S-ar putea să vă placă și

- How To Apply For A Homestead ExemptionDocument6 paginiHow To Apply For A Homestead ExemptionO'Connor AssociateÎncă nu există evaluări

- Why O'Connor For Property Tax Reduction?Document7 paginiWhy O'Connor For Property Tax Reduction?O'Connor AssociateÎncă nu există evaluări

- Top 3 Methods of Valuing Personal PropertyDocument7 paginiTop 3 Methods of Valuing Personal PropertyO'Connor AssociateÎncă nu există evaluări

- Tax Benefits For Home OwnersDocument7 paginiTax Benefits For Home OwnersO'Connor AssociateÎncă nu există evaluări

- Steps To Protest in Harris CountyDocument7 paginiSteps To Protest in Harris CountyO'Connor AssociateÎncă nu există evaluări

- Wisconsin Municipal AssessorsDocument48 paginiWisconsin Municipal AssessorsO'Connor AssociateÎncă nu există evaluări

- The IRS Guidelines For Non-Load Bearing WallsDocument5 paginiThe IRS Guidelines For Non-Load Bearing WallsO'Connor AssociateÎncă nu există evaluări

- PRESENTATION - ERE - Tactics For Investors To Drive ROIDocument7 paginiPRESENTATION - ERE - Tactics For Investors To Drive ROIO'Connor AssociateÎncă nu există evaluări

- House Flipping - A New Way of IncomeDocument6 paginiHouse Flipping - A New Way of IncomeO'Connor AssociateÎncă nu există evaluări

- How Can Cost Segregation Help Minimize Your Tax BurdenDocument6 paginiHow Can Cost Segregation Help Minimize Your Tax BurdenO'Connor AssociateÎncă nu există evaluări

- 3 Ways To Reduce Your Commercial Property Taxes With Cost SegregationDocument7 pagini3 Ways To Reduce Your Commercial Property Taxes With Cost SegregationO'Connor AssociateÎncă nu există evaluări

- PRESENTATION - OCA - The Thinning Line of Rental Collection in April - 2020Document6 paginiPRESENTATION - OCA - The Thinning Line of Rental Collection in April - 2020O'Connor AssociateÎncă nu există evaluări

- Hcad Business Personal Property FaqDocument2 paginiHcad Business Personal Property FaqO'Connor AssociateÎncă nu există evaluări

- 25+ Reasons You SHOULD Protest Your HIGH PROPERTY TAXESDocument8 pagini25+ Reasons You SHOULD Protest Your HIGH PROPERTY TAXESO'Connor AssociateÎncă nu există evaluări

- Property Assessment Appeal To The County Board of EqualizationDocument4 paginiProperty Assessment Appeal To The County Board of EqualizationO'Connor AssociateÎncă nu există evaluări

- Cap Rate Rate ReportDocument207 paginiCap Rate Rate ReportO'Connor Associate0% (1)

- Tax DeferralDocument1 paginăTax DeferralO'Connor AssociateÎncă nu există evaluări

- Hcad Business Personal Property FaqDocument2 paginiHcad Business Personal Property FaqO'Connor AssociateÎncă nu există evaluări

- Texas Real Estate InspectorDocument25 paginiTexas Real Estate InspectorO'Connor AssociateÎncă nu există evaluări

- Commercial Real Estate International Business TrendsDocument21 paginiCommercial Real Estate International Business TrendsNational Association of REALTORS®100% (2)

- Dallascad - Propertytaxoverview2017Document30 paginiDallascad - Propertytaxoverview2017O'Connor AssociateÎncă nu există evaluări

- GeorgiaCertificationProgram2017 2018Document2 paginiGeorgiaCertificationProgram2017 2018O'Connor AssociateÎncă nu există evaluări

- Dallas Central Appraisal District 2017 2018Document30 paginiDallas Central Appraisal District 2017 2018O'Connor AssociateÎncă nu există evaluări

- Lincoln Institute of Land Policy's Comparison of 2016 Property TaxesDocument108 paginiLincoln Institute of Land Policy's Comparison of 2016 Property TaxescrainsnewyorkÎncă nu există evaluări

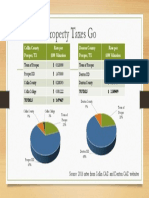

- Where The Property Taxes GoDocument1 paginăWhere The Property Taxes GoO'Connor AssociateÎncă nu există evaluări

- Montgomery County Exemption AnalysisDocument19 paginiMontgomery County Exemption AnalysisO'Connor AssociateÎncă nu există evaluări

- Austin Property Taxpayer Remedies 2017Document1 paginăAustin Property Taxpayer Remedies 2017O'Connor AssociateÎncă nu există evaluări

