S-ar putea să vă placă și

- Deed of Conditional Sal1Document2 paginiDeed of Conditional Sal1Julian HemedezÎncă nu există evaluări

- Chattel Mortgage: AnnumDocument2 paginiChattel Mortgage: AnnumArmand Rey SabidoÎncă nu există evaluări

- CIR v. CA (Jan. 20, 1999)Document14 paginiCIR v. CA (Jan. 20, 1999)Crizza RondinaÎncă nu există evaluări

- Revenue Regulations No. 6-2008Document7 paginiRevenue Regulations No. 6-2008Krstn RsslliniÎncă nu există evaluări

- Donor's Tax-2Document36 paginiDonor's Tax-2Razel Mhin MendozaÎncă nu există evaluări

- FORM NO. 2. Acknowledgement of Instrument Consisting of Two or More PagesDocument1 paginăFORM NO. 2. Acknowledgement of Instrument Consisting of Two or More PagesXirkul TupasÎncă nu există evaluări

- Case Digest Local GovernmentDocument188 paginiCase Digest Local GovernmentGideon Tangan Ines Jr.Încă nu există evaluări

- Agarian Law and Social Legislation SyllabusDocument6 paginiAgarian Law and Social Legislation SyllabusAstakunÎncă nu există evaluări

- Deed of Absolute Sale LandDocument3 paginiDeed of Absolute Sale LandKriselle Armi Umingan100% (2)

- Affidavit of Damage To VehicleDocument1 paginăAffidavit of Damage To VehicleJohn Mark OpenianoÎncă nu există evaluări

- Denr Administrative Order No. 2007 - 12Document9 paginiDenr Administrative Order No. 2007 - 12cookiemonster1996Încă nu există evaluări

- Sale Lopez To Anuran - Dors PDFDocument3 paginiSale Lopez To Anuran - Dors PDFMars Rañola-CamilonÎncă nu există evaluări

- Fort Bonifacio V CirDocument4 paginiFort Bonifacio V CirJasÎncă nu există evaluări

- SSSForms Change Request PDFDocument2 paginiSSSForms Change Request PDFRon Ico Ramos100% (1)

- FINALS Summary of DecisionDocument15 paginiFINALS Summary of DecisionKirk Patrick LopezÎncă nu există evaluări

- Contract To SellDocument2 paginiContract To SellUnsolicited CommentÎncă nu există evaluări

- Revised Ortega Notes Book I General Provisions: Criminal LawDocument63 paginiRevised Ortega Notes Book I General Provisions: Criminal LawHaniel GAÎncă nu există evaluări

- Tax Remedies (Part 1)Document32 paginiTax Remedies (Part 1)AysÎncă nu există evaluări

- Affidavit of DenialDocument1 paginăAffidavit of DenialGerwin100% (1)

- Contract of Loan and Promissory NoteDocument2 paginiContract of Loan and Promissory NoteZor Ro100% (1)

- AppsDocument8 paginiAppsNathaniel CamachoÎncă nu există evaluări

- Deed of Sale of Motor VehicleDocument1 paginăDeed of Sale of Motor Vehiclebenjamin ladesmaÎncă nu există evaluări

- Deed of Absolute SaleDocument2 paginiDeed of Absolute SaleClaire SilvestreÎncă nu există evaluări

- Deed of Sale of Motor VehicleDocument7 paginiDeed of Sale of Motor VehicleMarc CalderonÎncă nu există evaluări

- DEED OF SALE With Assumption of ObligationDocument2 paginiDEED OF SALE With Assumption of ObligationShai Gogolin100% (1)

- BIS - No-Dollar Importation of Used Motor Vehicle (Balikbayan) EO 156-LpvDocument3 paginiBIS - No-Dollar Importation of Used Motor Vehicle (Balikbayan) EO 156-Lpvlito77Încă nu există evaluări

- NIRC As AmendedDocument249 paginiNIRC As Amendedsteve_roldanÎncă nu există evaluări

- Contract To Sell Edited ReguaDocument20 paginiContract To Sell Edited ReguaFlorabel LazaroÎncă nu există evaluări

