S-ar putea să vă placă și

- Southern Rock Insurance Company 2014 AccountsDocument28 paginiSouthern Rock Insurance Company 2014 AccountsMarcus LerouxÎncă nu există evaluări

- Covernote SA665687 1630735019386Document2 paginiCovernote SA665687 1630735019386Firoj ShaikhÎncă nu există evaluări

- 7S Electronic Payout MandateDocument1 pagină7S Electronic Payout MandateMatri SearchÎncă nu există evaluări

- Condolence and Requirement Letter PDFDocument2 paginiCondolence and Requirement Letter PDFWaseemÎncă nu există evaluări

- Q&A For Permanent Secretary For Before Meeting With Moy Park in 2014Document9 paginiQ&A For Permanent Secretary For Before Meeting With Moy Park in 2014Marcus LerouxÎncă nu există evaluări

- Dom Care InfoDocument3 paginiDom Care InfoAnakha AbeyÎncă nu există evaluări

- Recruitment Policy and Procedure Nov 06Document16 paginiRecruitment Policy and Procedure Nov 06maswoodÎncă nu există evaluări

- Project On Maxlife InsuranceDocument41 paginiProject On Maxlife Insurancejigna kelaÎncă nu există evaluări

- The Control of Noise at Work Regulations 2005: 2005 No.1643 Health and SafetyDocument16 paginiThe Control of Noise at Work Regulations 2005: 2005 No.1643 Health and SafetyDorae ChuÎncă nu există evaluări

- HIH Insurance GroupDocument41 paginiHIH Insurance Groupgigito100% (1)

- DPR LP Guidelines 2015 Edition v.16!04!2015Document19 paginiDPR LP Guidelines 2015 Edition v.16!04!2015Txkti Babel100% (1)

- Sector Risk Assessment For Registered BanksDocument56 paginiSector Risk Assessment For Registered BanksmutasimÎncă nu există evaluări

- Ethics in The Insurance Sector (23 Pages)Document24 paginiEthics in The Insurance Sector (23 Pages)Al-Imran Bin KhodadadÎncă nu există evaluări

- Northern Ireland Synopsis of Responses To Nitrates Action Plan For 2015 To 2018Document45 paginiNorthern Ireland Synopsis of Responses To Nitrates Action Plan For 2015 To 2018Marcus LerouxÎncă nu există evaluări

- Almaha Ceramics ProspectusDocument148 paginiAlmaha Ceramics ProspectusAbdoKhaledÎncă nu există evaluări

- Def Pen Handbook 2017Document392 paginiDef Pen Handbook 2017vijaya36fÎncă nu există evaluări

- NOISE INSPECTION GUIDANCEDocument24 paginiNOISE INSPECTION GUIDANCERamadan KareemÎncă nu există evaluări

- Green Delta Insurance PDFDocument98 paginiGreen Delta Insurance PDFSayeedMdAzaharulIslamÎncă nu există evaluări

- PWC Mutual Fund Regulatory Services Brochure PDFDocument31 paginiPWC Mutual Fund Regulatory Services Brochure PDFramaraajunÎncă nu există evaluări

- Protocol for ambient noise monitoringDocument5 paginiProtocol for ambient noise monitoringDavid ThangaduraiÎncă nu există evaluări

- Aviva Life InsuranceDocument3 paginiAviva Life InsuranceumashankarsinghÎncă nu există evaluări

- The Relevance of Mathematics in Insurance Industry PDFDocument65 paginiThe Relevance of Mathematics in Insurance Industry PDFMeriÎncă nu există evaluări

- Understanding Financial Statements of Life Insurance Corporation of IndiaDocument50 paginiUnderstanding Financial Statements of Life Insurance Corporation of IndiaSaurabh TayalÎncă nu există evaluări

- Africa Banking SurveyDocument88 paginiAfrica Banking SurveyShailendra DwiwediÎncă nu există evaluări

- Lic Surrender SamplerDocument4 paginiLic Surrender SamplerjeevarvinderÎncă nu există evaluări

- General Insurance Claim RequirementDocument13 paginiGeneral Insurance Claim RequirementFaheemÎncă nu există evaluări

- Operators Extra Expense Insurance Contract for American Air Liquide Holdings IncDocument23 paginiOperators Extra Expense Insurance Contract for American Air Liquide Holdings IncAshutosh Sharma100% (1)

- Insurance Survey 2023.low Res - SMLDocument192 paginiInsurance Survey 2023.low Res - SMLmoodley.vadynÎncă nu există evaluări

