S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- AWS Certified Cloud Practitioner Practice Tests Dumps 2021Document10 paginiAWS Certified Cloud Practitioner Practice Tests Dumps 2021Aaron Clifton100% (1)

- Prestige Telephone Company (Solutions)Document4 paginiPrestige Telephone Company (Solutions)Joseph Loyola71% (7)

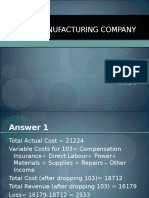

- Hilton Manufacturing Company 1201326783827489 2Document6 paginiHilton Manufacturing Company 1201326783827489 2julijulijulioÎncă nu există evaluări

- Prestige Telephone Company (Solutions)Document4 paginiPrestige Telephone Company (Solutions)Joseph Loyola71% (7)

- Prestige Telephone Company (Solutions)Document4 paginiPrestige Telephone Company (Solutions)Joseph Loyola71% (7)

- December + Yearly ReviewDocument2 paginiDecember + Yearly ReviewNick FabrioÎncă nu există evaluări

- In-Film BrandingDocument27 paginiIn-Film BrandingSantosh Parachuri0% (1)

- Civil Procedure Flash CardsDocument48 paginiCivil Procedure Flash CardsNick Ashjian100% (1)

- Train Control Basics-1Document1 paginăTrain Control Basics-1uqui_5Încă nu există evaluări

- Marriott CorporationDocument25 paginiMarriott Corporationuqui_50% (1)

- Pinkerton (A) PDFDocument7 paginiPinkerton (A) PDFuqui_5Încă nu există evaluări

- Lie, E. and H. Lie, 2002, Multiples Used To Estimate Corporate Value, Financial Analyst Journal 58, 44 - 54Document11 paginiLie, E. and H. Lie, 2002, Multiples Used To Estimate Corporate Value, Financial Analyst Journal 58, 44 - 54uqui_5Încă nu există evaluări

- Doing Business 2017 EcuadorDocument112 paginiDoing Business 2017 Ecuadoruqui_5Încă nu există evaluări

- Pinkerton (A)Document7 paginiPinkerton (A)uqui_5Încă nu există evaluări

- Hilton Manufacturing CompanyDocument6 paginiHilton Manufacturing CompanyShreenivas KVÎncă nu există evaluări

- Hilton 1Document4 paginiHilton 1uqui_5Încă nu există evaluări

- 50 TipsDocument2 pagini50 Tipsuqui_5Încă nu există evaluări

- Lesson 2. WHAT IS AGROTECHNOPRENEURSHIPDocument23 paginiLesson 2. WHAT IS AGROTECHNOPRENEURSHIPRhea Jane DugadugaÎncă nu există evaluări

- 13 Ways The Coronavirus Pandemic Could Forever Change The Way We WorkDocument20 pagini13 Ways The Coronavirus Pandemic Could Forever Change The Way We WorkAbidullahÎncă nu există evaluări

- Accounting QuestionsDocument16 paginiAccounting QuestionsPrachi ChananaÎncă nu există evaluări

- Teaching Strategies, Styles and Qualities of ADocument6 paginiTeaching Strategies, Styles and Qualities of AjixÎncă nu există evaluări

- Lateral Pile Paper - Rev01Document6 paginiLateral Pile Paper - Rev01YibinGongÎncă nu există evaluări

- HVCB 0120Document70 paginiHVCB 0120adeeÎncă nu există evaluări

- Lapid V CADocument11 paginiLapid V CAChami YashaÎncă nu există evaluări

- Murugan Temple of North America: Ahkpuf F Gankd - FZGJP JizDocument8 paginiMurugan Temple of North America: Ahkpuf F Gankd - FZGJP JizOurMuruganTempleÎncă nu există evaluări

- Assy Conveyor 4 MTR (2 Unit) : Part Number Description Qty. Item NODocument11 paginiAssy Conveyor 4 MTR (2 Unit) : Part Number Description Qty. Item NOFaiz Qilafa ZimamÎncă nu există evaluări

- Synchronization Checklist PDFDocument8 paginiSynchronization Checklist PDFAdhyartha KerafÎncă nu există evaluări

- LivePerson Chat ReportsDocument23 paginiLivePerson Chat ReportsEdenEtfÎncă nu există evaluări

- Appendix: Dhuts-Phase Ii Dhaka Urban Transport Network Development Study-Phase IIDocument20 paginiAppendix: Dhuts-Phase Ii Dhaka Urban Transport Network Development Study-Phase IIhhbeckÎncă nu există evaluări

- 2023 - Kadam - Review On Nanoparticles - SocioeconomicalDocument9 pagini2023 - Kadam - Review On Nanoparticles - Socioeconomicaldba1992Încă nu există evaluări

- QuickRide LogcatDocument53 paginiQuickRide LogcatAthira OSÎncă nu există evaluări

- Fly The Maddog X User Manual MSFS 2020Document15 paginiFly The Maddog X User Manual MSFS 2020KING OF NOOBSÎncă nu există evaluări

- RBA Catalog Maltby GBR Aug 16 2023 NL NLDocument131 paginiRBA Catalog Maltby GBR Aug 16 2023 NL NLKelvin FaneyteÎncă nu există evaluări

- Yesenia Acc SjournalsDocument7 paginiYesenia Acc SjournalsFileon ChiacÎncă nu există evaluări

- Subject: Industrial Marketing Topic/Case Name: Electrical Equipment LTDDocument4 paginiSubject: Industrial Marketing Topic/Case Name: Electrical Equipment LTDRucha ShirudkarÎncă nu există evaluări

- Due Friday, February 21, 2014 by 5:00 P.M. To The AE312 MailboxDocument3 paginiDue Friday, February 21, 2014 by 5:00 P.M. To The AE312 MailboxankstamanÎncă nu există evaluări

- Integrated CircuitsDocument13 paginiIntegrated CircuitsAbdelheq SaidouneÎncă nu există evaluări

- Cima E1 2019 Notes Managing Finance in A Digital WorldDocument91 paginiCima E1 2019 Notes Managing Finance in A Digital Worldumarfarooque869Încă nu există evaluări

- Corporation Law Syllabus With Assignment of CasesDocument4 paginiCorporation Law Syllabus With Assignment of CasesMarilou AgustinÎncă nu există evaluări

- Oracle Flash Storage System CLI ReferenceDocument454 paginiOracle Flash Storage System CLI Referencebsduser07Încă nu există evaluări

- AAU Karate Handbook: "Sports For All, Forever"Document58 paginiAAU Karate Handbook: "Sports For All, Forever"jeffrey_trzaskusÎncă nu există evaluări

- Mystique-1 Shark Bay Block Diagram: Project Code: 91.4LY01.001 PCB (Raw Card) : 12298-2Document80 paginiMystique-1 Shark Bay Block Diagram: Project Code: 91.4LY01.001 PCB (Raw Card) : 12298-2Ion PetruscaÎncă nu există evaluări

- Project 2 - Home InsuranceDocument15 paginiProject 2 - Home InsuranceNaveen KumarÎncă nu există evaluări