S-ar putea să vă placă și

- Its The Scaling The Organization ChallengeDocument1 paginăIts The Scaling The Organization ChallengeAsm BurraqÎncă nu există evaluări

- Step 1: Consider All The FactsDocument1 paginăStep 1: Consider All The FactsAsm BurraqÎncă nu există evaluări

- The Design and Architecture Analysis WhichDocument1 paginăThe Design and Architecture Analysis WhichAsm BurraqÎncă nu există evaluări

- New Customer Setup in Microsoft Dynamics AX - Contoso Entertainment System US (USMF)Document3 paginiNew Customer Setup in Microsoft Dynamics AX - Contoso Entertainment System US (USMF)Asm BurraqÎncă nu există evaluări

- Assignment 2 Q 15Document2 paginiAssignment 2 Q 15Asm BurraqÎncă nu există evaluări

- Assignment 1 CDocument1 paginăAssignment 1 CAsm BurraqÎncă nu există evaluări

- Dis 7 ADocument1 paginăDis 7 AAsm BurraqÎncă nu există evaluări

- Dis 6 GDocument1 paginăDis 6 GAsm BurraqÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5795)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1091)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- GHMC Property Tax 10-7-163-NRDocument1 paginăGHMC Property Tax 10-7-163-NRndeepak9291384506Încă nu există evaluări

- Economic Impact StudyDocument3 paginiEconomic Impact StudyBASK DigitalÎncă nu există evaluări

- Procedure For Assessment of Income TaxDocument3 paginiProcedure For Assessment of Income Taxdiksha kumariÎncă nu există evaluări

- GST Book by Suraj Agrawal SirDocument560 paginiGST Book by Suraj Agrawal SirPiyush JainÎncă nu există evaluări

- TaxDocument1 paginăTaxHarlene HemorÎncă nu există evaluări

- Impact of Goods and Services Tax (GST) On Indian EconomyDocument5 paginiImpact of Goods and Services Tax (GST) On Indian EconomyMCOM 2050 MAMGAIN RAHUL PRASADÎncă nu există evaluări

- E-Filing of Taxes - A Research PaperDocument8 paginiE-Filing of Taxes - A Research PaperRieke Savitri Agustin0% (1)

- Executive Summary My ReportDocument1 paginăExecutive Summary My ReportNirob Hasan VoorÎncă nu există evaluări

- Implementation of Goods and Services Tax (GST) in IndiaDocument18 paginiImplementation of Goods and Services Tax (GST) in IndiaAkanksha BhattÎncă nu există evaluări

- Delhi Price List - May 2021 (SONET)Document1 paginăDelhi Price List - May 2021 (SONET)Lakshay GautamÎncă nu există evaluări

- Income Taxation Reviewer Banggawan 2019 PDFDocument10 paginiIncome Taxation Reviewer Banggawan 2019 PDFKryzzel Anne Jon100% (1)

- RR No. 9-1998Document10 paginiRR No. 9-1998Rhinnell RiveraÎncă nu există evaluări

- Print: Make Transfer ConfirmDocument1 paginăPrint: Make Transfer ConfirmFaz Rahman100% (1)

- Credit Card BusinessDocument51 paginiCredit Card BusinessAsefÎncă nu există evaluări

- Company Registration CertificateDocument1 paginăCompany Registration Certificatevamsikl100% (1)

- Faq of Banking WebsiteDocument74 paginiFaq of Banking Websitemoney coxÎncă nu există evaluări

- "A Parcel of Land Situated in Sitio Sangab, Municipality of Tanay, Province of Rizal.Document2 pagini"A Parcel of Land Situated in Sitio Sangab, Municipality of Tanay, Province of Rizal.Mark RuzÎncă nu există evaluări

- Revised Standards For AN 4317 Revised Standards For Global Support of Partial ApprovalDocument8 paginiRevised Standards For AN 4317 Revised Standards For Global Support of Partial ApprovalmoltilibriÎncă nu există evaluări

- Film Development Council v. Colon Heritage Realty Corp. DigestDocument2 paginiFilm Development Council v. Colon Heritage Realty Corp. DigestNicole CruzÎncă nu există evaluări

- Account StatementDocument2 paginiAccount StatementRohit GuptaÎncă nu există evaluări

- Evolution of PH TaxationDocument45 paginiEvolution of PH TaxationShai Anne CortezÎncă nu există evaluări

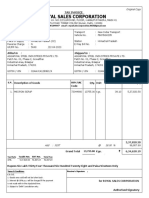

- Royal Sales Corporation: Tax InvoiceDocument2 paginiRoyal Sales Corporation: Tax InvoiceKailash GoyalÎncă nu există evaluări

- Computing Pay For Work Done On: Below Are The Steps On Computing Employee's SalaryDocument20 paginiComputing Pay For Work Done On: Below Are The Steps On Computing Employee's Salaryburn lastÎncă nu există evaluări

- Packing List: This Packing List Must Be Completed in EnglishDocument2 paginiPacking List: This Packing List Must Be Completed in EnglishJuarez NetoÎncă nu există evaluări

- Customer StatementDocument4 paginiCustomer StatementMention UnwanaÎncă nu există evaluări

- Julien Day School FeesDocument22 paginiJulien Day School Fees32.Soumik AdakÎncă nu există evaluări

- To Tax Church PropertyDocument2 paginiTo Tax Church PropertyKino MarinayÎncă nu există evaluări

- IV. CIR vs. PALDocument14 paginiIV. CIR vs. PALStef OcsalevÎncă nu există evaluări

- Certificate of Compensation Payment/Tax Withheld: Rivera St. San Francisco, Red-V, Ibabang Dupay, Lucena CityDocument2 paginiCertificate of Compensation Payment/Tax Withheld: Rivera St. San Francisco, Red-V, Ibabang Dupay, Lucena CityACYATAN & CO., CPAs 2020Încă nu există evaluări

- Tax Setup Document PDFDocument26 paginiTax Setup Document PDFhariyhnÎncă nu există evaluări