S-ar putea să vă placă și

- Topic:Implications of Fair Value Accounting: The Case of Fiji Sugar Corporation1.0 IntroductionDocument6 paginiTopic:Implications of Fair Value Accounting: The Case of Fiji Sugar Corporation1.0 IntroductionShazia MohammedÎncă nu există evaluări

- Topic: Implications of Fair Value Accounting: The Case of Fiji Sugar Corporation 1.0Document8 paginiTopic: Implications of Fair Value Accounting: The Case of Fiji Sugar Corporation 1.0ashmeeta_singh0% (1)

- Financial Reporting Quality Fair ValueDocument13 paginiFinancial Reporting Quality Fair ValueÁgnes SchwarczÎncă nu există evaluări

- Accounting For Financial Instruments Conceptual Paper: April 2008Document14 paginiAccounting For Financial Instruments Conceptual Paper: April 2008indahmuliasariÎncă nu există evaluări

- Review Na Sa Conceptual FrameworkDocument5 paginiReview Na Sa Conceptual FrameworkMARY ROSEÎncă nu există evaluări

- Jawaban Versi Indo Akm 2Document8 paginiJawaban Versi Indo Akm 2dindaÎncă nu există evaluări

- Case Study - 1Document5 paginiCase Study - 1Jordan BimandamaÎncă nu există evaluări

- Historical Costing Is An Important Element of Financial Bookkeeping For A CompanyDocument5 paginiHistorical Costing Is An Important Element of Financial Bookkeeping For A CompanyYolanda FosalaÎncă nu există evaluări

- AC420 Deprival Value EssayDocument4 paginiAC420 Deprival Value EssayBrian LiangÎncă nu există evaluări

- Fair Value AccountingDocument13 paginiFair Value AccountinghaarvendraraoÎncă nu există evaluări

- Historical Cost Accounting or Fair Value Accounting: A Historical PerspectiveDocument5 paginiHistorical Cost Accounting or Fair Value Accounting: A Historical PerspectiveanimecrushÎncă nu există evaluări

- Historical Harming Is An Main Part of Financial Accounting For A AssociationDocument2 paginiHistorical Harming Is An Main Part of Financial Accounting For A AssociationYolanda FosalaÎncă nu există evaluări

- Uts Teori AkuntansiDocument6 paginiUts Teori AkuntansiARYA AZHARI -Încă nu există evaluări

- Market Value Vs Historical CostDocument6 paginiMarket Value Vs Historical Costassime_hÎncă nu există evaluări

- Renew (Corporate ReportingDocument11 paginiRenew (Corporate ReportingBeng PutraÎncă nu există evaluări

- Measurement Theory and Cost AllocationDocument17 paginiMeasurement Theory and Cost AllocationYusuf RaharjaÎncă nu există evaluări

- CF Qualitative CharacteristicsDocument3 paginiCF Qualitative Characteristicspanda 1Încă nu există evaluări

- TA - Four Measurements of Accounting - Group 5Document10 paginiTA - Four Measurements of Accounting - Group 5Ayu Go to SchoolÎncă nu există evaluări

- Usefulness of AccountingDocument17 paginiUsefulness of AccountingMochamadMaarifÎncă nu există evaluări

- Accounting Concepts For The Actuary: by Ralph S. Blanchard III, FCAS, MAAADocument16 paginiAccounting Concepts For The Actuary: by Ralph S. Blanchard III, FCAS, MAAAvikvikkiÎncă nu există evaluări

- MeasurementDocument2 paginiMeasurementJolaica DiocolanoÎncă nu există evaluări

- Historical Cost ConceptDocument3 paginiHistorical Cost ConceptAfrina KarimÎncă nu există evaluări

- Fair Value Accounting ArticleDocument3 paginiFair Value Accounting ArticleVeena HingarhÎncă nu există evaluări

- Week 3 NotesDocument5 paginiWeek 3 Notestim.k.g.12Încă nu există evaluări

- Chapter 6: MEASUREMENT: Conceptual Framework in Financial ReportingDocument24 paginiChapter 6: MEASUREMENT: Conceptual Framework in Financial ReportingHarel LeeÎncă nu există evaluări

