDocument17 paginiLeasingvineet ranjanÎncă nu există evaluări

- Financial Markets & Institutions: Maria Jorgeth O. CarbonDocument65 paginiFinancial Markets & Institutions: Maria Jorgeth O. CarbonFelsie Jane Penaso100% (1)

- 083 11 542.pdfp03782 PDFDocument67 pagini083 11 542.pdfp03782 PDFSultana LaboniÎncă nu există evaluări

- The Impact of Key Audit Matters Disclosure On Communicative ValueDocument19 paginiThe Impact of Key Audit Matters Disclosure On Communicative ValueDzulfaqor Tanzil ArifinÎncă nu există evaluări

- Compound Interest FormulaDocument2 paginiCompound Interest FormulaЕлизавета ЛебедеваÎncă nu există evaluări

- GR CACDocument41 paginiGR CACAnna Lyssa BatasÎncă nu există evaluări

- FN107-1342 - Footnotes Levin-Coburn Report.Document1.037 paginiFN107-1342 - Footnotes Levin-Coburn Report.Rick ThomaÎncă nu există evaluări

- 26 Estat PDFDocument4 pagini26 Estat PDFRicky CazaresÎncă nu există evaluări

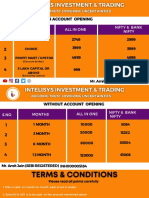

- Intelisys Pricing PlanDocument5 paginiIntelisys Pricing PlanregsÎncă nu există evaluări

- 905 XXXXXXXXX 20267Document2 pagini905 XXXXXXXXX 20267snbnbbÎncă nu există evaluări

- Chapter 02 Final AccountsDocument69 paginiChapter 02 Final AccountsAuthor Jyoti Prakash rathÎncă nu există evaluări

- Trevor Johnson Resume 6-1-2020Document1 paginăTrevor Johnson Resume 6-1-2020api-255502508Încă nu există evaluări

- Introduction To BankingDocument24 paginiIntroduction To Bankingmihir kothariÎncă nu există evaluări

- Mastering QuickBooks Level 2 Learning Manual (PDFDrive)Document240 paginiMastering QuickBooks Level 2 Learning Manual (PDFDrive)Kendrew Sujide100% (1)

- Mortgage Assumption Agreement Template PDFDocument4 paginiMortgage Assumption Agreement Template PDFMarcLouieMagbitangTiraoÎncă nu există evaluări

- FAR 3 Sample QuestionsDocument2 paginiFAR 3 Sample Questionsfrancis dungcaÎncă nu există evaluări

- ACCOUNTING For FOREIGN CURRENCYDocument11 paginiACCOUNTING For FOREIGN CURRENCYmkbooks4uÎncă nu există evaluări

- Mutual Fund PresentationDocument14 paginiMutual Fund PresentationHetal ShahÎncă nu există evaluări

- Penyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Document2 paginiPenyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Vitus JTinusÎncă nu există evaluări

- Designing Capital StructureDocument13 paginiDesigning Capital StructuresiddharthdileepkamatÎncă nu există evaluări

- Srinivasan CVDocument4 paginiSrinivasan CVnarayan patelÎncă nu există evaluări

- Point72 ApplicationDocument2 paginiPoint72 ApplicationNima AttarÎncă nu există evaluări

- Idbi Objectives and Functions of IDBI ObjectivesDocument2 paginiIdbi Objectives and Functions of IDBI ObjectivesRohit Pandey0% (1)