S-ar putea să vă placă și

- 29-30 Dec 7th Thirumal State LVL TMTDocument2 pagini29-30 Dec 7th Thirumal State LVL TMTkalyanÎncă nu există evaluări

- 50 Fighting Games PDFDocument376 pagini50 Fighting Games PDFkalyan100% (3)

- Bill Wall - Off The Wall Chess Trivia (2001) PDFDocument287 paginiBill Wall - Off The Wall Chess Trivia (2001) PDFGiovanni De GirolamoÎncă nu există evaluări

- 2018 Mar Chronicle AICFDocument52 pagini2018 Mar Chronicle AICFkalyanÎncă nu există evaluări

- Yajur Vedi Avani Avittam Ritual GuideDocument20 paginiYajur Vedi Avani Avittam Ritual GuideSrikumar Krishna IyerÎncă nu există evaluări

- 2018 July Chronicle AICFDocument27 pagini2018 July Chronicle AICFkalyanÎncă nu există evaluări

- Chernev, Irving - Logical Chess Move by MoveDocument256 paginiChernev, Irving - Logical Chess Move by Movegerardohpm88% (8)

- #1 e Scan ProtectedDocument2 pagini#1 e Scan ProtectedkalyanÎncă nu există evaluări

- 2018 Feb Chronicle AICFDocument27 pagini2018 Feb Chronicle AICFkalyanÎncă nu există evaluări

- 2018 Apr Chronicle AICFDocument27 pagini2018 Apr Chronicle AICFkalyanÎncă nu există evaluări

- Major Field Test in PsychologyDocument3 paginiMajor Field Test in PsychologyMadalinaElenaÎncă nu există evaluări

- Technical SpecificationDocument18 paginiTechnical SpecificationkalyanÎncă nu există evaluări

- 2018 May Chronicle AICFDocument27 pagini2018 May Chronicle AICFkalyanÎncă nu există evaluări

- M.Sc. Degree Examination - JUNE 2013Document2 paginiM.Sc. Degree Examination - JUNE 2013kalyanÎncă nu există evaluări

- 2018 June Chronicle AICFDocument27 pagini2018 June Chronicle AICFkalyanÎncă nu există evaluări

- Global WarmingDocument25 paginiGlobal WarmingManish Kumar sharma64% (11)

- GetSmartBrainHealth Handout2Document4 paginiGetSmartBrainHealth Handout2dandoldenyusÎncă nu există evaluări

- DR Analysis On Chess PsychologyDocument4 paginiDR Analysis On Chess Psychologykalyan100% (1)

- Vishy Anand BiographyDocument2 paginiVishy Anand BiographykalyanÎncă nu există evaluări

- Chess Team Tournament Rules and RegulationsDocument1 paginăChess Team Tournament Rules and RegulationskalyanÎncă nu există evaluări

- Mr Computers Budget PC Parts QuotationDocument1 paginăMr Computers Budget PC Parts QuotationkalyanÎncă nu există evaluări

- Chess exam questions on laws, notation, pairings and penaltiesDocument4 paginiChess exam questions on laws, notation, pairings and penaltieskalyanÎncă nu există evaluări

- List of Licensed Chess Arbiters Around the WorldDocument204 paginiList of Licensed Chess Arbiters Around the WorldkalyanÎncă nu există evaluări

- Welcome To City of Lakes 3.21lakh4Document7 paginiWelcome To City of Lakes 3.21lakh4kalyanÎncă nu există evaluări

- FIDE Arbiters Magazine No 4 - February 2017Document15 paginiFIDE Arbiters Magazine No 4 - February 2017FSTIMJPÎncă nu există evaluări

- FIDE Arbiters Magazine No 5 - September 2017Document16 paginiFIDE Arbiters Magazine No 5 - September 2017kalyanÎncă nu există evaluări

- An Arbiter 'S Notebook: What Shall We Do With An Annoying Spectator?Document8 paginiAn Arbiter 'S Notebook: What Shall We Do With An Annoying Spectator?kalyanÎncă nu există evaluări

- FIDE Arbiters Magazine No 4 - February 2017Document15 paginiFIDE Arbiters Magazine No 4 - February 2017FSTIMJPÎncă nu există evaluări

- FIDE Arbiters Magazine No 2 - February 2016Document16 paginiFIDE Arbiters Magazine No 2 - February 2016Liga Muncipal De Ajedrez HuejutlaÎncă nu există evaluări

- FIDE Arbiters' Magazine Case CompilationDocument16 paginiFIDE Arbiters' Magazine Case CompilationkalyanÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5783)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- A On The Organizational System and Organizational Progress of Bangalore Milk Union LTD (BAMUL)Document74 paginiA On The Organizational System and Organizational Progress of Bangalore Milk Union LTD (BAMUL)Tilak Raj100% (5)

