S-ar putea să vă placă și

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesDe la EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesÎncă nu există evaluări

- US Taxation - Outline: I. Types of Tax Rate StructuresDocument12 paginiUS Taxation - Outline: I. Types of Tax Rate Structuresvarghese2007Încă nu există evaluări

- Progressive Consumption Taxation: The X Tax RevisitedDe la EverandProgressive Consumption Taxation: The X Tax RevisitedÎncă nu există evaluări

- Fundamentals of Taxation 2019 12th Edition Schisler Test BankDocument17 paginiFundamentals of Taxation 2019 12th Edition Schisler Test BankJaredStantonpqcrj100% (11)

- Chapters 1-3Document12 paginiChapters 1-3BethellaSamPhillipsÎncă nu există evaluări

- LEGT2751 Lecture 1Document14 paginiLEGT2751 Lecture 1reflecti0nÎncă nu există evaluări

- Some Terms in Income Tax ClarifiedDocument9 paginiSome Terms in Income Tax ClarifiedAnonymous ATg0gvcf9Încă nu există evaluări

- Personal Finance Another Perspective: Tax PlanningDocument50 paginiPersonal Finance Another Perspective: Tax PlanningcrazysidzÎncă nu există evaluări

- Theoretical FrameworkDocument14 paginiTheoretical Frameworkfadi786Încă nu există evaluări

- Income AssignmentDocument5 paginiIncome Assignmentwxwgmumpd100% (1)

- What Are TaxesDocument7 paginiWhat Are TaxesNasir AliÎncă nu există evaluări

- Miller 14e Ppt06 Mac AbbrevDocument50 paginiMiller 14e Ppt06 Mac AbbrevAbdulkerim SadıqovÎncă nu există evaluări

- Research Paper On Income TaxDocument7 paginiResearch Paper On Income Taxafedonkfh100% (1)

- Chap 007Document6 paginiChap 007nasmoe321Încă nu există evaluări

- Tax Research PaperDocument7 paginiTax Research Papergz7gh8h0100% (1)

- Canadian Income TaxationDocument33 paginiCanadian Income Taxationndaguiam100% (1)

- 450 499 PDFDocument44 pagini450 499 PDFSamuelÎncă nu există evaluări

- Q and Answers SDocument8 paginiQ and Answers SPriyesha UnagarÎncă nu există evaluări

- Tax Income, Sunk Cost and Opportunity Cost: Week 13Document46 paginiTax Income, Sunk Cost and Opportunity Cost: Week 13satryoyu811Încă nu există evaluări

- Deferred Taxes: Damona Doye J.C. Hobbs Randy TrueDocument16 paginiDeferred Taxes: Damona Doye J.C. Hobbs Randy TrueYeng SureiyāzuÎncă nu există evaluări

- Aq 10Document58 paginiAq 10Minie KimÎncă nu există evaluări

- Exam III Practice ProblemsDocument10 paginiExam III Practice ProblemsAbdul SattarÎncă nu există evaluări

- Keown Perfin5 Im 04Document23 paginiKeown Perfin5 Im 04a_hslr100% (1)

- Answers To Concept ChecksDocument5 paginiAnswers To Concept ChecksSuhaybAhmed100% (1)

- Tax Law Snapshot 2014Document4 paginiTax Law Snapshot 2014HosameldeenSalehÎncă nu există evaluări

- Assessment 1 - Written or Oral QuestionsDocument7 paginiAssessment 1 - Written or Oral Questionswilson garzonÎncă nu există evaluări

- Lesson 3 MGT207 Escape From Taxation Prepared by SKM (Additional)Document25 paginiLesson 3 MGT207 Escape From Taxation Prepared by SKM (Additional)Alkhair SangcopanÎncă nu există evaluări

- Interview QuestionsDocument12 paginiInterview QuestionsnadeemÎncă nu există evaluări

- JA-03 - Topic 2Document6 paginiJA-03 - Topic 2Kashif MalikÎncă nu există evaluări

