S-ar putea să vă placă și

- Jope 38 SDocument6 paginiJope 38 SRhyka AchmadÎncă nu există evaluări

- Costs of Health Care Across Primary Care Models in Ontario: ResearcharticleDocument9 paginiCosts of Health Care Across Primary Care Models in Ontario: ResearcharticleAswarÎncă nu există evaluări

- HPN6Document50 paginiHPN6Joy MichaelÎncă nu există evaluări

- AHA Patient Centered Medical HomeDocument21 paginiAHA Patient Centered Medical Homein678Încă nu există evaluări

- Better Ways To Pay For Health Care FOCUSDocument8 paginiBetter Ways To Pay For Health Care FOCUSCristhian LarrahondoÎncă nu există evaluări

- AHA BundledPayment ReportDocument20 paginiAHA BundledPayment Reportbikram2128100% (1)

- A Cost-Consequence Analysis ofDocument10 paginiA Cost-Consequence Analysis ofviviana benavidesÎncă nu există evaluări

- The Journal of ArthroplastyDocument4 paginiThe Journal of ArthroplastyLuke Wolfstein HidetoraÎncă nu există evaluări

- Radiology Aco Whitepaper 11-18-14Document9 paginiRadiology Aco Whitepaper 11-18-14api-271257796Încă nu există evaluări

- MCO Three-Year Cost ReportDocument28 paginiMCO Three-Year Cost Reporttinareedreporter100% (1)

- The Effect of Pay-For-Performance in Hospitals: Lessons For Quality ImprovementDocument9 paginiThe Effect of Pay-For-Performance in Hospitals: Lessons For Quality ImprovementMasrun FatanahÎncă nu există evaluări

- Identifying and Resolving Disputes in New Accountable Care SettingsDocument10 paginiIdentifying and Resolving Disputes in New Accountable Care SettingsRothHealthLawÎncă nu există evaluări

- Hess 2016Document9 paginiHess 2016kevin gelaudeÎncă nu există evaluări

- Ramos, Sioco Chapter 25 and 26Document59 paginiRamos, Sioco Chapter 25 and 26DOROTHY ANN SOMBILUNAÎncă nu există evaluări

- Lean Management and U.S. Public Hospital Performance Results From A National SurveyDocument17 paginiLean Management and U.S. Public Hospital Performance Results From A National SurveyArnoldYRPÎncă nu există evaluări

- Population Health ManagementDocument25 paginiPopulation Health ManagementVitreosHealthÎncă nu există evaluări

- Kiss ADocument22 paginiKiss AJean M Huaman FiallegaÎncă nu există evaluări

- Value Based HealthcareDocument48 paginiValue Based HealthcareAsem Shadid100% (1)

- 40 A National Strategy Pp982 990Document9 pagini40 A National Strategy Pp982 990cma909Încă nu există evaluări

- Economic Evaluation Strategies in Telehealth: Obtaining A More Holistic Valuation of Telehealth InterventionsDocument5 paginiEconomic Evaluation Strategies in Telehealth: Obtaining A More Holistic Valuation of Telehealth InterventionsAlejandro CardonaÎncă nu există evaluări

- Arnold Ventures Comment On CY2024 MPFS RuleDocument9 paginiArnold Ventures Comment On CY2024 MPFS RuleArnold VenturesÎncă nu există evaluări

- NR700 Week 7 Initial PostDocument2 paginiNR700 Week 7 Initial PostEllie Vale-SaquieresÎncă nu există evaluări

- Jurnal PRBDocument5 paginiJurnal PRBJoanne AngelinaÎncă nu există evaluări

- Neumann 2010Document3 paginiNeumann 2010Afshan GulÎncă nu există evaluări

- Practice Size, Financial Sharing and Quality of Care: Researcharticle Open AccessDocument9 paginiPractice Size, Financial Sharing and Quality of Care: Researcharticle Open AccessIndah ShofiyahÎncă nu există evaluări

- Aco + PCMH PDFDocument7 paginiAco + PCMH PDFsandhyasrÎncă nu există evaluări

- Health Affairs: For Reprints, Links & Permissions: E-Mail Alerts: To SubscribeDocument11 paginiHealth Affairs: For Reprints, Links & Permissions: E-Mail Alerts: To SubscribeDesak ErnaÎncă nu există evaluări