- Financial Reporting PDFDocument67 paginiFinancial Reporting PDFlukamasia93% (15)

- Fair Value Accounting For FinancialDocument4 paginiFair Value Accounting For FinancialAashie SkystÎncă nu există evaluări

- Advantages and Disadvantages of Historical Cost AccountingDocument3 paginiAdvantages and Disadvantages of Historical Cost AccountingBhaskar MallubhotlaÎncă nu există evaluări

- Af210 AssignmentDocument1 paginăAf210 AssignmentSagar SharmaÎncă nu există evaluări

- Financial Accounting AssignmentDocument6 paginiFinancial Accounting AssignmentSanjeevParajuliÎncă nu există evaluări

- Accounting Measurement SystemDocument7 paginiAccounting Measurement SystemDionysius Ivan Hertanto100% (1)

- Investment Valuation: Learn Proven Methods For Determining Asset Value And Taking The Right Investing DecisionsDe la EverandInvestment Valuation: Learn Proven Methods For Determining Asset Value And Taking The Right Investing DecisionsÎncă nu există evaluări

- Fair Value Xi WeiDocument5 paginiFair Value Xi Weiapi-415645328Încă nu există evaluări

- Tugas TA FrendDocument11 paginiTugas TA FrendFrendy YusufÎncă nu există evaluări

- VCM Module 7 - Tools Used in Asset-Based Valuation and Asset-Based Valuation MethodsDocument58 paginiVCM Module 7 - Tools Used in Asset-Based Valuation and Asset-Based Valuation MethodsLaurie Mae ToledoÎncă nu există evaluări

- Chapter 1 FUNDAMENTALS PRINCIPLES OF VALUATIONDocument52 paginiChapter 1 FUNDAMENTALS PRINCIPLES OF VALUATIONMs. VelÎncă nu există evaluări

- Qualitative Characteristics of Accounting InformationDocument24 paginiQualitative Characteristics of Accounting InformationWahyudi SyaputraÎncă nu există evaluări

- Principles of Accounting, Historical Cost & Current Cost ApproachesDocument2 paginiPrinciples of Accounting, Historical Cost & Current Cost ApproachesAthirah RosleeÎncă nu există evaluări

- Historical Cost Vs Fair Market ValueDocument4 paginiHistorical Cost Vs Fair Market Valueoliver smithÎncă nu există evaluări

- Principles-Based Accounting Standards: A Message From The Ceos of The International Audit NetworksDocument23 paginiPrinciples-Based Accounting Standards: A Message From The Ceos of The International Audit NetworksdeividtobonÎncă nu există evaluări

- Far210 Chap 2 Notes For Chapter 2Document11 paginiFar210 Chap 2 Notes For Chapter 2Nur ain Natasha ShaharudinÎncă nu există evaluări

- Session 4 Financial Reporting QualityDocument13 paginiSession 4 Financial Reporting QualityAntony ShillerÎncă nu există evaluări

- The Impact of IFRS On Value Relevance of AccountingDocument6 paginiThe Impact of IFRS On Value Relevance of AccountingSarah Yasmin Mat YasinÎncă nu există evaluări

- Topic 1 Practice QuestionsDocument12 paginiTopic 1 Practice QuestionsLena ZhengÎncă nu există evaluări

- Duke Fed Speech 9.14.09Document7 paginiDuke Fed Speech 9.14.09mrericwangÎncă nu există evaluări

- Accounting Theory - Summary Chapter 6Document10 paginiAccounting Theory - Summary Chapter 6Boby Kristanto ChandraÎncă nu există evaluări

- Contemporary Issues in Accounting: Solution ManualDocument17 paginiContemporary Issues in Accounting: Solution ManualKeiLiewÎncă nu există evaluări

- Answer 210Document6 paginiAnswer 210Hazel F.Încă nu există evaluări

- Lecture NotesDocument32 paginiLecture NotesRavinesh PrasadÎncă nu există evaluări

- AccountsDocument9 paginiAccountsSivaÎncă nu există evaluări

- Historical Vs Fair Value EssayDocument7 paginiHistorical Vs Fair Value EssayWarren C. CannonÎncă nu există evaluări

