S-ar putea să vă placă și

- Impact Assessment AAK: Taxes and the Local Manufacture of PesticidesDe la EverandImpact Assessment AAK: Taxes and the Local Manufacture of PesticidesÎncă nu există evaluări

- Impact assessment AAK: The impact of Tax on the Local Manufacture of PesticidesDe la EverandImpact assessment AAK: The impact of Tax on the Local Manufacture of PesticidesÎncă nu există evaluări

- Manila: The President of The PhilippinesDocument3 paginiManila: The President of The PhilippinesmeriiÎncă nu există evaluări

- Salient Features: BUDGET 2021-22 Sales Tax Act 1990Document11 paginiSalient Features: BUDGET 2021-22 Sales Tax Act 1990sundasÎncă nu există evaluări

- Comparative Analysis of Financial Bills: C C C CCDocument5 paginiComparative Analysis of Financial Bills: C C C CCpdabriwalÎncă nu există evaluări

- Memorandum Train LawDocument23 paginiMemorandum Train LawKweeng Tayrus FaelnarÎncă nu există evaluări

- Budget 2009Document7 paginiBudget 2009JayÎncă nu există evaluări

- Salient Features For The Budget 2010-11Document11 paginiSalient Features For The Budget 2010-11kaashifhassanÎncă nu există evaluări

- Coke Is An Important Industrial Product, Used Mainly in Iron Ore Smelting, But Also As A Fuel in Stoves and Forges When Air Pollution Is A ConcernDocument6 paginiCoke Is An Important Industrial Product, Used Mainly in Iron Ore Smelting, But Also As A Fuel in Stoves and Forges When Air Pollution Is A ConcernGf NavarroÎncă nu există evaluări

- Proposed Reforms On Value-Added Tax: Executive Order (EO) No. 273Document53 paginiProposed Reforms On Value-Added Tax: Executive Order (EO) No. 273Pari DelictoÎncă nu există evaluări

- Garcia V Executive SecretaryDocument8 paginiGarcia V Executive Secretarycarla_cariaga_2Încă nu există evaluări

- Income Tax: 2013-14 Brief Commentary On Major Proposed Amendments Salary Income TaxationDocument10 paginiIncome Tax: 2013-14 Brief Commentary On Major Proposed Amendments Salary Income TaxationUmar SulemanÎncă nu există evaluări

- Salient Features CustomsDocument5 paginiSalient Features Customssaqlain3210Încă nu există evaluări

- Salient Features: Customs Budgetary Measures 2008-09Document16 paginiSalient Features: Customs Budgetary Measures 2008-09sadiajanÎncă nu există evaluări

- 1 Garcia vs. Executive Secretary (GR No. 101273)Document7 pagini1 Garcia vs. Executive Secretary (GR No. 101273)yra crisostomoÎncă nu există evaluări

- (G1) Highlights of The Train Law Ra 10963 and NIRCDocument37 pagini(G1) Highlights of The Train Law Ra 10963 and NIRCFiliusdeiÎncă nu există evaluări

- Salient Features Income Tax)Document5 paginiSalient Features Income Tax)bbaahmad89Încă nu există evaluări

- New Decree 1277-12Document4 paginiNew Decree 1277-12Sebastian MaggioÎncă nu există evaluări

- Tax - Case DigestsDocument13 paginiTax - Case DigestsSkylee SoÎncă nu există evaluări

- Salient Feature - FY 2019-20Document30 paginiSalient Feature - FY 2019-20fawad iqbalÎncă nu există evaluări

- Tax Reform For Acceleration and Inclusion (Train) Act (RA # 10963)Document4 paginiTax Reform For Acceleration and Inclusion (Train) Act (RA # 10963)thepoetsedgeÎncă nu există evaluări

- Sen. Ralph G. Recto Renz Michael Anthony C.Ocampo Informatics CollegeDocument4 paginiSen. Ralph G. Recto Renz Michael Anthony C.Ocampo Informatics CollegeRich De Mesa OcampoÎncă nu există evaluări

