S-ar putea să vă placă și

- Restrictions on franking creditsDocument1 paginăRestrictions on franking creditsoddsey0713Încă nu există evaluări

- 2-3 Capital AllowancesDocument1 pagină2-3 Capital Allowancesoddsey0713Încă nu există evaluări

- 1-8 GST - GST Payable or ITC AvalDocument2 pagini1-8 GST - GST Payable or ITC Avaloddsey0713Încă nu există evaluări

- 3-3 Div 7A Deemed Divs - VLDocument1 pagină3-3 Div 7A Deemed Divs - VLoddsey0713Încă nu există evaluări

- 4-3 Part IVA General AntiAvoidanceDocument1 pagină4-3 Part IVA General AntiAvoidanceoddsey0713Încă nu există evaluări

- ADJUSTMENTS AT FINANCIAL PERIOD ENDDocument18 paginiADJUSTMENTS AT FINANCIAL PERIOD ENDTevabless Suoived SpotlightbabeÎncă nu există evaluări

- Module 2Document12 paginiModule 2zoyaÎncă nu există evaluări

- Equity Financing A Complete Guide - 2020 EditionDe la EverandEquity Financing A Complete Guide - 2020 EditionÎncă nu există evaluări

- TAX ADMINISTRATION GUIDEDocument4 paginiTAX ADMINISTRATION GUIDEwumel01Încă nu există evaluări

- GST On Property Transactions - 99 Page Research ReportDocument99 paginiGST On Property Transactions - 99 Page Research ReporttestnationÎncă nu există evaluări

- Capital Budgeting Decision - SBSDocument43 paginiCapital Budgeting Decision - SBSSahil SherasiyaÎncă nu există evaluări

- Tax Book 2016-17 - Version 1.0a USB PDFDocument372 paginiTax Book 2016-17 - Version 1.0a USB PDFemc2_mcv100% (1)

- Understanding Income TaxDocument43 paginiUnderstanding Income TaxMerediths KrisKringleÎncă nu există evaluări

- Income Taxes (IAS 12)Document15 paginiIncome Taxes (IAS 12)Mahir RahmanÎncă nu există evaluări

- Code of Ethics Part C Professional Accountants in Business 1 Jan 2011Document11 paginiCode of Ethics Part C Professional Accountants in Business 1 Jan 2011James De Torres CarilloÎncă nu există evaluări

- Smieliauskas 6e - Solutions Manual - Chapter 02Document14 paginiSmieliauskas 6e - Solutions Manual - Chapter 02scribdteaÎncă nu există evaluări

- Balance Sheet: For Year Ending June 30, 2008Document3 paginiBalance Sheet: For Year Ending June 30, 2008arazeqÎncă nu există evaluări

- CMA Handbook: Your Guide To Information and Requirements For CMA CertificationDocument13 paginiCMA Handbook: Your Guide To Information and Requirements For CMA CertificationBupe ChaliÎncă nu există evaluări

- CPA TestDocument22 paginiCPA Testdani13_335942Încă nu există evaluări

- TABL2751 2016-2 Tutorial Program FinalDocument25 paginiTABL2751 2016-2 Tutorial Program FinalAnna ChenÎncă nu există evaluări

- LifeInsRetirementValuation M15 AppraisalValues 181205Document46 paginiLifeInsRetirementValuation M15 AppraisalValues 181205Jeff JonesÎncă nu există evaluări

- VIVA Answers (Mock-2)Document12 paginiVIVA Answers (Mock-2)isuri abeykoon100% (1)

- When To Hire A Tax ProfessionalDocument7 paginiWhen To Hire A Tax ProfessionalMaimai Durano100% (1)

- SwotDocument3 paginiSwotShahebazÎncă nu există evaluări

- Start Your BusinessDocument8 paginiStart Your BusinessIqbal MOUSSAÎncă nu există evaluări

- Cma Final Law Hand Written Notes - 1608742860Document2 paginiCma Final Law Hand Written Notes - 1608742860Dharshini AravamudhanÎncă nu există evaluări

- Ipcc Tax Practice Manual PDFDocument651 paginiIpcc Tax Practice Manual PDFshakshi gupta100% (1)

- Accounting Dissertations - IfRSDocument30 paginiAccounting Dissertations - IfRSgappu002Încă nu există evaluări

- Benifit Pension ObligationDocument20 paginiBenifit Pension ObligationTouseefÎncă nu există evaluări

- Assignment 2: Tracy Van Rensburg STUDENT NUMBER 59548525Document8 paginiAssignment 2: Tracy Van Rensburg STUDENT NUMBER 59548525Chris NdlovuÎncă nu există evaluări

