S-ar putea să vă placă și

- Sample Resignation LetterDocument15 paginiSample Resignation LetterJohnson Mallibago71% (7)

- Purchases Audit ProgramDocument3 paginiPurchases Audit Programvarghese200795% (22)

- Audit Program For InventoriesDocument2 paginiAudit Program For InventoriesRex Munda Duhaylungsod71% (7)

- CORPORATE PURCHASES AUDITDocument3 paginiCORPORATE PURCHASES AUDITCristina Rosal100% (6)

- Internal Audit Department Audit Program For Cash: Audit Scope: Audit ObjectivesDocument3 paginiInternal Audit Department Audit Program For Cash: Audit Scope: Audit ObjectivesRijo Jacob75% (4)

- ABC Company Audit Program - Receivables Department:: 1) Analytical Procedures-GeneralDocument7 paginiABC Company Audit Program - Receivables Department:: 1) Analytical Procedures-Generalvarghese200779% (14)

- Deposit Operations Audit ProgramDocument9 paginiDeposit Operations Audit Programzubair_z100% (1)

- Audit of InventoryDocument5 paginiAudit of InventoryMa. Hazel Donita DiazÎncă nu există evaluări

- Internal Control QuestionnaireDocument2 paginiInternal Control Questionnairepeterpancanfly100% (3)

- Substantive Tests of Receivables and SalesDocument4 paginiSubstantive Tests of Receivables and SalesKeith Joshua Gabiason100% (1)

- Operational Auditing A Complete Guide - 2021 EditionDe la EverandOperational Auditing A Complete Guide - 2021 EditionÎncă nu există evaluări

- Jawaban CH 14Document28 paginiJawaban CH 14Heltiana Nufriyanti80% (5)

- Dispute Credit Report Inaccuracies FormDocument1 paginăDispute Credit Report Inaccuracies FormJessica Ashley0% (1)

- Audit of The Revenue and Collection CycleDocument5 paginiAudit of The Revenue and Collection CycleLalaine ReyesÎncă nu există evaluări

- 1 Audit Program ExpensesDocument14 pagini1 Audit Program Expensesmaleenda100% (3)

- Audit Program Liabilities Against AssetsDocument11 paginiAudit Program Liabilities Against AssetsRoemi Rivera Robedizo100% (3)

- Audit Program For Property, Plant and Equipment Agency Name: Balance Sheet DateDocument7 paginiAudit Program For Property, Plant and Equipment Agency Name: Balance Sheet DateZosimo Solano100% (3)

- Audit Investment FinancialsDocument3 paginiAudit Investment FinancialsHannah Tudio100% (1)

- Cash Audit ProgramDocument7 paginiCash Audit Program구니타67% (3)

- Audit Programe - InventoryDocument3 paginiAudit Programe - InventoryAnnete Utomo HutabaratÎncă nu există evaluări

- Audit AssertionsDocument3 paginiAudit Assertionsdarknessmind50% (2)

- Internal Audit ProgramDocument8 paginiInternal Audit ProgramKrishna Khandelwal100% (3)

- 143 InchiquinDocument705 pagini143 InchiquinJohn Mikla100% (2)

- Audit of The Revenue and Collection CycleDocument9 paginiAudit of The Revenue and Collection CyclePaulo Lopez100% (3)

- Revenue Cycle Audit Program Final 140810Document11 paginiRevenue Cycle Audit Program Final 140810Pushkar Deodhar100% (1)

- Audit ProgramsDocument492 paginiAudit ProgramsNa-na Bucu100% (7)

- AUDIT PROCEDURES: SUBSTANTIVE TESTING, ANALYTICAL REVIEWS, RELIANCE ON OTHERS (39Document43 paginiAUDIT PROCEDURES: SUBSTANTIVE TESTING, ANALYTICAL REVIEWS, RELIANCE ON OTHERS (39nychan99100% (10)

- Audit ProgramDocument16 paginiAudit Programanon_806011137100% (4)

- Audit Program Physical InventoryDocument7 paginiAudit Program Physical InventoryAditya Bist100% (3)