- Ebook Economics Today The Macro View 18Th Edition Miller Solutions Manual Full Chapter PDFDocument36 paginiEbook Economics Today The Macro View 18Th Edition Miller Solutions Manual Full Chapter PDFgebbiasadaik100% (9)

- Taxation of Business Entities 4Th Edition Spilker Test Bank Full Chapter PDFDocument67 paginiTaxation of Business Entities 4Th Edition Spilker Test Bank Full Chapter PDFKelseyWeberbdwk100% (8)

- Running Head: INCOME TAXDocument9 paginiRunning Head: INCOME TAXKashif MalikÎncă nu există evaluări

- Tax Policy Center Cruz AnalysisDocument37 paginiTax Policy Center Cruz AnalysisAndrew NeuberÎncă nu există evaluări

- BUS345 Midterm 1 NotesDocument31 paginiBUS345 Midterm 1 NotesՄարիա ՄինասեանÎncă nu există evaluări

- Are You Properly Specifying MaterialsDocument6 paginiAre You Properly Specifying MaterialsDia MujahedÎncă nu există evaluări

- CH 1Document14 paginiCH 1Taha Wael QandeelÎncă nu există evaluări

- Tax AccountingDocument7 paginiTax Accountingjeka0521Încă nu există evaluări

- Group Work #1 With SolutionsDocument3 paginiGroup Work #1 With SolutionsShadi MorakabatiÎncă nu există evaluări

- Dfi 201 Lec Three Managing Taxes Teaching NotesDocument14 paginiDfi 201 Lec Three Managing Taxes Teaching Notesraina mattÎncă nu există evaluări

- Master of Business Administration - MBA Semester 3 Subject Code - MF0012 Subject Name - Taxation Management 4 Credits (Book ID: B1210) Assignment Set-1 (60 Marks)Document10 paginiMaster of Business Administration - MBA Semester 3 Subject Code - MF0012 Subject Name - Taxation Management 4 Credits (Book ID: B1210) Assignment Set-1 (60 Marks)balakalasÎncă nu există evaluări

- International Tax EnvironmentDocument14 paginiInternational Tax EnvironmentAnonymous VstguMKrb50% (2)

- Chapter 1 Individual Income TaxDocument21 paginiChapter 1 Individual Income TaxtravellingÎncă nu există evaluări

- Notes From Cases For CFEDocument8 paginiNotes From Cases For CFEdarknessmindÎncă nu există evaluări

- ACC 470 Taxation Spring 2021 Lecture Notes Module 1Document4 paginiACC 470 Taxation Spring 2021 Lecture Notes Module 1Ahmad Farhad TaneenÎncă nu există evaluări

- Chapter 1 1 CotxaDocument27 paginiChapter 1 1 Cotxafs5kxrcn2gÎncă nu există evaluări

- Accounting Principles and StandardsDocument6 paginiAccounting Principles and StandardswondmagegnÎncă nu există evaluări

- Developing Consistent Tax Bases For Broad-Based Reform: Fiscal Associates, IncDocument10 paginiDeveloping Consistent Tax Bases For Broad-Based Reform: Fiscal Associates, IncThe Washington PostÎncă nu există evaluări

- Income Tax Literature ReviewDocument4 paginiIncome Tax Literature Reviewfvgczbcy100% (1)

- Parametric U.S. Tax Primer 2013.web .CADocument24 paginiParametric U.S. Tax Primer 2013.web .CAGabriella RicardoÎncă nu există evaluări

- Research Paper On Tax ReformDocument5 paginiResearch Paper On Tax Reformc9k7jjfk100% (1)

- How To Compute Income TaxDocument36 paginiHow To Compute Income TaxbrownboomerangÎncă nu există evaluări

- Taxation Principles and PracticesDocument16 paginiTaxation Principles and PracticesAmira NajjarÎncă nu există evaluări

- CH 3Document24 paginiCH 3Eric YaoÎncă nu există evaluări

- Answers To Chapter 12 QuestionsDocument5 paginiAnswers To Chapter 12 QuestionsManuel SantanaÎncă nu există evaluări