- Taxation (Bs211)Document348 paginiTaxation (Bs211)RewardMaturureÎncă nu există evaluări

- 51 List of CA Final Law SectionsDocument35 pagini51 List of CA Final Law SectionsAishwarya TiwariÎncă nu există evaluări

- 401K PlannerDocument3 pagini401K Plannertf2025Încă nu există evaluări

- Fin701 Module3Document22 paginiFin701 Module3Krista CataldoÎncă nu există evaluări

- AUD Notes Chapter 2Document20 paginiAUD Notes Chapter 2janell184100% (1)

- SMA QuizDocument76 paginiSMA QuizQuỳnh ChâuÎncă nu există evaluări

- Audit Practices ManualDocument354 paginiAudit Practices ManualRaif QelaÎncă nu există evaluări

- MBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 3Document25 paginiMBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 3Jesse Rielle CarasÎncă nu există evaluări

- Section A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Document24 paginiSection A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Kenny HoÎncă nu există evaluări

- SBR Study Support Guide: Plan Prepare PassDocument27 paginiSBR Study Support Guide: Plan Prepare PassNitesh RawatÎncă nu există evaluări

- F7 Technical ArticlesDocument121 paginiF7 Technical ArticlesNicquain0% (1)

- Exp Fia-Ffm NotesDocument51 paginiExp Fia-Ffm Notesati19100% (1)

- BEC Study Guide 4-19-2013Document220 paginiBEC Study Guide 4-19-2013Valerie Readhimer100% (1)

- Additional Deferred Tax Examples.2Document3 paginiAdditional Deferred Tax Examples.2milton1986100% (1)

- Aud NotesDocument75 paginiAud NotesClaire O'BrienÎncă nu există evaluări

- Auditors' responsibilities and ethicsDocument12 paginiAuditors' responsibilities and ethicsscribdtea100% (1)

- Part 3 - Understanding Financial Statements and ReportsDocument7 paginiPart 3 - Understanding Financial Statements and ReportsJeanrey AlcantaraÎncă nu există evaluări

- Acca SBR 691 698 PDFDocument8 paginiAcca SBR 691 698 PDFYudheesh P 1822082Încă nu există evaluări

- MBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 1Document23 paginiMBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 1Jesse Rielle CarasÎncă nu există evaluări

- US CMA MCQ QuestionsDocument5 paginiUS CMA MCQ QuestionsSachin Kandloor0% (1)

- What Is The Indirect MethodDocument3 paginiWhat Is The Indirect MethodHsin Wua ChiÎncă nu există evaluări

- William WongDocument3 paginiWilliam WongKashif Mehmood0% (1)

- Lsbf-Mock Answer f8Document15 paginiLsbf-Mock Answer f8emmadavisonsÎncă nu există evaluări

- 04 Working Capital Management and Corporate GovernanceDocument26 pagini04 Working Capital Management and Corporate GovernanceKrutika NandanÎncă nu există evaluări

- Income TaxDocument109 paginiIncome TaxDaksh KohliÎncă nu există evaluări

- CFA Investment Foundations - Module 1 (CFA Institute) (Z-Library)Document39 paginiCFA Investment Foundations - Module 1 (CFA Institute) (Z-Library)gmofneweraÎncă nu există evaluări

- Cma TemplateDocument25 paginiCma TemplateSavoir PenÎncă nu există evaluări

- Fringe Benefit Tax (FBT)Document35 paginiFringe Benefit Tax (FBT)SanjayÎncă nu există evaluări

- ACCT604 Week 7 Lecture SlidesDocument29 paginiACCT604 Week 7 Lecture SlidesBuddika PrasannaÎncă nu există evaluări

- CIR v. SOJ & PAGCOR: Final Withholding Tax on Fringe BenefitsDocument4 paginiCIR v. SOJ & PAGCOR: Final Withholding Tax on Fringe BenefitsIan Villafuerte100% (1)

- 1-4 Deductions FlowchartDocument2 pagini1-4 Deductions Flowchartoddsey0713Încă nu există evaluări

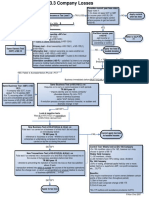

- 3-3 Company LossesDocument1 pagină3-3 Company Lossesoddsey0713Încă nu există evaluări

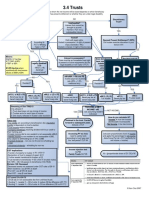

- 3-4 TrustsDocument1 pagină3-4 Trustsoddsey0713Încă nu există evaluări

- 1-3 Assessable IncomeDocument2 pagini1-3 Assessable Incomeoddsey0713Încă nu există evaluări

