S-ar putea să vă placă și

- SCM Chapter NotesDocument50 paginiSCM Chapter Notesnishavijay0586% (37)

- Case 13 - Dream BeautyDocument2 paginiCase 13 - Dream Beautyahscen0% (1)

- MBS568 Org Change Management Assign 3Document12 paginiMBS568 Org Change Management Assign 3Senior Assistant Secretary EducationÎncă nu există evaluări

- Discussion QA 9to17Document56 paginiDiscussion QA 9to17April Reynolds100% (16)

- Case Study 3 - Westminster Company - ICO Bobby NortonDocument10 paginiCase Study 3 - Westminster Company - ICO Bobby NortonZeubenChatodkath0% (1)

- Case 1 - TQMDocument8 paginiCase 1 - TQMladdooparmarÎncă nu există evaluări

- Supply Chain Management Case StudyDocument2 paginiSupply Chain Management Case StudyLeonidÎncă nu există evaluări

- Assignment 9Document2 paginiAssignment 9Umar GondalÎncă nu există evaluări

- SCM 1-3 QuestionsDocument3 paginiSCM 1-3 Questionsvdfbdfh100% (1)

- DsvesrvceswcdsacDocument1 paginăDsvesrvceswcdsacBagasÎncă nu există evaluări

- Case Study: Manajemen Logistik & Rantai PasokDocument30 paginiCase Study: Manajemen Logistik & Rantai PasokDede AtmokoÎncă nu există evaluări

- Discussion Ch01Document16 paginiDiscussion Ch01An A Meisly80% (5)

- Supply Chain Logistics Management 4th Edition Bowersox Solutions ManualDocument3 paginiSupply Chain Logistics Management 4th Edition Bowersox Solutions Manuala37113077575% (4)

- Problem SetDocument5 paginiProblem SetKUMRÎncă nu există evaluări

- AmazonDocument9 paginiAmazonrubabÎncă nu există evaluări

- Where in The World Is Timbuk 2Document5 paginiWhere in The World Is Timbuk 2Anjulie LattaÎncă nu există evaluări

- Supply Chain ManagementDocument12 paginiSupply Chain ManagementRazib Razon100% (1)

- ME Problem Set-1 (2019)Document2 paginiME Problem Set-1 (2019)pikuÎncă nu există evaluări

- BMW Supply Chain NowDocument26 paginiBMW Supply Chain Nowapi-239652082100% (4)

- Chapter 8 Answers To ExercisesDocument12 paginiChapter 8 Answers To ExercisesSaroj Kumar RaiÎncă nu există evaluări

- Assignment 2: Competitive Forces Models Value Chain Model of The Foremost Common Business Level AreDocument6 paginiAssignment 2: Competitive Forces Models Value Chain Model of The Foremost Common Business Level AreNguyễn Quỳnh100% (1)

- Westminster CompanyDocument11 paginiWestminster CompanyAbhas Gupta100% (1)

- Case Study 1: E-Procurement at IBM: Answer The Questions (A)Document5 paginiCase Study 1: E-Procurement at IBM: Answer The Questions (A)Zannatun NayeemÎncă nu există evaluări

- Frequent FlierDocument2 paginiFrequent FlierSuman Nayak0% (2)

- CaseStudy SameDayDelivery Chopra 2019 PDFDocument2 paginiCaseStudy SameDayDelivery Chopra 2019 PDFApril NgÎncă nu există evaluări

- Integrated L & SCM Case StudyDocument21 paginiIntegrated L & SCM Case Studyrahul_thorat01Încă nu există evaluări

- Amazon Supply Chain Case StudyDocument2 paginiAmazon Supply Chain Case Studyknadmk100% (2)

- Assignment 8: Due Date: Nov. 6, 2003 (Thursday)Document4 paginiAssignment 8: Due Date: Nov. 6, 2003 (Thursday)mnbvqwerty100% (2)

- Syndicate-8 - OSCM-Group Assignment - Oil IndianDocument10 paginiSyndicate-8 - OSCM-Group Assignment - Oil IndianHasbi Asidik100% (1)

