S-ar putea să vă placă și

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document10 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid AliÎncă nu există evaluări

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document11 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali100% (1)

- Corporate Financial Analysis with Microsoft ExcelDe la EverandCorporate Financial Analysis with Microsoft ExcelEvaluare: 5 din 5 stele5/5 (1)

- Statement of Cash Flows: Preparation, Presentation, and UseDe la EverandStatement of Cash Flows: Preparation, Presentation, and UseÎncă nu există evaluări

- Equity Financing A Complete Guide - 2020 EditionDe la EverandEquity Financing A Complete Guide - 2020 EditionÎncă nu există evaluări

- Cash Budget - Cash Budgeting:: Definition and ExplanationDocument5 paginiCash Budget - Cash Budgeting:: Definition and ExplanationPrajay KhÎncă nu există evaluări

- CH 4Document6 paginiCH 4Jean ValderramaÎncă nu există evaluări

- BFC5935 - Tutorial 9 SolutionsDocument6 paginiBFC5935 - Tutorial 9 SolutionsXue XuÎncă nu există evaluări

- MCS MatH QSTN NewDocument7 paginiMCS MatH QSTN NewSrijita SahaÎncă nu există evaluări

- Quantitative TechniquesDocument11 paginiQuantitative TechniquessanjayifmÎncă nu există evaluări

- AccA P4/3.7 - 2002 - Dec - QDocument12 paginiAccA P4/3.7 - 2002 - Dec - Qroker_m3Încă nu există evaluări

- Financial Accounting (Unsolved Papers of ICMAP)Document48 paginiFinancial Accounting (Unsolved Papers of ICMAP)Platonic0% (1)

- Cost of Capital Lecture Slides in PDF FormatDocument18 paginiCost of Capital Lecture Slides in PDF FormatLucy UnÎncă nu există evaluări

- Based On Session 5 - Responsibility Accounting & Transfer PricingDocument5 paginiBased On Session 5 - Responsibility Accounting & Transfer PricingMERINAÎncă nu există evaluări

- Couresot LineDocument2 paginiCouresot LineSeifu BekeleÎncă nu există evaluări

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document10 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali0% (1)

- Weighted Average Cost of Capital: Banikanta MishraDocument21 paginiWeighted Average Cost of Capital: Banikanta MishraManu ThomasÎncă nu există evaluări

- LN01 Rejda99500X 12 Principles LN04Document40 paginiLN01 Rejda99500X 12 Principles LN04Abdirahman M. SalahÎncă nu există evaluări

- Equity Valuation-1Document37 paginiEquity Valuation-1Disha BakshiÎncă nu există evaluări

- Functions of Treasury MGTDocument5 paginiFunctions of Treasury MGTk-911Încă nu există evaluări

- Fixed Assets Interview Questions and Answers 432 1Document10 paginiFixed Assets Interview Questions and Answers 432 1Ekramullah SadatÎncă nu există evaluări

- Exam 1 - VI SolutionsDocument9 paginiExam 1 - VI Solutionssyeda hifzaÎncă nu există evaluări

- ICMA Questions Dec 2012Document55 paginiICMA Questions Dec 2012Asadul HoqueÎncă nu există evaluări

- Final Accounts With Out AdjustmentsDocument2 paginiFinal Accounts With Out AdjustmentsMurari NayuduÎncă nu există evaluări

- WAQ Produces A Single Product XDocument2 paginiWAQ Produces A Single Product Xmj192Încă nu există evaluări

- NPV Practice CompleteDocument5 paginiNPV Practice CompleteShakeel AslamÎncă nu există evaluări

- RatioDocument24 paginiRatioSadika KhanÎncă nu există evaluări

- An Iso 9001: 2000 Certified International B-SchoolDocument4 paginiAn Iso 9001: 2000 Certified International B-SchoolKunal BadhwarÎncă nu există evaluări

- E-14 AfrDocument5 paginiE-14 AfrInternational Iqbal ForumÎncă nu există evaluări

