S-ar putea să vă placă și

- The Constitutional Case for Religious Exemptions from Federal Vaccine MandatesDe la EverandThe Constitutional Case for Religious Exemptions from Federal Vaccine MandatesÎncă nu există evaluări

- U.S. v. Sun Myung Moon 718 F.2d 1210 (1983)De la EverandU.S. v. Sun Myung Moon 718 F.2d 1210 (1983)Încă nu există evaluări

- NY Appellate Court Ruling, Maisto, Et. Al. v. State of New YorkDocument52 paginiNY Appellate Court Ruling, Maisto, Et. Al. v. State of New YorkDaily FreemanÎncă nu există evaluări

- Flast v. Cohen, 392 U.S. 83 (1968)Document37 paginiFlast v. Cohen, 392 U.S. 83 (1968)Scribd Government DocsÎncă nu există evaluări

- Opinion - Gary B Vs Richard Snyder 16-13292Document40 paginiOpinion - Gary B Vs Richard Snyder 16-13292Detroit Free Press100% (1)

- April 26Document7 paginiApril 26Jon CampbellÎncă nu există evaluări

- LLC 2 PDFDocument4 paginiLLC 2 PDFChris BraggÎncă nu există evaluări

- Supreme Court Rules Proviso On Mask Mandates in Schools Is ConstitutionalDocument6 paginiSupreme Court Rules Proviso On Mask Mandates in Schools Is ConstitutionalABC15 NewsÎncă nu există evaluări

- Pork Lawsuit HeardDocument8 paginiPork Lawsuit HeardJimmyVielkindÎncă nu există evaluări

- Memo in Support of PI in Sauer V NixonDocument25 paginiMemo in Support of PI in Sauer V NixonDerek MullerÎncă nu există evaluări

- Read The State's Motion For A StayDocument18 paginiRead The State's Motion For A StayUSA TODAY NetworkÎncă nu există evaluări

- Askew v. Hargrave, 401 U.S. 476 (1971)Document3 paginiAskew v. Hargrave, 401 U.S. 476 (1971)Scribd Government DocsÎncă nu există evaluări

- Schulz DecisionDocument7 paginiSchulz DecisionCasey SeilerÎncă nu există evaluări

- Court DecisionDocument22 paginiCourt DecisionJessie BalmertÎncă nu există evaluări

- United States Court of Appeals, Second Circuit.: No. 248, Docket 80-6050Document6 paginiUnited States Court of Appeals, Second Circuit.: No. 248, Docket 80-6050Scribd Government DocsÎncă nu există evaluări

- Americans United For Separation of Church and State v. Newell J. Paire, As Commissioner of Education of The State of New Hampshire, 475 F.2d 462, 1st Cir. (1973)Document7 paginiAmericans United For Separation of Church and State v. Newell J. Paire, As Commissioner of Education of The State of New Hampshire, 475 F.2d 462, 1st Cir. (1973)Scribd Government DocsÎncă nu există evaluări

- Not PrecedentialDocument7 paginiNot PrecedentialScribd Government DocsÎncă nu există evaluări

- State of New Jersey, Dept. of Education v. Shirley Hufstedler, Secretary of Education, Etc., 724 F.2d 34, 3rd Cir. (1984)Document4 paginiState of New Jersey, Dept. of Education v. Shirley Hufstedler, Secretary of Education, Etc., 724 F.2d 34, 3rd Cir. (1984)Scribd Government DocsÎncă nu există evaluări

- THE Supreme Court OF Washington: - FiledDocument46 paginiTHE Supreme Court OF Washington: - FiledAlfred DanezÎncă nu există evaluări

- United States Court of Appeals, Second Circuit.: Nos. 132, 253, Dockets 84-7308, 84-7382Document16 paginiUnited States Court of Appeals, Second Circuit.: Nos. 132, 253, Dockets 84-7308, 84-7382Scribd Government DocsÎncă nu există evaluări

- United States Court of Appeals, Third CircuitDocument35 paginiUnited States Court of Appeals, Third CircuitScribd Government DocsÎncă nu există evaluări

- 22A444Document42 pagini22A444Chris GeidnerÎncă nu există evaluări

- Carson V MakinDocument9 paginiCarson V MakinAnonymous HiNeTxLMÎncă nu există evaluări

- Reply Memorandum of Law in Further Support of Motion To DismissDocument12 paginiReply Memorandum of Law in Further Support of Motion To DismissBasseemÎncă nu există evaluări