- PDF Solution Manual For Supply Chain Management 4 e Sunil Chopra Peter MeindlDocument16 paginiPDF Solution Manual For Supply Chain Management 4 e Sunil Chopra Peter MeindlsivaÎncă nu există evaluări

- ToshibaDocument2 paginiToshibaRian KrisnaÎncă nu există evaluări

- Chopra Meindl SCM Ch1 PDFDocument19 paginiChopra Meindl SCM Ch1 PDFKausarAtique100% (1)

- Two Wheeler Industry - Probability DistributionDocument7 paginiTwo Wheeler Industry - Probability DistributionSrikanth Kumar KonduriÎncă nu există evaluări

- EOQ ModelDocument41 paginiEOQ ModelAbhijeet Agarwal100% (1)

- Walmart SCM Project Final DraftDocument23 paginiWalmart SCM Project Final Draftapi-2826902350% (1)

- Supply Chain Management Chopra 4th Solut PDFDocument6 paginiSupply Chain Management Chopra 4th Solut PDFAkash Kyal0% (1)

- Operations Management Pactice QuestionsDocument8 paginiOperations Management Pactice QuestionsHumphrey OsaigbeÎncă nu există evaluări

- Problem1: Several Samples of Size N 8 Have Been TakenDocument4 paginiProblem1: Several Samples of Size N 8 Have Been TakenavgadekarÎncă nu există evaluări

- SCM G Students Handout Solutions - SP5 - 2013Document25 paginiSCM G Students Handout Solutions - SP5 - 2013lordraiÎncă nu există evaluări

- Chapter 5: Procurement and OutsourcingDocument3 paginiChapter 5: Procurement and OutsourcingLinh LêÎncă nu există evaluări

- Supply Chain Management at AmulDocument25 paginiSupply Chain Management at AmulSanu KumarÎncă nu există evaluări

- (P-7) As A Hospital Administrator of A Large Hospital, You Are Concerned With The Absenteeism Among Nurses' Aides. The Issue HasDocument6 pagini(P-7) As A Hospital Administrator of A Large Hospital, You Are Concerned With The Absenteeism Among Nurses' Aides. The Issue HasHarmanda Berima Putra100% (1)

- Supply Chain Management Notes For Distribution PlanningDocument40 paginiSupply Chain Management Notes For Distribution PlanningahahaÎncă nu există evaluări

- Itc Supply ChainDocument18 paginiItc Supply Chainrukhsar nasimÎncă nu există evaluări

- Discussion QuestionsDocument60 paginiDiscussion QuestionsUmar Gondal100% (1)

- P&G Case: Proctor and Gamble India: Gap in The Product Portfolio?Document6 paginiP&G Case: Proctor and Gamble India: Gap in The Product Portfolio?Param NagdaÎncă nu există evaluări

- Chap 04Document9 paginiChap 04gttomcatÎncă nu există evaluări

- Chapter 11 Project Analysis and ValuationDocument24 paginiChapter 11 Project Analysis and ValuationElizabeth Alexandria Lauren100% (1)

- Discussion Ch01Document3 paginiDiscussion Ch01Zoey Schully100% (7)

- SCM Sunil Chopra Chapter 2 DISCUSSION QUESTION.Document11 paginiSCM Sunil Chopra Chapter 2 DISCUSSION QUESTION.Seher NazÎncă nu există evaluări

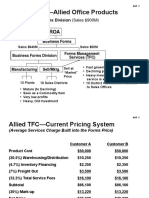

- ABC Costing Allied Office ProductsDocument13 paginiABC Costing Allied Office ProductsProfessorAsim Kumar Mishra100% (1)

- Dream Beauty Case StudyDocument2 paginiDream Beauty Case StudyWoocationsÎncă nu există evaluări

- Assessment 2 Group Case Study PresentationDocument3 paginiAssessment 2 Group Case Study PresentationSenisaaÎncă nu există evaluări

- Faculty of Business and Management Individual AssignmentDocument9 paginiFaculty of Business and Management Individual Assignment静思Încă nu există evaluări

