S-ar putea să vă placă și

- Second Quarter Fiscal Update and Economic Statement: November 2012Document16 paginiSecond Quarter Fiscal Update and Economic Statement: November 2012pkGlobalÎncă nu există evaluări

- City of Fort St. John - Pandemic Effect On The Operating Budget, March 2020Document4 paginiCity of Fort St. John - Pandemic Effect On The Operating Budget, March 2020AlaskaHighwayNewsÎncă nu există evaluări

- The Amortization of Fixed Assets in Terms of Deferred TaxesDocument12 paginiThe Amortization of Fixed Assets in Terms of Deferred TaxesMessiÎncă nu există evaluări

- FinalDocument2 paginiFinalDebÎncă nu există evaluări

- Budget Analysis 09Document33 paginiBudget Analysis 09Vikash Kumar AgrawalÎncă nu există evaluări

- Fiscal PolicyDocument15 paginiFiscal PolicyRohit RohitÎncă nu există evaluări

- Ias 12,7 Ifrs 9Document10 paginiIas 12,7 Ifrs 9AssignemntÎncă nu există evaluări

- Executive Summary of New Bataan MunicipalityDocument5 paginiExecutive Summary of New Bataan MunicipalityJoergen Mae MicabaloÎncă nu există evaluări

- 2017 PBB AsDocument29 pagini2017 PBB AsDonkuro PuovarrÎncă nu există evaluări

- Shuttlers Metropolitan ReportDocument7 paginiShuttlers Metropolitan ReportAkinyemi SilasÎncă nu există evaluări

- 2021 Budget Plan Executive Summary: City of Akron, Ohio Dan Horrigan, MayorDocument8 pagini2021 Budget Plan Executive Summary: City of Akron, Ohio Dan Horrigan, MayorDougÎncă nu există evaluări

- Income Tax Reporting: DR Jacek Welc: Jacek - Welc@ue - Wroc.plDocument49 paginiIncome Tax Reporting: DR Jacek Welc: Jacek - Welc@ue - Wroc.plaÎncă nu există evaluări

- Notes To Financial Statements: 1. Agency Profile 2Document9 paginiNotes To Financial Statements: 1. Agency Profile 2Chito BarsabalÎncă nu există evaluări

- Deferred TaxDocument14 paginiDeferred Taxiftekharul alamÎncă nu există evaluări

- Finance Act Era Critical Evaluation 1 1Document22 paginiFinance Act Era Critical Evaluation 1 1Folawiyo AgbokeÎncă nu există evaluări

- Public Finance in Economics (Econ 3122) : The Theory of Taxation and Tax PolicyDocument46 paginiPublic Finance in Economics (Econ 3122) : The Theory of Taxation and Tax Policyabigael kebedeÎncă nu există evaluări

- Corporations Act 2001Document8 paginiCorporations Act 2001vicky singhÎncă nu există evaluări

- Fs - Aguilar Golden Harvest MPC 2020Document37 paginiFs - Aguilar Golden Harvest MPC 2020Ma Teresa B. CerezoÎncă nu există evaluări

- R1201SDocument3 paginiR1201SIv marÎncă nu există evaluări

- Budget of the Orenburg Region 2014-2017Document6 paginiBudget of the Orenburg Region 2014-2017Lolita IsakhanyanÎncă nu există evaluări

- PUBLIC FINANCE UNDERSTANDING MARKET FAILUREDocument6 paginiPUBLIC FINANCE UNDERSTANDING MARKET FAILUREanjudeshÎncă nu există evaluări

- Resource Collection Model of The GovernmentDocument18 paginiResource Collection Model of The GovernmentSarita BhandariÎncă nu există evaluări

- Module-Accounting For Income TaxDocument13 paginiModule-Accounting For Income TaxJohn Mark FernandoÎncă nu există evaluări

- Note 17. Collections and Refunds of Federal RevenueDocument3 paginiNote 17. Collections and Refunds of Federal RevenueLokiÎncă nu există evaluări

