S-ar putea să vă placă și

- Cotton Usa UpdatesDocument2 paginiCotton Usa UpdatescottontradeÎncă nu există evaluări

- August ReportDocument2 paginiAugust ReportcottontradeÎncă nu există evaluări

- Cotton USA Global Fax Update - May 2010Document2 paginiCotton USA Global Fax Update - May 2010cottontradeÎncă nu există evaluări

- World Cotton Situation 2010Document5 paginiWorld Cotton Situation 2010Dr. Hussain NaqviÎncă nu există evaluări

- GF0817new LogoDocument2 paginiGF0817new LogoDiawage SackoÎncă nu există evaluări

- COTTON USA Global Fax Update - November 2010Document2 paginiCOTTON USA Global Fax Update - November 2010mlganesh666Încă nu există evaluări

- Forecast Month - June 2010 Table Beginning Year - 2006 Table Beginning Quarter - 200601Document38 paginiForecast Month - June 2010 Table Beginning Year - 2006 Table Beginning Quarter - 200601younesselkandoussiÎncă nu există evaluări

- Presentation MarketReportTanzania 02Document11 paginiPresentation MarketReportTanzania 02ngobilegodwin121Încă nu există evaluări

- Indian Sugar Mills Production and Pricing TrendsDocument6 paginiIndian Sugar Mills Production and Pricing TrendsdangmilanÎncă nu există evaluări

- MKT Shre Redymd AprlDocument1 paginăMKT Shre Redymd AprlkbinayÎncă nu există evaluări

- Viability of Coffee Farming As A Business: Lucy MuriithiDocument11 paginiViability of Coffee Farming As A Business: Lucy MuriithiTrey NgugiÎncă nu există evaluări

- Lampiran A-01: Investasi Ikan Kerapu Material Ukuran Satuan Harga @unit Jumlah Unit Unit KerambaDocument16 paginiLampiran A-01: Investasi Ikan Kerapu Material Ukuran Satuan Harga @unit Jumlah Unit Unit KerambafadliÎncă nu există evaluări

- Atbsp Map-Abcd 070218 PDFDocument113 paginiAtbsp Map-Abcd 070218 PDFGsp ChrismonÎncă nu există evaluări

- Sugarcane Crisis of Uttar Pradesh: 2013: Economic Survey of IndiaDocument28 paginiSugarcane Crisis of Uttar Pradesh: 2013: Economic Survey of IndiaAishwarya RaoÎncă nu există evaluări

- NAZMUL4Document28 paginiNAZMUL4Ar N RimonÎncă nu există evaluări

- Aare DairyDocument2 paginiAare Dairyshailesh98233275Încă nu există evaluări

- Nouman Sarfaraz: Group Members: - Zaka Ul HassanDocument22 paginiNouman Sarfaraz: Group Members: - Zaka Ul HassanZaka Ul Hassan100% (1)

- Vava'u Farmers CouncilDocument2 paginiVava'u Farmers CouncilAkosita100% (1)

- Excel FormulaDocument6 paginiExcel FormulaChandan_RicharyaaÎncă nu există evaluări

- Design of A Sprinkler Irrigation System For Sun Flower in Malawa-A VillageDocument19 paginiDesign of A Sprinkler Irrigation System For Sun Flower in Malawa-A VillageAodi NabothÎncă nu există evaluări

- Strenthening of BankDocument12 paginiStrenthening of BankVinay GurramÎncă nu există evaluări

- MAP Market Feasibility StudyDocument39 paginiMAP Market Feasibility StudyJohn Leonard FazÎncă nu există evaluări

- Sip Assessment Ab-ProcessDocument2 paginiSip Assessment Ab-Processhoney lee longaresÎncă nu există evaluări

- Morning Briefing: Afnan Iqbal 30 January 2020Document16 paginiMorning Briefing: Afnan Iqbal 30 January 2020afnaniqbalÎncă nu există evaluări