- Case Study 03Document6 paginiCase Study 03Shahana AfrozÎncă nu există evaluări

- LOGISTICSDocument7 paginiLOGISTICStania navaÎncă nu există evaluări

- CHAPTER 6: (C8 Trong Sách) Strategic Alliances: Case: How Kimberly-Clark Keeps Client Costco in DiapersDocument11 paginiCHAPTER 6: (C8 Trong Sách) Strategic Alliances: Case: How Kimberly-Clark Keeps Client Costco in DiapersLinh LêÎncă nu există evaluări

- 7 Ways Everyone Can Cut Supply Chain CostsDocument7 pagini7 Ways Everyone Can Cut Supply Chain CostsbumbiazarkaÎncă nu există evaluări

- Retail Supply Chain ManagementDocument9 paginiRetail Supply Chain ManagementShivatiÎncă nu există evaluări

- SCM PDFDocument32 paginiSCM PDFFikr SelamÎncă nu există evaluări

- Wall WashDocument3 paginiWall WashANZÎncă nu există evaluări

- VTS Operator Model Course v103!1!1Document86 paginiVTS Operator Model Course v103!1!1ANZÎncă nu există evaluări

- MenuDocument1 paginăMenuANZÎncă nu există evaluări

- Ship-Brokers 02 March 2016Document2 paginiShip-Brokers 02 March 2016ANZ100% (1)

- Evergas: 6) GML SERVICES GAC Management Labour (Product One of GAC) 8) Hub Services (Product Two of GAC)Document2 paginiEvergas: 6) GML SERVICES GAC Management Labour (Product One of GAC) 8) Hub Services (Product Two of GAC)ANZÎncă nu există evaluări

- SBR 4 Group 2Document5 paginiSBR 4 Group 2ANZÎncă nu există evaluări

- Differences Between The Hamburg and HaguDocument9 paginiDifferences Between The Hamburg and HaguANZÎncă nu există evaluări

- S.No Item Description Unit Qty Unit PriceDocument4 paginiS.No Item Description Unit Qty Unit PriceANZÎncă nu există evaluări

- BrunswickDistn Optn11Document8 paginiBrunswickDistn Optn11ANZÎncă nu există evaluări

- Report AssignmentDocument1 paginăReport AssignmentANZÎncă nu există evaluări

- Zara Case StudyDocument2 paginiZara Case StudyANZÎncă nu există evaluări

- Leather's Best Inc. v. SS MormaclynxDocument5 paginiLeather's Best Inc. v. SS MormaclynxANZÎncă nu există evaluări

- OM Set 3Document26 paginiOM Set 3ANZÎncă nu există evaluări

- Zara BenettonDocument2 paginiZara BenettonANZÎncă nu există evaluări

- Answer 2: Conflicts That Are Likely To Be Created Within Barilla by The JITD ProgramDocument2 paginiAnswer 2: Conflicts That Are Likely To Be Created Within Barilla by The JITD ProgramANZÎncă nu există evaluări

- SBR Schedule Supply ChainDocument1 paginăSBR Schedule Supply ChainANZÎncă nu există evaluări

- Zara BenettonDocument2 paginiZara BenettonANZÎncă nu există evaluări

- Core Values Behavioral Statements Quarter 1 2 3 4Document1 paginăCore Values Behavioral Statements Quarter 1 2 3 4Michael Fernandez ArevaloÎncă nu există evaluări

- Febi Dwirahmadi - PPT Disaster Management and COVID19Document34 paginiFebi Dwirahmadi - PPT Disaster Management and COVID19Fenny RahmadianitaÎncă nu există evaluări

- (Bloom's Modern Critical Views) (2000)Document267 pagini(Bloom's Modern Critical Views) (2000)andreea1613232100% (1)

- Basic Accounting Equation Exercises 2Document2 paginiBasic Accounting Equation Exercises 2Ace Joseph TabaderoÎncă nu există evaluări

- CMAT Score CardDocument1 paginăCMAT Score CardRaksha RudraÎncă nu există evaluări

- Functional Skill: 1. Offering HelpDocument36 paginiFunctional Skill: 1. Offering HelpAnita Sri WidiyaaÎncă nu există evaluări

- Biology 31a2011 (Female)Document6 paginiBiology 31a2011 (Female)Hira SikanderÎncă nu există evaluări

- E-Conclave Spon BrochureDocument17 paginiE-Conclave Spon BrochureNimish KadamÎncă nu există evaluări