- 3.17.2022 Mask Mandate Ruling by The Austin-Based 3rd Court of AppealsDocument20 pagini3.17.2022 Mask Mandate Ruling by The Austin-Based 3rd Court of AppealsCBS Austin WebteamÎncă nu există evaluări

- Eulitt v. ME Dept. of Edu, 386 F.3d 344, 1st Cir. (2004)Document16 paginiEulitt v. ME Dept. of Edu, 386 F.3d 344, 1st Cir. (2004)Scribd Government DocsÎncă nu există evaluări

- 15 - Flast v. Cohen, 392 US 83Document31 pagini15 - Flast v. Cohen, 392 US 83Jester ConwayÎncă nu există evaluări

- Judge's Decision On Brown County Taxpayers Association vs. BidenDocument5 paginiJudge's Decision On Brown County Taxpayers Association vs. BidenScott Hurley WLUK-TVÎncă nu există evaluări

- McCall V Scott Stetson Law ReviewDocument21 paginiMcCall V Scott Stetson Law ReviewGeorge-Maria Hector RosalesÎncă nu există evaluări

- United States of America, and South End Education Committee, Intervening v. Board of Education of Waterbury, Connecticut, 605 F.2d 573, 2d Cir. (1979)Document7 paginiUnited States of America, and South End Education Committee, Intervening v. Board of Education of Waterbury, Connecticut, 605 F.2d 573, 2d Cir. (1979)Scribd Government DocsÎncă nu există evaluări

- School Committee of The Town of Rockland v. Massachusetts Department of Education, 753 F.2d 169, 1st Cir. (1985)Document8 paginiSchool Committee of The Town of Rockland v. Massachusetts Department of Education, 753 F.2d 169, 1st Cir. (1985)Scribd Government DocsÎncă nu există evaluări

- Kadrmas v. Dickinson Public Schools, 487 U.S. 450 (1988)Document19 paginiKadrmas v. Dickinson Public Schools, 487 U.S. 450 (1988)Scribd Government DocsÎncă nu există evaluări

- United States Court of Appeals: For The First CircuitDocument23 paginiUnited States Court of Appeals: For The First CircuitScribd Government DocsÎncă nu există evaluări

- United States Court of Appeals, Tenth CircuitDocument6 paginiUnited States Court of Appeals, Tenth CircuitScribd Government DocsÎncă nu există evaluări

- Ny Tenant Scot Us RLG 081221Document5 paginiNy Tenant Scot Us RLG 081221Foreclosure FraudÎncă nu există evaluări

- Mueller v. Allen, 463 U.S. 388 (1983)Document25 paginiMueller v. Allen, 463 U.S. 388 (1983)Scribd Government DocsÎncă nu există evaluări

- APSCU v. DuncanDocument55 paginiAPSCU v. DuncanBarmak NassirianÎncă nu există evaluări

- FLASTDocument11 paginiFLASTAngelo AlmeroÎncă nu există evaluări

- Bennett v. New Jersey, 470 U.S. 632 (1985)Document20 paginiBennett v. New Jersey, 470 U.S. 632 (1985)Scribd Government DocsÎncă nu există evaluări

- Kate Frazier v. Fairhaven School Committee, 276 F.3d 52, 1st Cir. (2002)Document19 paginiKate Frazier v. Fairhaven School Committee, 276 F.3d 52, 1st Cir. (2002)Scribd Government DocsÎncă nu există evaluări

- CREW V. U.S. Department of Education: Regarding Outside Email Addresses: 5/30/2008 - Reply To Opposition To MotionDocument9 paginiCREW V. U.S. Department of Education: Regarding Outside Email Addresses: 5/30/2008 - Reply To Opposition To MotionCREWÎncă nu există evaluări

- Elsa Gulino, Mayling Ralph and Peter Wilds, on Behalf of Themselves and All Others Similarly Situated, Nia Greene v. New York State Education Department, Defendant-Cross-Defendant-Appellee, Board of Education of the New York City School District of the City of New York, Defendant-Cross-Claimant-Appellee. Docket No. 03-9062-Cv, 460 F.3d 361, 2d Cir. (2006)Document35 paginiElsa Gulino, Mayling Ralph and Peter Wilds, on Behalf of Themselves and All Others Similarly Situated, Nia Greene v. New York State Education Department, Defendant-Cross-Defendant-Appellee, Board of Education of the New York City School District of the City of New York, Defendant-Cross-Claimant-Appellee. Docket No. 03-9062-Cv, 460 F.3d 361, 2d Cir. (2006)Scribd Government DocsÎncă nu există evaluări