- Morning Breifing 30-01-2020Document16 paginiMorning Breifing 30-01-2020afnaniqbalÎncă nu există evaluări

- EQ FR RR 14-01 1300 1000 1600 14-02 1511 1000 900 14-03 14-04 14-05 14-06 14-07 14-08 14-09 14-10 Date Pres Date Prev Days RUN Hours RUN FR PrevDocument5 paginiEQ FR RR 14-01 1300 1000 1600 14-02 1511 1000 900 14-03 14-04 14-05 14-06 14-07 14-08 14-09 14-10 Date Pres Date Prev Days RUN Hours RUN FR PrevMike OrtizÎncă nu există evaluări

- 3.0 Agricultural SectorDocument29 pagini3.0 Agricultural SectorPei YuÎncă nu există evaluări

- Cmo October 2017 ForecastsDocument4 paginiCmo October 2017 Forecastsyan energiaÎncă nu există evaluări

- Currency Futures in India-Status Check After One Year-Vrk100-14102009Document13 paginiCurrency Futures in India-Status Check After One Year-Vrk100-14102009RamaKrishna Vadlamudi, CFAÎncă nu există evaluări

- World Bank Commodities Price Forecast (Nominal US Dollars)Document4 paginiWorld Bank Commodities Price Forecast (Nominal US Dollars)marceloÎncă nu există evaluări

- Km. Intan Daya 7Document15 paginiKm. Intan Daya 7muhammad aminuddinÎncă nu există evaluări

- IMO DCS Musi ProsperityDocument24 paginiIMO DCS Musi ProsperitySanusi AbdullahÎncă nu există evaluări

- Cara Membuat Larutan Induk Alum PACDocument3 paginiCara Membuat Larutan Induk Alum PACSoniaBungaDatuanÎncă nu există evaluări

- Al-Karam Textile Mills (PVT.) LTD.: Henriette / GLCG, (Esprit)Document4 paginiAl-Karam Textile Mills (PVT.) LTD.: Henriette / GLCG, (Esprit)Bouleghab HamidÎncă nu există evaluări

- Brick LayerDocument8 paginiBrick Layerram skytradeÎncă nu există evaluări

- Q1 2009-10 Performance Update GCPLDocument31 paginiQ1 2009-10 Performance Update GCPLArks_Dawn_5956Încă nu există evaluări

- Malaysia's Agricultural Sector: Growth, Production and Policy TrendsDocument58 paginiMalaysia's Agricultural Sector: Growth, Production and Policy TrendsNURUL EZZAH BINTI ISMAILÎncă nu există evaluări

- Financial Year 2006 07Document46 paginiFinancial Year 2006 07Prabal SenÎncă nu există evaluări

- Pulse of Cotton 31-01-2023Document9 paginiPulse of Cotton 31-01-2023J.SathishÎncă nu există evaluări

- RMCAO Manual Batch DesignDocument2 paginiRMCAO Manual Batch DesignReno Pratama Adi SaputraÎncă nu există evaluări

- Cmo January 2017 ForecastsDocument4 paginiCmo January 2017 Forecaststania__starÎncă nu există evaluări

- A/b/ A/b/: Source: Philippine Statistics AuthorityDocument3 paginiA/b/ A/b/: Source: Philippine Statistics AuthorityJacket TralalaÎncă nu există evaluări

- Pulse of Cotton 11-02-2023Document12 paginiPulse of Cotton 11-02-2023J.SathishÎncă nu există evaluări

- Basic Things of Manufactruing PlantDocument4 paginiBasic Things of Manufactruing PlantKalpesh PatilÎncă nu există evaluări

- Design MixDocument1 paginăDesign MixrakeshÎncă nu există evaluări

- BD F118S en WW - LDocument12 paginiBD F118S en WW - LyusufÎncă nu există evaluări

- Grafik QC Hematologi 2023 BaruDocument125 paginiGrafik QC Hematologi 2023 BaruSyifa nurfitriÎncă nu există evaluări