- Exercises On Issue of Shares and DebenturesDocument6 paginiExercises On Issue of Shares and Debenturesontykerls100% (1)

- Transfer PricingDocument15 paginiTransfer PricingEjaz Khan100% (1)

- Sol 3 CH 6Document46 paginiSol 3 CH 6Aditya KrishnaÎncă nu există evaluări

- Financial Markets QuestionsDocument54 paginiFinancial Markets QuestionsMathias VindalÎncă nu există evaluări

- T1 - Tutorial MaDocument10 paginiT1 - Tutorial Matylee970% (1)

- Chapter-1-Regulatory FrameworkDocument6 paginiChapter-1-Regulatory FrameworkYean Soramy100% (1)

- CE 366 Exam 3 Review - SDocument7 paginiCE 366 Exam 3 Review - SShaunak TripathiÎncă nu există evaluări

- International Portfolio Investment Q & ADocument7 paginiInternational Portfolio Investment Q & AaasisranjanÎncă nu există evaluări

- Exam Answers HHHDocument2 paginiExam Answers HHHKhalid Mishczsuski Limu100% (1)

- Activity Base Costing (ABC Costing)Document12 paginiActivity Base Costing (ABC Costing)SantÎncă nu există evaluări

- ACCA F9 Revision Notes OpenTuition PDFDocument48 paginiACCA F9 Revision Notes OpenTuition PDFchilloutdude108Încă nu există evaluări

- Accounting For LeasesDocument4 paginiAccounting For LeasesSebastian MlingwaÎncă nu există evaluări

- P2 November 2014 Question Paper PDFDocument20 paginiP2 November 2014 Question Paper PDFAnu MauryaÎncă nu există evaluări

- How To Pass AFC CAF in 2.5 To 3 YearsDocument5 paginiHow To Pass AFC CAF in 2.5 To 3 YearsSyed Muhammad Nabeel Akhter0% (2)

- Income StatementDocument13 paginiIncome StatementThéotime HabinezaÎncă nu există evaluări

- IntangiblesDocument2 paginiIntangiblesMuhammadUmarNazirChishtiÎncă nu există evaluări

- Test and Exam Qs Topic 2 - Solutions - v2 PDFDocument20 paginiTest and Exam Qs Topic 2 - Solutions - v2 PDFCindy YinÎncă nu există evaluări

- Assignment of Time Value of MoneyDocument3 paginiAssignment of Time Value of MoneyMuxammil IqbalÎncă nu există evaluări

- Decision-Making Using Marginal Costing-IDocument11 paginiDecision-Making Using Marginal Costing-Iapi-27014089100% (3)

- Acct 2 0Document9 paginiAcct 2 0Kamran HaiderÎncă nu există evaluări

- Ratio Analysis of Bank Al Habib Limited, Habib Metropolitan Bank Limited and J.S Bank Limited For Financial Year 2013, 2014 and 2015Document11 paginiRatio Analysis of Bank Al Habib Limited, Habib Metropolitan Bank Limited and J.S Bank Limited For Financial Year 2013, 2014 and 2015Mubarak HussainÎncă nu există evaluări

- Discussion QuestionsDocument12 paginiDiscussion Questionsđức nguyễn minh100% (1)

- ACCA F5: Chapter 13 - Divisional Performance Measurement and Transfer PricingDocument8 paginiACCA F5: Chapter 13 - Divisional Performance Measurement and Transfer PricingRajeshwar NagaisarÎncă nu există evaluări

- FINANCIAL MANAGEMENT Assignment Questions 22Document12 paginiFINANCIAL MANAGEMENT Assignment Questions 22Natasha DavidsÎncă nu există evaluări

- Exposure Management Internal TechniquesDocument8 paginiExposure Management Internal TechniquesArockia Shiny SÎncă nu există evaluări

- All HOMEWORK ANSWER KEYDocument6 paginiAll HOMEWORK ANSWER KEYhy_saingheng_7602609Încă nu există evaluări

- Tutorial Problems - Capital BudgetingDocument6 paginiTutorial Problems - Capital BudgetingMarcoBonaparte0% (1)