- Accounting Information System Performance Task Week 6Document1 paginăAccounting Information System Performance Task Week 6Cristel Ann DotimasÎncă nu există evaluări

- Design of Swimming Pool PDFDocument21 paginiDesign of Swimming Pool PDFjanithbogahawatta67% (3)

- All Region TMLDocument9 paginiAll Region TMLVijayalakshmiÎncă nu există evaluări

- Financial Report: The Coca Cola Company: Ews/2021-10-27 - Coca - Cola - Reports - Continued - Momentum - and - Strong - 1040 PDFDocument3 paginiFinancial Report: The Coca Cola Company: Ews/2021-10-27 - Coca - Cola - Reports - Continued - Momentum - and - Strong - 1040 PDFDominic MuliÎncă nu există evaluări

- Marking SchemeDocument57 paginiMarking SchemeBurhanÎncă nu există evaluări

- Business Enterprise Simulation Quarter 3 - Module 2 - Lesson 1: Analyzing The MarketDocument13 paginiBusiness Enterprise Simulation Quarter 3 - Module 2 - Lesson 1: Analyzing The MarketJtm GarciaÎncă nu există evaluări

- Times Leader 03-16-2013Document61 paginiTimes Leader 03-16-2013The Times LeaderÎncă nu există evaluări

- NIST SP 800-53ar5-1Document5 paginiNIST SP 800-53ar5-1Guillermo Valdès100% (1)

- Glories of Srimad Bhagavatam - Bhaktivedanta VidyapithaDocument7 paginiGlories of Srimad Bhagavatam - Bhaktivedanta VidyapithaPrajot NairÎncă nu există evaluări

- Organization and ManagementDocument65 paginiOrganization and ManagementIvan Kirby EncarnacionÎncă nu există evaluări

- DepEd Red Cross 3 4 Seater Detached PoWs BoQsDocument42 paginiDepEd Red Cross 3 4 Seater Detached PoWs BoQsRamil S. ArtatesÎncă nu există evaluări

- Kaalabhiravashtakam With English ExplainationDocument2 paginiKaalabhiravashtakam With English ExplainationShashanka KshetrapalasharmaÎncă nu există evaluări

- Down in Porto Rico With A KodakDocument114 paginiDown in Porto Rico With A KodakBeba Atsg100% (1)

- Dam Water SensorDocument63 paginiDam Water SensorMuhammad RizalÎncă nu există evaluări

- Developing A Business Plan For Your Vet PracticeDocument7 paginiDeveloping A Business Plan For Your Vet PracticeMujtaba AusafÎncă nu există evaluări

- Form Audit QAV 1&2 Supplier 2020 PDFDocument1 paginăForm Audit QAV 1&2 Supplier 2020 PDFovanÎncă nu există evaluări

- Republic Act No. 9775 (#1)Document6 paginiRepublic Act No. 9775 (#1)Marc Jalen ReladorÎncă nu există evaluări

- Tally Trading and Profit Loss Acc Balance SheetDocument14 paginiTally Trading and Profit Loss Acc Balance Sheetsuresh kumar10Încă nu există evaluări

- Ch.6 TariffsDocument59 paginiCh.6 TariffsDina SamirÎncă nu există evaluări

- Starmada House RulesDocument2 paginiStarmada House Ruleshvwilson62Încă nu există evaluări

- Literacy Technology of The IntellectDocument20 paginiLiteracy Technology of The IntellectFrances Tay100% (1)

- The Age of Agile: How Smart Companies Are Transforming the Way Work Gets DoneDe la EverandThe Age of Agile: How Smart Companies Are Transforming the Way Work Gets DoneEvaluare: 4.5 din 5 stele4.5/5 (5)

- PMP Exam Prep: How to pass the PMP Exam on your First Attempt – Learn Faster, Retain More and Pass the PMP ExamDe la EverandPMP Exam Prep: How to pass the PMP Exam on your First Attempt – Learn Faster, Retain More and Pass the PMP ExamEvaluare: 4.5 din 5 stele4.5/5 (3)

- The Goal: A Process of Ongoing Improvement - 30th Aniversary EditionDe la EverandThe Goal: A Process of Ongoing Improvement - 30th Aniversary EditionEvaluare: 4 din 5 stele4/5 (685)