- Cambodia Grain and Feed Annual Report 2018Document15 paginiCambodia Grain and Feed Annual Report 2018Faran MoonisÎncă nu există evaluări

- Article On Cotton & Man Made Fibres 07-08Document10 paginiArticle On Cotton & Man Made Fibres 07-08agra_vikashÎncă nu există evaluări

- Final Cut-Off Details For Allotment of 5000 Sites in Nadaprabhu Kempegowda Layout Dimension and Category WiseDocument1 paginăFinal Cut-Off Details For Allotment of 5000 Sites in Nadaprabhu Kempegowda Layout Dimension and Category WiseAmitKumarÎncă nu există evaluări

- Consumption of Fresh Acetone in Dye Lab Jan'2008: Check SheetDocument34 paginiConsumption of Fresh Acetone in Dye Lab Jan'2008: Check SheetMurtaza sherwaniÎncă nu există evaluări

- Textile Industry - Overview: Ministry of Textile Fact SheetDocument7 paginiTextile Industry - Overview: Ministry of Textile Fact SheetSylvia GraceÎncă nu există evaluări

- Sirin SereethoranakulDocument35 paginiSirin SereethoranakulGanesh BonganeÎncă nu există evaluări

- Textiles Gran Fe TextileDocument17 paginiTextiles Gran Fe TextileCanche Adriano DiazÎncă nu există evaluări

- Cotton Profile May 2019Document10 paginiCotton Profile May 2019Jahanvi KhannaÎncă nu există evaluări

- HNF MISReport081Document28 paginiHNF MISReport081city1212Încă nu există evaluări

- Tugas Mining Economic (NPV)Document5 paginiTugas Mining Economic (NPV)Sandhi FardiansyahÎncă nu există evaluări

- Bangladesh Bank indicators reportDocument1 paginăBangladesh Bank indicators reportschizitÎncă nu există evaluări

- Polysymetrics: The Art of Making Geometric PatternsDe la EverandPolysymetrics: The Art of Making Geometric PatternsEvaluare: 3.5 din 5 stele3.5/5 (3)

- British Commercial Computer Digest: Pergamon Computer Data SeriesDe la EverandBritish Commercial Computer Digest: Pergamon Computer Data SeriesÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

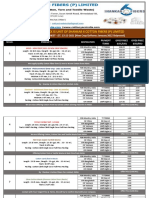

- PT Global Spintex Is Unit of Shankar 6 Cotton Fibers (P) LimitedDocument3 paginiPT Global Spintex Is Unit of Shankar 6 Cotton Fibers (P) LimitedcottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 23 12 2021 Yarn Export Price OfferDocument1 pagină23 12 2021 Yarn Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- 12-11-2021-Todays Export Price OfferDocument3 pagini12-11-2021-Todays Export Price OffercottontradeÎncă nu există evaluări

- Brochure LEET 2013 14 FinalDocument114 paginiBrochure LEET 2013 14 FinalAnsh SharmaÎncă nu există evaluări

- Easy Egg Custard Pie Recipedrjgq PDFDocument3 paginiEasy Egg Custard Pie Recipedrjgq PDFMonahanStokholm25Încă nu există evaluări

- Global Regulations Affecting Copper in 2021 2023 1666654228Document99 paginiGlobal Regulations Affecting Copper in 2021 2023 1666654228Leonardo Guerini MazettiÎncă nu există evaluări

- 이공도를 위한 물리화학Document543 pagini이공도를 위한 물리화학이사제 (사제)Încă nu există evaluări

- Manuskrip Jurnal IndahDocument6 paginiManuskrip Jurnal IndahindahÎncă nu există evaluări

- Small Animal Dermatology Self Assessment ColouDocument243 paginiSmall Animal Dermatology Self Assessment ColouRatna Mani Upadhyay100% (3)

- The Sacred Groves and Their Significance in ConserDocument16 paginiThe Sacred Groves and Their Significance in ConserMalu Kishore100% (1)