- SEDC DecisionDocument6 paginiSEDC DecisionWendy LiberatoreÎncă nu există evaluări

- Ray Crocker Susan Crocker, as Legal Guardians and Next Friends of Michael Crocker v. Tennessee Secondary School Athletic Association, (88-6063) Charles Smith, Commissioner of the Tennessee Department of Education Metro Nashville-Davidson County, Tennessee, (88-6185), 873 F.2d 933, 2d Cir. (1989)Document7 paginiRay Crocker Susan Crocker, as Legal Guardians and Next Friends of Michael Crocker v. Tennessee Secondary School Athletic Association, (88-6063) Charles Smith, Commissioner of the Tennessee Department of Education Metro Nashville-Davidson County, Tennessee, (88-6185), 873 F.2d 933, 2d Cir. (1989)Scribd Government DocsÎncă nu există evaluări

- U.S. Supreme Court Upholds Minnesota Tax Deduction for Private School ExpensesDocument9 paginiU.S. Supreme Court Upholds Minnesota Tax Deduction for Private School ExpensesMWinbee VisitacionÎncă nu există evaluări

- United States Court of Appeals, Third Circuit. Submitted Under Third Circuit LAR 34.1 (A)Document6 paginiUnited States Court of Appeals, Third Circuit. Submitted Under Third Circuit LAR 34.1 (A)Scribd Government DocsÎncă nu există evaluări

- In The Boone Circuit Court Boone County, Kentucky 21-CI-00161Document15 paginiIn The Boone Circuit Court Boone County, Kentucky 21-CI-00161ChrisÎncă nu există evaluări

- United States Court of Appeals, Eleventh CircuitDocument14 paginiUnited States Court of Appeals, Eleventh CircuitScribd Government DocsÎncă nu există evaluări

- State of New York v. Richard Riley, Secretary of The United States Department of Education, 53 F.3d 520, 2d Cir. (1995)Document5 paginiState of New York v. Richard Riley, Secretary of The United States Department of Education, 53 F.3d 520, 2d Cir. (1995)Scribd Government DocsÎncă nu există evaluări

- United States Court of Appeals, Second CircuitDocument10 paginiUnited States Court of Appeals, Second CircuitScribd Government DocsÎncă nu există evaluări

- State of Wyoming v. Lamar Alexander, Secretary of Education, United States Department of Education, 971 F.2d 531, 10th Cir. (1992)Document19 paginiState of Wyoming v. Lamar Alexander, Secretary of Education, United States Department of Education, 971 F.2d 531, 10th Cir. (1992)Scribd Government DocsÎncă nu există evaluări

- Tuition DecisionDocument15 paginiTuition DecisionHayden SparksÎncă nu există evaluări

- Coalition of New York State Career Schools, Inc. v. Richard W. Riley, Secretary of Education, in His Official Capacity, 129 F.3d 276, 2d Cir. (1997)Document8 paginiCoalition of New York State Career Schools, Inc. v. Richard W. Riley, Secretary of Education, in His Official Capacity, 129 F.3d 276, 2d Cir. (1997)Scribd Government DocsÎncă nu există evaluări

- United States Court of Appeals, Second Circuit.: No. 190, Docket 89-7382Document8 paginiUnited States Court of Appeals, Second Circuit.: No. 190, Docket 89-7382Scribd Government DocsÎncă nu există evaluări

- Third RulingDocument13 paginiThird RulingThe Washington PostÎncă nu există evaluări

- Opinion - Circuit Court AffirmedDocument8 paginiOpinion - Circuit Court Affirmedcarrie provinsalÎncă nu există evaluări

- Doe V Peyser Memo and Order On Defendants' Motion To DismissDocument22 paginiDoe V Peyser Memo and Order On Defendants' Motion To DismissGintautas DumciusÎncă nu există evaluări

- Avoiding Workplace Discrimination: A Guide for Employers and EmployeesDe la EverandAvoiding Workplace Discrimination: A Guide for Employers and EmployeesÎncă nu există evaluări

- How to Get Rid of Your Unwanted Debt: A Litigation Attorney Representing Homeowners, Credit Card Holders & OthersDe la EverandHow to Get Rid of Your Unwanted Debt: A Litigation Attorney Representing Homeowners, Credit Card Holders & OthersEvaluare: 3 din 5 stele3/5 (1)