- Leave Rule and Service Book of College TeachersDocument69 paginiLeave Rule and Service Book of College TeachersDepartment of Education100% (1)

- How to Create and Manage an Effective Sales TeamDocument28 paginiHow to Create and Manage an Effective Sales TeamganeshkumarÎncă nu există evaluări

- Research Paper - Low Salary and ContractualizationDocument16 paginiResearch Paper - Low Salary and ContractualizationTrisha Marie PillenaÎncă nu există evaluări

- De Thi HSG Anh 9 - 2019 Chinh ThucDocument8 paginiDe Thi HSG Anh 9 - 2019 Chinh Thuctrang100% (1)

- Human Resource PlanningDocument11 paginiHuman Resource PlanningJohn Vincent Musngi100% (1)

- Live payroll process and checkpointsDocument7 paginiLive payroll process and checkpointsDhruv JainÎncă nu există evaluări

- A Project Report On "Industrial Relations in Bhel, Hyderabad"Document32 paginiA Project Report On "Industrial Relations in Bhel, Hyderabad"Salman KhanÎncă nu există evaluări

- Employee HandbookDocument16 paginiEmployee HandbookShubhojit GanguliÎncă nu există evaluări

- NBA Uniform Player Contract ExplainedDocument14 paginiNBA Uniform Player Contract ExplainedEvery ChinÎncă nu există evaluări

- Ahmad Fine Textile Mills LTDDocument83 paginiAhmad Fine Textile Mills LTDfaisalÎncă nu există evaluări

- Court rules on water utility labor disputesDocument6 paginiCourt rules on water utility labor disputesnathÎncă nu există evaluări

- Nss Report 554 31jan14Document1.069 paginiNss Report 554 31jan14Mandar Priya Phatak100% (1)

- 2019 PROBLEM EXERCISES IN INCOME TAXATION and TRAIN LAW (B)Document11 pagini2019 PROBLEM EXERCISES IN INCOME TAXATION and TRAIN LAW (B)MGVMonÎncă nu există evaluări

- 2020 PDFDocument6 pagini2020 PDFAbraham ItchonÎncă nu există evaluări

- Functions of Personnel Management Are Categorized UnderDocument8 paginiFunctions of Personnel Management Are Categorized UnderMangue AlaizaÎncă nu există evaluări

- EWAC Incentive AppendixDocument2 paginiEWAC Incentive AppendixNapoleon DasÎncă nu există evaluări

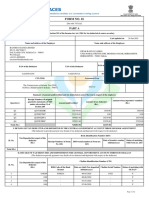

- Form No. 16: Part ADocument7 paginiForm No. 16: Part AMirza Aftab BaigÎncă nu există evaluări

- Sales Associate Offer LetterDocument3 paginiSales Associate Offer LetterRishabh PathaniaÎncă nu există evaluări

- 4 Completing The Accounting Cycle PartDocument1 pagină4 Completing The Accounting Cycle PartTalionÎncă nu există evaluări

- Erectors vs. NLRCDocument2 paginiErectors vs. NLRCAmethyst Vivo Tanio100% (3)

- Pay Slip TemplateDocument1 paginăPay Slip TemplateJohn Rheymar TamayoÎncă nu există evaluări

- Danish Embassy Visa Officer Jobs in New DelhiDocument3 paginiDanish Embassy Visa Officer Jobs in New DelhiYash SolankiÎncă nu există evaluări

- AFSCMENegotiatedAgreementJune-8-202 Charles CountyDocument38 paginiAFSCMENegotiatedAgreementJune-8-202 Charles CountyDavid M. Higgins IIÎncă nu există evaluări

- Management AnalysisDocument23 paginiManagement AnalysisMiracle Vertera100% (1)

- Tangazo La Kazi 6 Januari 2014Document45 paginiTangazo La Kazi 6 Januari 2014Aaron DelaneyÎncă nu există evaluări

- (Liability of Local Recruitment Agency and Foreign Employer - Solidary Liability) Princess Talent Center Prod. Inc v. Desiree Masagca PDFDocument3 pagini(Liability of Local Recruitment Agency and Foreign Employer - Solidary Liability) Princess Talent Center Prod. Inc v. Desiree Masagca PDFRuth Angelica TeoxonÎncă nu există evaluări

- Manage Direct Labor CostsDocument26 paginiManage Direct Labor Costshae1234Încă nu există evaluări

- Sameer Overseas Placement Agency Vs CabilesDocument10 paginiSameer Overseas Placement Agency Vs CabilesKastin SantosÎncă nu există evaluări

- #6 C.M. Hoskins v. CirDocument2 pagini#6 C.M. Hoskins v. CirKORINA NGALOYÎncă nu există evaluări