- Unit 6 Discussion 1 Value of The APRN ModelDocument3 paginiUnit 6 Discussion 1 Value of The APRN ModelYash RamawatÎncă nu există evaluări

- Accurate Measurement of Financial Toxicity Is A Prerequisite To Finding A RemedyDocument3 paginiAccurate Measurement of Financial Toxicity Is A Prerequisite To Finding A Remedyشهر رمزحنÎncă nu există evaluări

- The Utilization of Hospitalists Associated With Compensation: Insourcing Instead of Outsourcing Health CareDocument10 paginiThe Utilization of Hospitalists Associated With Compensation: Insourcing Instead of Outsourcing Health Careadrian_badriÎncă nu există evaluări

- The Top 6 Examples of Quality Improvement in HealthcareDocument7 paginiThe Top 6 Examples of Quality Improvement in HealthcareDennis Junior ChorumaÎncă nu există evaluări

- Cost BenefitDocument11 paginiCost BenefitGabriel EllisÎncă nu există evaluări

- Module 4 - Purchasing Health ServicesDocument18 paginiModule 4 - Purchasing Health Services98b5jc5hgtÎncă nu există evaluări

- Development and Validation of PACICDocument9 paginiDevelopment and Validation of PACICKristen LynchÎncă nu există evaluări

- Wk5 ContentServer - AspDocument11 paginiWk5 ContentServer - Aspvanessaloreni2190Încă nu există evaluări

- EpisodeBasedPayment PerspectivesforConsiderationDocument24 paginiEpisodeBasedPayment PerspectivesforConsiderationHazelnutÎncă nu există evaluări

- Cost Study 2Document3 paginiCost Study 2amira alyÎncă nu există evaluări

- 11 Hospi PerformanceDocument5 pagini11 Hospi PerformancedoctoooorÎncă nu există evaluări

- The Effects of Benefit Design and Managed Care On Care CostsDocument18 paginiThe Effects of Benefit Design and Managed Care On Care CostsKuttiyar YeamsriÎncă nu există evaluări

- Textbook of Urgent Care Management: Chapter 34, Engaging Accountable Care Organizations in Urgent Care CentersDe la EverandTextbook of Urgent Care Management: Chapter 34, Engaging Accountable Care Organizations in Urgent Care CentersÎncă nu există evaluări

- Order#1150365Document10 paginiOrder#1150365Gaddafi PhelixÎncă nu există evaluări

- Costs and Cost Effectiveness of Community Health WorkersDocument16 paginiCosts and Cost Effectiveness of Community Health WorkersMike TeeÎncă nu există evaluări

- 2016 Article 1603Document12 pagini2016 Article 1603Nino AlicÎncă nu există evaluări

- 5 Quality Measures That Matter For Value-Based CareDocument8 pagini5 Quality Measures That Matter For Value-Based CareTuan Nguyen DangÎncă nu există evaluări

- Investigating Discrete Event Simulation Method To Assess The Effectiveness of Wearable Health Monitoring Devices 2014 Procedia Economics and FinanceDocument19 paginiInvestigating Discrete Event Simulation Method To Assess The Effectiveness of Wearable Health Monitoring Devices 2014 Procedia Economics and FinanceRupaliÎncă nu există evaluări

- How To Determine Cost Effective Analysis - RatikaDocument14 paginiHow To Determine Cost Effective Analysis - Ratikatifanny carolinaÎncă nu există evaluări

- Eview F Herapeutics: Economic Evaluations of Clinical Pharmacy Services: 2006 - 2010Document23 paginiEview F Herapeutics: Economic Evaluations of Clinical Pharmacy Services: 2006 - 2010Igor SilvaÎncă nu există evaluări

- Economic Evaluation and Health Sytems StrenghteningDocument11 paginiEconomic Evaluation and Health Sytems StrenghteningDiego Andre Ale MauricioÎncă nu există evaluări