- Summary Enhancing Qualitative CharacteristicsDocument3 paginiSummary Enhancing Qualitative CharacteristicsCahyani PrastutiÎncă nu există evaluări

- Reliabiliity and AccuracyDocument6 paginiReliabiliity and AccuracyReiner PrayogaÎncă nu există evaluări

- 42-44 Standards & PracticesDocument2 pagini42-44 Standards & PracticesArif AhmedÎncă nu există evaluări

- Cash Flow Theory of Stock ValuationDocument29 paginiCash Flow Theory of Stock ValuationRANDAÎncă nu există evaluări

- Financial ReportingDocument7 paginiFinancial ReportingInnocent MollaÎncă nu există evaluări

- Solutions To Assigned Problems Chapters 1 and 2Document6 paginiSolutions To Assigned Problems Chapters 1 and 2meÎncă nu există evaluări

- Resume 11Document5 paginiResume 11MariaÎncă nu există evaluări

- MeasurementDocument3 paginiMeasurementSahin AydinÎncă nu există evaluări

- Financial ReportingDocument133 paginiFinancial ReportingClerry SamuelÎncă nu există evaluări

- Transfer - Advice - 2022-04-27T092000.818Document1 paginăTransfer - Advice - 2022-04-27T092000.818raini95Încă nu există evaluări

- Attn: Mr. Tan Hoe Him Ref: Contra Ramadhan Voucher With Outstanding BalanceDocument1 paginăAttn: Mr. Tan Hoe Him Ref: Contra Ramadhan Voucher With Outstanding Balanceraini95Încă nu există evaluări

- Transfer - Advice - 2022-04-27T092037.409Document1 paginăTransfer - Advice - 2022-04-27T092037.409raini95Încă nu există evaluări

- Slip Gaji - Sinar Suria GlobalDocument9 paginiSlip Gaji - Sinar Suria Globalraini95Încă nu există evaluări

- CasesmanegemntaccountingDocument171 paginiCasesmanegemntaccountingjose Martin100% (2)

- Facing Challenges Through Opportunities and StrategiesDocument2 paginiFacing Challenges Through Opportunities and Strategiesraini95Încă nu există evaluări

- Case Study - DelimaDocument6 paginiCase Study - Delimaraini95Încă nu există evaluări

- Dual Measurement and Financial Reporting System ExplainedDocument2 paginiDual Measurement and Financial Reporting System Explainedraini95Încă nu există evaluări

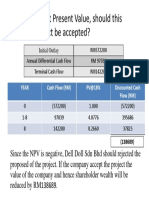

- C) Based On Net Present Value, Should This Capital Project Be Accepted?Document1 paginăC) Based On Net Present Value, Should This Capital Project Be Accepted?raini95Încă nu există evaluări

- MPERSvs MFRSDocument12 paginiMPERSvs MFRSraini95Încă nu există evaluări

- 17) True 18) True 19) False 20) FalseDocument2 pagini17) True 18) True 19) False 20) Falseraini95Încă nu există evaluări

- EthicsDocument8 paginiEthicsraini95Încă nu există evaluări

- Understanding Extroversion and Agreeableness: En Rashid's Personality TraitsDocument1 paginăUnderstanding Extroversion and Agreeableness: En Rashid's Personality Traitsraini95Încă nu există evaluări

- Questions-Assignment On CommunicationDocument3 paginiQuestions-Assignment On Communicationraini95Încă nu există evaluări

- ACRV 1023 Final Exams With Answers PDFDocument8 paginiACRV 1023 Final Exams With Answers PDFMary Grace Narag100% (1)

- Chapter 19 - Biological AssetsDocument40 paginiChapter 19 - Biological AssetsDidik DidiksterÎncă nu există evaluări

- Business Combinations Chapter 1Document16 paginiBusiness Combinations Chapter 1Alif NurjanahÎncă nu există evaluări

- The Objective of General Purpose Financial ReportingDocument86 paginiThe Objective of General Purpose Financial ReportingAlex liaoÎncă nu există evaluări

