S-ar putea să vă placă și

- IC-532III Komori ManualDocument408 paginiIC-532III Komori ManualHuy Nguyen Q100% (1)

- Intecont Tersus Weighfeeder: Instruction ManualDocument176 paginiIntecont Tersus Weighfeeder: Instruction ManualJuan Roa100% (3)

- PPM 300 Picus Manual 4189341080 UkDocument127 paginiPPM 300 Picus Manual 4189341080 UkЖора СупрунюкÎncă nu există evaluări

- Solutions Manual: Introducing Corporate Finance 2eDocument9 paginiSolutions Manual: Introducing Corporate Finance 2eMane Scal JayÎncă nu există evaluări

- NADCAP - Pyrometry Guide 20 Nov 12Document51 paginiNADCAP - Pyrometry Guide 20 Nov 12Renato Fernandes100% (1)

- Tms ScriptDocument24 paginiTms ScriptNidal Kourbage100% (1)

- Genesys CSTA Troubleshooting GuideDocument34 paginiGenesys CSTA Troubleshooting GuideHassan DaoudÎncă nu există evaluări

- Towed-System Operators Manual V1.1.0Document69 paginiTowed-System Operators Manual V1.1.0Nur FatmalaÎncă nu există evaluări

- Intecont Tersus - MulticorDocument182 paginiIntecont Tersus - Multicorramprakashpatel100% (2)

- Oracle Banking Sales and PreSalesDocument12 paginiOracle Banking Sales and PreSalesSeboeng MashilangoakoÎncă nu există evaluări

- ComConf User EN V2 25Document160 paginiComConf User EN V2 25JOEKESÎncă nu există evaluări

- Manual UsuarioDocument22 paginiManual Usuariowilliam rojas mendozaÎncă nu există evaluări

- Agriculture Rural and Urban Development Sector Report 1Document103 paginiAgriculture Rural and Urban Development Sector Report 1KyteÎncă nu există evaluări

- 04 Plug-And-Produce Adaptable Facories en 2017Document68 pagini04 Plug-And-Produce Adaptable Facories en 2017Luis GarcíaÎncă nu există evaluări

- Itera Integrated Command Control and Communication: Operations GuideDocument232 paginiItera Integrated Command Control and Communication: Operations Guidefelius21811Încă nu există evaluări

- Vsphere5 Vcops InterviewDocument38 paginiVsphere5 Vcops InterviewashokkumarmduÎncă nu există evaluări

- Alcatel 4059 Attendant ConsoleDocument102 paginiAlcatel 4059 Attendant ConsoleKeiber PeñaÎncă nu există evaluări

- Rehearsal Questions Taw10 Taw12Document15 paginiRehearsal Questions Taw10 Taw12Carlos MarioÎncă nu există evaluări

- OCPI 2.2 d2Document186 paginiOCPI 2.2 d2jaimin patelÎncă nu există evaluări

- PDL2 Language Programming Manual PDFDocument582 paginiPDL2 Language Programming Manual PDFgapam_2Încă nu există evaluări

- ABB Drives: Application Guide Adaptive ProgramDocument44 paginiABB Drives: Application Guide Adaptive Programhartman_mdÎncă nu există evaluări

- Basic 52 ManualDocument220 paginiBasic 52 ManualziopiriÎncă nu există evaluări

- DVOP User ManualDocument210 paginiDVOP User ManualJim HerwigÎncă nu există evaluări

- PDF Managing The Audit Function 3rd Edition John Wiley Amp Sons CompressDocument274 paginiPDF Managing The Audit Function 3rd Edition John Wiley Amp Sons CompressArif Gunabar FatahillahÎncă nu există evaluări

- Bvh2464gb Instruction Manual IntecontDocument166 paginiBvh2464gb Instruction Manual IntecontSaeed Ahmad ChandioÎncă nu există evaluări

- DynaLift 3 6 User Guide A4Document53 paginiDynaLift 3 6 User Guide A4Quy HoangÎncă nu există evaluări

- Scarlett Solo 4th Gen User Guide V3-Pdf-EnDocument37 paginiScarlett Solo 4th Gen User Guide V3-Pdf-EnJuan ValenciaÎncă nu există evaluări

- Staruml Sample:Ucs: Usecase Specification DocumentDocument16 paginiStaruml Sample:Ucs: Usecase Specification Documentandres cÎncă nu există evaluări

- 4.5.1.0 Config Tool II ManualDocument82 pagini4.5.1.0 Config Tool II ManualJohn Jairo MochaÎncă nu există evaluări

- OCPP-2.0.1 Part2 Specification Edition2Document481 paginiOCPP-2.0.1 Part2 Specification Edition2FabianoÎncă nu există evaluări

- Fluent Udf Training 2 - CompressDocument39 paginiFluent Udf Training 2 - CompressRafik BouakkazÎncă nu există evaluări

