S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Faisal StarterDocument9 paginiFaisal StarterHaniya Princexx KousarÎncă nu există evaluări

- VTROB10Document4 paginiVTROB10Haniya Princexx KousarÎncă nu există evaluări

- EcgDocument4 paginiEcgHaniya Princexx KousarÎncă nu există evaluări

- Zubair DocumentationDocument10 paginiZubair DocumentationHaniya Princexx KousarÎncă nu există evaluări

- Summer Training Proect On Comparison of Home Loan Scheme of Different BanksDocument63 paginiSummer Training Proect On Comparison of Home Loan Scheme of Different Banksakshparmar2510Încă nu există evaluări

- Major Project On 2 WheelerDocument69 paginiMajor Project On 2 WheelerManvendra Kumar73% (11)

- Technical ReportDocument16 paginiTechnical ReportHaniya Princexx KousarÎncă nu există evaluări

- Tech PB For StudentsDocument4 paginiTech PB For StudentsHaniya Princexx KousarÎncă nu există evaluări

- Major Project On 2 WheelerDocument70 paginiMajor Project On 2 WheelerHaniya Princexx KousarÎncă nu există evaluări

- Digital Object Counter Project ReportDocument6 paginiDigital Object Counter Project ReportHaniya Princexx KousarÎncă nu există evaluări

- Asset Liability Management IciciDocument71 paginiAsset Liability Management IciciHaniya Princexx Kousar0% (2)

- Line Following Robot: A Mini Project Report OnDocument9 paginiLine Following Robot: A Mini Project Report OnHaniya Princexx KousarÎncă nu există evaluări

- Lighting Bolt of RobotDocument10 paginiLighting Bolt of RobotHaniya Princexx KousarÎncă nu există evaluări

- Light Seeking Robot Project ReportDocument9 paginiLight Seeking Robot Project ReportHaniya Princexx KousarÎncă nu există evaluări

- Isro 2012 PDFDocument19 paginiIsro 2012 PDFsharada_346460992Încă nu există evaluări

- Isro 2012 PDFDocument19 paginiIsro 2012 PDFsharada_346460992Încă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- F 1099 ADocument6 paginiF 1099 AIRS100% (1)

- KFS HBL@ Work Conventional AccountsDocument6 paginiKFS HBL@ Work Conventional AccountsArslan BaigÎncă nu există evaluări

- Agent Name, License No & IRDA URN ListDocument20 paginiAgent Name, License No & IRDA URN ListHarshad BhirudÎncă nu există evaluări

- Central Bank Names of Different CountriesDocument6 paginiCentral Bank Names of Different CountrieskalasriÎncă nu există evaluări

- PDFDocument7 paginiPDFSoman MenonÎncă nu există evaluări

- Analysis of Audit Report of HindalcoDocument16 paginiAnalysis of Audit Report of HindalcoYogesh SahaniÎncă nu există evaluări

- RECONCILE BANK & CASH BOOK BALANCESDocument16 paginiRECONCILE BANK & CASH BOOK BALANCESMichael AsieduÎncă nu există evaluări

- Summer Internship Project at ICICI BankDocument81 paginiSummer Internship Project at ICICI BankNeha Vora100% (3)

- PDF DocumentDocument4 paginiPDF Documentangye08vivasÎncă nu există evaluări

- Cynthia Riley Depo 1-15-2013 HighlightedDocument110 paginiCynthia Riley Depo 1-15-2013 Highlightedmmeindl100% (1)

- A Study of Bank Audit ProcessDocument61 paginiA Study of Bank Audit ProcessSunil PawarÎncă nu există evaluări

- RMC 59-08 (Mcit) PDFDocument8 paginiRMC 59-08 (Mcit) PDFAnonymous DpHYeqzbp1Încă nu există evaluări

- Bni PT Bangun Jun22Document3 paginiBni PT Bangun Jun22Yehezkiel AdhiÎncă nu există evaluări

- Assignment Form PDFDocument2 paginiAssignment Form PDFjoitaÎncă nu există evaluări

- Executive Summary of Internet Banking Risks and OpportunitiesDocument13 paginiExecutive Summary of Internet Banking Risks and OpportunitiesJaydeep DhandhaliyaÎncă nu există evaluări

- Master Policy Bond SPGIDocument17 paginiMaster Policy Bond SPGIDARSHAN ROYGAGAÎncă nu există evaluări

- IcotermsDocument3 paginiIcotermsMiguel Estrada DíazÎncă nu există evaluări

- Study On Credit PolicyDocument12 paginiStudy On Credit PolicyVaibhav GawandeÎncă nu există evaluări

- Fannie Updates To Foreclosure Time FramesDocument3 paginiFannie Updates To Foreclosure Time FramesForeclosure FraudÎncă nu există evaluări

- App QDocument11 paginiApp Qkasi_raghav50% (2)

- Chapter 2 Solutions and ExercisesDocument15 paginiChapter 2 Solutions and ExercisesKashif IshaqÎncă nu există evaluări

- BSP Circular 1107Document7 paginiBSP Circular 1107Maya Julieta Catacutan-EstabilloÎncă nu există evaluări

- Basic Sales TrainingDocument36 paginiBasic Sales TrainingManraj Singh100% (1)

- Transaction StatementDocument10 paginiTransaction Statementsukeshsree sree33% (3)

- Successful Transactions PDFDocument1 paginăSuccessful Transactions PDFQhairin BaharudinÎncă nu există evaluări

- SYMBOL CONTRACTS ANALYSISDocument8 paginiSYMBOL CONTRACTS ANALYSISSiddharth TripathiÎncă nu există evaluări

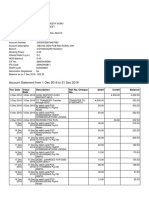

- Account Statement From 1 Dec 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 paginiAccount Statement From 1 Dec 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceENDLURI DEEPAK KUMARÎncă nu există evaluări

- Feasibility Report on Establishing Microfinance in Port MoresbyDocument164 paginiFeasibility Report on Establishing Microfinance in Port MoresbyterrancekuÎncă nu există evaluări

- Annual Report 2008Document83 paginiAnnual Report 2008Dhivya SivananthamÎncă nu există evaluări

- UCPB v. MasaganaDocument5 paginiUCPB v. MasaganajrfbalamientoÎncă nu există evaluări