- RA 8179 Amendatory Law On Foreign Invest ActDocument5 paginiRA 8179 Amendatory Law On Foreign Invest ActCrislene CruzÎncă nu există evaluări

- Option To PurchaseDocument3 paginiOption To PurchasePonching OriosteÎncă nu există evaluări

- Deed of Absolute Sale of Large CattleDocument3 paginiDeed of Absolute Sale of Large CattleChristian jade HensonÎncă nu există evaluări

- Bureau of Jail Management and Penology: Republic of The Philippines Department of The Interior and Local GovernmentDocument12 paginiBureau of Jail Management and Penology: Republic of The Philippines Department of The Interior and Local GovernmentAl DrinÎncă nu există evaluări

- Contract of LeaseDocument3 paginiContract of LeaseJosh YamatÎncă nu există evaluări

- Deed of Sale of Motor Vehicle With Assumption of MortgageDocument5 paginiDeed of Sale of Motor Vehicle With Assumption of MortgageAron PunciaÎncă nu există evaluări

- Affidavit of SupportDocument1 paginăAffidavit of SupportRaymund Christian Ong AbrantesÎncă nu există evaluări

- Deed of Sale of Motor VehicleDocument1 paginăDeed of Sale of Motor VehicleSampaguita RamosÎncă nu există evaluări

- RMC No. 32-2022Document5 paginiRMC No. 32-2022Shiela Marie MaraonÎncă nu există evaluări

- Deed of Sale of A Motorcycle With Side CarDocument3 paginiDeed of Sale of A Motorcycle With Side CarMikko AcubaÎncă nu există evaluări

- Guidelines On Petitions For Money Claim Filed With COADocument21 paginiGuidelines On Petitions For Money Claim Filed With COAcoadilgrovÎncă nu există evaluări

- Hereinafter Referred To As VENDEEDocument2 paginiHereinafter Referred To As VENDEEEun YoonÎncă nu există evaluări

- Deed of Sale - Motor VehicleDocument2 paginiDeed of Sale - Motor VehicledcmanlangitÎncă nu există evaluări

- Consent DecreeDocument29 paginiConsent DecreeJermain GibsonÎncă nu există evaluări

- Deed of Conditional SaleDocument3 paginiDeed of Conditional SaleSharrah San MiguelÎncă nu există evaluări

- Deed of Sale of Motor VehicleDocument1 paginăDeed of Sale of Motor Vehicleveniceangeli1001 DCÎncă nu există evaluări

- Presumption of Negligence Pestano vs. Sumayang FactsDocument2 paginiPresumption of Negligence Pestano vs. Sumayang FactsJayÎncă nu există evaluări

- OCA-Circular-No.-107-2013 Jail VisitationDocument7 paginiOCA-Circular-No.-107-2013 Jail VisitationJordan GimarazÎncă nu există evaluări

- Extrajudicial Settlement of Estate in The PhilippinesDocument4 paginiExtrajudicial Settlement of Estate in The PhilippinesDon Astorga Dehayco0% (1)

- Special Power of Atty - BIR - TemplateDocument1 paginăSpecial Power of Atty - BIR - TemplatePSLaw OfficeÎncă nu există evaluări

- LTFRB vs. G.V. Florida TransportDocument3 paginiLTFRB vs. G.V. Florida TransportApril GonzagaÎncă nu există evaluări

- Memorandum of Agreement - Tinambacan-Andrew SantosDocument4 paginiMemorandum of Agreement - Tinambacan-Andrew SantosDerrick de los ReyesÎncă nu există evaluări

- Crim Reviewer Section 00224 PDFDocument1 paginăCrim Reviewer Section 00224 PDFLawStudent101412Încă nu există evaluări

- Spa - To Court - BLANKDocument1 paginăSpa - To Court - BLANKernesto del rosarioÎncă nu există evaluări

- Buy Sale Agreement 123ZDocument5 paginiBuy Sale Agreement 123ZcefuneslpezÎncă nu există evaluări