- Apache Unomi 1.X - DocumentationDocument53 paginiApache Unomi 1.X - Documentationkuldeep singhÎncă nu există evaluări

- Spare Parts CatalogueDocument708 paginiSpare Parts Cataloguepperic_51Încă nu există evaluări

- Manual Intecont Tersus PDFDocument176 paginiManual Intecont Tersus PDFDouglas Souza100% (1)

- Beam BookDocument218 paginiBeam BookLuca Selva CampobassoÎncă nu există evaluări

- Intecont Tersus - SFFDocument162 paginiIntecont Tersus - SFFansar100% (1)

- R-J3 IO LINK Inetrface Operator ManualDocument58 paginiR-J3 IO LINK Inetrface Operator ManualPiotrÎncă nu există evaluări

- Mispa I2 User ManualDocument43 paginiMispa I2 User ManualJosef GrapesÎncă nu există evaluări

- # Basics of ProgrammingDocument76 pagini# Basics of ProgrammingPrajik ShresthaÎncă nu există evaluări

- Fleet Maintenance Pro 11Document68 paginiFleet Maintenance Pro 11Islam ShoukryÎncă nu există evaluări

- Fundamentals of Computer StudiesDocument60 paginiFundamentals of Computer StudiesADEBISI JELEEL ADEKUNLEÎncă nu există evaluări

- Intecont - Tersus Operating ManualDocument164 paginiIntecont - Tersus Operating ManualNarasimha NaruÎncă nu există evaluări

- Reactive SpringDocument421 paginiReactive SpringfranceteÎncă nu există evaluări

- Lmix3 000 Ma eDocument20 paginiLmix3 000 Ma eruperto sapertoÎncă nu există evaluări

- UserGuide OMNet++Document107 paginiUserGuide OMNet++duytanhyvn123Încă nu există evaluări

- Final WKU Reviewed Industrial ProjectDocument99 paginiFinal WKU Reviewed Industrial ProjectKidist AsefaÎncă nu există evaluări

- O9400S-V10-M No-BrandDocument259 paginiO9400S-V10-M No-Brandnguyenbaviet89Încă nu există evaluări

- Work InstructionsDocument72 paginiWork InstructionsErik VeraÎncă nu există evaluări

- Network Management Application Release Version: 2Document54 paginiNetwork Management Application Release Version: 2Dewa PerangÎncă nu există evaluări

- Issaf0 2 1ADocument462 paginiIssaf0 2 1AJeri BlackÎncă nu există evaluări

- Deliverable 1 2 Report On Global AnalysiDocument126 paginiDeliverable 1 2 Report On Global AnalysiStefan StojanovÎncă nu există evaluări

- Infinity Stand-Alone Programmable Engine Management System Full ManualDocument403 paginiInfinity Stand-Alone Programmable Engine Management System Full ManualTeodor AynadzhievÎncă nu există evaluări

- 睿能全电脑普通袜机使用说明书10寸屏 英文版Document45 pagini睿能全电脑普通袜机使用说明书10寸屏 英文版Christian CaballeroÎncă nu există evaluări

- Carrier Supra-St-Operator-EnglishDocument16 paginiCarrier Supra-St-Operator-Englishcraig LattanziÎncă nu există evaluări

- UM-30201120-ENG - VX120+ FEB - 2020 - Rev3.0.1Document228 paginiUM-30201120-ENG - VX120+ FEB - 2020 - Rev3.0.1Joshua Rodas RocaÎncă nu există evaluări

- Frontier AnalystWorkbook - 4Document39 paginiFrontier AnalystWorkbook - 4Leidy BernalÎncă nu există evaluări

- Tms ScriptDocument24 paginiTms Scriptdavid.martim8612Încă nu există evaluări

- Staruml Sample:Ucs: Usecase Specification DocumentDocument18 paginiStaruml Sample:Ucs: Usecase Specification DocumentMartha SalinasÎncă nu există evaluări

- Tib Designer PalettesDocument280 paginiTib Designer PalettesbajjurianÎncă nu există evaluări

- PDL2 Language Programming ManualDocument582 paginiPDL2 Language Programming Manualuriahp76100% (4)

- The Forensic Documentation Sourcebook: The Complete Paperwork Resource for Forensic Mental Health PracticeDe la EverandThe Forensic Documentation Sourcebook: The Complete Paperwork Resource for Forensic Mental Health PracticeEvaluare: 1 din 5 stele1/5 (1)

- Teardowns: Learn How Electronics Work by Taking Them ApartDe la EverandTeardowns: Learn How Electronics Work by Taking Them ApartÎncă nu există evaluări

- Dwnload Full Essentials of Corporate Finance 8th Edition Ross Test Bank PDFDocument35 paginiDwnload Full Essentials of Corporate Finance 8th Edition Ross Test Bank PDFoutlying.pedantry.85yc100% (9)