- 3 5 PartnershipsDocument1 pagină3 5 Partnershipsoddsey0713Încă nu există evaluări

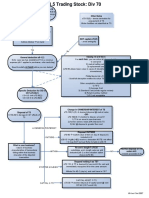

- 1-5 Trading StockDocument1 pagină1-5 Trading Stockoddsey0713Încă nu există evaluări

- 2-4,5 Capital WorksDocument1 pagină2-4,5 Capital Worksoddsey0713Încă nu există evaluări

- Creating Effective Ads PPT 4 MGMTDocument22 paginiCreating Effective Ads PPT 4 MGMToddsey0713Încă nu există evaluări

- Executing-The-Creative Design Elements and Layout Styles With ADS As ExamplesDocument47 paginiExecuting-The-Creative Design Elements and Layout Styles With ADS As Examplesoddsey0713Încă nu există evaluări

- T5 Chapters 4 and 8 Solutions To The Essential ActivitiesDocument18 paginiT5 Chapters 4 and 8 Solutions To The Essential Activitiesoddsey0713Încă nu există evaluări

- Case Summaries 1 193Document54 paginiCase Summaries 1 193oddsey0713100% (1)

- T7 Chapter 6 Solutions To The Essential ActivitiesDocument26 paginiT7 Chapter 6 Solutions To The Essential Activitiesoddsey0713Încă nu există evaluări

- T6 Chapter 5 Solutions To The Essential ActivitiesDocument12 paginiT6 Chapter 5 Solutions To The Essential Activitiesoddsey0713Încă nu există evaluări

- T8 Chapters 9 and 7 Solutions To The Essential ActivitiesDocument12 paginiT8 Chapters 9 and 7 Solutions To The Essential Activitiesoddsey0713Încă nu există evaluări

- 2006 Planning EvalDocument33 pagini2006 Planning EvalSanjay SahooÎncă nu există evaluări

- CAVB - Appointment BookingHERODEDocument2 paginiCAVB - Appointment BookingHERODEmerlinebelony16Încă nu există evaluări

- Olaf Peter Juda v. Dennis Michael Nerney, Assistant U.S. Attorney, Northern District of California Stephen R. Kotz, Assistant U.S. Attorney, Albuquerque, New Mexico John J. Kelly, U.S. Attorney, Albuquerque, New Mexico Michael Yamaguchi, U.S. Attorney, San Francisco, California Robert L. Holler, District Director, U.S. Customs Service, El Paso, Texas Leonard S. Walton, Acting Assistant Commissioner, U.S. Customs Service, Washington, D.C. Bonnie L. Gay, Foia Unit, Attorney-In-Charge, Washington, D.C. John and Jane Does 1-25 United States of America, Olaf Peter Juda v. United States Customs Service, Robert L. Holler, Joy M. Hughan, Daniel Luar, Rita Alfaro, Dolores Payan, Gina E. Fuentes, Internal Revenue Service, George Terpack, Carolyn Leonard, Timothy A. Towns, John Does, Jane Does, 149 F.3d 1190, 10th Cir. (1998)Document13 paginiOlaf Peter Juda v. Dennis Michael Nerney, Assistant U.S. Attorney, Northern District of California Stephen R. Kotz, Assistant U.S. Attorney, Albuquerque, New Mexico John J. Kelly, U.S. Attorney, Albuquerque, New Mexico Michael Yamaguchi, U.S. Attorney, San Francisco, California Robert L. Holler, District Director, U.S. Customs Service, El Paso, Texas Leonard S. Walton, Acting Assistant Commissioner, U.S. Customs Service, Washington, D.C. Bonnie L. Gay, Foia Unit, Attorney-In-Charge, Washington, D.C. John and Jane Does 1-25 United States of America, Olaf Peter Juda v. United States Customs Service, Robert L. Holler, Joy M. Hughan, Daniel Luar, Rita Alfaro, Dolores Payan, Gina E. Fuentes, Internal Revenue Service, George Terpack, Carolyn Leonard, Timothy A. Towns, John Does, Jane Does, 149 F.3d 1190, 10th Cir. (1998)Scribd Government DocsÎncă nu există evaluări

- REVUP Notes in Criminal LawDocument28 paginiREVUP Notes in Criminal LawAndrea Klein LechugaÎncă nu există evaluări

- The Case Geluz vs. Court of AppealsDocument5 paginiThe Case Geluz vs. Court of AppealsJhaquelynn DacomosÎncă nu există evaluări

- in Re Buscayno v. MIlitary CommissionDocument4 paginiin Re Buscayno v. MIlitary CommissionKim B.Încă nu există evaluări