- 2017 08 18 Constitution OrderDocument27 pagini2017 08 18 Constitution OrderjspectorÎncă nu există evaluări

- Joseph Ruggiero Employment AgreementDocument6 paginiJoseph Ruggiero Employment AgreementjspectorÎncă nu există evaluări

- IG LetterDocument3 paginiIG Letterjspector100% (1)

- Cornell ComplaintDocument41 paginiCornell Complaintjspector100% (1)

- Pennies For Charity 2018Document12 paginiPennies For Charity 2018ZacharyEJWilliamsÎncă nu există evaluări

- NYSCrimeReport2016 PrelimDocument14 paginiNYSCrimeReport2016 PrelimjspectorÎncă nu există evaluări

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocument8 paginiFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorÎncă nu există evaluări

- Federal Budget Fiscal Year 2017 Web VersionDocument36 paginiFederal Budget Fiscal Year 2017 Web VersionjspectorÎncă nu există evaluări

- State Health CoverageDocument26 paginiState Health CoveragejspectorÎncă nu există evaluări

- Hiffa Settlement Agreement ExecutedDocument5 paginiHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- Inflation AllowablegrowthfactorsDocument1 paginăInflation AllowablegrowthfactorsjspectorÎncă nu există evaluări

- Abo 2017 Annual ReportDocument65 paginiAbo 2017 Annual ReportrkarlinÎncă nu există evaluări

- SNY0517 Crosstabs 052417Document4 paginiSNY0517 Crosstabs 052417Nick ReismanÎncă nu există evaluări

- Teacher Shortage Report 05232017 PDFDocument16 paginiTeacher Shortage Report 05232017 PDFjspectorÎncă nu există evaluări

- Class of 2022Document1 paginăClass of 2022jspectorÎncă nu există evaluări

- Opiods 2017-04-20-By Numbers Brief No8Document17 paginiOpiods 2017-04-20-By Numbers Brief No8rkarlinÎncă nu există evaluări

- Siena Poll March 27, 2017Document7 paginiSiena Poll March 27, 2017jspectorÎncă nu există evaluări

- p12 Budget Testimony 2-14-17Document31 paginip12 Budget Testimony 2-14-17jspectorÎncă nu există evaluări

- Youth Cigarette and E-Cigs UseDocument1 paginăYouth Cigarette and E-Cigs UsejspectorÎncă nu există evaluări

- Oag Sed Letter Ice 2-27-17Document3 paginiOag Sed Letter Ice 2-27-17BethanyÎncă nu există evaluări

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocument55 pagini16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorÎncă nu există evaluări

- 2017 School Bfast Report Online Version 3-7-17 0Document29 pagini2017 School Bfast Report Online Version 3-7-17 0jspectorÎncă nu există evaluări

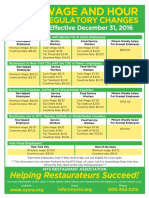

- Wage and Hour Regulatory Changes 2016Document2 paginiWage and Hour Regulatory Changes 2016jspectorÎncă nu există evaluări

- Schneiderman Voter Fraud Letter 022217Document2 paginiSchneiderman Voter Fraud Letter 022217Matthew HamiltonÎncă nu există evaluări

- Darweesh Cities AmicusDocument32 paginiDarweesh Cities AmicusjspectorÎncă nu există evaluări

- Review of Executive Budget 2017Document102 paginiReview of Executive Budget 2017Nick ReismanÎncă nu există evaluări

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Document4 paginiActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorÎncă nu există evaluări

- 2016 Local Sales Tax CollectionsDocument4 pagini2016 Local Sales Tax CollectionsjspectorÎncă nu există evaluări

- Pub Auth Num 2017Document54 paginiPub Auth Num 2017jspectorÎncă nu există evaluări

- Voting Report CardDocument1 paginăVoting Report CardjspectorÎncă nu există evaluări

- PFRS 16 Lease Accounting GuideDocument2 paginiPFRS 16 Lease Accounting GuideQueen ValleÎncă nu există evaluări

- Company Report - Venus Remedies LTDDocument36 paginiCompany Report - Venus Remedies LTDseema1707Încă nu există evaluări

- Saral Gyan Stocks Past Performance 050113Document13 paginiSaral Gyan Stocks Past Performance 050113saptarshidas21Încă nu există evaluări

