S-ar putea să vă placă și

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- K-12 Science Curriculum Guide promotes scientific literacyDocument66 paginiK-12 Science Curriculum Guide promotes scientific literacycatherinefernandezÎncă nu există evaluări

- Revenue Regulation No. 16-2005Document0 paginiRevenue Regulation No. 16-2005Kaye MendozaÎncă nu există evaluări

- Ping Pong AnyoneDocument5 paginiPing Pong AnyoneSy HimÎncă nu există evaluări

- K-12 Science Curriculum Guide promotes scientific literacyDocument66 paginiK-12 Science Curriculum Guide promotes scientific literacycatherinefernandezÎncă nu există evaluări

- 21429RR15 2005Document3 pagini21429RR15 2005Sy HimÎncă nu există evaluări

- 27697rr No. 02-2006Document10 pagini27697rr No. 02-2006Sy HimÎncă nu există evaluări

- 29411rr No. 06-2006Document7 pagini29411rr No. 06-2006Sy HimÎncă nu există evaluări

- Chapter 1Document8 paginiChapter 1Rafael GarciaÎncă nu există evaluări

- Revenue Regulations No. 7 - 2006: Quezon City May 18, 2006Document2 paginiRevenue Regulations No. 7 - 2006: Quezon City May 18, 2006Sy HimÎncă nu există evaluări

- 27695rr No. 01-2006Document4 pagini27695rr No. 01-2006Sy HimÎncă nu există evaluări

- 28495rr No. 04-2006Document11 pagini28495rr No. 04-2006Jas MineÎncă nu există evaluări

- 21171rr05 14Document54 pagini21171rr05 14Sy HimÎncă nu există evaluări

- 29083rr No. 05-2006Document1 pagină29083rr No. 05-2006Sy HimÎncă nu există evaluări

- Implementing Guidelines on Revised Tax Rates for Alcohol and TobaccoDocument44 paginiImplementing Guidelines on Revised Tax Rates for Alcohol and TobaccoSy HimÎncă nu există evaluări

- 26814rr No. 19-2005Document1 pagină26814rr No. 19-2005Sy HimÎncă nu există evaluări

- 26715rr No. 18-2005Document9 pagini26715rr No. 18-2005Sy HimÎncă nu există evaluări

- Ask For ReceiptDocument2 paginiAsk For ReceiptSy HimÎncă nu există evaluări

- Philippine Tax Subsidy Regulations for Subic-Clark-Tarlac Expressway ProjectDocument10 paginiPhilippine Tax Subsidy Regulations for Subic-Clark-Tarlac Expressway ProjectSy HimÎncă nu există evaluări

- 16771rr05 05Document8 pagini16771rr05 05Sy HimÎncă nu există evaluări

- 17541rr05 06Document6 pagini17541rr05 06Sy HimÎncă nu există evaluări

- 21103RR 11-2005Document2 pagini21103RR 11-2005Sy HimÎncă nu există evaluări

- Republika NG Pilipinas Kagawaran NG Pananalapi Kawanihan NG Rentas InternasDocument2 paginiRepublika NG Pilipinas Kagawaran NG Pananalapi Kawanihan NG Rentas InternasSy HimÎncă nu există evaluări

- 20286RR 8-2005Document3 pagini20286RR 8-2005Sy HimÎncă nu există evaluări

- 16769rr05 04Document4 pagini16769rr05 04Sy HimÎncă nu există evaluări

- 16723RR 1-2005Document4 pagini16723RR 1-2005Sy HimÎncă nu există evaluări

- Ensuring Tax Compliance for Government ContractsDocument4 paginiEnsuring Tax Compliance for Government ContractsCarla GrepoÎncă nu există evaluări

- 15711rr04 11Document16 pagini15711rr04 11Sy HimÎncă nu există evaluări

- 15439rr04 12Document16 pagini15439rr04 12Sy HimÎncă nu există evaluări

- 15441rr04 13Document14 pagini15441rr04 13Sy HimÎncă nu există evaluări

- 14592rr04 10Document2 pagini14592rr04 10Sy HimÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Tax Invoice Galaxy Note20Document1 paginăTax Invoice Galaxy Note20akshaybasal jainÎncă nu există evaluări

- AM Tax Working New RegimeDocument6 paginiAM Tax Working New RegimeabhishekmenonÎncă nu există evaluări

- Don't Miss Out On Free School Meals!: Application Form 2012/2013Document1 paginăDon't Miss Out On Free School Meals!: Application Form 2012/2013esolnexusÎncă nu există evaluări