- Revenue Memorandum Order No. 35-1990Document2 paginiRevenue Memorandum Order No. 35-1990Kaye MendozaÎncă nu există evaluări

- Easement of Right of WayDocument3 paginiEasement of Right of WayChristian Jade HensonÎncă nu există evaluări

- Bar Exam TipsDocument2 paginiBar Exam TipsNyl AnerÎncă nu există evaluări

- Callanta Vs OmbudsmanDocument7 paginiCallanta Vs OmbudsmanAnton SingeÎncă nu există evaluări

- Callanta V Ombudsman G.R. Nos. 115253-74 January 30, 1998Document12 paginiCallanta V Ombudsman G.R. Nos. 115253-74 January 30, 1998Ernesto NeriÎncă nu există evaluări

- Republic of Tile Philippines Court of Tax Appeals Quezon CityDocument43 paginiRepublic of Tile Philippines Court of Tax Appeals Quezon CityCL DelabahanÎncă nu există evaluări

- Cta 3D Ac 00077 D 2012nov15 Ass PDFDocument14 paginiCta 3D Ac 00077 D 2012nov15 Ass PDFr....aÎncă nu există evaluări

- Real Estate Brokerage PracticeDocument23 paginiReal Estate Brokerage PracticeGeorge Poligratis Rico67% (3)

- Valuation of Gross Estate TaxesDocument1 paginăValuation of Gross Estate TaxesGeorge Poligratis RicoÎncă nu există evaluări

- Real Estate Mathematics Sample Problems (Ref: 0505) : I. Perimeter Fencing ProblemDocument4 paginiReal Estate Mathematics Sample Problems (Ref: 0505) : I. Perimeter Fencing ProblemGeorge Poligratis RicoÎncă nu există evaluări

- Sample Computation of Estate Tax Part 2Document4 paginiSample Computation of Estate Tax Part 2George Poligratis RicoÎncă nu există evaluări

- Real Estate Mathematics SAMPLE PROBLEMS (REF: 0505) W/ SolutionDocument11 paginiReal Estate Mathematics SAMPLE PROBLEMS (REF: 0505) W/ SolutionGeorge Poligratis Rico100% (2)

- Sample Computation of Estate TaxDocument2 paginiSample Computation of Estate TaxGeorge Poligratis RicoÎncă nu există evaluări

- Donor Tax Rates and CreditDocument2 paginiDonor Tax Rates and CreditGeorge Poligratis RicoÎncă nu există evaluări

- Estate TaxesDocument3 paginiEstate TaxesGeorge Poligratis RicoÎncă nu există evaluări

- Gross Gift Valuation and CompositionDocument2 paginiGross Gift Valuation and CompositionGeorge Poligratis RicoÎncă nu există evaluări

- Donor's TAxDocument2 paginiDonor's TAxGeorge Poligratis RicoÎncă nu există evaluări

- Estate Tax New ProvisionsDocument1 paginăEstate Tax New ProvisionsGeorge Poligratis RicoÎncă nu există evaluări

- Subdivision Approach Valuation: Drainage, Water & Other Utilities) P 100,000,000Document1 paginăSubdivision Approach Valuation: Drainage, Water & Other Utilities) P 100,000,000George Poligratis RicoÎncă nu există evaluări

- Exemptions From Donor's TaxDocument1 paginăExemptions From Donor's TaxGeorge Poligratis RicoÎncă nu există evaluări

- Donor's Tax ProblemsDocument3 paginiDonor's Tax ProblemsGeorge Poligratis RicoÎncă nu există evaluări

- REVIEWER: Mathematics in Brokerage Practice Problems/QuestionDocument18 paginiREVIEWER: Mathematics in Brokerage Practice Problems/QuestionGeorge Poligratis Rico100% (1)

- Classification of Donors TaxDocument1 paginăClassification of Donors TaxGeorge Poligratis RicoÎncă nu există evaluări

- Deductions From Gross GiftsDocument1 paginăDeductions From Gross GiftsGeorge Poligratis RicoÎncă nu există evaluări

