S-ar putea să vă placă și

- Ormoc City Lumber Tax Upheld by Supreme CourtDocument3 paginiOrmoc City Lumber Tax Upheld by Supreme CourtClyde KitongÎncă nu există evaluări

- Double TaxationDocument26 paginiDouble TaxationAnonymous XsaqDYDÎncă nu există evaluări

- Santos Lumber Company, Et Al., vs. City of Cebu, G.R. No. L-10196Document4 paginiSantos Lumber Company, Et Al., vs. City of Cebu, G.R. No. L-10196MARICEL DEFELESÎncă nu există evaluări

- Ponce Enrile, Siguion Reyna, Montecillo & Belo and Teehankee, Carreon & Tañada For Plaintiff-Appellant. Ramon O. de Veyra For Defendants-AppelleesDocument8 paginiPonce Enrile, Siguion Reyna, Montecillo & Belo and Teehankee, Carreon & Tañada For Plaintiff-Appellant. Ramon O. de Veyra For Defendants-AppelleesJoseff Anthony FernandezÎncă nu există evaluări

- 32 Serafica Vs Treasurer of Ormoc FULLDocument4 pagini32 Serafica Vs Treasurer of Ormoc FULLQueenie Hadiyah Diampuan SaripÎncă nu există evaluări

- Local Tax Ordinance Upheld by Supreme CourtDocument4 paginiLocal Tax Ordinance Upheld by Supreme CourtAli NamlaÎncă nu există evaluări

- Punzalan vs. Municipal BoardDocument1 paginăPunzalan vs. Municipal Boardenan_intonÎncă nu există evaluări

- G.R. No. L-24322Document2 paginiG.R. No. L-24322Sara Dela Cruz AvillonÎncă nu există evaluări

- Local Govt TaxDocument18 paginiLocal Govt TaxJermaine SemañaÎncă nu există evaluări

- Basco Vs PagcorDocument5 paginiBasco Vs PagcorDenver Dela Cruz PadrigoÎncă nu există evaluări

- Supreme Court: F. S. Villarin For Petitioners. Jose B. Navarro For RespondentDocument7 paginiSupreme Court: F. S. Villarin For Petitioners. Jose B. Navarro For RespondentgheljoshÎncă nu există evaluări

- Administrative Law Full Text Set 4Document107 paginiAdministrative Law Full Text Set 4Darlene GanubÎncă nu există evaluări

- Punsalan V Mun Board of The City of ManilaDocument2 paginiPunsalan V Mun Board of The City of ManilaHyacinth Valera BalonglongÎncă nu există evaluări

- Crimpro Cases (Jurisdiction Venue)Document60 paginiCrimpro Cases (Jurisdiction Venue)Roan BacÎncă nu există evaluări

- Ormoc Sugar Company v. Treasurer of Ormoc CityDocument4 paginiOrmoc Sugar Company v. Treasurer of Ormoc CityCedrick Contado Susi BocoÎncă nu există evaluări

- 21 30Document46 pagini21 30Michael Renz PalabayÎncă nu există evaluări

- Procter & Gamble Philippine Manufacturing Corp. vs. Municipality of JagnaDocument13 paginiProcter & Gamble Philippine Manufacturing Corp. vs. Municipality of JagnaXtine CampuPot100% (1)

- Merrera, Christianne Joyse V. Criminal Procedure: March 25, 1994Document3 paginiMerrera, Christianne Joyse V. Criminal Procedure: March 25, 1994Christianne Joyse MerreraÎncă nu există evaluări

- SC Rules Against Ormoc City Sugar Tax as UnconstitutionalDocument2 paginiSC Rules Against Ormoc City Sugar Tax as UnconstitutionalulticonÎncă nu există evaluări

- Santos vs. Aquino, 94 Phil., 65, November 28, 1953Document5 paginiSantos vs. Aquino, 94 Phil., 65, November 28, 1953Jaden Jacob IvoryÎncă nu există evaluări

- Ormoc Sugar Company vs. Treasurer of Ormoc CityDocument3 paginiOrmoc Sugar Company vs. Treasurer of Ormoc CityHannah Keziah Dela CernaÎncă nu există evaluări

