S-ar putea să vă placă și

- Sensory - Based Reflection Sensory - Based Reflection: 1. What and Who Do I See? 1. What and Who Do I See?Document1 paginăSensory - Based Reflection Sensory - Based Reflection: 1. What and Who Do I See? 1. What and Who Do I See?Janica GaynorÎncă nu există evaluări

- Missionary Sisters of The Queen of The ApostlesDocument1 paginăMissionary Sisters of The Queen of The ApostlesJanica GaynorÎncă nu există evaluări

- Industry SituationDocument7 paginiIndustry SituationJanica GaynorÎncă nu există evaluări

- Chapter 1: Critical Evaluation in The Context of John RawlsDocument2 paginiChapter 1: Critical Evaluation in The Context of John RawlsJanica GaynorÎncă nu există evaluări

- Buddhism:: The Enlightened OneDocument7 paginiBuddhism:: The Enlightened OneJanica GaynorÎncă nu există evaluări

- Buddhism:: The Enlightened OneDocument7 paginiBuddhism:: The Enlightened OneJanica GaynorÎncă nu există evaluări

- Zamboanga Del Sur - 51Document6 paginiZamboanga Del Sur - 51Janica GaynorÎncă nu există evaluări

- IT QuestionsDocument1 paginăIT QuestionsJanica GaynorÎncă nu există evaluări

- 2015 Report No. 5 - Institutional Population - Statistical TablesDocument220 pagini2015 Report No. 5 - Institutional Population - Statistical TablesJanica GaynorÎncă nu există evaluări

- Case lawTIBAJIADocument11 paginiCase lawTIBAJIAJanica GaynorÎncă nu există evaluări

- DDocument1 paginăDCarmela EspirituÎncă nu există evaluări

- Case lawTIBAJIADocument11 paginiCase lawTIBAJIAJanica GaynorÎncă nu există evaluări

- Aistotle AndplatoDocument1 paginăAistotle AndplatoJanica GaynorÎncă nu există evaluări

- Children of The CityDocument9 paginiChildren of The CityJanica GaynorÎncă nu există evaluări

- IT QuestionsDocument1 paginăIT QuestionsJanica GaynorÎncă nu există evaluări

- RizalDocument2 paginiRizalJanica GaynorÎncă nu există evaluări

- AcctgDocument2 paginiAcctgJanica GaynorÎncă nu există evaluări

- Tibajia vs. Ca and Eden Tan G.R. No. 100290 June 4, 1993 FactsDocument3 paginiTibajia vs. Ca and Eden Tan G.R. No. 100290 June 4, 1993 FactsJanica GaynorÎncă nu există evaluări

- RizalDocument1 paginăRizalJanica GaynorÎncă nu există evaluări

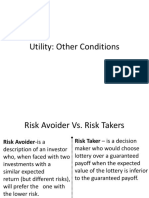

- 5 3utilityDocument2 pagini5 3utilityJanica GaynorÎncă nu există evaluări

- Audit Trail - The Path of TransactionsDocument1 paginăAudit Trail - The Path of TransactionsJanica GaynorÎncă nu există evaluări

- Gaynor, Janica Teresa P. Bsma-Iv PHILO 106-C July 17, 2017: JustificationsDocument1 paginăGaynor, Janica Teresa P. Bsma-Iv PHILO 106-C July 17, 2017: JustificationsJanica GaynorÎncă nu există evaluări

- Assistant DirectorDocument1 paginăAssistant DirectorJanica GaynorÎncă nu există evaluări

- Aistotle AndplatoDocument1 paginăAistotle AndplatoJanica GaynorÎncă nu există evaluări

- Chapter 5 Summary (The Expenditure Cycle Part I)Document11 paginiChapter 5 Summary (The Expenditure Cycle Part I)Janica GaynorÎncă nu există evaluări

- Revenue Cycle Activities & Business ProcessesDocument6 paginiRevenue Cycle Activities & Business ProcessesJanica GaynorÎncă nu există evaluări

- ArcillasDocument4 paginiArcillasJanica GaynorÎncă nu există evaluări

- Chapter 5 Summary (The Expenditure Cycle Part I)Document11 paginiChapter 5 Summary (The Expenditure Cycle Part I)Janica GaynorÎncă nu există evaluări

- Chapter 1 GlobalizationDocument1 paginăChapter 1 GlobalizationJanica GaynorÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5782)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Geopolitical Economy: The Discipline of MultipolarityDocument12 paginiGeopolitical Economy: The Discipline of MultipolarityValdai Discussion ClubÎncă nu există evaluări

