S-ar putea să vă placă și

- 85 Inspiring Ways To Market Your Small BusinessDocument257 pagini85 Inspiring Ways To Market Your Small BusinessSaagar Patil100% (4)

- Adaptive Leadership - Workbook 2Document15 paginiAdaptive Leadership - Workbook 2nitinsoni807359100% (2)

- Consumer Behavior Study Material For MBADocument71 paginiConsumer Behavior Study Material For MBAgirikiruba82% (38)

- Spencer Stuart CMO - Brochureu1Document12 paginiSpencer Stuart CMO - Brochureu1Edmund TanÎncă nu există evaluări

- Emarketer - Retail Trends 2023Document6 paginiEmarketer - Retail Trends 2023jhoni ambaritaÎncă nu există evaluări

- ACTS Business PlanDocument15 paginiACTS Business PlanZsoltÎncă nu există evaluări

- CMS Guide To PassportingDocument44 paginiCMS Guide To PassportingnuseÎncă nu există evaluări

- B2B Marketing (Business Marketing)Document17 paginiB2B Marketing (Business Marketing)Chirag Bansal0% (2)

- ISO 14064 - Awareness Training - 20january2022Document88 paginiISO 14064 - Awareness Training - 20january2022Atul Takarkhede100% (6)

- BSBAMM 2.1 Group 4Document47 paginiBSBAMM 2.1 Group 4sachi u0% (1)

- ISWA WtE State of The Art Report 2012 08 FVDocument209 paginiISWA WtE State of The Art Report 2012 08 FVPéter NovákÎncă nu există evaluări

- ESS8 Data Documentation Report E02 2Document190 paginiESS8 Data Documentation Report E02 2Guillem RicoÎncă nu există evaluări

- Lecture 29 PDFDocument20 paginiLecture 29 PDFSergi Pérez-Rejón GarcíaÎncă nu există evaluări

- Capital MarketDocument60 paginiCapital MarketTatyana KOVPAKÎncă nu există evaluări

- Regional Innovation Scoreboard (RIS) 2009 (Eng) / Indicadores de Innovación Regional 2009 (Ing) / Eskualdeko Berrikuntza Adierazleak 2009 (Ing)Document65 paginiRegional Innovation Scoreboard (RIS) 2009 (Eng) / Indicadores de Innovación Regional 2009 (Ing) / Eskualdeko Berrikuntza Adierazleak 2009 (Ing)EKAI CenterÎncă nu există evaluări

- European Free Trade Association (EFTA)Document15 paginiEuropean Free Trade Association (EFTA)kanikaÎncă nu există evaluări

- Measuring Ireland Progress 2010Document102 paginiMeasuring Ireland Progress 2010uguraliÎncă nu există evaluări

- Smes - Observatory - 2003 - Report4 - en - EOURPEDocument67 paginiSmes - Observatory - 2003 - Report4 - en - EOURPEMoh SaadÎncă nu există evaluări

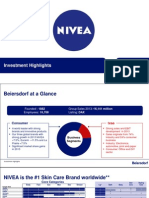

- Reasons To Invest 2014 en BeiersdorfDocument11 paginiReasons To Invest 2014 en BeiersdorfjackyagreenÎncă nu există evaluări

- Nordic Lights Kapitel 4 Bruhn Kjellberg Sandberg CorrectDocument67 paginiNordic Lights Kapitel 4 Bruhn Kjellberg Sandberg CorrectNagy Andrea RekaÎncă nu există evaluări

- MRKM 50 ReposrtingDocument22 paginiMRKM 50 ReposrtingIan Ceazar Abucay AbadiesÎncă nu există evaluări

- B2C E-Commerce StatisticsDocument20 paginiB2C E-Commerce StatisticsMaihong NguyenÎncă nu există evaluări

- Simsambruh Fish CaseDocument16 paginiSimsambruh Fish CaseBruno FardilhaÎncă nu există evaluări

- Iea Statistics: EditionDocument35 paginiIea Statistics: EditionLiliana KennedyÎncă nu există evaluări

- Aai - Ii PDFDocument2 paginiAai - Ii PDFmassimoriserboÎncă nu există evaluări

- NordicDocument59 paginiNordicLuz Eneida CabreraÎncă nu există evaluări

- Newsletter OctoberDocument11 paginiNewsletter OctoberBrian HÎncă nu există evaluări

- Nordic Energy Technology Perspectives 2016Document269 paginiNordic Energy Technology Perspectives 2016gldiasÎncă nu există evaluări

- Social Enterprises and Their Ecosystems in Europe. Updated Country Report SpainDocument130 paginiSocial Enterprises and Their Ecosystems in Europe. Updated Country Report SpainPierre CamiloÎncă nu există evaluări

- Methodology and Organisation of The StudyDocument5 paginiMethodology and Organisation of The Studyanuchandran95Încă nu există evaluări