- Acc708 Lecture 1Document16 paginiAcc708 Lecture 1Emjes GianoÎncă nu există evaluări

- Annex 7Document17 paginiAnnex 7YasinÎncă nu există evaluări

- SM Report G3Document29 paginiSM Report G3SriSaraswathyÎncă nu există evaluări

- Fund Acct 4.1Document23 paginiFund Acct 4.1Gabi MamushetÎncă nu există evaluări

- Budget 2021 22 Highlights CommentsDocument135 paginiBudget 2021 22 Highlights CommentsArsal GujjarÎncă nu există evaluări

- Pleasanton City Council Report On Budget Revisions 4/15/2020Document7 paginiPleasanton City Council Report On Budget Revisions 4/15/2020Courtney TeagueÎncă nu există evaluări

- FinolexDocument171 paginiFinolexAkash Nil ChatterjeeÎncă nu există evaluări

- 2021 Q3 Quarterly Report 01Document8 pagini2021 Q3 Quarterly Report 01mimmoÎncă nu există evaluări

- Report of The Auditor-General On The Accounts of Lagos Island Local Government For The Year Ended 31St December, 2020Document7 paginiReport of The Auditor-General On The Accounts of Lagos Island Local Government For The Year Ended 31St December, 2020Chinwe GloryÎncă nu există evaluări

- Taxation: MD Mashiur Rahaman Robin KPMG-RRHDocument12 paginiTaxation: MD Mashiur Rahaman Robin KPMG-RRHZidan ZaifÎncă nu există evaluări

- Estimated Revenues, Profits and Expenditure For Next Three YearsDocument6 paginiEstimated Revenues, Profits and Expenditure For Next Three YearsRajeev Kumar GottumukkalaÎncă nu există evaluări

- Union Budget FY12: Reasonable Under The CircumstancesDocument25 paginiUnion Budget FY12: Reasonable Under The CircumstancesNitesh SuranaÎncă nu există evaluări

- Handouts SAICA Tax Bill UpdateDocument222 paginiHandouts SAICA Tax Bill UpdateMohola Tebello GriffithÎncă nu există evaluări

- Ind As - 12 Income TaxesDocument26 paginiInd As - 12 Income TaxesAlok ThakurÎncă nu există evaluări

- Financial Accounting & AnalysisDocument9 paginiFinancial Accounting & AnalysisRiya DhanukaÎncă nu există evaluări

- KMC Budget Statement 2019-20 Highlights Key Projects and Revenue SourcesDocument58 paginiKMC Budget Statement 2019-20 Highlights Key Projects and Revenue SourcesAbhishek SatpathyÎncă nu există evaluări

- BSBFIM601 Manage FinancesDocument34 paginiBSBFIM601 Manage Financesneha0% (1)

- Kitsap Budget MemoDocument18 paginiKitsap Budget MemopaulbalcerakÎncă nu există evaluări

- 10-Casiguran Aurora 2010 Part1-Notes To FSDocument9 pagini10-Casiguran Aurora 2010 Part1-Notes To FSKasiguruhan AuroraÎncă nu există evaluări

- Tax Memorandum 2012 FinalDocument58 paginiTax Memorandum 2012 FinalAzka KhalidÎncă nu există evaluări

- 2022 Tax Expenditure Report FinalDocument43 pagini2022 Tax Expenditure Report FinalKirimi StanleyÎncă nu există evaluări

- Provincial Government Financial SummaryDocument7 paginiProvincial Government Financial SummarySen LinÎncă nu există evaluări

- Chapter 31 - Parkin - PowerPointDocument15 paginiChapter 31 - Parkin - PowerPointUzair IsmailÎncă nu există evaluări

- Moody's Adjustments To Vattenfall's Accounts: ObjectiveDocument4 paginiMoody's Adjustments To Vattenfall's Accounts: ObjectiveSunny VohraÎncă nu există evaluări