- Administrative Requirements of Donors TaxDocument2 paginiAdministrative Requirements of Donors TaxGeorge Poligratis RicoÎncă nu există evaluări

- Basis and Rate of Donors TaxDocument2 paginiBasis and Rate of Donors TaxGeorge Poligratis RicoÎncă nu există evaluări

- Bir-Taxation - Definition of TermsDocument2 paginiBir-Taxation - Definition of TermsGeorge Poligratis RicoÎncă nu există evaluări

- 25 RESA vs. MO 39Document37 pagini25 RESA vs. MO 39George Poligratis Rico100% (2)

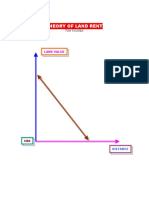

- 6-3-Land Rent Theory PDFDocument1 pagină6-3-Land Rent Theory PDFGeorge Poligratis RicoÎncă nu există evaluări

- 6-2-Car Appraisal PDFDocument1 pagină6-2-Car Appraisal PDFGeorge Poligratis RicoÎncă nu există evaluări

- Bir Taxation PurposeDocument2 paginiBir Taxation PurposeGeorge Poligratis RicoÎncă nu există evaluări

- Accounting & Taxation On Real Estate Transactions by DDV Nov 2015Document159 paginiAccounting & Taxation On Real Estate Transactions by DDV Nov 2015George Poligratis RicoÎncă nu există evaluări

- Exponential Geometrical Linear-Growth RateDocument1 paginăExponential Geometrical Linear-Growth RateGeorge Poligratis RicoÎncă nu există evaluări

- 1examination On Legal Aspects of Sale PDFDocument53 pagini1examination On Legal Aspects of Sale PDFGeorge Poligratis RicoÎncă nu există evaluări

- i-PROBLEM CASH FLOW FORMULA EL-377 A MS EXCEL PDFDocument1 paginăi-PROBLEM CASH FLOW FORMULA EL-377 A MS EXCEL PDFGeorge Poligratis RicoÎncă nu există evaluări

- ILLUSTRATION - RESIDUAL TECHNIQUE by PDFDocument12 paginiILLUSTRATION - RESIDUAL TECHNIQUE by PDFGeorge Poligratis RicoÎncă nu există evaluări

- DIFFERENT REPAYMENT PLAN by PDFDocument4 paginiDIFFERENT REPAYMENT PLAN by PDFGeorge Poligratis RicoÎncă nu există evaluări

- Dae Sung Hi Tech v. Sarasota Stamps - ComplaintDocument67 paginiDae Sung Hi Tech v. Sarasota Stamps - ComplaintSarah Burstein100% (1)

- 33 - Unson vs. AbellaDocument8 pagini33 - Unson vs. Abellavince005Încă nu există evaluări

- Roberts v. Locke PDFDocument7 paginiRoberts v. Locke PDFAbigayle GapongliÎncă nu există evaluări

- LAWS3111 Case Notes Lecture 1 - Title To LandDocument11 paginiLAWS3111 Case Notes Lecture 1 - Title To LandThoughts of a Law Student100% (1)

- Henry J. Werdann Margaret Werdann v. Bill & Jenny Enterprises, Incorporated, and Niles Austin William Jones, 995 F.2d 1065, 4th Cir. (1993)Document6 paginiHenry J. Werdann Margaret Werdann v. Bill & Jenny Enterprises, Incorporated, and Niles Austin William Jones, 995 F.2d 1065, 4th Cir. (1993)Scribd Government DocsÎncă nu există evaluări

- All Work and No Pay - Paul HeinDocument48 paginiAll Work and No Pay - Paul HeinJeffrey ChangÎncă nu există evaluări

- Bailey v. Courchesne Courchesne, ANDap-99-021 (Androscoggin Super. CT., 2000)Document3 paginiBailey v. Courchesne Courchesne, ANDap-99-021 (Androscoggin Super. CT., 2000)Chris BuckÎncă nu există evaluări

- Merrero Vs BocarDocument7 paginiMerrero Vs BocarKrishaRueco-AngoluanÎncă nu există evaluări