- Sgs Ind NDT Thermography A4 en 10Document167 paginiSgs Ind NDT Thermography A4 en 10Anonymous Wu6FDjbÎncă nu există evaluări

- Nordic Model - A Success Story?Document15 paginiNordic Model - A Success Story?EmmanuelÎncă nu există evaluări

- ESS1 Data Documentation Report E06 5Document178 paginiESS1 Data Documentation Report E06 5ajp11Încă nu există evaluări

- Measuring The Size and Scope of The Cooperative EconomyDocument9 paginiMeasuring The Size and Scope of The Cooperative EconomyTamahome TakaÎncă nu există evaluări

- Second European Survey On Working Condition.Document368 paginiSecond European Survey On Working Condition.danielÎncă nu există evaluări

- Onu Censo Mundial Cooperativas 2014Document8 paginiOnu Censo Mundial Cooperativas 2014jordmoralesÎncă nu există evaluări

- Aula 2 - Hallin and Mancini 2004Document27 paginiAula 2 - Hallin and Mancini 2004Dan NamiseÎncă nu există evaluări

- Case 1 Gucci Organization and Strategy 2017Document48 paginiCase 1 Gucci Organization and Strategy 2017Indrani PanÎncă nu există evaluări

- ISWA6 7-000-2 WtE State of The Art Report 2012 Revised November 2013 PDFDocument210 paginiISWA6 7-000-2 WtE State of The Art Report 2012 Revised November 2013 PDFCesar LopezÎncă nu există evaluări

- TableauBordInnovationUE 2014 enDocument100 paginiTableauBordInnovationUE 2014 enindustrie_technosÎncă nu există evaluări

- The European Foundry Industry 2019 Annual Statistics and National Reports 1Document112 paginiThe European Foundry Industry 2019 Annual Statistics and National Reports 1Ryan KnightÎncă nu există evaluări

- Nature Energy SupplementaryDocument10 paginiNature Energy SupplementaryEcho TangÎncă nu există evaluări

- Policy Innovation in Refugee IntegrationDocument95 paginiPolicy Innovation in Refugee IntegrationBalan AndreiÎncă nu există evaluări

- ESS8 Appendix A1 E02 3Document73 paginiESS8 Appendix A1 E02 3Guillem RicoÎncă nu există evaluări

- Contributions of "Knowledge" in World Economy: Gabriela-Liliana CIOBANDocument7 paginiContributions of "Knowledge" in World Economy: Gabriela-Liliana CIOBANAlla BeeÎncă nu există evaluări

- Vision Report enDocument116 paginiVision Report enVikas SinghÎncă nu există evaluări

- IEA 2014 Energy Statistics of OECD CountriesDocument431 paginiIEA 2014 Energy Statistics of OECD CountriesLoading YuriÎncă nu există evaluări

- ESS8 Data Documentation Report E01 0Document150 paginiESS8 Data Documentation Report E01 0ajp11Încă nu există evaluări

- ICOLD EurClub - Dam Legislation Report - Dec 2017Document96 paginiICOLD EurClub - Dam Legislation Report - Dec 2017Zito CarlosÎncă nu există evaluări

- Assignment - II PSDocument5 paginiAssignment - II PSParvathyÎncă nu există evaluări

- Electric Transport in The NetherlandsDocument44 paginiElectric Transport in The NetherlandsMaryam AsdÎncă nu există evaluări

- Manual: Energy StatisticsDocument196 paginiManual: Energy StatisticsFrancescoMoriÎncă nu există evaluări

- International TradeDocument10 paginiInternational Tradehasan jamiÎncă nu există evaluări

- Roofing Materials Full Product Catalog and Technical Info PDFDocument65 paginiRoofing Materials Full Product Catalog and Technical Info PDFFrank SongÎncă nu există evaluări

- Factors DeterminingDocument52 paginiFactors DeterminingSantosh MahatoÎncă nu există evaluări

- Enel Risultati FinanziariDocument46 paginiEnel Risultati FinanziariEnrico BenassiÎncă nu există evaluări

- Swedbank Annual Report 2008Document135 paginiSwedbank Annual Report 2008andrea_baffoÎncă nu există evaluări

- Energy Balances of OECD Countries 2010-6110043eDocument314 paginiEnergy Balances of OECD Countries 2010-6110043eb1_mit297Încă nu există evaluări

- Ce 2013Document80 paginiCe 2013mhldcnÎncă nu există evaluări

- Questions and Answers On Gross Domestic Product (GDP) : MEMO/07/472Document4 paginiQuestions and Answers On Gross Domestic Product (GDP) : MEMO/07/472kelvinÎncă nu există evaluări