- FINAL Downer Tax Report FY21Document18 paginiFINAL Downer Tax Report FY21Kevin PhamÎncă nu există evaluări

- Audit of CoE, CB, AB, SES and PPE - SW10Document8 paginiAudit of CoE, CB, AB, SES and PPE - SW10d.pagkatoytoyÎncă nu există evaluări

- Maydolong Executive Summary 2011Document6 paginiMaydolong Executive Summary 2011Floydlizamarie PatualÎncă nu există evaluări

- Uttar_Pradesh_Revene_Sector_3_2013_Chap_2Document26 paginiUttar_Pradesh_Revene_Sector_3_2013_Chap_2rajendra lalÎncă nu există evaluări

- TaxationDocument12 paginiTaxationjanahh.omÎncă nu există evaluări

- AFM Project Report FinalDocument19 paginiAFM Project Report FinalRitu KumariÎncă nu există evaluări

- FAR05 - Accounting For Income and Deferred TaxesDocument4 paginiFAR05 - Accounting For Income and Deferred TaxesDisguised owlÎncă nu există evaluări

- An Analysis of The Budget of Bangladesh For The Fiscal Year 2015-16 Along With Its Previous Trend of Growth and ReductionDocument26 paginiAn Analysis of The Budget of Bangladesh For The Fiscal Year 2015-16 Along With Its Previous Trend of Growth and ReductionSekender AliÎncă nu există evaluări

- Tax Expenditure FinalDocument34 paginiTax Expenditure Finalመቅዲ ሀበሻዊትÎncă nu există evaluări

- IAS 12 Income Tax GuideDocument18 paginiIAS 12 Income Tax GuideTawanda Tatenda HerbertÎncă nu există evaluări

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineDe la EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineÎncă nu există evaluări

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionDe la EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionÎncă nu există evaluări

- Budget and Budget Execution in The Northwest Region of RomaniaDocument1 paginăBudget and Budget Execution in The Northwest Region of Romaniarodica_limbutuÎncă nu există evaluări

- Analysis Model of Financial Investment and Budget ExecutionDocument9 paginiAnalysis Model of Financial Investment and Budget Executionrodica_limbutuÎncă nu există evaluări

- Mirela - Pintea@econ - Ubbcluj.ro Sorin - Achim@econ - Ubbcluj.ro Viorel - Lacatus@econ - UbbclujDocument11 paginiMirela - Pintea@econ - Ubbcluj.ro Sorin - Achim@econ - Ubbcluj.ro Viorel - Lacatus@econ - Ubbclujrodica_limbutuÎncă nu există evaluări

- International Finance and Banking Conference FI BA 2015 XIIIth Ed PDFDocument391 paginiInternational Finance and Banking Conference FI BA 2015 XIIIth Ed PDFrodica_limbutuÎncă nu există evaluări

- Open Budget IndexDocument1 paginăOpen Budget Indexrodica_limbutuÎncă nu există evaluări

- SSRN Id877951 PDFDocument30 paginiSSRN Id877951 PDFrodica_limbutuÎncă nu există evaluări

- Mushak 9.1 UpdatedDocument15 paginiMushak 9.1 UpdatedRakibul HassanÎncă nu există evaluări

- Nikhil Internship Report PDFDocument24 paginiNikhil Internship Report PDFNikhil Jain56% (9)

- t1229 Fill 23eDocument2 paginit1229 Fill 23eShiblee Khalid AhmodÎncă nu există evaluări

- Business Tax: Value Added Tax Percentage Tax Excise Tax Documentary Stamp TaxDocument7 paginiBusiness Tax: Value Added Tax Percentage Tax Excise Tax Documentary Stamp TaxJessaÎncă nu există evaluări

- Form W-8BEN-E InstructionsDocument15 paginiForm W-8BEN-E InstructionsSteve ThompsonÎncă nu există evaluări