- Rule of Strict Liability in Motor Accidents Adopted - Air 2001 SC 485Document6 paginiRule of Strict Liability in Motor Accidents Adopted - Air 2001 SC 485Sridhara babu. N - ಶ್ರೀಧರ ಬಾಬು. ಎನ್Încă nu există evaluări

- John J. Hanna v. Commissioner of Internal Revenue, 763 F.2d 171, 4th Cir. (1985)Document4 paginiJohn J. Hanna v. Commissioner of Internal Revenue, 763 F.2d 171, 4th Cir. (1985)Scribd Government DocsÎncă nu există evaluări

- Warrant Cases Before MagistrateDocument13 paginiWarrant Cases Before MagistratetusharÎncă nu există evaluări

- Ortiz V KayananDocument2 paginiOrtiz V KayananMark Anthony Javellana SicadÎncă nu există evaluări

- Plea BargainingDocument10 paginiPlea Bargainingtunkucute05Încă nu există evaluări

- Adversary ProceedingDocument6 paginiAdversary ProceedingDerrick HannaÎncă nu există evaluări

- Santos vs. YatcoDocument3 paginiSantos vs. YatcoVeraNataa100% (1)

- Digest - in Re BadoyDocument1 paginăDigest - in Re Badoyianlayno0% (1)

- United States v. Jewell, 60 F.3d 20, 1st Cir. (1995)Document6 paginiUnited States v. Jewell, 60 F.3d 20, 1st Cir. (1995)Scribd Government DocsÎncă nu există evaluări

- Ruth Pollack SCOTUS Petition For Certiorari On 2nd Circuit Court FraudDocument205 paginiRuth Pollack SCOTUS Petition For Certiorari On 2nd Circuit Court FraudBeverly TranÎncă nu există evaluări

- DM Consunji V CA DIGEST PDFDocument1 paginăDM Consunji V CA DIGEST PDFAKÎncă nu există evaluări

- Joint Letter Brief RE: Discovery Matter, Hard Drive Productions, Inc. v. Does 1-33, 3:11-cv-03827-LBDocument5 paginiJoint Letter Brief RE: Discovery Matter, Hard Drive Productions, Inc. v. Does 1-33, 3:11-cv-03827-LBcopyrightclerkÎncă nu există evaluări

- United States v. DiBiase, 1st Cir. (1995)Document20 paginiUnited States v. DiBiase, 1st Cir. (1995)Scribd Government DocsÎncă nu există evaluări

- 46 To 54 Due Process Full CasesDocument65 pagini46 To 54 Due Process Full CasesLAW10101Încă nu există evaluări

- Week 6 Case 5Document6 paginiWeek 6 Case 5Earl NuydaÎncă nu există evaluări

- United States v. Ashraf Yousef Abozid, Mohsin Rashid, Parvez Ali, Isaac Agha, AKA Hazem Agha, 257 F.3d 191, 2d Cir. (2001)Document12 paginiUnited States v. Ashraf Yousef Abozid, Mohsin Rashid, Parvez Ali, Isaac Agha, AKA Hazem Agha, 257 F.3d 191, 2d Cir. (2001)Scribd Government DocsÎncă nu există evaluări

- Property Cases 1 (Incomplete, No: Ayala Land V Ray Burton (1969)Document17 paginiProperty Cases 1 (Incomplete, No: Ayala Land V Ray Burton (1969)Jierah ManahanÎncă nu există evaluări

- Rule 13 Filing and Service of PleadingsDocument2 paginiRule 13 Filing and Service of PleadingsSushenSisonÎncă nu există evaluări

- Chapter 5 - IndigoDocument7 paginiChapter 5 - Indigosharique alamÎncă nu există evaluări

- Carandang v. SantiagoDocument3 paginiCarandang v. SantiagoPu Pujalte0% (1)

- Masangkay v. Del RosarioDocument19 paginiMasangkay v. Del RosarioRea Jane B. MalcampoÎncă nu există evaluări

- Yakub Memon Sem 8Document18 paginiYakub Memon Sem 8arnavbishnoiÎncă nu există evaluări