- Republic Act 7691, 1994Document4 paginiRepublic Act 7691, 1994AAMCÎncă nu există evaluări

- Bagatsing Vs Ramirez 74 Scra 306 1976Document5 paginiBagatsing Vs Ramirez 74 Scra 306 1976andangÎncă nu există evaluări

- 61.-Hodges v. Mun. Board of Iloilo City, G.R No. L-18276Document5 pagini61.-Hodges v. Mun. Board of Iloilo City, G.R No. L-18276Christine Rose Bonilla LikiganÎncă nu există evaluări

- Supreme Court: Attorney-General Jaranilla For Appellant. Jose C. Abrew For AppelleeDocument46 paginiSupreme Court: Attorney-General Jaranilla For Appellant. Jose C. Abrew For AppelleeLuelle B. PacquingÎncă nu există evaluări

- Jurisdiction and Special Powers of Metropolitan, Municipal and Circuit Trial CourtsDocument4 paginiJurisdiction and Special Powers of Metropolitan, Municipal and Circuit Trial CourtsGLENDEL GUEVARRAÎncă nu există evaluări

- Republic of The PhilippinesDocument51 paginiRepublic of The PhilippinesMariaÎncă nu există evaluări

- Ra 7691 PDFDocument3 paginiRa 7691 PDFIvan LinÎncă nu există evaluări

- MAGTAJAS V. PRYCE PROPERTIES - CASE DIGEST ON LOCAL GOVERNMENT POWERSDocument34 paginiMAGTAJAS V. PRYCE PROPERTIES - CASE DIGEST ON LOCAL GOVERNMENT POWERSChristopher GuevarraÎncă nu există evaluări

- Power of TaxationDocument15 paginiPower of TaxationVel June De LeonÎncă nu există evaluări

- Court Upholds Manila Occupation Tax But Finds Penalty InvalidDocument1 paginăCourt Upholds Manila Occupation Tax But Finds Penalty InvalidMichael Mendoza MarpuriÎncă nu există evaluări

- Taxation Dispute Over Property Rental IncomeDocument9 paginiTaxation Dispute Over Property Rental IncomemaeÎncă nu există evaluări

- Philippines expands lower court jurisdictionDocument3 paginiPhilippines expands lower court jurisdictionGab NaparatoÎncă nu există evaluări

- Ra 7691Document23 paginiRa 7691Elenita OrdaÎncă nu există evaluări

- RA 7691 An Act Amending BP 129Document6 paginiRA 7691 An Act Amending BP 129Nea TanÎncă nu există evaluări

- Supreme Court upholds Manila occupation tax ordinanceDocument2 paginiSupreme Court upholds Manila occupation tax ordinanceSharliemagne B. BayanÎncă nu există evaluări

- Court upholds sugar workers' right to sue as pauper litigantsDocument4 paginiCourt upholds sugar workers' right to sue as pauper litigantsJohn Patrick GarciaÎncă nu există evaluări

- Manila Market Stall Fees UpheldDocument6 paginiManila Market Stall Fees UpheldSharon BakerÎncă nu există evaluări

- G.R. No. L 23794 Ormoc Sugar Co. Inc. v. Treasurer of Ormoc CityDocument4 paginiG.R. No. L 23794 Ormoc Sugar Co. Inc. v. Treasurer of Ormoc CityKryzza CaloÎncă nu există evaluări

- Republic Act No 7691Document8 paginiRepublic Act No 7691Estela BenegildoÎncă nu există evaluări

- Punsalan vs. Municipal Board of Manila 95 Phil 46Document2 paginiPunsalan vs. Municipal Board of Manila 95 Phil 46eunice demaclidÎncă nu există evaluări

- Silvestre Punsalan v. The Municipal Board of The City of ManilaDocument4 paginiSilvestre Punsalan v. The Municipal Board of The City of ManilaBREL GOSIMATÎncă nu există evaluări