- TAX Quiz 1Document12 paginiTAX Quiz 1Ednalyn CruzÎncă nu există evaluări

- Donors Taxation and Intro To Tax Remedies BsaDocument36 paginiDonors Taxation and Intro To Tax Remedies BsaPipz G. CastroÎncă nu există evaluări

- Brokerage Scenario and Computation.2Document3 paginiBrokerage Scenario and Computation.2Rolly Pagtolon-anÎncă nu există evaluări

- Tax II DoctrinesDocument22 paginiTax II DoctrinesnikkiÎncă nu există evaluări

- 2014 Federal 1040 (Esther)Document2 pagini2014 Federal 1040 (Esther)Abdirahman Abdullahi Omar43% (7)

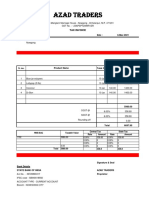

- Invoice 26Document2 paginiInvoice 26asim khanÎncă nu există evaluări

- Understanding VAT: A Guide to Value-Added Tax ConceptsDocument9 paginiUnderstanding VAT: A Guide to Value-Added Tax Conceptsjanjan eresoÎncă nu există evaluări

- Creating A 501c4 With 501c3 - c4 - 527 - GuideDocument100 paginiCreating A 501c4 With 501c3 - c4 - 527 - GuideNoah PainterÎncă nu există evaluări

- Taxpayers Account Management Program (Tamp)Document8 paginiTaxpayers Account Management Program (Tamp)mark liezerÎncă nu există evaluări

- Differences between Composition and Regular Firms in GSTDocument4 paginiDifferences between Composition and Regular Firms in GSTAadarsh LamaÎncă nu există evaluări

- GFSM 2014 (91-108)Document18 paginiGFSM 2014 (91-108)Jackson Ubulele DadeÎncă nu există evaluări

- Taxation and Tax Law QuestionsDocument5 paginiTaxation and Tax Law Questionsnicole08030% (1)

- PDF 236811830140623Document1 paginăPDF 236811830140623Akeybo 340Încă nu există evaluări

- RMC No. 117-2021Document1 paginăRMC No. 117-2021Em SantosÎncă nu există evaluări

- Transfer and Business Taxation-1Document22 paginiTransfer and Business Taxation-1Harry Jericho DemafilesÎncă nu există evaluări

- GST invoice summary reportDocument28 paginiGST invoice summary reportHarinath HnÎncă nu există evaluări

- Elimination of Cascading Tax EffectDocument2 paginiElimination of Cascading Tax EffectHariharanÎncă nu există evaluări

- Income Tax Challan - 280Document1 paginăIncome Tax Challan - 280Subrata SarkarÎncă nu există evaluări

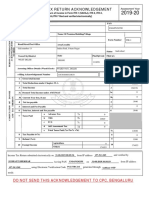

- Indian Income Tax Return Acknowledgement SummaryDocument1 paginăIndian Income Tax Return Acknowledgement SummaryAnonymous k9nrtxAÎncă nu există evaluări

- Taxation (Malawi) : Tuesday 4 June 2013Document10 paginiTaxation (Malawi) : Tuesday 4 June 2013angaÎncă nu există evaluări

- Comparing Macroeconomics of India and France EconomiesDocument26 paginiComparing Macroeconomics of India and France EconomiesDiksha LathÎncă nu există evaluări

- Monthly Remittance Return of Value-Added Tax Withheld 2 0: BIR Form NoDocument2 paginiMonthly Remittance Return of Value-Added Tax Withheld 2 0: BIR Form NoMark Joseph Baja67% (3)

- Assignment 6Document1 paginăAssignment 6aafÎncă nu există evaluări

- Chapter 3 SolutionsssssDocument22 paginiChapter 3 SolutionsssssBharat SinghÎncă nu există evaluări

- Anukret On Tax Incentive in Securities Sector EnglishDocument4 paginiAnukret On Tax Incentive in Securities Sector EnglishChou ChantraÎncă nu există evaluări