- Grand Strategy UsDocument44 paginiGrand Strategy Ussaad aliÎncă nu există evaluări

- Volatility Exchange-Traded Notes - Curse or CureDocument25 paginiVolatility Exchange-Traded Notes - Curse or CurelastkraftwagenfahrerÎncă nu există evaluări

- Time Management PresentationDocument81 paginiTime Management Presentationsau_org71% (7)

- Hubbert's Peak TheoryDocument15 paginiHubbert's Peak TheoryHrishikesh ChappadiÎncă nu există evaluări

- 36% in UK will never buy own home as prices soarDocument4 pagini36% in UK will never buy own home as prices soarBojana StankovskiÎncă nu există evaluări

- Erikson Developmental Theory PDFDocument2 paginiErikson Developmental Theory PDFPatriciaÎncă nu există evaluări

- Essay On NeoliberalismDocument16 paginiEssay On NeoliberalismBrian John SpencerÎncă nu există evaluări

- Avon ProductsDocument21 paginiAvon ProductsAfshan RahmanÎncă nu există evaluări

- 5.1foreign Exchange Rate Determination and ForecastingDocument34 pagini5.1foreign Exchange Rate Determination and ForecastingSanaFatimaÎncă nu există evaluări

- Econ PuzzleDocument3 paginiEcon Puzzleapi-589326054Încă nu există evaluări

- Introduction To Energy CrisisDocument6 paginiIntroduction To Energy CrisisTalha RiazÎncă nu există evaluări

- Introduction To Management - Management EnvironmentDocument9 paginiIntroduction To Management - Management EnvironmentDhanis ParamaguruÎncă nu există evaluări

- Cadbury Crisis in IndiaDocument6 paginiCadbury Crisis in IndiaKushagra VarmaÎncă nu există evaluări

- Financial RegulationDocument21 paginiFinancial RegulationMitesh PatilÎncă nu există evaluări

- Financial Hardship Letter SampleDocument2 paginiFinancial Hardship Letter SampleWilliam BluntÎncă nu există evaluări

- Business Cycles & Theories of Business CyclesDocument7 paginiBusiness Cycles & Theories of Business CyclesAppan Kandala VasudevacharyÎncă nu există evaluări

- PetrofinDocument30 paginiPetrofinergonblognewsÎncă nu există evaluări

- Toyota (Automobile) - Waqas FinalDocument55 paginiToyota (Automobile) - Waqas FinalRaza HassanÎncă nu există evaluări

- Rmi 2302 Final Study GuideDocument2 paginiRmi 2302 Final Study GuideDerek GarberÎncă nu există evaluări

- Opportunity of Financial Investment in Cambodia by Dr. Chhiv ThetDocument38 paginiOpportunity of Financial Investment in Cambodia by Dr. Chhiv ThetHong KhengÎncă nu există evaluări

- UssamaDocument12 paginiUssamaRizwan RizzuÎncă nu există evaluări

- Revolution in The 21st Century (Chris Harman)Document65 paginiRevolution in The 21st Century (Chris Harman)Sinsia Van Kalkeren100% (2)

- Lazzarato IndebtedManDocument86 paginiLazzarato IndebtedManPatrick W. GalbraithÎncă nu există evaluări

- My Internship Report (2) Hina MasoodDocument255 paginiMy Internship Report (2) Hina Masoodulovet67% (3)

- Container Industry Value ChainDocument14 paginiContainer Industry Value ChainRasmus ArentsenÎncă nu există evaluări

- From Crisis To Financial Stability Turkey Experience 3rd EdDocument98 paginiFrom Crisis To Financial Stability Turkey Experience 3rd Edsuhail.rizwanÎncă nu există evaluări

- Demo 2 Va 3Document40 paginiDemo 2 Va 3Quang HuyÎncă nu există evaluări

- STRUKTUR CRISIS MANAGEMENT TEAM PT. BANK MANDIRI (PERSERO) Tbk. KK MalukDocument1 paginăSTRUKTUR CRISIS MANAGEMENT TEAM PT. BANK MANDIRI (PERSERO) Tbk. KK MalukFadhlan FrOstÎncă nu există evaluări

- Foreign Portfolio Equity Investment in Egypt An Analytical OverviewDocument55 paginiForeign Portfolio Equity Investment in Egypt An Analytical OverviewGibran KasrinÎncă nu există evaluări