S-ar putea să vă placă și

- Six Strategies To Deal Withcompetition SandhiDocument3 paginiSix Strategies To Deal Withcompetition SandhiKaran BhatiaÎncă nu există evaluări

- Even If A Snake Is Not PoisonousDocument5 paginiEven If A Snake Is Not PoisonousKaran BhatiaÎncă nu există evaluări

- Again NNNDocument3 paginiAgain NNNKaran BhatiaÎncă nu există evaluări

- Literature Review Sneha ProjectDocument3 paginiLiterature Review Sneha ProjectKaran BhatiaÎncă nu există evaluări

- 1st 3 N Last 2 Pgs.Document11 pagini1st 3 N Last 2 Pgs.Karan BhatiaÎncă nu există evaluări

- Final Format of Covering PageDocument5 paginiFinal Format of Covering PageKaran BhatiaÎncă nu există evaluări

- Questionnaire Black BookDocument2 paginiQuestionnaire Black BookKaran Bhatia100% (1)

- A Resarch Paper On GST and Its Impact On Service SectorDocument7 paginiA Resarch Paper On GST and Its Impact On Service SectorKaran BhatiaÎncă nu există evaluări

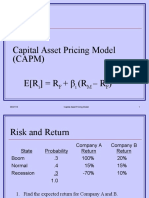

- Capital Asset Pricing ModelDocument25 paginiCapital Asset Pricing ModelKaran BhatiaÎncă nu există evaluări

- A Resarch Paper On GST and Its Impact On Service SectorDocument7 paginiA Resarch Paper On GST and Its Impact On Service SectorKaran BhatiaÎncă nu există evaluări

- Capital Market LineDocument2 paginiCapital Market LineKaran BhatiaÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Ee Announcement Presentation FinalDocument31 paginiEe Announcement Presentation Finalkoundi_3Încă nu există evaluări

- Dominos+Pizza+Financial+Model+v1 TemplateDocument5 paginiDominos+Pizza+Financial+Model+v1 TemplateEmperor OverwatchÎncă nu există evaluări

- Interim Financial Reporting: Problem 45-1: True or FalseDocument7 paginiInterim Financial Reporting: Problem 45-1: True or FalseMarjorieÎncă nu există evaluări

- Sample Engagement LetterDocument4 paginiSample Engagement LetterAnurag Gupta50% (2)

- USA V Sales - IndictmentDocument6 paginiUSA V Sales - IndictmentJustin OkunÎncă nu există evaluări

- Daily Lesson Log/Plan: Monday Tuesday Wednesday ThursdayDocument5 paginiDaily Lesson Log/Plan: Monday Tuesday Wednesday ThursdayJovelyn Ignacio VinluanÎncă nu există evaluări

- 47 Electricity Accounting Theory ProblemsDocument5 pagini47 Electricity Accounting Theory Problemsbala_ae100% (1)

- Multiple Choice. Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionsDocument8 paginiMultiple Choice. Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionsRandy ManzanoÎncă nu există evaluări

- Agreement To Organize A BankDocument3 paginiAgreement To Organize A BankrotiliÎncă nu există evaluări

- Airthread Acquisition: Income StatementDocument31 paginiAirthread Acquisition: Income StatementnidhidÎncă nu există evaluări

- Formation of A Company Act 1956Document56 paginiFormation of A Company Act 1956Dhaval ThakorÎncă nu există evaluări

- Manage Work Priorities and Professional LevelDocument6 paginiManage Work Priorities and Professional Levelparul sharmaÎncă nu există evaluări

- CemexDocument21 paginiCemexMiguel Leal100% (4)

- State Bank of India Internship ProjectDocument61 paginiState Bank of India Internship ProjectPrince BhardwajÎncă nu există evaluări

- Corporate Finance Chapter10Document55 paginiCorporate Finance Chapter10James ManningÎncă nu există evaluări

- FPA Entrance Test 60 Menit (Answer)Document10 paginiFPA Entrance Test 60 Menit (Answer)Andri GintingÎncă nu există evaluări

- Case 4Document11 paginiCase 4krish lopezÎncă nu există evaluări

- Sikkim Co Operative Societies Act 1978Document67 paginiSikkim Co Operative Societies Act 1978Latest Laws TeamÎncă nu există evaluări

- KelloggsDocument4 paginiKelloggshasan_waqar2004Încă nu există evaluări

- Non-Banking Finance Companies in India's Financial LandscapeDocument18 paginiNon-Banking Finance Companies in India's Financial Landscapeshubham moonÎncă nu există evaluări

- ONG YONG Vs TIUDocument14 paginiONG YONG Vs TIUJan MartinÎncă nu există evaluări

- Valuation of BondsDocument7 paginiValuation of BondsHannah Louise Gutang PortilloÎncă nu există evaluări

- Cash Flow Statement: (Cheat Sheet)Document5 paginiCash Flow Statement: (Cheat Sheet)LinyVatÎncă nu există evaluări

- S.I and C.IDocument16 paginiS.I and C.IMumtazAhmad100% (1)

- Corporate Strategy A Lecture 1Document64 paginiCorporate Strategy A Lecture 1Falak ShaikhaniÎncă nu există evaluări

- PT ESS1217 - Mapping Report Break LinkDocument392 paginiPT ESS1217 - Mapping Report Break Linkricho naiborhuÎncă nu există evaluări

- Production of Urea Formaldehyde UF85-947312 - 2Document66 paginiProduction of Urea Formaldehyde UF85-947312 - 2Sanzar Rahman 1621555030Încă nu există evaluări

- International Public Sector Accounting Standards (IPSAS) (A4)Document12 paginiInternational Public Sector Accounting Standards (IPSAS) (A4)Moses K. Wangaruro100% (1)

- Nature of Financial ManagementDocument12 paginiNature of Financial ManagementShashankÎncă nu există evaluări

- My Subscriptions Courses ACC410-Advanced Accounting Chapter 2 HomeworkDocument29 paginiMy Subscriptions Courses ACC410-Advanced Accounting Chapter 2 Homeworksuruth242Încă nu există evaluări