- If The Lease Were NonrenewableDocument2 paginiIf The Lease Were NonrenewableChris Tian FlorendoÎncă nu există evaluări

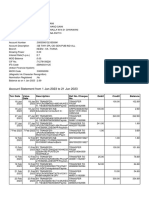

- Account Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument6 paginiAccount Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceKumar SunilÎncă nu există evaluări

- Cbroa News December 2020 2 PDFDocument37 paginiCbroa News December 2020 2 PDFVijay IyerÎncă nu există evaluări

- G.O.MS - No. 218Document5 paginiG.O.MS - No. 218younusbasha143Încă nu există evaluări

- Approaches To International Compensation NWDocument7 paginiApproaches To International Compensation NWazaruddin_mhmd1988Încă nu există evaluări

- Chapter 01Document10 paginiChapter 01ShantamÎncă nu există evaluări

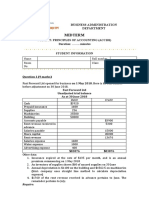

- Midterm: Hoa Lac Subject: Principles of Accounting (Acc101) Duration: .. Minutes Student InformationDocument2 paginiMidterm: Hoa Lac Subject: Principles of Accounting (Acc101) Duration: .. Minutes Student InformationNguyen Ngoc Minh Chau (K15 HL)Încă nu există evaluări

- AC - IntAcctg1 Quiz 04 With AnswersDocument2 paginiAC - IntAcctg1 Quiz 04 With AnswersSherri Bonquin100% (1)

- Bank Account Creation - S4HANA 1605 OP HDBDocument10 paginiBank Account Creation - S4HANA 1605 OP HDBRishikeshGuttigraharamÎncă nu există evaluări

- Monthly Banking/ Financial/ Economic Awareness SagaDocument48 paginiMonthly Banking/ Financial/ Economic Awareness SagaSunday MondayÎncă nu există evaluări

- #Pvofguaranteedpaymentof10,000In5Years: PV PVDocument7 pagini#Pvofguaranteedpaymentof10,000In5Years: PV PVL.E.O.ZÎncă nu există evaluări

- Ar 2020 BTPN Eng 14 AprilDocument612 paginiAr 2020 BTPN Eng 14 AprilklieindwrÎncă nu există evaluări

- Impact Assessment TemplateDocument3 paginiImpact Assessment Templatezio_nanoÎncă nu există evaluări

- Entrepreneurship and Start-Ups 03600201: Lecturer-Applied Science, Diploma StudyDocument85 paginiEntrepreneurship and Start-Ups 03600201: Lecturer-Applied Science, Diploma StudySMIT CHRISTIANÎncă nu există evaluări

- The Impact of Sustainability (Environmental, Social, and Governance) Disclosure and Board Diversity On Firm Value - The Moderating Role of Industry SensitivityDocument16 paginiThe Impact of Sustainability (Environmental, Social, and Governance) Disclosure and Board Diversity On Firm Value - The Moderating Role of Industry SensitivityHENI YUSNITAÎncă nu există evaluări

- Final PPT Adr-GdrDocument71 paginiFinal PPT Adr-Gdr24_anuÎncă nu există evaluări

- Mergeracquisitionwithcasestudy PPTPDFDocument45 paginiMergeracquisitionwithcasestudy PPTPDFMandip LuitelÎncă nu există evaluări

- Seminar Presentation ON Cost of CapitalDocument17 paginiSeminar Presentation ON Cost of CapitalViswajitÎncă nu există evaluări

- Birth Date: Birth Date:: Mirage Hatchback at GLXDocument1 paginăBirth Date: Birth Date:: Mirage Hatchback at GLXLerma LandiÎncă nu există evaluări

- CFPB List Consumer Reporting AgenciesDocument26 paginiCFPB List Consumer Reporting Agenciesrodney80% (5)

- Gurpreet Case StudyDocument3 paginiGurpreet Case StudyAditya BohraÎncă nu există evaluări

- Education Loans by Commercial Banks in IndiaDocument164 paginiEducation Loans by Commercial Banks in IndiaAnand Sharma100% (1)

- Stock Swap Transaction - Ratio of Exchange & Effect On EPS: Acquiring Company Target CompanyDocument3 paginiStock Swap Transaction - Ratio of Exchange & Effect On EPS: Acquiring Company Target Companypriyal patelÎncă nu există evaluări

- Audit 2 - Concept Map For InvestmentsDocument4 paginiAudit 2 - Concept Map For InvestmentsPrecious Recede100% (1)

- Konkan RailwayDocument20 paginiKonkan Railwayashutosh1202Încă nu există evaluări

- Solved Karrie Is A Golf Pro and After She Paid TaxesDocument1 paginăSolved Karrie Is A Golf Pro and After She Paid TaxesM Bilal SaleemÎncă nu există evaluări

- The Japanese Financial SystemDocument1 paginăThe Japanese Financial SystemSalil AggarwalÎncă nu există evaluări