- NURS FPX 6612 Assessment 1 Triple Aim Outcome MeasuresDocument8 paginiNURS FPX 6612 Assessment 1 Triple Aim Outcome MeasuresEmma WatsonÎncă nu există evaluări

- Bodenheimer PrimCareDocument4 paginiBodenheimer PrimCareJaume SanahujaÎncă nu există evaluări

- Activity Based ManagementDocument26 paginiActivity Based Managementfortune90100% (2)

- ACO Final ReportDocument24 paginiACO Final ReportSowmya ParthasarathyÎncă nu există evaluări

- Barreras Facilitadores Implementacion PerinatalDocument13 paginiBarreras Facilitadores Implementacion PerinatalOpeÎncă nu există evaluări

- s12913 022 08783 9Document23 paginis12913 022 08783 9Shuai ShaoÎncă nu există evaluări

- Value and Payment in Sleep Medicine JCSM 2018Document4 paginiValue and Payment in Sleep Medicine JCSM 2018cjbae22Încă nu există evaluări

- Physician Practice Patterns in Primary Care: Do Ownership and Payment Mechanism Matter?Document10 paginiPhysician Practice Patterns in Primary Care: Do Ownership and Payment Mechanism Matter?Bryan SalvaÎncă nu există evaluări

- APM Companion Paper Formatted FINALDocument11 paginiAPM Companion Paper Formatted FINALAnonymous 2zbzrvÎncă nu există evaluări

- Reducing Hospital Readmissions in New York State: A Simulation Analysis of Alternative Payment IncentivesDocument51 paginiReducing Hospital Readmissions in New York State: A Simulation Analysis of Alternative Payment IncentivesjspectorÎncă nu există evaluări

- The New Hospital-Physician Enterprise: Meeting the Challenges of Value-Based CareDe la EverandThe New Hospital-Physician Enterprise: Meeting the Challenges of Value-Based CareÎncă nu există evaluări

- Strategies to Explore Ways to Improve Efficiency While Reducing Health Care CostsDe la EverandStrategies to Explore Ways to Improve Efficiency While Reducing Health Care CostsÎncă nu există evaluări

- International Strategy: Pertemuan 9Document18 paginiInternational Strategy: Pertemuan 9Amira AlhadarÎncă nu există evaluări

- Global Values and Competitive Advantages Within The Scope of International Strategy in Health Care SystemDocument21 paginiGlobal Values and Competitive Advantages Within The Scope of International Strategy in Health Care SystemAmira AlhadarÎncă nu există evaluări

- Rencanakerjaoperasi Onalpetugastkhi2016 Satuankerja:Kloter33Jkg Jeni Spetugas:TkhiDocument25 paginiRencanakerjaoperasi Onalpetugastkhi2016 Satuankerja:Kloter33Jkg Jeni Spetugas:TkhiAmira AlhadarÎncă nu există evaluări

- Restraint Use Among Nursing Home Residents: Cross-Sectional Study and Prospective Cohort StudyDocument18 paginiRestraint Use Among Nursing Home Residents: Cross-Sectional Study and Prospective Cohort StudyAmira AlhadarÎncă nu există evaluări

- Eva Diana, S - H: Curriculum VitaeDocument3 paginiEva Diana, S - H: Curriculum VitaeAmira AlhadarÎncă nu există evaluări

- Item7 KPMG Audit Strategy Planning MemorandumDocument14 paginiItem7 KPMG Audit Strategy Planning Memorandumshane natividad100% (3)

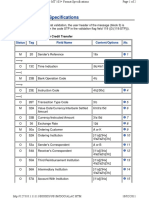

- MT 103+ Format Specifications: MT 103+ Single Customer Credit TransferDocument2 paginiMT 103+ Format Specifications: MT 103+ Single Customer Credit Transferme Nader100% (1)

- (Resume Suit) Creative Resume With Self-Recommendation 11Document3 pagini(Resume Suit) Creative Resume With Self-Recommendation 11প্রমিত সরকারÎncă nu există evaluări

- Order Summary PDFDocument4 paginiOrder Summary PDFAlyaa Syafika NadiraÎncă nu există evaluări