- Leadership in Change Management Group WorkDocument11 paginiLeadership in Change Management Group WorkRakinduÎncă nu există evaluări

- Financial Analysis - Marketing - Circa Lynnwood 100% (2023 - 10 - 31 10 - 38 - 56 UTC)Document13 paginiFinancial Analysis - Marketing - Circa Lynnwood 100% (2023 - 10 - 31 10 - 38 - 56 UTC)SiyabongaÎncă nu există evaluări

- Upkar Dhawan Fy 2016-17Document3 paginiUpkar Dhawan Fy 2016-17amit22505Încă nu există evaluări

- Formats Pensioners NHIS 2014Document4 paginiFormats Pensioners NHIS 2014Raj RudrapaaÎncă nu există evaluări

- Reauthorization of The National Flood Insurance ProgramDocument137 paginiReauthorization of The National Flood Insurance ProgramScribd Government DocsÎncă nu există evaluări

- MGMT E-2000 Fall 2014 SyllabusDocument13 paginiMGMT E-2000 Fall 2014 Syllabusm1k0eÎncă nu există evaluări

- The Journal of Performance Measurement Table of ContentsDocument12 paginiThe Journal of Performance Measurement Table of ContentsEttore TruccoÎncă nu există evaluări

- Syllabus - Wills and SuccessionDocument14 paginiSyllabus - Wills and SuccessionJImlan Sahipa IsmaelÎncă nu există evaluări

- Cooperative ManualDocument35 paginiCooperative ManualPratik MogheÎncă nu există evaluări

- Artist Village Detroit Revitalizes Neighborhood Through Creative EnterpriseDocument6 paginiArtist Village Detroit Revitalizes Neighborhood Through Creative EnterpriseVaishali JoshiÎncă nu există evaluări

- INVESTMENT MANAGEMENT-lakatan and CondoDocument22 paginiINVESTMENT MANAGEMENT-lakatan and CondoJewelyn C. Espares-CioconÎncă nu există evaluări

- Nse & BseDocument120 paginiNse & BseArjun PatelÎncă nu există evaluări

- Esteriana Haskasa - General ResumeDocument3 paginiEsteriana Haskasa - General ResumeEster HaskaÎncă nu există evaluări

- s6 Econ (Public Finance and Fiscal Policy)Document50 paginis6 Econ (Public Finance and Fiscal Policy)juniormugarura5Încă nu există evaluări

- Textron Inc. v. Commissioner of IRS, 336 F.3d 26, 1st Cir. (2003)Document11 paginiTextron Inc. v. Commissioner of IRS, 336 F.3d 26, 1st Cir. (2003)Scribd Government DocsÎncă nu există evaluări

- Travis Kalanick and UberDocument3 paginiTravis Kalanick and UberHarsh GadhiyaÎncă nu există evaluări

- Breaking The Time Barrier PDFDocument70 paginiBreaking The Time Barrier PDFCalypso LearnerÎncă nu există evaluări

- Overview of Working Capital Management and Cash ManagementDocument48 paginiOverview of Working Capital Management and Cash ManagementChrisÎncă nu există evaluări

- Notes # 2 - Fundamentals of Real Estate Management PDFDocument3 paginiNotes # 2 - Fundamentals of Real Estate Management PDFGessel Xan Lopez100% (2)

- P4 Taxation New Suggested CA Inter May 18Document27 paginiP4 Taxation New Suggested CA Inter May 18Durgadevi BaskaranÎncă nu există evaluări

- Joseph Showry MBADocument3 paginiJoseph Showry MBAjosephshowryÎncă nu există evaluări

- Acct TutorDocument22 paginiAcct TutorKthln Mntlla100% (1)

- IPP Report PakistanDocument296 paginiIPP Report PakistanALI100% (1)

- CBSE Class 12 Economics Sample Paper (For 2014)Document19 paginiCBSE Class 12 Economics Sample Paper (For 2014)cbsesamplepaperÎncă nu există evaluări

- T3-Sample Answers-Consideration PDFDocument10 paginiT3-Sample Answers-Consideration PDF--bolabolaÎncă nu există evaluări

- Global Dis Trip Arks ProspectusDocument250 paginiGlobal Dis Trip Arks ProspectusSandeepan ChaudhuriÎncă nu există evaluări

- Fin 580 WK 2 Paper - Team CDocument5 paginiFin 580 WK 2 Paper - Team Cchad salcidoÎncă nu există evaluări