- TRAIN Law PDFDocument124 paginiTRAIN Law PDFKrizel BianoÎncă nu există evaluări

- Taxation of OilDocument81 paginiTaxation of OilPrince McGershonÎncă nu există evaluări

- Guiding PrinciplesDocument19 paginiGuiding PrinciplesTelle MarieÎncă nu există evaluări

- Module 10 Business Taxation Required ReadingDocument17 paginiModule 10 Business Taxation Required Readingfranz mallariÎncă nu există evaluări

- Train Law Excise Tax 1Document29 paginiTrain Law Excise Tax 1Assuy AsufraÎncă nu există evaluări

- Salient Features: Customs Budgetary Measures 2007-08Document17 paginiSalient Features: Customs Budgetary Measures 2007-08sadiajanÎncă nu există evaluări

- Garcia vs. Executive SecretaryDocument8 paginiGarcia vs. Executive SecretaryMoonÎncă nu există evaluări

- Excise, DST Syllabi 17-18 Train LawDocument19 paginiExcise, DST Syllabi 17-18 Train LawTelle MarieÎncă nu există evaluări

- TRAIN LAW - 3.9.18 - Laguna ChapterDocument408 paginiTRAIN LAW - 3.9.18 - Laguna ChapterDeoshel AlagonÎncă nu există evaluări

- Law of Taxation ProjDocument14 paginiLaw of Taxation ProjAniket SachanÎncă nu există evaluări

- Global Petroleum Tax GuideDocument14 paginiGlobal Petroleum Tax Guidemuki10Încă nu există evaluări

- Budget 2009: KIA AssociatesDocument16 paginiBudget 2009: KIA Associatesalmas_sshahidÎncă nu există evaluări

- Central Excise & Customs: Salient Features of Budgetary ChangesDocument5 paginiCentral Excise & Customs: Salient Features of Budgetary ChangesYunus ShaikhÎncă nu există evaluări

- HighLights ST FEDocument34 paginiHighLights ST FEShakir MuhammadÎncă nu există evaluări

- TRAIN (Changes) ???? Pages 2, 5 - 7Document4 paginiTRAIN (Changes) ???? Pages 2, 5 - 7blackmail1Încă nu există evaluări

- Budget Commentary 2021-22Document21 paginiBudget Commentary 2021-22Tahera AbbotabadwalaÎncă nu există evaluări

- Train TaxDocument11 paginiTrain TaxLucela InocÎncă nu există evaluări

- Salient Features For Income TaxDocument6 paginiSalient Features For Income TaxRimsha AslamÎncă nu există evaluări

- Vat Ruling No 7-2006Document2 paginiVat Ruling No 7-2006MCÎncă nu există evaluări

- Republic Act 8479 and 6361Document16 paginiRepublic Act 8479 and 6361MayAnn SisonÎncă nu există evaluări

- What To Know Re Vat Reform Law (Ra 9337)Document5 paginiWhat To Know Re Vat Reform Law (Ra 9337)Jamie ArquiroÎncă nu există evaluări

- Required ReadingDocument11 paginiRequired ReadingJennelyn Asas PagaduanÎncă nu există evaluări

- SPE-193470-MS Analysis of Government and Contractor Take Statistics in The Proposed Petroleum Industry Fiscal BillDocument14 paginiSPE-193470-MS Analysis of Government and Contractor Take Statistics in The Proposed Petroleum Industry Fiscal Billipali4christ_5308248Încă nu există evaluări

- April 2010 Tax BriefDocument10 paginiApril 2010 Tax BriefAna MergalÎncă nu există evaluări

- Nigeria's Government Considers Petroleum Industry Bill 2020, A New Framework For The Oil and Gas SectorDocument6 paginiNigeria's Government Considers Petroleum Industry Bill 2020, A New Framework For The Oil and Gas Sectorpradeep s gillÎncă nu există evaluări