- G.R. No. L-23858, November 21, 1979Document7 paginiG.R. No. L-23858, November 21, 1979MATANG PilipinoÎncă nu există evaluări

- H.27 Benguet Corp Vs CBAA GR No. 100959 06291992 PDFDocument3 paginiH.27 Benguet Corp Vs CBAA GR No. 100959 06291992 PDFbabyclaire17Încă nu există evaluări

- Republic Act No. 7691 - Official Gazette of The Republic of The PhilippinesDocument4 paginiRepublic Act No. 7691 - Official Gazette of The Republic of The PhilippinesMTC - DIFFUNÎncă nu există evaluări

- SC CircularsDocument65 paginiSC CircularskaiÎncă nu există evaluări

- Admin Vi ViiiDocument106 paginiAdmin Vi ViiiAriel Mark PilotinÎncă nu există evaluări

- RA 7691 Expands Jurisdiction of Metro Trial Courts, Municipal Trial Courts, Municipal Circuit Trial CourtsDocument16 paginiRA 7691 Expands Jurisdiction of Metro Trial Courts, Municipal Trial Courts, Municipal Circuit Trial CourtsRoberts SamÎncă nu există evaluări

- Cebu Portland Cement Co V Municipality of NagaDocument5 paginiCebu Portland Cement Co V Municipality of NagaChloe HernaneÎncă nu există evaluări

- Cebu Portland Cement Co. v. Municipality ofDocument5 paginiCebu Portland Cement Co. v. Municipality ofDenise LabagnaoÎncă nu există evaluări

- #76 Punzalan v. Municipal Board of ManilaDocument2 pagini#76 Punzalan v. Municipal Board of ManilaKristine EnriquezÎncă nu există evaluări

- Double Taxation of Professions UpheldDocument4 paginiDouble Taxation of Professions UpheldSarah Jean SiloterioÎncă nu există evaluări

- Ra 7902-7691Document3 paginiRa 7902-7691Cha AgaderÎncă nu există evaluări

- RTC case dismissal motionDocument8 paginiRTC case dismissal motionRosario NicanorÎncă nu există evaluări

- Bagatsing v. RamirezDocument6 paginiBagatsing v. RamirezUnis BautistaÎncă nu există evaluări

- City of Government of Caloocan vs. DavidDocument10 paginiCity of Government of Caloocan vs. DavidCharmaine GraceÎncă nu există evaluări

- Civ Pro Cases SyllabusDocument9 paginiCiv Pro Cases SyllabusJocelynyemvelosoÎncă nu există evaluări

- Civil Procedure CasesDocument48 paginiCivil Procedure CasesangelicaÎncă nu există evaluări

- 129-City of Iloilo v. Villanueva, 105 Phil. 337Document4 pagini129-City of Iloilo v. Villanueva, 105 Phil. 337Jopan SJÎncă nu există evaluări

- 10Document11 pagini10Yanhicoh CySaÎncă nu există evaluări

- Republic V GrijaldoDocument7 paginiRepublic V Grijaldocookbooks&lawbooks0% (1)

- Republic V GrijaldoDocument7 paginiRepublic V Grijaldocookbooks&lawbooks0% (1)

- Tolentino V GonzalesDocument12 paginiTolentino V GonzalesKenneth BuriÎncă nu există evaluări

- Cir Vs Pineda 21 Scra 105Document4 paginiCir Vs Pineda 21 Scra 105Atty JV AbuelÎncă nu există evaluări

- MMDADocument6 paginiMMDAYanhicoh CySaÎncă nu există evaluări

- Phcpi vs. CirDocument10 paginiPhcpi vs. CirYanhicoh CySaÎncă nu există evaluări

- Supreme CourtDocument6 paginiSupreme CourtYanhicoh CySaÎncă nu există evaluări

- 8Document146 pagini8Yanhicoh CySaÎncă nu există evaluări

- BPI Investment V CA - GR 133632Document6 paginiBPI Investment V CA - GR 133632Jeremiah ReynaldoÎncă nu există evaluări

- Coc v. Hypermix FeedsDocument9 paginiCoc v. Hypermix FeedsHaniyyah FtmÎncă nu există evaluări