- Inventory: Change Comparatives AlsoDocument3 paginiInventory: Change Comparatives AlsoLennyÎncă nu există evaluări

- QB Income TaxesDocument6 paginiQB Income TaxesSarthak MalhotraÎncă nu există evaluări

- Taxation: Presented By: Gaurav Yadav Rishabh Sharma Sandeep SinghDocument32 paginiTaxation: Presented By: Gaurav Yadav Rishabh Sharma Sandeep SinghjurdaÎncă nu există evaluări

- IncomeTaxation VirreyDocument14 paginiIncomeTaxation VirreyAdilyn Grace VirreyÎncă nu există evaluări

- Evaluate The MattersDocument3 paginiEvaluate The MattersLennyÎncă nu există evaluări

- C. Liability - 2, 3 - 4 SessionDocument18 paginiC. Liability - 2, 3 - 4 SessionBareera NasirÎncă nu există evaluări

- Saint Columban College College of Busineess Education Pagadian City Income Taxation Midterm ExaminationsDocument1 paginăSaint Columban College College of Busineess Education Pagadian City Income Taxation Midterm Examinationscarl fuerzasÎncă nu există evaluări

- GST 7th Edition With CorrectionsDocument512 paginiGST 7th Edition With CorrectionsMemeswale BhaiyaaaÎncă nu există evaluări

- Ads 2122 555603 PDFDocument3 paginiAds 2122 555603 PDFHarsh PatelÎncă nu există evaluări

- FX AC 13 Transfer and Business Taxes - INTRUZO ANSWERDocument6 paginiFX AC 13 Transfer and Business Taxes - INTRUZO ANSWERPam IntruzoÎncă nu există evaluări

- Notice of Assessment 2023 04 11 11 51 12 947361Document4 paginiNotice of Assessment 2023 04 11 11 51 12 947361Amelia D. LopezÎncă nu există evaluări

- Tax System of SingaporeDocument19 paginiTax System of SingaporeMahbub HussainÎncă nu există evaluări

- Chapter 26 MCQs On International TaxationDocument26 paginiChapter 26 MCQs On International TaxationSuranjali Tiwari100% (1)

- Following Your Retirement As Senior Vice President of Finance ForDocument1 paginăFollowing Your Retirement As Senior Vice President of Finance Fortrilocksp SinghÎncă nu există evaluări

- 1 - Payslip - July 2020Document2 pagini1 - Payslip - July 2020B.GOUTHAM SABARIESÎncă nu există evaluări

- RR 2-95Document11 paginiRR 2-95cheska_abigail950Încă nu există evaluări

- Payslip To Print - Report Design 10-01-2020Document1 paginăPayslip To Print - Report Design 10-01-2020martin avinaÎncă nu există evaluări

- Circular Refund 142 11 2020Document3 paginiCircular Refund 142 11 2020Gulrana AlamÎncă nu există evaluări

- Book 2Document4 paginiBook 2maurÎncă nu există evaluări

- BIR Ruling DA-445-05Document3 paginiBIR Ruling DA-445-05MaeJoÎncă nu există evaluări

- It - Rebates and ReliefsDocument5 paginiIt - Rebates and ReliefsJitendra VernekarÎncă nu există evaluări

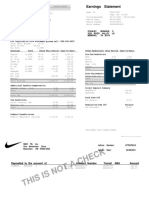

- Earnings Statement: Stanley, Monique S 3232 River Valley LN Memphis, TN 38119Document1 paginăEarnings Statement: Stanley, Monique S 3232 River Valley LN Memphis, TN 38119Miquel JonesÎncă nu există evaluări

- Net Operating Losses (Nols) For Individuals, Estates, and TrustsDocument12 paginiNet Operating Losses (Nols) For Individuals, Estates, and TrustsAdi PutraÎncă nu există evaluări

- TRAIN Law Lecture by Dr. Lim PDFDocument12 paginiTRAIN Law Lecture by Dr. Lim PDFAnonymous 8SUSyvGc3d100% (1)

- Amrutha Feb Salary SlipDocument1 paginăAmrutha Feb Salary SlipAmrutha H NÎncă nu există evaluări