- Policy Analysis - Train LawDocument6 paginiPolicy Analysis - Train LawJoyce GemÎncă nu există evaluări

- Ryhuqphqwri, QGLD 0Lqlvwu/Ri) LQDQFH 'Hsduwphqwri5Hyhqxh &Hqwudo%Rdugri'Luhfw7D (HVDocument24 paginiRyhuqphqwri, QGLD 0Lqlvwu/Ri) LQDQFH 'Hsduwphqwri5Hyhqxh &Hqwudo%Rdugri'Luhfw7D (HVNiraj JainÎncă nu există evaluări

- Transfer Tax Train Law 2Document6 paginiTransfer Tax Train Law 2Mark DasiganÎncă nu există evaluări

- PSX Budget ProposalDocument28 paginiPSX Budget ProposalAhmed WaleedÎncă nu există evaluări

- Domestic Tax Laws of Uganda 2016. Updated and Tracked Compendium.Document370 paginiDomestic Tax Laws of Uganda 2016. Updated and Tracked Compendium.URAuganda100% (8)

- Taxation 2015 CasesDocument21 paginiTaxation 2015 CasesErika Mae GumabolÎncă nu există evaluări

- Customs and Tariff Fees-EGDocument3 paginiCustoms and Tariff Fees-EGMina BebawyÎncă nu există evaluări

- Pre 4 - Audit of The Gas, Petroleum, and Oil Sectors (Powerpoint)Document59 paginiPre 4 - Audit of The Gas, Petroleum, and Oil Sectors (Powerpoint)nefael lanciolaÎncă nu există evaluări

- Royalty HandbookDocument189 paginiRoyalty Handbooktuandat_hpÎncă nu există evaluări

- Taxation: The Train Law in FocusDocument9 paginiTaxation: The Train Law in FocusLj Paul YumulÎncă nu există evaluări

- 1 DigestedDocument5 pagini1 DigestedYvet KatÎncă nu există evaluări

- Train Law Additional ReadingsDocument2 paginiTrain Law Additional ReadingsMaria Angelica PanongÎncă nu există evaluări

- VatDocument9 paginiVatGianna CantoriaÎncă nu există evaluări

- Criminal Law ReviewDocument80 paginiCriminal Law ReviewGianna CantoriaÎncă nu există evaluări

- Commrev CompilationDocument11 paginiCommrev CompilationAC SubijanoÎncă nu există evaluări

- People Vs MamatakDocument2 paginiPeople Vs MamatakGianna CantoriaÎncă nu există evaluări

- 2 Reasons For Prescribed Fire in Forest Resource ManagementDocument11 pagini2 Reasons For Prescribed Fire in Forest Resource ManagementGianna CantoriaÎncă nu există evaluări

- 4 BT Talong Case International Service For The Acquisition of Agri Biotech Applications Inc Et Al V Greenpeace Southeast Asia Philippines Et Al BT Talong CaDocument7 pagini4 BT Talong Case International Service For The Acquisition of Agri Biotech Applications Inc Et Al V Greenpeace Southeast Asia Philippines Et Al BT Talong CaGianna CantoriaÎncă nu există evaluări

- TRAIN Part 2 - Value-Added TaxDocument42 paginiTRAIN Part 2 - Value-Added TaxGianna CantoriaÎncă nu există evaluări

- TRAIN Part 7 - Vetoed ProvisionsDocument11 paginiTRAIN Part 7 - Vetoed ProvisionsGianna CantoriaÎncă nu există evaluări

- A. Assessment B. Collection: Remedies of The GovernmentDocument10 paginiA. Assessment B. Collection: Remedies of The GovernmentGianna CantoriaÎncă nu există evaluări

- TRAIN Part 4 - Documentary Stamp TaxDocument21 paginiTRAIN Part 4 - Documentary Stamp TaxGianna CantoriaÎncă nu există evaluări