- MODULE 2 - Partnership AccountingDocument14 paginiMODULE 2 - Partnership AccountingEdison Salgado CastigadorÎncă nu există evaluări

- Apex Mining Co Inc - Conso AFS As of 12.13.14Document100 paginiApex Mining Co Inc - Conso AFS As of 12.13.14Ashley Ibe GuevarraÎncă nu există evaluări

- Investment in Equity SecuritiesDocument11 paginiInvestment in Equity SecuritiesJANISCHAJEAN RECTOÎncă nu există evaluări

- Annotated BB2023 A IAS02 PartA PDFDocument20 paginiAnnotated BB2023 A IAS02 PartA PDFKhutso MabalaÎncă nu există evaluări

- MOCK EXAMS CAF AUTUMN 2022 FINANCIAL ACCOUNTING AND REPORTING IDocument130 paginiMOCK EXAMS CAF AUTUMN 2022 FINANCIAL ACCOUNTING AND REPORTING IHadeed HafeezÎncă nu există evaluări

- Chapter 30 Impairment of AssetDocument15 paginiChapter 30 Impairment of AssetCrizel Dario0% (1)

- 31 August 2023 Purple Group Company AFSDocument53 pagini31 August 2023 Purple Group Company AFSmkhize.christian.21Încă nu există evaluări

- Advance Assignment FinalDocument18 paginiAdvance Assignment Finalaklilu shiferawÎncă nu există evaluări

- Quiz 2 - MidtermDocument9 paginiQuiz 2 - Midtermnatalie clyde matesÎncă nu există evaluări

- PSAK 50 & 55 Revisions on Financial InstrumentsDocument4 paginiPSAK 50 & 55 Revisions on Financial Instrumentsjmy'Încă nu există evaluări

- Nightmare On Wall StreetDocument304 paginiNightmare On Wall Streetbrown.mel337100% (5)

- Assignment On International Accounting StandardsDocument23 paginiAssignment On International Accounting StandardsIstiak HasanÎncă nu există evaluări

- Advanced Accounts MERGED May '18 To Nov '22 PYQDocument290 paginiAdvanced Accounts MERGED May '18 To Nov '22 PYQHanna GeorgeÎncă nu există evaluări

- Notes ReceivableDocument47 paginiNotes ReceivableAlexandria Ann FloresÎncă nu există evaluări

- Consolidated Accounts December 31 2011 For Web (Revised) PDFDocument93 paginiConsolidated Accounts December 31 2011 For Web (Revised) PDFElegant EmeraldÎncă nu există evaluări

- IFRS SOLVED QUESTIONSDocument15 paginiIFRS SOLVED QUESTIONSSharan ReddyÎncă nu există evaluări

- Deferred Tax Ias 12Document22 paginiDeferred Tax Ias 12Jawad Akbar KhanÎncă nu există evaluări

- Updated Pensions Training - Slides 05.03.18Document101 paginiUpdated Pensions Training - Slides 05.03.18archanaanuÎncă nu există evaluări

- PWC Intagible AssetDocument393 paginiPWC Intagible AssetEnggar J PrasetyaÎncă nu există evaluări

- Investments in Debt SecuritiesDocument34 paginiInvestments in Debt SecuritiesNobu NobuÎncă nu există evaluări

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument25 paginiAccounting Policies, Changes in Accounting Estimates and ErrorsAshish agrawalÎncă nu există evaluări

- Financial Reporting Disclosures for Consolidated and Separate StatementsDocument37 paginiFinancial Reporting Disclosures for Consolidated and Separate Statementsaman vermaÎncă nu există evaluări

- Soal AKL21bDocument5 paginiSoal AKL21bIzzatul kamilaÎncă nu există evaluări

- Philippine PIC Q&A on Accounting for Cancellation of Real Estate SalesDocument9 paginiPhilippine PIC Q&A on Accounting for Cancellation of Real Estate SalesKai SanchezÎncă nu există evaluări

- Afar 3Document2 paginiAfar 3Eric Kevin LecarosÎncă nu există evaluări

- PPL Cup EasyDocument6 paginiPPL Cup EasyRukia KuchikiÎncă nu există evaluări