- BRD InvoicesDocument29 paginiBRD InvoicesJTOCCN ORAIÎncă nu există evaluări

- Evolution of Public Finance in IndiaDocument6 paginiEvolution of Public Finance in IndiaVishal Mandaviya100% (1)

- REVENUE MEMORANDUM CIRCULAR NO. 64-2020 Issued On June 24, 2020 CircularizesDocument2 paginiREVENUE MEMORANDUM CIRCULAR NO. 64-2020 Issued On June 24, 2020 CircularizesAceGun'nerÎncă nu există evaluări

- New Jersey Long Term Care Facilities SearchDocument144 paginiNew Jersey Long Term Care Facilities SearchkellyKooÎncă nu există evaluări

- GR: Donations Inter Vivos Are Subject To Donor's Taxes While DonationsDocument8 paginiGR: Donations Inter Vivos Are Subject To Donor's Taxes While DonationsDominic EmbodoÎncă nu există evaluări

- TAX 06.2 - Fringe Benefit TaxDocument2 paginiTAX 06.2 - Fringe Benefit TaxMary Louise CamposanoÎncă nu există evaluări

- TABL2751 Tax Rates 2021 - UpdatedDocument4 paginiTABL2751 Tax Rates 2021 - UpdatedPeper12345Încă nu există evaluări

- Annual Gross IncomeDocument4 paginiAnnual Gross IncomeMarilyn Perez OlañoÎncă nu există evaluări

- Payslip For The Month of May 2021: ICE Data Services India Private LimitedDocument1 paginăPayslip For The Month of May 2021: ICE Data Services India Private Limitedtirupathaiah pÎncă nu există evaluări

- Taxation - Gross Income - Quizzer - 2018 - MayDocument5 paginiTaxation - Gross Income - Quizzer - 2018 - MayKenneth Bryan Tegerero TegioÎncă nu există evaluări

- KafilatDocument1 paginăKafilatBusiness HubÎncă nu există evaluări

- How to get US Bank Account for Non US ResidentDe la EverandHow to get US Bank Account for Non US ResidentEvaluare: 5 din 5 stele5/5 (1)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesDe la EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesÎncă nu există evaluări

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyDe la EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyÎncă nu există evaluări

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProDe la EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProEvaluare: 4.5 din 5 stele4.5/5 (43)

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessDe la EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessEvaluare: 5 din 5 stele5/5 (5)

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationDe la EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationÎncă nu există evaluări

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCDe la EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCEvaluare: 4 din 5 stele4/5 (5)

- Tax Savvy for Small Business: A Complete Tax Strategy GuideDe la EverandTax Savvy for Small Business: A Complete Tax Strategy GuideEvaluare: 5 din 5 stele5/5 (1)

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesDe la EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesEvaluare: 4 din 5 stele4/5 (9)

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipDe la EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipÎncă nu există evaluări

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyDe la EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyEvaluare: 4 din 5 stele4/5 (52)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingDe la EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingEvaluare: 5 din 5 stele5/5 (3)

- Invested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)De la EverandInvested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)Evaluare: 4.5 din 5 stele4.5/5 (43)

- Tax-Free Wealth For Life: How to Permanently Lower Your Taxes And Build More WealthDe la EverandTax-Free Wealth For Life: How to Permanently Lower Your Taxes And Build More WealthÎncă nu există evaluări

- Small Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessDe la EverandSmall Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessÎncă nu există evaluări

- S Corporation ESOP Traps for the UnwaryDe la EverandS Corporation ESOP Traps for the UnwaryÎncă nu există evaluări

- The Payroll Book: A Guide for Small Businesses and StartupsDe la EverandThe Payroll Book: A Guide for Small Businesses and StartupsEvaluare: 5 din 5 stele5/5 (1)

- Make Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionDe la EverandMake Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionÎncă nu există evaluări

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsDe la EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsÎncă nu există evaluări

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsDe la EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsEvaluare: 3.5 din 5 stele3.5/5 (9)

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderDe la EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderÎncă nu există evaluări