- Chemical Safety HandbookDocument39 paginiChemical Safety HandbookZach AdamsonÎncă nu există evaluări

- 3 Gorges DamDocument2 pagini3 Gorges DamAdeel AsgharÎncă nu există evaluări

- Edc 1 PDFDocument18 paginiEdc 1 PDFchetan kapoorÎncă nu există evaluări

- Cell Cycle (Scitable)Document2 paginiCell Cycle (Scitable)LibrofiloÎncă nu există evaluări

- Bed Making: Occupied Bed Unoccupied BedDocument16 paginiBed Making: Occupied Bed Unoccupied BedHakdog ShermolangÎncă nu există evaluări

- Key Benefits: Benefit TableDocument12 paginiKey Benefits: Benefit TableRaaj ChoudhuryÎncă nu există evaluări

- Reg. No. IV SEMESTER B.TECH. (MECHATRONICS ENGINEERING) END SEMESTER EXAMINATIONS, JUNE 2018 DESIGN OF MACHINE LEMENTS MTE 2202Document3 paginiReg. No. IV SEMESTER B.TECH. (MECHATRONICS ENGINEERING) END SEMESTER EXAMINATIONS, JUNE 2018 DESIGN OF MACHINE LEMENTS MTE 2202MeghaÎncă nu există evaluări

- U.K. Shakyawar - ERDMPDocument32 paginiU.K. Shakyawar - ERDMPPanchdev KumarÎncă nu există evaluări

- MEC420 - 3 - Kinetics of Particles - Work - ImpluseDocument69 paginiMEC420 - 3 - Kinetics of Particles - Work - Implusesimon georgeÎncă nu există evaluări

- F3 - Day 20Document6 paginiF3 - Day 20Duy LêÎncă nu există evaluări

- My ScramjetDocument13 paginiMy ScramjetHimanshu GuptaÎncă nu există evaluări

- Leopold ManeuverDocument1 paginăLeopold ManeuverLego BrickheadzÎncă nu există evaluări

- Predicaments & DefinitionDocument32 paginiPredicaments & DefinitionGisselle PauloÎncă nu există evaluări

- 11-6A Championship Full Meet ProgramDocument19 pagini11-6A Championship Full Meet ProgramJason JeffriesÎncă nu există evaluări

- Green Computing - A SurveyDocument7 paginiGreen Computing - A SurveyseventhsensegroupÎncă nu există evaluări

- Name: Parmar Pratik K. MSC Sem-1 Roll No.-7 Guided By-Dr. N. Y. BhattDocument29 paginiName: Parmar Pratik K. MSC Sem-1 Roll No.-7 Guided By-Dr. N. Y. BhattPratik ParmarÎncă nu există evaluări

- FMC Product OverviewDocument32 paginiFMC Product OverviewGustavoSilvinoSilvinoÎncă nu există evaluări

- Kultura at Tradisyon NG Mga HAPONDocument1 paginăKultura at Tradisyon NG Mga HAPONJullianMarkÎncă nu există evaluări

- 13 HD 120Document4 pagini13 HD 120văn hiếu phanÎncă nu există evaluări

- William Smith: English None None NoneDocument2 paginiWilliam Smith: English None None NoneArthur NunesÎncă nu există evaluări

- Seleccion & Brochure Bomba Griswold BoosterDocument19 paginiSeleccion & Brochure Bomba Griswold BoosterJonathan Mario Bolivar AldanaÎncă nu există evaluări

- Problem No. 3,6,8,11,16, Lecture 2b-MedicineDocument39 paginiProblem No. 3,6,8,11,16, Lecture 2b-MedicineMelwyn FranciscoÎncă nu există evaluări

- Uhf Ask Receiver IC U3741BM: FeaturesDocument33 paginiUhf Ask Receiver IC U3741BM: FeaturesBegu CataÎncă nu există evaluări