- Phil Petroleum Corp Vs Municipality of Pililia, RizalDocument6 paginiPhil Petroleum Corp Vs Municipality of Pililia, RizalrrrhesariezenÎncă nu există evaluări

- 02 People V ConcepcionDocument6 pagini02 People V Concepcionamazing_pinoyÎncă nu există evaluări

- 1-Lorenzo Vs PosadasDocument9 pagini1-Lorenzo Vs PosadasNimpa PichayÎncă nu există evaluări

- SC upholds municipality's power to levy production taxDocument8 paginiSC upholds municipality's power to levy production taxKristineSherikaChyÎncă nu există evaluări

- City of Manila vs. Coca ColaDocument10 paginiCity of Manila vs. Coca ColaYanhicoh CySaÎncă nu există evaluări

- Leido, Andrada, Perez and Associates For Petitioners. Office of The Solicitor General For RespondentsDocument6 paginiLeido, Andrada, Perez and Associates For Petitioners. Office of The Solicitor General For RespondentsYanhicoh CySaÎncă nu există evaluări

- 12 Philippine Airlines V Edu (1988)Document8 pagini12 Philippine Airlines V Edu (1988)KristineSherikaChyÎncă nu există evaluări

- Gaston Vs Republic Planters BankDocument5 paginiGaston Vs Republic Planters BankRyan SuaverdezÎncă nu există evaluări

- Intro To LawDocument12 paginiIntro To LawRea Jane B. MalcampoÎncă nu există evaluări

- G.R. No. L-7859 - Lutz Vs Araneta (22 Dec 55)Document3 paginiG.R. No. L-7859 - Lutz Vs Araneta (22 Dec 55)jdz1988Încă nu există evaluări

- Caltex vs. CoaDocument16 paginiCaltex vs. CoaYanhicoh CySaÎncă nu există evaluări

- UN Convention against Torture key obligationsDocument9 paginiUN Convention against Torture key obligationsYanhicoh CySaÎncă nu există evaluări

- Convention For Ozone Layer PDFDocument81 paginiConvention For Ozone Layer PDFYanhicoh CySaÎncă nu există evaluări

- Developments in PhilippineDocument6 paginiDevelopments in PhilippineYanhicoh CySaÎncă nu există evaluări

- Forum On Environmental JusticeDocument4 paginiForum On Environmental JusticeYanhicoh CySaÎncă nu există evaluări

- Universal Declaration of Human RightsDocument6 paginiUniversal Declaration of Human RightsYanhicoh CySaÎncă nu există evaluări

- Human Rights EducationDocument13 paginiHuman Rights EducationYanhicoh CySaÎncă nu există evaluări

- Rules Implementing Code of Conduct for Public OfficialsDocument18 paginiRules Implementing Code of Conduct for Public OfficialsicebaguilatÎncă nu există evaluări

- Roadmap To Freedom Ebook Access Your Secret Trust and Become Financially Abundant260822Document16 paginiRoadmap To Freedom Ebook Access Your Secret Trust and Become Financially Abundant260822Edis Mendoza100% (12)

- RFBT.O 1601.law On Obligations WithanswersDocument34 paginiRFBT.O 1601.law On Obligations WithanswersUnpopular VoiceÎncă nu există evaluări

- MIS in BankingDocument34 paginiMIS in BankingAlmira Menezes100% (1)

- Diego v. DiegoDocument13 paginiDiego v. DiegoIvan LuzuriagaÎncă nu există evaluări

- CIVIL LAW REVIEW 2 EXAMDocument19 paginiCIVIL LAW REVIEW 2 EXAMPilacan KarylÎncă nu există evaluări

- Statement EUDocument41 paginiStatement EUuyên đỗÎncă nu există evaluări

- Essential Wedding Package for 150+ GuestsDocument2 paginiEssential Wedding Package for 150+ GuestsVic VerraÎncă nu există evaluări