- 2 Moodle Assignment 1Document6 pagini2 Moodle Assignment 1SOHAIL TARIQÎncă nu există evaluări

- The Cost of Trade CreditDocument4 paginiThe Cost of Trade CreditWawex DavisÎncă nu există evaluări

- ACCA F8-2015-Jun-QDocument10 paginiACCA F8-2015-Jun-QSusie HopeÎncă nu există evaluări

- Chapter 11 SolutionsDocument22 paginiChapter 11 SolutionsChander Santos Monteiro100% (3)

- Chapter 16Document11 paginiChapter 16Aarti J50% (2)

- Chpater 4 SolutionsDocument13 paginiChpater 4 SolutionsAhmed Rawy100% (1)

- Chapter 13 Solutions MKDocument26 paginiChapter 13 Solutions MKCindy Kirana17% (6)

- Chapter 14 SolutionsDocument10 paginiChapter 14 SolutionsAmanda Ng100% (1)

- Chapter 9 SolutionsDocument11 paginiChapter 9 Solutionssaddam hussain80% (5)

- Chapter 12 SolutionsDocument13 paginiChapter 12 SolutionsCindy Lee75% (4)

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document11 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali100% (1)

- Chapter 15Document6 paginiChapter 15Rayhan Atunu100% (1)

- Chapter 8 Solutions GitmanDocument22 paginiChapter 8 Solutions GitmanCat Valentine100% (3)

- Chapter 10 SolutionsDocument21 paginiChapter 10 SolutionsFranco Ambunan Regino75% (8)

- Chapter 7 SolutionsDocument9 paginiChapter 7 SolutionsMuhammad Naeem100% (3)

- Chapter 2 SolutionsDocument5 paginiChapter 2 SolutionskendozxÎncă nu există evaluări

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document10 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali0% (1)

- Chapter 1 SolutionsDocument3 paginiChapter 1 SolutionsChadwick PohÎncă nu există evaluări

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document13 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid AliÎncă nu există evaluări

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document12 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali50% (2)

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document12 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali67% (3)

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document11 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali100% (1)

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document11 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid AliÎncă nu există evaluări

- Notice Transitional ArrangementDocument1 paginăNotice Transitional ArrangementSajid AliÎncă nu există evaluări

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document12 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali100% (1)

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document12 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid AliÎncă nu există evaluări

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document12 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid AliÎncă nu există evaluări

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document15 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid AliÎncă nu există evaluări

- Jvi RPT 23062k16Document23 paginiJvi RPT 23062k16Sajid AliÎncă nu există evaluări

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document14 pagini3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali100% (1)

- Tool SatenaDocument59 paginiTool SatenaJeysson SilvaÎncă nu există evaluări

- Sps. Nilo Cha and Stella Uy Cha, Et. Al. vs. Court of Appeals, Et. Al., G.R. No. 124520. Aug. 18, 1997Document1 paginăSps. Nilo Cha and Stella Uy Cha, Et. Al. vs. Court of Appeals, Et. Al., G.R. No. 124520. Aug. 18, 1997Minorka Sushmita Pataunia SantoluisÎncă nu există evaluări

- 1 s2.0 S2772801321000026 MainDocument9 pagini1 s2.0 S2772801321000026 Mainishani sahaÎncă nu există evaluări

- Powers of The CorporationDocument7 paginiPowers of The CorporationMon RamÎncă nu există evaluări

- About Globalisation and IHRMDocument29 paginiAbout Globalisation and IHRMsharnagatÎncă nu există evaluări

- R15 Firm and Market Structures - Q BankDocument12 paginiR15 Firm and Market Structures - Q Bankakshay mouryaÎncă nu există evaluări

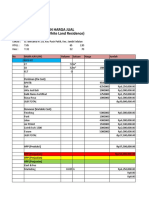

- Modular Harga Jual WLR2Document25 paginiModular Harga Jual WLR2Next LevelManagementÎncă nu există evaluări

