S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Financial Engineering Principles - Perry BeaumontDocument0 paginiFinancial Engineering Principles - Perry BeaumontShankey Gupta100% (5)

- RTP CA Final New Course Paper 2 Strategic Financial ManagemeDocument26 paginiRTP CA Final New Course Paper 2 Strategic Financial ManagemeTusharÎncă nu există evaluări

- Investors Perception Towards Real Estate InvestmentDocument38 paginiInvestors Perception Towards Real Estate InvestmentMohd Fahd Kapadia25% (4)

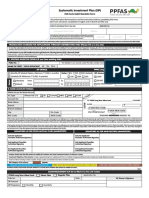

- Ppfas Sip FormDocument2 paginiPpfas Sip FormAmol ChikhalkarÎncă nu există evaluări

- FinanceDocument7 paginiFinanceanon_945457258Încă nu există evaluări

- Sterne Agee On Brinker - EATDocument5 paginiSterne Agee On Brinker - EATlehighsolutionsÎncă nu există evaluări

- Factors Influencing Individual Investor BehaviourDocument13 paginiFactors Influencing Individual Investor BehavioursheetalÎncă nu există evaluări

- Introduction to financial analysis of a manufacturing firmDocument77 paginiIntroduction to financial analysis of a manufacturing firmrayhan555Încă nu există evaluări

- Final Project Report On Small Saving OptionsDocument56 paginiFinal Project Report On Small Saving Optionsrajeshbohra67% (3)

- 7 Bursa Malaysia Story SunumDocument21 pagini7 Bursa Malaysia Story SunumHafiz KAÎncă nu există evaluări

- Munk - 2008 - Financial Asset Pricing TheoryDocument360 paginiMunk - 2008 - Financial Asset Pricing TheoryDong Song100% (1)

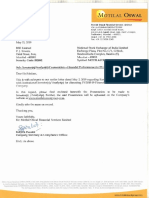

- Motilal Oswal Q4 Investor PresentationDocument70 paginiMotilal Oswal Q4 Investor PresentationSammyÎncă nu există evaluări

- BSE Stock Exchange Guide: History, Features & How to TradeDocument17 paginiBSE Stock Exchange Guide: History, Features & How to TradekiranÎncă nu există evaluări

- Assignment 2Document3 paginiAssignment 2Shulav ShresthaÎncă nu există evaluări

- Ratio Analysis of Textile IndustryDocument17 paginiRatio Analysis of Textile IndustrySumon SahaÎncă nu există evaluări

- Week 9 PPT 9 - Statement of Cash FlowsDocument23 paginiWeek 9 PPT 9 - Statement of Cash FlowsAmel Surya GumilangÎncă nu există evaluări

- Valuation of Life Insurance Companies in IndiaDocument11 paginiValuation of Life Insurance Companies in IndiaVersha KaushikÎncă nu există evaluări

- MGMT 30A: Practice FinalDocument18 paginiMGMT 30A: Practice FinalFUSION AcademicsÎncă nu există evaluări

- Water Ownership DatabaseDocument21 paginiWater Ownership DatabaseAlessandre OliveiraÎncă nu există evaluări

- Investors Perception Towards Online TradingDocument53 paginiInvestors Perception Towards Online TradingEvin Benny75% (4)

- Mergers and AcquisitionDocument93 paginiMergers and Acquisitionapi-3712392100% (7)

- Mint Money 1 For WEBDocument17 paginiMint Money 1 For WEBRoshan KumarÎncă nu există evaluări

- Dividend DatesDocument2 paginiDividend DatesEmaanÎncă nu există evaluări

- Consolidated Financial Statements (CFS) ExplainedDocument130 paginiConsolidated Financial Statements (CFS) ExplainedKumar SwamyÎncă nu există evaluări

- Derivatives FinalDocument37 paginiDerivatives FinalmannashkshitigarÎncă nu există evaluări

- Differences between Private and Public CompaniesDocument7 paginiDifferences between Private and Public CompaniesBilawal MughalÎncă nu există evaluări

- Stock Market IndicesDocument15 paginiStock Market IndicesSIdhu SimmiÎncă nu există evaluări

- Seminar ReportDocument13 paginiSeminar Reportdipti_1312Încă nu există evaluări