- SpiceJet - E-Ticket - PNR - H854QV 26 Jan 2022 Patna-Pune For MR. RANJANDocument3 paginiSpiceJet - E-Ticket - PNR - H854QV 26 Jan 2022 Patna-Pune For MR. RANJANRajat RanjanÎncă nu există evaluări

- UBP Corporate Card Application - Employee - New FillableDocument5 paginiUBP Corporate Card Application - Employee - New FillableAdam Albert DomendenÎncă nu există evaluări

- Accounting Information System ReviewDocument5 paginiAccounting Information System ReviewALMA MORENAÎncă nu există evaluări

- Maritime Law - Chapter 5Document14 paginiMaritime Law - Chapter 5Mohan RamÎncă nu există evaluări

- Laporan Keuangan Konsolidasian PT Pegadaian (Persero) Tahun 2020 - Audited 4ARDocument126 paginiLaporan Keuangan Konsolidasian PT Pegadaian (Persero) Tahun 2020 - Audited 4ARFahmi FalahÎncă nu există evaluări

- Auto Debit Arrangement - 20190804 - 020707 PDFDocument4 paginiAuto Debit Arrangement - 20190804 - 020707 PDFKim Josashiwa BergulaÎncă nu există evaluări

- Internship Report LcwuDocument125 paginiInternship Report LcwuNidaÎncă nu există evaluări

- Capture D'écran . 2023-11-09 À 16.14.52Document24 paginiCapture D'écran . 2023-11-09 À 16.14.52hocine.belghoulÎncă nu există evaluări

- Housing Information: (1) On-Campus DormitoryDocument4 paginiHousing Information: (1) On-Campus DormitoryNico Illarregui HelÎncă nu există evaluări

- Mbeya University of Science and TechnologyDocument2 paginiMbeya University of Science and TechnologyDanny TzÎncă nu există evaluări

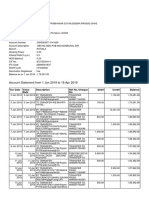

- Account Statement From 1 Jan 2019 To 18 Apr 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 paginiAccount Statement From 1 Jan 2019 To 18 Apr 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceManoj PrabhakarÎncă nu există evaluări

- 03 - Business TransactionDocument28 pagini03 - Business TransactionLeandro FariaÎncă nu există evaluări

- 01 Mar 2020 Bill PDFDocument5 pagini01 Mar 2020 Bill PDFChanel PhangÎncă nu există evaluări

- P38 Parts List PDFDocument308 paginiP38 Parts List PDFkkÎncă nu există evaluări

- Statement of Account: Smartsaver Credit CardDocument5 paginiStatement of Account: Smartsaver Credit CardGeorgeEdwardÎncă nu există evaluări

- Voucher Form For NGODocument1 paginăVoucher Form For NGOjoy elizondoÎncă nu există evaluări

- Oporto v. Members of The Board of Inquiry and Discipline of The National Power CorporationDocument2 paginiOporto v. Members of The Board of Inquiry and Discipline of The National Power CorporationAlyssa Alee Angeles JacintoÎncă nu există evaluări

- RITSWIFT Interface User GuideDocument144 paginiRITSWIFT Interface User GuidePrachi SaxenaÎncă nu există evaluări

- KY Auto Insurance ApplicationDocument7 paginiKY Auto Insurance ApplicationRoll Kings0% (1)

- Columbario de Santa Ana: Purchase AgreementDocument3 paginiColumbario de Santa Ana: Purchase AgreementRambotan17Încă nu există evaluări

- IBS Gurgaon Enrollment Letter for PGPM Program 2021-23Document4 paginiIBS Gurgaon Enrollment Letter for PGPM Program 2021-23Gaurav gusaiÎncă nu există evaluări

- Apex Clearing One Dallas Center 350 North ST Paul Suite 1300 DALLAS, TX 75201 in Account WithDocument8 paginiApex Clearing One Dallas Center 350 North ST Paul Suite 1300 DALLAS, TX 75201 in Account WithMandy PaweenaÎncă nu există evaluări

- L - Cash 18 PDFDocument32 paginiL - Cash 18 PDFHaidar Aulia RahmanÎncă nu există evaluări