- York County Court Schedule For March 24, 2016Document5 paginiYork County Court Schedule For March 24, 2016HafizRashidÎncă nu există evaluări

- Compliance of Citizenship Requirement For Application of CPF GrantDocument2 paginiCompliance of Citizenship Requirement For Application of CPF GrantSGExecCondosÎncă nu există evaluări

- Recase T - THBT ASEAN Should Suspend The Membership of Myanmar Until The Tatmadaw Cedes Power To The Democratically Elected GovernmentDocument3 paginiRecase T - THBT ASEAN Should Suspend The Membership of Myanmar Until The Tatmadaw Cedes Power To The Democratically Elected GovernmentTania Regina PingkanÎncă nu există evaluări

- Prepositions Exercise ExplainedDocument4 paginiPrepositions Exercise Explainediwibab 2018Încă nu există evaluări

- Indian Penal CodeDocument3 paginiIndian Penal CodeSHRUTI SINGHÎncă nu există evaluări

- ARTA MC No. 2021-09 - Issuance of The Whole of Governemnt Reengineering ManualDocument4 paginiARTA MC No. 2021-09 - Issuance of The Whole of Governemnt Reengineering ManualYnon FranciscoÎncă nu există evaluări

- Pabillar-Bsn B (Gec 112)Document2 paginiPabillar-Bsn B (Gec 112)ANDREA SHANE PABILLARÎncă nu există evaluări

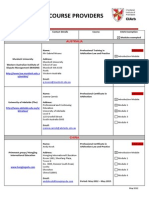

- Recognised Course Providers ListDocument13 paginiRecognised Course Providers ListSo LokÎncă nu există evaluări

- Bedding F-702 NEWDocument2 paginiBedding F-702 NEWBADIGA SHIVA GOUDÎncă nu există evaluări

- LIABILITYDocument8 paginiLIABILITYkaviyapriyaÎncă nu există evaluări

- Salient Features of RA 7610Document28 paginiSalient Features of RA 7610Pevi Mae Jalipa83% (12)

- What's Happening in Zimbabwe?: Important Elections Took Place in Zimbabwe in Southern Africa On 30 July 2018Document6 paginiWhat's Happening in Zimbabwe?: Important Elections Took Place in Zimbabwe in Southern Africa On 30 July 2018EriqÎncă nu există evaluări

- Dgt-1 Form - Per 10 - 2017Document12 paginiDgt-1 Form - Per 10 - 2017Adanbungaran PangribÎncă nu există evaluări

- M783 & Prem CF Ammo Rebate FORMDocument1 paginăM783 & Prem CF Ammo Rebate FORMdunhamssports1Încă nu există evaluări

- 74th AmendmentDocument23 pagini74th Amendmentadityaap100% (3)

- CIVPRO Mod 1 CompilationDocument33 paginiCIVPRO Mod 1 CompilationKatrina PerezÎncă nu există evaluări

- Taxation Law ReviewerDocument6 paginiTaxation Law ReviewerAlex RabanesÎncă nu există evaluări

- Contractualization 4Document4 paginiContractualization 4grace hutallaÎncă nu există evaluări

- Final ObliconDocument4 paginiFinal ObliconPortgas D. AceÎncă nu există evaluări

- International Criminal Law Professor Scharf's Module on Nuremberg TrialsDocument245 paginiInternational Criminal Law Professor Scharf's Module on Nuremberg TrialsAlba P. Romero100% (1)

- Amritansh Agarwal: 15 Lacs 7 Yrs BhilaiDocument4 paginiAmritansh Agarwal: 15 Lacs 7 Yrs BhilaiAndreÎncă nu există evaluări

- Ortiz-Anglada v. Ortiz-Perez, 183 F.3d 65, 1st Cir. (1999)Document4 paginiOrtiz-Anglada v. Ortiz-Perez, 183 F.3d 65, 1st Cir. (1999)Scribd Government DocsÎncă nu există evaluări

- Drugstores Association of The Philippines, Inc. v. National Council On Disability AffairsDocument8 paginiDrugstores Association of The Philippines, Inc. v. National Council On Disability AffairsPatricia BautistaÎncă nu există evaluări

- Evidence-Hierarchy of CourtsDocument4 paginiEvidence-Hierarchy of CourtsShasharu Fei-fei LimÎncă nu există evaluări

- United States v. Andrew Jones, JR., 952 F.2d 397, 4th Cir. (1991)Document2 paginiUnited States v. Andrew Jones, JR., 952 F.2d 397, 4th Cir. (1991)Scribd Government DocsÎncă nu există evaluări