- Jacobs ResumeDocument2 paginiJacobs Resumeapi-384314675Încă nu există evaluări

- Amadeus Basic Reservation & Ticketing Manual - SWDocument27 paginiAmadeus Basic Reservation & Ticketing Manual - SWSwazon HossainÎncă nu există evaluări

- Tn28aa 4446 Tax CH 40764Document1 paginăTn28aa 4446 Tax CH 40764Magesh .RÎncă nu există evaluări

- Recio, Angelic A-IpcrDocument18 paginiRecio, Angelic A-IpcrAngelic RecioÎncă nu există evaluări

- Rtgs Neft FormDocument2 paginiRtgs Neft Formanaga1982Încă nu există evaluări

- 3PL Central 3PL Warehouse Benchmark Report 2021Document34 pagini3PL Central 3PL Warehouse Benchmark Report 2021mohammadÎncă nu există evaluări

- Case Analysis: Netflix: Pricing Decision 2011: Group 3Document7 paginiCase Analysis: Netflix: Pricing Decision 2011: Group 3vedant thakreÎncă nu există evaluări

- Read MeDocument7 paginiRead Meamitdhawan1Încă nu există evaluări

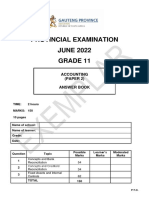

- Gr11 ACC P2 (ENG) June 2022 Answer BookDocument10 paginiGr11 ACC P2 (ENG) June 2022 Answer Bookora mashaÎncă nu există evaluări

- Ynatrwl Nonannexure2022augm25 5532078444 8661400943Document4 paginiYnatrwl Nonannexure2022augm25 5532078444 8661400943INSIGNIA LABS - DATAÎncă nu există evaluări

- Oracle FLEXCUBE AnsswerDocument22 paginiOracle FLEXCUBE AnsswerAMJ TELÎncă nu există evaluări

- PWC Hri Top Healthcare Issues 2017Document23 paginiPWC Hri Top Healthcare Issues 2017devanÎncă nu există evaluări

- Ap 1-4 IsDocument1 paginăAp 1-4 Isapi-334420312Încă nu există evaluări

- NHS Lothian A& EDocument2 paginiNHS Lothian A& EKezia Dugdale MSPÎncă nu există evaluări

- A Study On Performance, Efficiency and Solvency Measurement Towards Retail BankingDocument2 paginiA Study On Performance, Efficiency and Solvency Measurement Towards Retail BankingannamyemÎncă nu există evaluări

- Ofc Ass3Document8 paginiOfc Ass3Ifra MalikÎncă nu există evaluări

- Refer To The Exhibit.: Ape3: Key Server - Customer 2 Ces: Group MembersDocument57 paginiRefer To The Exhibit.: Ape3: Key Server - Customer 2 Ces: Group Membersdany sayedÎncă nu există evaluări

- International Premium Outlets - Cuponera 2022Document7 paginiInternational Premium Outlets - Cuponera 2022Juan P. TestaÎncă nu există evaluări

- 0452 w11 QP 12Document20 pagini0452 w11 QP 12Faisal RaoÎncă nu există evaluări

- Complaint Detail 23109230073779Document2 paginiComplaint Detail 23109230073779Ankit DubeyÎncă nu există evaluări

- Citilink Online Refund IndexDocument1 paginăCitilink Online Refund IndexVaisal DarmawanÎncă nu există evaluări

- Emarketer The Great Realignment StatPackDocument49 paginiEmarketer The Great Realignment StatPackMyriam PerezÎncă nu există evaluări

- 2024 01 31 StatementDocument6 pagini2024 01 31 StatementAlex NeziÎncă nu există evaluări

- Case Study For BADocument14 paginiCase Study For BAHONGHANH DINHCHAUÎncă nu există evaluări

- General Routing Encapsulation (GRE) Protocol 1Document2 paginiGeneral Routing Encapsulation (GRE) Protocol 1Habet MoshmoshÎncă nu există evaluări

- Ericsson - Benchmark Measurements in 5G NR NetworksDocument8 paginiEricsson - Benchmark Measurements in 5G NR Networksyou are awesomeÎncă nu există evaluări