S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Inv 688817583 200279620 202011200114 PDFDocument1 paginăInv 688817583 200279620 202011200114 PDFriyasathsafranÎncă nu există evaluări

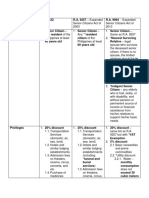

- Title R.A. 7432 R.A. 9257 R.A. 9994 - ExpandedDocument11 paginiTitle R.A. 7432 R.A. 9257 R.A. 9994 - ExpandedAngel Alejo AcobaÎncă nu există evaluări

- DTC Agreement Between Israel and BelgiumDocument30 paginiDTC Agreement Between Israel and BelgiumOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- Income Tax On Intraday TradingDocument7 paginiIncome Tax On Intraday Tradingkrutarth patelÎncă nu există evaluări

- HotelDocument2 paginiHotelSagar KattimaniÎncă nu există evaluări

- Payroll Training PresentationDocument47 paginiPayroll Training PresentationMarkandeya ChitturiÎncă nu există evaluări

- ACP312 - ULOb - IN A NUTSHELL - ReflectionDocument1 paginăACP312 - ULOb - IN A NUTSHELL - Reflectionalmira garciaÎncă nu există evaluări

- Auditing AssignmentDocument8 paginiAuditing AssignmentApril ManjaresÎncă nu există evaluări

- Congress of The Philippines Metro ManilaDocument13 paginiCongress of The Philippines Metro ManilaLyna Manlunas GayasÎncă nu există evaluări

- Taxation: Taxation Is The Supreme Power of A Sovereign State Through Its Law-Making Body, To Impose BurdensDocument6 paginiTaxation: Taxation Is The Supreme Power of A Sovereign State Through Its Law-Making Body, To Impose BurdensTriangular PrismÎncă nu există evaluări

- Solution Manual For Concepts in Federal Taxation 2018 25th Edition Murphy, HigginsDocument2 paginiSolution Manual For Concepts in Federal Taxation 2018 25th Edition Murphy, Higginsa882650259Încă nu există evaluări

- Financial Statements PreparationDocument6 paginiFinancial Statements Preparationana lopezÎncă nu există evaluări

- Reply For 16Document1 paginăReply For 16Abhay NandaÎncă nu există evaluări

- C4 PDFDocument373 paginiC4 PDFIssa Adiema100% (4)

- Ashley Dixon-Harrison 293 Whittenton ST Apt 1Ft TAUNTON MA 02780-1305Document2 paginiAshley Dixon-Harrison 293 Whittenton ST Apt 1Ft TAUNTON MA 02780-1305ashcat227 DÎncă nu există evaluări

- Form GST REG-06: (Amended)Document3 paginiForm GST REG-06: (Amended)Mehak LohiaÎncă nu există evaluări

- Basics of Income Tax of India PDFDocument19 paginiBasics of Income Tax of India PDFJai VermaÎncă nu există evaluări

- Impact of GST On WholesalerDocument20 paginiImpact of GST On Wholesalerjayesh50% (2)

- Goods and Services Tax (GST) in India: CA. Preeti GoyalDocument30 paginiGoods and Services Tax (GST) in India: CA. Preeti GoyalArvind PalÎncă nu există evaluări

- Bitumen VG-30-3Document2 paginiBitumen VG-30-3Morya RonakÎncă nu există evaluări

- Business Taxation Solman Tabag@garcia PDFDocument42 paginiBusiness Taxation Solman Tabag@garcia PDFJoey AbrahamÎncă nu există evaluări

- Quiz Number 4Document24 paginiQuiz Number 4justine cabanaÎncă nu există evaluări

- Tax Allocations and ApportionmentDocument18 paginiTax Allocations and Apportionmentrobertkolasa100% (1)

- Manual Instruction - 1770 - 2010 - English PDFDocument46 paginiManual Instruction - 1770 - 2010 - English PDFHafiedz SÎncă nu există evaluări

- TAX EVASION and AVOIDANCE - A REAL PROBDocument14 paginiTAX EVASION and AVOIDANCE - A REAL PROBAsaduzzaman ShuvoÎncă nu există evaluări

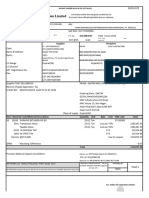

- Worldone Enterprises: Billing Address: Shipping AddressDocument1 paginăWorldone Enterprises: Billing Address: Shipping AddressAmit SinghÎncă nu există evaluări

- Essay DemonetizationDocument4 paginiEssay DemonetizationRaj SharmaÎncă nu există evaluări

- 2C00445Document41 pagini2C00445VijayÎncă nu există evaluări

- Multiple-Choice-Questions FinalDocument3 paginiMultiple-Choice-Questions FinalFreann Sharisse Austria100% (1)