- TRAIN Part 6 - Other Tax ComplianceDocument20 paginiTRAIN Part 6 - Other Tax ComplianceGianna Cantoria100% (1)

- Chapter 6 HRDocument21 paginiChapter 6 HRGianna CantoriaÎncă nu există evaluări

- TRAIN Part 1 - Income TaxDocument53 paginiTRAIN Part 1 - Income TaxGianna CantoriaÎncă nu există evaluări

- TRAIN Part 3 - Estate and Donors TaxDocument20 paginiTRAIN Part 3 - Estate and Donors TaxGianna CantoriaÎncă nu există evaluări

- Section 19 of Batas Pambansa Blg. 129Document3 paginiSection 19 of Batas Pambansa Blg. 129Gianna CantoriaÎncă nu există evaluări

- Insurance OutlineDocument10 paginiInsurance OutlineGianna CantoriaÎncă nu există evaluări

- Cases SummaryDocument2 paginiCases SummaryGianna CantoriaÎncă nu există evaluări

- Digest FormatDocument2 paginiDigest FormatGianna CantoriaÎncă nu există evaluări

- Labor Law II Session #2Document2 paginiLabor Law II Session #2Gianna CantoriaÎncă nu există evaluări

- Group 1 - Batch 3 - Cases 1 To 3Document8 paginiGroup 1 - Batch 3 - Cases 1 To 3Gianna CantoriaÎncă nu există evaluări

- Assigned Case - Bank of Luzon v. Reyes Sample DraftDocument15 paginiAssigned Case - Bank of Luzon v. Reyes Sample DraftKim Roque-AquinoÎncă nu există evaluări

- Digest FormatDocument2 paginiDigest FormatGianna CantoriaÎncă nu există evaluări

- Section 19 of Batas Pambansa Blg. 129Document3 paginiSection 19 of Batas Pambansa Blg. 129Gianna CantoriaÎncă nu există evaluări

- Weeks 4,5,7,8Document8 paginiWeeks 4,5,7,8Gianna CantoriaÎncă nu există evaluări

- Human Rights - General Considerations-1Document166 paginiHuman Rights - General Considerations-1Gianna CantoriaÎncă nu există evaluări

- Cantoria CrimProDigestDocument6 paginiCantoria CrimProDigestGianna CantoriaÎncă nu există evaluări

- Overview:: Name of The Case: Asylum Case (Columbia/Peru) Year of The Decision: 1950 and Court: IcjDocument37 paginiOverview:: Name of The Case: Asylum Case (Columbia/Peru) Year of The Decision: 1950 and Court: IcjGianna CantoriaÎncă nu există evaluări

- PEOPLE Vs MARTI, GR 81561 Jan.18.1991 - Case Digest - CantoriaDocument2 paginiPEOPLE Vs MARTI, GR 81561 Jan.18.1991 - Case Digest - CantoriaGianna CantoriaÎncă nu există evaluări

- Cases For Sources of International Law With Short Summary2Document37 paginiCases For Sources of International Law With Short Summary2Gianna CantoriaÎncă nu există evaluări

- Compagnie Financiere Sucres Et Denrees v. CIRDocument8 paginiCompagnie Financiere Sucres Et Denrees v. CIRAdi SalvadorÎncă nu există evaluări

- Chapter 10 Tabag - Serrano NotesDocument5 paginiChapter 10 Tabag - Serrano NotesNatalie SerranoÎncă nu există evaluări

- Financial Statement (Short Form) Division: (Attach A Completed Schedule A)Document4 paginiFinancial Statement (Short Form) Division: (Attach A Completed Schedule A)rfortier6760Încă nu există evaluări

- Taxation of GPP Estates TrustsDocument7 paginiTaxation of GPP Estates TrustsSharn Linzi Buan MontañoÎncă nu există evaluări