- Safety Audit - Regional District of Okanagan-SimilkameenDocument105 paginiSafety Audit - Regional District of Okanagan-SimilkameenJoe FriesÎncă nu există evaluări

- NEBOSH EC2 Practical GuidanceDocument31 paginiNEBOSH EC2 Practical Guidanceragaie100% (1)

- Dinwiddie Lampton's Insurance Company Mired in Family LawsuitDocument59 paginiDinwiddie Lampton's Insurance Company Mired in Family LawsuitCourier JournalÎncă nu există evaluări

- Frauds in Insurance SectorDocument19 paginiFrauds in Insurance SectorNithin VargheseÎncă nu există evaluări

- Life Insurance: AN Assignment OnDocument40 paginiLife Insurance: AN Assignment OnAmar AhirwarÎncă nu există evaluări

- 02 PLI-HSE-G-05 Annex2-8 en Land Transportation HSE Requirements Rev02Document23 pagini02 PLI-HSE-G-05 Annex2-8 en Land Transportation HSE Requirements Rev02Eddie TaiÎncă nu există evaluări

- WPPF and WWF (As Per Labour Law and Rules Amended Upto Sept 2015) Accountants PerspectiveDocument29 paginiWPPF and WWF (As Per Labour Law and Rules Amended Upto Sept 2015) Accountants PerspectiveFahim Khan0% (1)

- Ultimate Kaiser Health BuilderDocument30 paginiUltimate Kaiser Health BuilderOmeng Tawid100% (7)

- IRDA Fit and Proper Criteria for Insurance SurveyorsDocument2 paginiIRDA Fit and Proper Criteria for Insurance SurveyorsGaurav KumarÎncă nu există evaluări

- INSURANCE COMPANIES IN INDIADocument10 paginiINSURANCE COMPANIES IN INDIAVarshith GowdaÎncă nu există evaluări

- Risk Management InsuranceDocument4 paginiRisk Management Insurancexone1215Încă nu există evaluări

- Tiner Insurance ReportDocument44 paginiTiner Insurance ReportNikhil FatnaniÎncă nu există evaluări

- QBE Technical Claims Brief September 2012Document9 paginiQBE Technical Claims Brief September 2012QBE European Operations Risk ManagementÎncă nu există evaluări

- Understanding Consequential Loss InsuranceDocument34 paginiUnderstanding Consequential Loss InsuranceAnmol GulatiÎncă nu există evaluări

- L 21 The Management of Health & Safety at Work Regulations 1999Document54 paginiL 21 The Management of Health & Safety at Work Regulations 19991DSBÎncă nu există evaluări

- III AssociateDocument2 paginiIII Associateagupta_118177Încă nu există evaluări

- Dolphin Trust Brochure - Jan 2015Document4 paginiDolphin Trust Brochure - Jan 2015hung_hatheÎncă nu există evaluări

- TSA Enforcement Sanction Guidance PolicyDocument10 paginiTSA Enforcement Sanction Guidance PolicyJustin RohrlichÎncă nu există evaluări

- Insurance Documents: Module - 3Document13 paginiInsurance Documents: Module - 3SasiÎncă nu există evaluări

- Ethics in Insurance SectorDocument40 paginiEthics in Insurance SectorRohan DhamiÎncă nu există evaluări

- Aspect of ContrAct HNDDocument16 paginiAspect of ContrAct HNDBachir SarreÎncă nu există evaluări

- Marime Chiedza Financial ReportingDocument15 paginiMarime Chiedza Financial Reportingchiedza MarimeÎncă nu există evaluări

- Horizon Housing REIT PLC ProspectusDocument214 paginiHorizon Housing REIT PLC ProspectusSean SongÎncă nu există evaluări

- Chap 001Document85 paginiChap 001Rong GuoÎncă nu există evaluări

- LPG-BUS-HSE-IST-0007 - Safety Data Sheet - Liquefied Petroleum GasDocument10 paginiLPG-BUS-HSE-IST-0007 - Safety Data Sheet - Liquefied Petroleum GasElias Jarjoura100% (1)

- Intro and Contents PDFDocument8 paginiIntro and Contents PDFHani ThaherÎncă nu există evaluări

- Insurance and Risk in Malaysia - A Perspective From Money Laundering ActivitiesDocument13 paginiInsurance and Risk in Malaysia - A Perspective From Money Laundering ActivitiesAmeer ShafiqÎncă nu există evaluări

- General Accident Annual Report 2016Document26 paginiGeneral Accident Annual Report 2016saxobobÎncă nu există evaluări