- Williamson Cad 2017 Rendition General InformationDocument2 paginiWilliamson Cad 2017 Rendition General InformationO'Connor AssociateÎncă nu există evaluări

- 2016 Annual Report TravisCADDocument41 pagini2016 Annual Report TravisCADO'Connor AssociateÎncă nu există evaluări

- W C A D: Ise Ounty Ppraisal IstrictDocument43 paginiW C A D: Ise Ounty Ppraisal IstrictO'Connor AssociateÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Clarifies On News Item (Company Update)Document3 paginiClarifies On News Item (Company Update)Shyam SunderÎncă nu există evaluări

- Sample Question AnswerDocument57 paginiSample Question Answerসজীব বসুÎncă nu există evaluări

- Notary Public : R State of California)Document5 paginiNotary Public : R State of California)Chapter 11 DocketsÎncă nu există evaluări

- Midterm Review - Key ConceptsDocument10 paginiMidterm Review - Key ConceptsGurpreetÎncă nu există evaluări

- Earnings Per ShareDocument15 paginiEarnings Per ShareMuhammad SajidÎncă nu există evaluări

- DBQ ManagementDocument3 paginiDBQ Managementrahul9801Încă nu există evaluări

- QUIZ Week 1Document2 paginiQUIZ Week 1hopefuldonorÎncă nu există evaluări

- Topic 6 - Concepts of National Income (Week5)Document52 paginiTopic 6 - Concepts of National Income (Week5)Wei SongÎncă nu există evaluări

- Case Study: Buffett Invests in Nebraska Furniture MartDocument8 paginiCase Study: Buffett Invests in Nebraska Furniture MartceojiÎncă nu există evaluări

- SindzaBG - N1 - Represented by Stefan TzvetkovDocument18 paginiSindzaBG - N1 - Represented by Stefan Tzvetkovdusandjordjevic011Încă nu există evaluări

- Final accounts for year ending 1992Document50 paginiFinal accounts for year ending 1992kalyanikamineniÎncă nu există evaluări

- CEILLI Trial Ques EnglishDocument15 paginiCEILLI Trial Ques EnglishUSCÎncă nu există evaluări

- Project GuideDocument22 paginiProject GuideMr DamphaÎncă nu există evaluări

- Mock Reviewer in Management AccountingDocument6 paginiMock Reviewer in Management AccountingJA VicenteÎncă nu există evaluări

- Strategic Management at Infosys (Business Strategy)Document19 paginiStrategic Management at Infosys (Business Strategy)Madhusudan22Încă nu există evaluări

- FM-capital Structure AnalysisDocument19 paginiFM-capital Structure AnalysisNikhil ReddyÎncă nu există evaluări

- f9 02 The Financial Management EnvironmentDocument27 paginif9 02 The Financial Management EnvironmentGAURAVÎncă nu există evaluări

- Tor PMSC UndipDocument22 paginiTor PMSC UndipSigit Nur WaskitoÎncă nu există evaluări

- SemesterDocument40 paginiSemestergokulsaravananÎncă nu există evaluări

- IFFCODocument1 paginăIFFCONapoleon DasÎncă nu există evaluări

- Book Invoice PDFDocument1 paginăBook Invoice PDFnoamaanÎncă nu există evaluări

- Name: Kimberly Anne P. Caballes Year and CourseDocument12 paginiName: Kimberly Anne P. Caballes Year and CourseKimberly Anne CaballesÎncă nu există evaluări

- Unintended Consequences: by John MauldinDocument11 paginiUnintended Consequences: by John Mauldinrichardck61Încă nu există evaluări

- Court rules on deductions from spousal support arrearsDocument1 paginăCourt rules on deductions from spousal support arrearsNicole CruzÎncă nu există evaluări

- Turn Albany UpsideDown 10-06-10 2 3Document4 paginiTurn Albany UpsideDown 10-06-10 2 3Elizabeth BenjaminÎncă nu există evaluări

- Chapter 12 Exercise SolutionDocument95 paginiChapter 12 Exercise SolutionKai FaggornÎncă nu există evaluări

- Ratio Analysis of Gokaldas Exports LTDDocument21 paginiRatio Analysis of Gokaldas Exports LTDGreeshmaÎncă nu există evaluări

- 7 Mega Trades That Could Hand You A 7 Figure PayouDocument30 pagini7 Mega Trades That Could Hand You A 7 Figure Payouyeahitsme604Încă nu există evaluări

- Company Limited: Claim For Reimbursement of Motor Car Running ExpensesDocument1 paginăCompany Limited: Claim For Reimbursement of Motor Car Running ExpensesRahul RawatÎncă nu există evaluări

- Event Contract - TemplateDocument17 paginiEvent Contract - Templatenoel damotÎncă nu există evaluări