- Superannuation WorksheetDocument2 paginiSuperannuation WorksheetAaron100% (1)

- Img 0001 PDFDocument9 paginiImg 0001 PDFAnonymous mzkNojivÎncă nu există evaluări

- Collection & Recovery of TaxDocument2 paginiCollection & Recovery of TaxrichaÎncă nu există evaluări

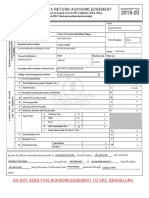

- Indian Income Tax Return Acknowledgement for AY 2019-20Document1 paginăIndian Income Tax Return Acknowledgement for AY 2019-20Sourav KumarÎncă nu există evaluări

- Federal Board of Revenue (FBR) Mcqs Federal Board of Revenue (FBR)Document14 paginiFederal Board of Revenue (FBR) Mcqs Federal Board of Revenue (FBR)Rana NabeelÎncă nu există evaluări

- SalarySchemeDocument2 paginiSalarySchemeMichelle Acebuche SibayanÎncă nu există evaluări

- Akmur Sentosa Jaya Gemah Ripah Sales ReportDocument2 paginiAkmur Sentosa Jaya Gemah Ripah Sales ReportSteve MedhurstÎncă nu există evaluări

- Taxation For CooperativesDocument27 paginiTaxation For Cooperativesdecember231981Încă nu există evaluări

- BIR Form No. 0608 PDFDocument2 paginiBIR Form No. 0608 PDFPaolo MartinÎncă nu există evaluări

- ERH BusinessEntityComparisonTableDocument1 paginăERH BusinessEntityComparisonTableEliss CainÎncă nu există evaluări

- College Savings Plan ComparisonDocument2 paginiCollege Savings Plan Comparisoncharanmann9165Încă nu există evaluări

- TMC Vs CIRDocument3 paginiTMC Vs CIREllaine BernardinoÎncă nu există evaluări

- Kensington Practice Pension Letter Joiner Mrs K. Paraiso Da Rocha 01-07-2023Document2 paginiKensington Practice Pension Letter Joiner Mrs K. Paraiso Da Rocha 01-07-2023Mia ZhandÎncă nu există evaluări

- Confidential: Infosys 29-08-2016 JUN 9 R Anvesh Banda 0 Designation Software EngineerDocument1 paginăConfidential: Infosys 29-08-2016 JUN 9 R Anvesh Banda 0 Designation Software EngineerAbdul Nayeem100% (1)

- BIR Ruling No 274-87Document3 paginiBIR Ruling No 274-87Peggy SalazarÎncă nu există evaluări

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument1 paginăBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountYash SinghviÎncă nu există evaluări

- India OSP GST Challan ReportDocument26 paginiIndia OSP GST Challan ReportLaxmidhara NayakÎncă nu există evaluări

- DST On Policy Holders Registered With PEZADocument5 paginiDST On Policy Holders Registered With PEZACkey ArÎncă nu există evaluări

- Fiserv November SalaryDocument1 paginăFiserv November SalarySiddharthÎncă nu există evaluări

- MCQ'S Practies: Direct TaxDocument12 paginiMCQ'S Practies: Direct TaxTina AggarwalÎncă nu există evaluări

- Tax Sept2002Document10 paginiTax Sept2002Insan KerdilÎncă nu există evaluări

- Tax Invoice: Purani Bazar Jamui-811307 (Bihar) GSTIN/UIN: 10AIIPB8433E1ZV State Name: Bihar, Code: 10Document1 paginăTax Invoice: Purani Bazar Jamui-811307 (Bihar) GSTIN/UIN: 10AIIPB8433E1ZV State Name: Bihar, Code: 10Randhir SinghÎncă nu există evaluări

- Fa Ia Fa2210d.2 923 CDocument11 paginiFa Ia Fa2210d.2 923 CtjyxwvjyttÎncă nu există evaluări

- Tax Payment Challan for Company DeducteesDocument1 paginăTax Payment Challan for Company DeducteesMadhyam JeswaniÎncă nu există evaluări

- June PayslipDocument3 paginiJune Paysliphennieswart62Încă nu există evaluări

- Nerolac Invoice n221011406Document5 paginiNerolac Invoice n221011406PANKAJ CHOPDAÎncă nu există evaluări

- CIR V General FoodsDocument2 paginiCIR V General FoodsNelsonPolinarLaurdenÎncă nu există evaluări