S-ar putea să vă placă și

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- ARTO Bank Report: Development, Shareholders, DividendsDocument3 paginiARTO Bank Report: Development, Shareholders, DividendsAfterneathÎncă nu există evaluări

- Accounting PrinciplesDocument36 paginiAccounting PrinciplesEshetieÎncă nu există evaluări

- Radha Sridhar - 2 - 2019-2020Document2 paginiRadha Sridhar - 2 - 2019-2020Radha SridharÎncă nu există evaluări

- ASA FPC Resource Book PDFDocument170 paginiASA FPC Resource Book PDFksm256Încă nu există evaluări

- PowerscreenDocument4 paginiPowerscreenMJ Cobb50% (2)

- Small Scale Industries Unit 3Document108 paginiSmall Scale Industries Unit 3Kismat SharmaÎncă nu există evaluări

- Managing Earnings Using Classification Shifting: Evidence From Quarterly Special ItemsDocument39 paginiManaging Earnings Using Classification Shifting: Evidence From Quarterly Special ItemsNovaz BestÎncă nu există evaluări

- Advacc Midterm AssignmentsDocument11 paginiAdvacc Midterm AssignmentsAccounting MaterialsÎncă nu există evaluări

- Multi-Level Marketing Firms Under Regulatory ScrutinyDocument37 paginiMulti-Level Marketing Firms Under Regulatory Scrutinylu_oshiro100% (1)

- Patent Infringement Damages - A Brief Summary - Articles - FinneganDocument14 paginiPatent Infringement Damages - A Brief Summary - Articles - FinneganneelgalaÎncă nu există evaluări

- TCS and Infosys - Financial AnalysisDocument10 paginiTCS and Infosys - Financial AnalysisGhritachi PaulÎncă nu există evaluări

- Master BudgetDocument32 paginiMaster BudgetKristelJaneDonaireBihag60% (5)

- Investor Presentation February 2016 (Company Update)Document42 paginiInvestor Presentation February 2016 (Company Update)Shyam SunderÎncă nu există evaluări

- PartnershipDocument330 paginiPartnershipAbby Sta Ana100% (2)

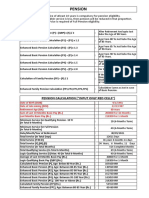

- Pension and Other Retirement BenifitsDocument8 paginiPension and Other Retirement BenifitsVikas GuptaÎncă nu există evaluări

- Garrison12ce PPT Ch04Document78 paginiGarrison12ce PPT Ch04snsahaÎncă nu există evaluări

- Case Study - Management Control - Texas Instruments and Hewlett - PackardDocument20 paginiCase Study - Management Control - Texas Instruments and Hewlett - PackardJed Estanislao80% (10)

- Pre-Feasibility Study on UPS and Stabilizer Assembling UnitDocument23 paginiPre-Feasibility Study on UPS and Stabilizer Assembling UnitRaza Un NabiÎncă nu există evaluări

- Working Capital ManagementDocument16 paginiWorking Capital ManagementjcshahÎncă nu există evaluări

- Accounting Chapter 2Document56 paginiAccounting Chapter 2hnhÎncă nu există evaluări

- Chapter No.40Document6 paginiChapter No.40Kamal SinghÎncă nu există evaluări

- Annual Report and Accounts 2020Document382 paginiAnnual Report and Accounts 2020EvgeniyÎncă nu există evaluări

- Bangladesh Income Tax RatesDocument5 paginiBangladesh Income Tax RatesaadonÎncă nu există evaluări

- 2023 Specimen Paper 3 Mark SchemeDocument14 pagini2023 Specimen Paper 3 Mark Schemewhumayun774Încă nu există evaluări

- Lembar Kerja UkkDocument46 paginiLembar Kerja UkkAmalia YuniarsihÎncă nu există evaluări

- A Great Valuation Play Where Commodity Business Is A Cash CowDocument29 paginiA Great Valuation Play Where Commodity Business Is A Cash Cowgullapalli123Încă nu există evaluări

- CREATE Act implementation guidelinesDocument51 paginiCREATE Act implementation guidelinesTreb LemÎncă nu există evaluări

- Constellation SoftwareDocument11 paginiConstellation SoftwaregalatimeÎncă nu există evaluări

- Basic Method For Making Economy Study NotesDocument3 paginiBasic Method For Making Economy Study NotesMichael DantogÎncă nu există evaluări