- Reliable Maintenance Planning, Estimating, and SchedulingDe la EverandReliable Maintenance Planning, Estimating, and SchedulingEvaluare: 5 din 5 stele5/5 (5)

- Revolutionizing Business Operations: How to Build Dynamic Processes for Enduring Competitive AdvantageDe la EverandRevolutionizing Business Operations: How to Build Dynamic Processes for Enduring Competitive AdvantageÎncă nu există evaluări

- Value Stream Mapping: How to Visualize Work and Align Leadership for Organizational Transformation: How to Visualize Work and Align Leadership for Organizational TransformationDe la EverandValue Stream Mapping: How to Visualize Work and Align Leadership for Organizational Transformation: How to Visualize Work and Align Leadership for Organizational TransformationEvaluare: 5 din 5 stele5/5 (34)

- The Supply Chain Revolution: Innovative Sourcing and Logistics for a Fiercely Competitive WorldDe la EverandThe Supply Chain Revolution: Innovative Sourcing and Logistics for a Fiercely Competitive WorldÎncă nu există evaluări

- The Influential Product Manager: How to Lead and Launch Successful Technology ProductsDe la EverandThe Influential Product Manager: How to Lead and Launch Successful Technology ProductsEvaluare: 4.5 din 5 stele4.5/5 (11)

- Project Planning and SchedulingDe la EverandProject Planning and SchedulingEvaluare: 5 din 5 stele5/5 (6)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItDe la EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItEvaluare: 4.5 din 5 stele4.5/5 (14)

- Working Backwards: Insights, Stories, and Secrets from Inside AmazonDe la EverandWorking Backwards: Insights, Stories, and Secrets from Inside AmazonEvaluare: 4.5 din 5 stele4.5/5 (44)

- Summary of High Output Management: by Andrew S. Grove| Includes AnalysisDe la EverandSummary of High Output Management: by Andrew S. Grove| Includes AnalysisÎncă nu există evaluări

- Working Backwards: Insights, Stories, and Secrets from Inside AmazonDe la EverandWorking Backwards: Insights, Stories, and Secrets from Inside AmazonEvaluare: 4.5 din 5 stele4.5/5 (14)

- Materials Management: An Executive's Supply Chain GuideDe la EverandMaterials Management: An Executive's Supply Chain GuideÎncă nu există evaluări

- The Toyota Way, Second Edition: 14 Management Principles from the World's Greatest ManufacturerDe la EverandThe Toyota Way, Second Edition: 14 Management Principles from the World's Greatest ManufacturerEvaluare: 4 din 5 stele4/5 (103)

- Design Thinking for Beginners: Innovation as a Factor for Entrepreneurial SuccessDe la EverandDesign Thinking for Beginners: Innovation as a Factor for Entrepreneurial SuccessEvaluare: 4.5 din 5 stele4.5/5 (7)

- The Influential Product Manager: How to Lead and Launch Successful Technology ProductsDe la EverandThe Influential Product Manager: How to Lead and Launch Successful Technology ProductsEvaluare: 5 din 5 stele5/5 (2)

- Spare Parts Inventory Management: A Complete Guide to SparesologyDe la EverandSpare Parts Inventory Management: A Complete Guide to SparesologyEvaluare: 4 din 5 stele4/5 (3)

- Vibration Basics and Machine Reliability Simplified : A Practical Guide to Vibration AnalysisDe la EverandVibration Basics and Machine Reliability Simplified : A Practical Guide to Vibration AnalysisEvaluare: 4 din 5 stele4/5 (2)

- Production Planning and Control: A Comprehensive ApproachDe la EverandProduction Planning and Control: A Comprehensive ApproachEvaluare: 5 din 5 stele5/5 (2)

- Results, Not Reports: Building Exceptional Organizations by Integrating Process, Performance, and PeopleDe la EverandResults, Not Reports: Building Exceptional Organizations by Integrating Process, Performance, and PeopleÎncă nu există evaluări

- Maintenance and Operational Reliability: 24 Essential Building BlocksDe la EverandMaintenance and Operational Reliability: 24 Essential Building BlocksÎncă nu există evaluări