- Chapter 6 - An Overview of Market Struture Based Upon Existing SourcesDocument15 paginiChapter 6 - An Overview of Market Struture Based Upon Existing Sourcesempower93 empower93Încă nu există evaluări

- Growing Unequal PDFDocument309 paginiGrowing Unequal PDFNincen Figueroa UrquizaÎncă nu există evaluări

- Leather Research PDFDocument162 paginiLeather Research PDFVishnuGundaÎncă nu există evaluări

- Dynamic Panel Data Analysis of European Tourism Demand in MalaysiaDocument15 paginiDynamic Panel Data Analysis of European Tourism Demand in MalaysiaAzizur RohmanÎncă nu există evaluări

- CodebookDocument316 paginiCodebookalanÎncă nu există evaluări

- Nordic Media Trends 11Document194 paginiNordic Media Trends 11JessyvsÎncă nu există evaluări

- Emerging Countries & World Summary: Emerging Countries and World SummaryDe la EverandEmerging Countries & World Summary: Emerging Countries and World SummaryÎncă nu există evaluări

- America, Japan & Asia Pacific: America, Japan & Asia PacificDe la EverandAmerica, Japan & Asia Pacific: America, Japan & Asia PacificÎncă nu există evaluări

- Products and Services For Consumers: True / False QuestionsDocument65 paginiProducts and Services For Consumers: True / False QuestionsThúy HiềnÎncă nu există evaluări

- EPGDM - MM - Shrutika Shriniwas Pobatti - PROVEPGDM-04-21090 - AssignmentDocument9 paginiEPGDM - MM - Shrutika Shriniwas Pobatti - PROVEPGDM-04-21090 - AssignmentSHRUTIÎncă nu există evaluări

- KPMG - Time To Open My Wallet or Not (July 2020)Document23 paginiKPMG - Time To Open My Wallet or Not (July 2020)Rural Marketing Association of IndiaÎncă nu există evaluări

- Viber For Business - Advertising Solutions-2Document24 paginiViber For Business - Advertising Solutions-2htetarkar022023Încă nu există evaluări

- Resume - Narendra Maheshwari (New) PDFDocument3 paginiResume - Narendra Maheshwari (New) PDFNarendra MaheshwariÎncă nu există evaluări

- Management Research Review: Article InformationDocument39 paginiManagement Research Review: Article InformationAnissa RachmaniaÎncă nu există evaluări

- Project ON STP in Nestle: Amity School of Business, NoidaDocument35 paginiProject ON STP in Nestle: Amity School of Business, NoidaSandeep PrabhakarÎncă nu există evaluări

- Bennett Advisory Services Brochure (Omaltaf@hotmail - Com)Document12 paginiBennett Advisory Services Brochure (Omaltaf@hotmail - Com)Osama AltafÎncă nu există evaluări

- Job Details: Marketing Manager, SpriteDocument11 paginiJob Details: Marketing Manager, SpriteVinod JoshiÎncă nu există evaluări

- Business Strategy: Kellogg's CompanyDocument14 paginiBusiness Strategy: Kellogg's CompanyRAJARSHI ChakrabortyÎncă nu există evaluări

- Mouthfreshener 111120055303 Phpapp01Document10 paginiMouthfreshener 111120055303 Phpapp01Shreyansh RavalÎncă nu există evaluări

- Article For Article SubmissionDocument8 paginiArticle For Article SubmissionShonali ChatterjeeÎncă nu există evaluări

- Grohe India PVTDocument34 paginiGrohe India PVTRaju PatowaryÎncă nu există evaluări

- HSBC Report On Two-Wheeler IndustryDocument64 paginiHSBC Report On Two-Wheeler Industrymanishsharma33Încă nu există evaluări

- Marketing Communications Mix Assessment 2Document10 paginiMarketing Communications Mix Assessment 2Lee RaesideÎncă nu există evaluări

- Group 3 BMC AHPL PresentationDocument18 paginiGroup 3 BMC AHPL PresentationPankaj ChandiramaniÎncă nu există evaluări

- Direct & Database MarketingDocument48 paginiDirect & Database MarketingNihar VoraÎncă nu există evaluări

- Beyond Factory Walls 2009 Timberland ReportDocument24 paginiBeyond Factory Walls 2009 Timberland ReportKenn KabiruÎncă nu există evaluări

- Flip Case StudyDocument30 paginiFlip Case StudyMarko ĆorićÎncă nu există evaluări

- Group 3 - Term Paper (Keya Cosmetic)Document17 paginiGroup 3 - Term Paper (Keya Cosmetic)Afsana RahmanÎncă nu există evaluări

- Competition Analysis of IT SectorDocument60 paginiCompetition Analysis of IT SectorNadarNaveenÎncă nu există evaluări

- Analyzing The Marketing Activities of NestleDocument12 paginiAnalyzing The Marketing Activities of NestleGiang NgôÎncă nu există evaluări