- Audit Program For Liabilities Format in The PhilippinesDocument2 paginiAudit Program For Liabilities Format in The PhilippinesDeloria Delsa100% (1)

- Accounts Receivable Audit ProceduresDocument5 paginiAccounts Receivable Audit ProceduresVivien NaigÎncă nu există evaluări

- Philippine International Trading Corporation Audit ProgramDocument2 paginiPhilippine International Trading Corporation Audit ProgramNephtali Gonzaga100% (2)

- 1-Processing Orders and Dispatching GoodsDocument5 pagini1-Processing Orders and Dispatching GoodsFaruk H. Irmak100% (1)

- Audit Program For Other IncomeDocument3 paginiAudit Program For Other IncomeCollins O.71% (7)

- Auditing Accounts ReceivableDocument3 paginiAuditing Accounts Receivables1mz100% (4)

- Internal Audit ProgramDocument3 paginiInternal Audit ProgramTakogee100% (1)

- Audit Planning MemoDocument5 paginiAudit Planning MemoAdolph AdolfoÎncă nu există evaluări

- Audit Cash Controls ProceduresDocument7 paginiAudit Cash Controls ProceduresEirene Joy VillanuevaÎncă nu există evaluări

- Audit Program For Inventory RisksDocument4 paginiAudit Program For Inventory RisksCrystal Chow100% (1)

- 5 - Audit of Purchasing Disbursement CycleDocument71 pagini5 - Audit of Purchasing Disbursement CycleJericho Pedragosa100% (1)

- Audit Accrued Expenses ProgramDocument10 paginiAudit Accrued Expenses ProgramPutu Adi NugrahaÎncă nu există evaluări

- Substantive Testing of Cash AssertionsDocument35 paginiSubstantive Testing of Cash AssertionsPamimoomimap Rufila100% (1)

- Audit of Cash On Hand and in BankDocument2 paginiAudit of Cash On Hand and in Bankdidiaen100% (1)

- Chapter03 - Audit of The Revenue and Collection Cycle - UnlockedDocument13 paginiChapter03 - Audit of The Revenue and Collection Cycle - UnlockedMark Kenneth Chan BalicantaÎncă nu există evaluări

- The Audit of LiabilitiesDocument3 paginiThe Audit of LiabilitiesIftekhar Ifte100% (3)

- M3 Assignment Internal Control Group 9 AUDIT SPECIAL INDUSTRYDocument5 paginiM3 Assignment Internal Control Group 9 AUDIT SPECIAL INDUSTRYReginald ValenciaÎncă nu există evaluări

- AUDIT PROCEDURES: 8 STEPSDocument3 paginiAUDIT PROCEDURES: 8 STEPSManish Kumar Sukhija67% (3)

- AP Cash Purchases Audit ProgramDocument5 paginiAP Cash Purchases Audit ProgramYvonne Granada0% (1)

- Permanent Audit FilesDocument4 paginiPermanent Audit FilesRevathi Vadakkedam100% (2)

- Audit Program: A. Planning and Administration SectionDocument3 paginiAudit Program: A. Planning and Administration SectionIzZa Rivera0% (1)

- Ap Audit DocumentDocument7 paginiAp Audit DocumentAnna Tran100% (1)

- Long Term Debt ProgramDocument10 paginiLong Term Debt ProgramSyarif Muhammad Hikmatyar100% (1)

- Audit Program-MSBPLDocument21 paginiAudit Program-MSBPLTasdik MahmudÎncă nu există evaluări

- Accounts Receivable Audit ProgramDocument3 paginiAccounts Receivable Audit Programaliraz101100% (2)

- Audit Program For Inventory Legal Company Name Client: Balance Sheet DateDocument3 paginiAudit Program For Inventory Legal Company Name Client: Balance Sheet DateHannah TudioÎncă nu există evaluări

- Audit of The Revenue and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Revenue and Collection CycleDocument20 paginiAudit of The Revenue and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Revenue and Collection Cycleem cortezÎncă nu există evaluări

- Chapter 14Document30 paginiChapter 14Tumpal Sagala100% (1)