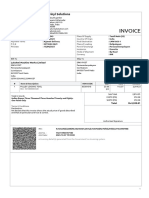

- Invoice: Sakvinyl SolutionsDocument1 paginăInvoice: Sakvinyl SolutionsMEENAKSHI IQCSÎncă nu există evaluări

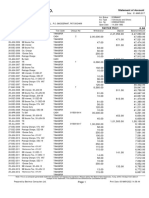

- Agrani Bank LTD.: Statement of AccountDocument2 paginiAgrani Bank LTD.: Statement of AccountBeximco Computers LTDÎncă nu există evaluări

- Increased Decreased: Sample: Cash in Bank Account Was DebitedDocument3 paginiIncreased Decreased: Sample: Cash in Bank Account Was DebitedAtty Cpa100% (2)

- Bill Hayton - Vietnam - Rising Dragon-Yale University Press (2010)Document273 paginiBill Hayton - Vietnam - Rising Dragon-Yale University Press (2010)Toan Tran100% (1)

- PayrollDocument3 paginiPayrolldesiree joy corpuz100% (1)

- How Can Corruption Influence The Work Practice?Document5 paginiHow Can Corruption Influence The Work Practice?Stacy LieutierÎncă nu există evaluări

- AKD - Good Day Service CompanyDocument9 paginiAKD - Good Day Service CompanyPuspita SariÎncă nu există evaluări

- How To Create A Pitch Deck For InvestorsDocument2 paginiHow To Create A Pitch Deck For InvestorsRoselyn MatienzoÎncă nu există evaluări

- RFB ReviewerDocument99 paginiRFB ReviewerAmpy SasutonaÎncă nu există evaluări

- Muskswap Whitepaper.81c7c978Document19 paginiMuskswap Whitepaper.81c7c978Afif KunÎncă nu există evaluări

- F23 Week 07 OPER8340 LectureDocument28 paginiF23 Week 07 OPER8340 LectureMurtuza SajidÎncă nu există evaluări

- Money: Nonfiction Reading TestDocument4 paginiMoney: Nonfiction Reading Testyollana riztyÎncă nu există evaluări

- Identifying Entrepreneurial Opportunities - PPTDocument10 paginiIdentifying Entrepreneurial Opportunities - PPTShabtab QuaiserÎncă nu există evaluări

- As Per Request 30 Days: QuotationDocument2 paginiAs Per Request 30 Days: QuotationAdmin SAF PrintersÎncă nu există evaluări

- Kogta Financial (India) LTDDocument3 paginiKogta Financial (India) LTDAnandÎncă nu există evaluări

- Genting Malaysia BerhadDocument13 paginiGenting Malaysia BerhadNur Athirah Binti Mahdir100% (1)

- Accounting For Merchandising Operations: Pertemuan 7Document16 paginiAccounting For Merchandising Operations: Pertemuan 7Herry ArsevenÎncă nu există evaluări

- The Emergence of Angel Investment Networks in Southeast Asia Report I A Good Practice Guide To Effective Angel InvestingDocument58 paginiThe Emergence of Angel Investment Networks in Southeast Asia Report I A Good Practice Guide To Effective Angel InvestingRick WongÎncă nu există evaluări

- AT6013-Unit IIDocument17 paginiAT6013-Unit IIKarthik SRS0% (1)

- Entrep Q2 SLM Lesson-1Document12 paginiEntrep Q2 SLM Lesson-1akiqt68Încă nu există evaluări

- Uttar Pradesh Power Corporation Ltd. - PAYMENTDocument1 paginăUttar Pradesh Power Corporation Ltd. - PAYMENTRAkeshÎncă nu există evaluări

- Receipt From STC Pay: Transaction ID: 55038609 Amount 388.87 BHD MTCN 9449703971Document1 paginăReceipt From STC Pay: Transaction ID: 55038609 Amount 388.87 BHD MTCN 9449703971Imran AliÎncă nu există evaluări

- D) Both B and C: Balance of Payments Total Weightage-6 MarksDocument9 paginiD) Both B and C: Balance of Payments Total Weightage-6 MarksShreya PushkarnaÎncă nu există evaluări