- CN 282Document1 paginăCN 282f4m0uqb2riÎncă nu există evaluări

- CHAPTER 13 A - Regular Allowable Itemized DeductionsDocument4 paginiCHAPTER 13 A - Regular Allowable Itemized DeductionsDeviane CalabriaÎncă nu există evaluări

- Monthly Remittance Return of Creditable Income Taxes Withheld (Expanded)Document3 paginiMonthly Remittance Return of Creditable Income Taxes Withheld (Expanded)appipinnim100% (2)

- Acc 496 Chapter 6Document2 paginiAcc 496 Chapter 6Abdul HassonÎncă nu există evaluări

- Qualified Dividends and Capital Gains WorksheetDocument1 paginăQualified Dividends and Capital Gains WorksheetBetty Ann LegerÎncă nu există evaluări

- English PB 23Document2 paginiEnglish PB 23bilal mustafa100% (1)

- Gross Income Inc Exc DedDocument9 paginiGross Income Inc Exc DedMelbert BallaraÎncă nu există evaluări

- Rent Invoice: INVOICE NO. 662346692 DELIVERY DATE Jan 01, 2024 02:36:00 ACCOUNT NO. 6627181Document1 paginăRent Invoice: INVOICE NO. 662346692 DELIVERY DATE Jan 01, 2024 02:36:00 ACCOUNT NO. 6627181Chinmay BeheraÎncă nu există evaluări

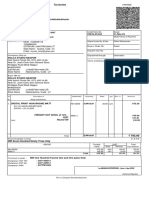

- Tax Invoice: 1046.17 Total Invoice Amount RsDocument2 paginiTax Invoice: 1046.17 Total Invoice Amount RsAayush AggarwalÎncă nu există evaluări

- Magistr OlDocument1 paginăMagistr OlHuseyn HiseynliÎncă nu există evaluări

- Mob Advance - Delhi PDFDocument1 paginăMob Advance - Delhi PDFsyed sulemanÎncă nu există evaluări

- Return of Organization Exempt From Income TaxDocument31 paginiReturn of Organization Exempt From Income TaxRBJÎncă nu există evaluări

- Income Taxation Reviewer PDFDocument65 paginiIncome Taxation Reviewer PDFPaulo Joshua Abasolo BetacheÎncă nu există evaluări

- E-Way Bill - TamDocument1 paginăE-Way Bill - TamPrashant GuptaÎncă nu există evaluări

- Tax 1.1Document13 paginiTax 1.1Mheryza De Castro PabustanÎncă nu există evaluări

- CS Professional Income Tax Handwritten Class NotesDocument240 paginiCS Professional Income Tax Handwritten Class Notesmittalansh899Încă nu există evaluări

- WWVVVDocument1 paginăWWVVVAnonymous HeN9yzg3Încă nu există evaluări

- Tax AssignmentDocument7 paginiTax AssignmentNaiha AbidÎncă nu există evaluări

- It 48Document40 paginiIt 48Robert Daysor BancifraÎncă nu există evaluări

- 26 USC 6033a3Document2 pagini26 USC 6033a3helpinghandoutreach100% (3)

- Electricity BillDocument1 paginăElectricity BillPaul LivesÎncă nu există evaluări

- (Digest) CIR v. AlgueDocument2 pagini(Digest) CIR v. AlgueHomer SimpsonÎncă nu există evaluări

- GSTR 3B Vs GSTR 1 Tax Comparison Report 2Document14 paginiGSTR 3B Vs GSTR 1 Tax Comparison Report 2Mani SinghÎncă nu există evaluări

- Income Taxation of Employees in The PhilippinesDocument4 paginiIncome Taxation of Employees in The Philippinesjoan villacastinÎncă nu există evaluări

- Recruiter Lite: Confirm Your Billing CycleDocument1 paginăRecruiter Lite: Confirm Your Billing Cycleజయ సింహ కసిరెడ్డిÎncă nu există evaluări

- Akshay Finance PRJCTDocument38 paginiAkshay Finance PRJCTsamarthadhkariÎncă nu există evaluări