- Audit Revenue Collection Cycle ControlsDocument25 paginiAudit Revenue Collection Cycle ControlsJudy UrciaÎncă nu există evaluări

- Kunci Jawaban Auditing Chapter 14 Arens 15th EditionDocument8 paginiKunci Jawaban Auditing Chapter 14 Arens 15th EditionArfini Lestari100% (2)

- Transaction Cycles Audit TestsDocument8 paginiTransaction Cycles Audit TestsTrixie CasipleÎncă nu există evaluări

- Material AuditingUNITS345Document57 paginiMaterial AuditingUNITS345Vishruthi MuruganÎncă nu există evaluări

- Jawaban CH 14Document28 paginiJawaban CH 14Heltiana NufriyantiÎncă nu există evaluări

- Audit Sales Revenue Cycle ControlsDocument9 paginiAudit Sales Revenue Cycle ControlsMa Tiffany Gura RobleÎncă nu există evaluări

- Ang Appurtenant Kay Parehas Man Ata Na Sa Silingan NamoDocument3 paginiAng Appurtenant Kay Parehas Man Ata Na Sa Silingan NamoJulrick Cubio EgbusÎncă nu există evaluări

- WK 2 Individual AssignmentDocument24 paginiWK 2 Individual AssignmentRhett SageÎncă nu există evaluări

- Jessa M. Alcebar: EmployeeDocument2 paginiJessa M. Alcebar: EmployeeRhett SageÎncă nu există evaluări

- Lycee AdScriptDocument1 paginăLycee AdScriptRhett SageÎncă nu există evaluări

- Bsa BoothDocument6 paginiBsa BoothJulrick Cubio EgbusÎncă nu există evaluări

- Marketing A CadDocument4 paginiMarketing A CadRhett SageÎncă nu există evaluări

- Decision Theory (Group 2)Document31 paginiDecision Theory (Group 2)Rhett SageÎncă nu există evaluări

- Decision Tree AnalysisDocument9 paginiDecision Tree AnalysisRhett SageÎncă nu există evaluări

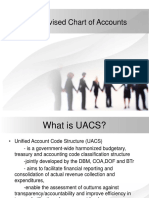

- Gov Acc ReportDocument16 paginiGov Acc ReportJulrick Cubio EgbusÎncă nu există evaluări

- Auditing QuestionsDocument22 paginiAuditing QuestionsRhett Sage100% (1)

- College of Business and Accountancy La Salle University - Ozamiz CityDocument5 paginiCollege of Business and Accountancy La Salle University - Ozamiz CityRhett SageÎncă nu există evaluări

- Jose Rizal'S Literary TalentDocument2 paginiJose Rizal'S Literary TalentRhett SageÎncă nu există evaluări

- Energy Report PhilippinesDocument45 paginiEnergy Report PhilippinesMark100% (1)

- R e G I o N 1Document55 paginiR e G I o N 1Rhett SageÎncă nu există evaluări

- Society Is Who: People Shape Lives Aggregated Patterned Ways Distinguish OtherDocument24 paginiSociety Is Who: People Shape Lives Aggregated Patterned Ways Distinguish OtherRhett SageÎncă nu există evaluări

- Social Stratification JulesDocument11 paginiSocial Stratification JulesRhett SageÎncă nu există evaluări

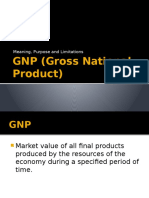

- Macro Econ 1 GNP DefinitionDocument5 paginiMacro Econ 1 GNP DefinitionRhett SageÎncă nu există evaluări

- Data vs. InformationDocument18 paginiData vs. InformationRhett SageÎncă nu există evaluări

- Deviance (IV)Document23 paginiDeviance (IV)Rhett SageÎncă nu există evaluări

- 2.8 Commissioner of Lnternal Revenue vs. Algue, Inc., 158 SCRA 9 (1988)Document10 pagini2.8 Commissioner of Lnternal Revenue vs. Algue, Inc., 158 SCRA 9 (1988)Joseph WallaceÎncă nu există evaluări

- Accounting Calling ListDocument4 paginiAccounting Calling Listsatendra singhÎncă nu există evaluări

- Financial Statement: Funds SummaryDocument1 paginăFinancial Statement: Funds SummarymorganÎncă nu există evaluări

- Jose Omana, 22sep 0854 CaliDocument2 paginiJose Omana, 22sep 0854 CaliAmilcar PérezÎncă nu există evaluări

- Block Class Action LawsuitDocument53 paginiBlock Class Action LawsuitGMG EditorialÎncă nu există evaluări

- English 7 AnnexeDocument4 paginiEnglish 7 AnnexeTASOEUR1234567890Încă nu există evaluări

- Safety data sheet for TL 011 lubricantDocument8 paginiSafety data sheet for TL 011 lubricantXavierÎncă nu există evaluări

- SEMESTER-VIDocument15 paginiSEMESTER-VIshivam_2607Încă nu există evaluări

- Childe Harolds Pilgrimage 432743Document4 paginiChilde Harolds Pilgrimage 432743Parthiva SinhaÎncă nu există evaluări

- Fraud, Internal Controls and Bank ReconciliationDocument15 paginiFraud, Internal Controls and Bank ReconciliationSadia ShithyÎncă nu există evaluări

- Bentham, Jeremy - Offences Against One's SelfDocument25 paginiBentham, Jeremy - Offences Against One's SelfprotonpseudoÎncă nu există evaluări

- Licensure Exams Criminologist ReviewDocument34 paginiLicensure Exams Criminologist ReviewKulot SisonÎncă nu există evaluări

- Maam CoryDocument3 paginiMaam CoryCHERIE ANN APRIL SULITÎncă nu există evaluări

- Peace Consciousness Zumba Dance ActivityDocument3 paginiPeace Consciousness Zumba Dance ActivityKhrylane Joy Sabellano CarbonÎncă nu există evaluări

- 26 VANGUARDIA, Cedric F. - COVID Essay PDFDocument1 pagină26 VANGUARDIA, Cedric F. - COVID Essay PDFEstrell VanguardiaÎncă nu există evaluări

- Business Law and Pil AssignmentDocument13 paginiBusiness Law and Pil Assignmentsurbhirajoria5Încă nu există evaluări

- Mana Angel de Amor BassDocument4 paginiMana Angel de Amor BassToreto SantanaÎncă nu există evaluări

- 해커스토익 김진태선생님 2020년 7월 적중예상문제Document7 pagini해커스토익 김진태선생님 2020년 7월 적중예상문제포도쨈오뚜기Încă nu există evaluări

- Script FiestaDocument5 paginiScript FiestaLourdes Bacay-DatinguinooÎncă nu există evaluări

- Ublox - 2007 - ANTARIS 4 GPS Modules System Integration Manual PDFDocument187 paginiUblox - 2007 - ANTARIS 4 GPS Modules System Integration Manual PDFCenascenascenascenasÎncă nu există evaluări

- John Hankinson AffidavitDocument16 paginiJohn Hankinson AffidavitRtrForumÎncă nu există evaluări

- CIR vs RUEDA Estate Tax Exemption for Spanish NationalDocument1 paginăCIR vs RUEDA Estate Tax Exemption for Spanish NationalAdriel MagpileÎncă nu există evaluări

- RTO ProcessDocument5 paginiRTO Processashutosh mauryaÎncă nu există evaluări

- NaMo Case StudyDocument4 paginiNaMo Case StudyManish ShawÎncă nu există evaluări

- Offer LetterDocument2 paginiOffer LetterIpe ClosaÎncă nu există evaluări

- Quotation Eoi/Rfp/Rft Process Checklist Goods And/Or ServicesDocument7 paginiQuotation Eoi/Rfp/Rft Process Checklist Goods And/Or ServicesTawanda KurasaÎncă nu există evaluări

- Smart Mobs Blog Archive Habermas Blows Off Question About The Internet and The Public SphereDocument3 paginiSmart Mobs Blog Archive Habermas Blows Off Question About The Internet and The Public SpheremaikonchaiderÎncă nu există evaluări