- Mercury Mining Investment LTD - Audited Reports For 2022Document16 paginiMercury Mining Investment LTD - Audited Reports For 2022tankodanjumacÎncă nu există evaluări

- General Accident PLC: Annual Report and Financial Statements 2014Document26 paginiGeneral Accident PLC: Annual Report and Financial Statements 2014saxobobÎncă nu există evaluări

- SBR 2020-21 MCQ Progress Test 2Document15 paginiSBR 2020-21 MCQ Progress Test 2A JamelÎncă nu există evaluări

- OSMF Report of Directors and Unaudited Financial Statements For Year Ended 20191231Document10 paginiOSMF Report of Directors and Unaudited Financial Statements For Year Ended 20191231vedadÎncă nu există evaluări

- Moy Park Litter Utilisation StrategyDocument1 paginăMoy Park Litter Utilisation StrategyMarcus LerouxÎncă nu există evaluări

- Northern Ireland Synopsis of Responses To Nitrates Action Plan For 2015 To 2018Document45 paginiNorthern Ireland Synopsis of Responses To Nitrates Action Plan For 2015 To 2018Marcus LerouxÎncă nu există evaluări

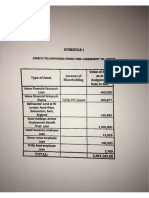

- List of Assets Assigned by Rock Holdings To Southern RockDocument1 paginăList of Assets Assigned by Rock Holdings To Southern RockMarcus LerouxÎncă nu există evaluări

- Accounts 2011 Technically Insolvent PDFDocument1 paginăAccounts 2011 Technically Insolvent PDFMarcus LerouxÎncă nu există evaluări

- Auditors Going Concern 12 PDFDocument1 paginăAuditors Going Concern 12 PDFMarcus LerouxÎncă nu există evaluări

- Putnam Vs KarrasDocument2 paginiPutnam Vs KarrasMarcus LerouxÎncă nu există evaluări

- Assignment of Assets From Rock Holdings To Southern RockDocument1 paginăAssignment of Assets From Rock Holdings To Southern RockMarcus LerouxÎncă nu există evaluări

- AB Assign 201112 Schedule PDFDocument1 paginăAB Assign 201112 Schedule PDFMarcus LerouxÎncă nu există evaluări

- Amendment To Southern Rock's Articles of AssociationDocument1 paginăAmendment To Southern Rock's Articles of AssociationMarcus LerouxÎncă nu există evaluări

- ICS Directors 2016Document3 paginiICS Directors 2016Marcus LerouxÎncă nu există evaluări

- ICS Directors 2015Document3 paginiICS Directors 2015Marcus LerouxÎncă nu există evaluări

- ICS Risk Solutions DirectorsDocument4 paginiICS Risk Solutions DirectorsMarcus LerouxÎncă nu există evaluări

- Letter From Gibraltar Financial Services Commission To STMDocument17 paginiLetter From Gibraltar Financial Services Commission To STMMarcus LerouxÎncă nu există evaluări

- Rationale For Instruction: Social Studies Lesson Plan TemplateDocument3 paginiRationale For Instruction: Social Studies Lesson Plan Templateapi-255764870Încă nu există evaluări

- The Indian Navy - Inet (Officers)Document3 paginiThe Indian Navy - Inet (Officers)ANKIT KUMARÎncă nu există evaluări

- Globalization Winners and LosersDocument2 paginiGlobalization Winners and Losersnprjkb5r2wÎncă nu există evaluări

- Controlled Chaos in Joseph Heller's Catch-22Document5 paginiControlled Chaos in Joseph Heller's Catch-22OliverÎncă nu există evaluări

- IFB Microwave Oven Customer Care in HyderabadDocument8 paginiIFB Microwave Oven Customer Care in HyderabadanilkumarÎncă nu există evaluări

- Key Concepts in Marketing: Maureen Castillo Dyna Enad Carelle Trisha Espital Ethel SilvaDocument35 paginiKey Concepts in Marketing: Maureen Castillo Dyna Enad Carelle Trisha Espital Ethel Silvasosoheart90Încă nu există evaluări

- ICAO EDTO Course - Basic Concepts ModuleDocument63 paginiICAO EDTO Course - Basic Concepts ModuleLbrito01100% (1)

- The Amtasiddhi Hahayogas Tantric Buddh PDFDocument14 paginiThe Amtasiddhi Hahayogas Tantric Buddh PDFalmadebuenosaires100% (1)

- 6th South African Armoured Division (Part 3)Document9 pagini6th South African Armoured Division (Part 3)Clifford HolmÎncă nu există evaluări

- History, and Culture of DenmarkDocument14 paginiHistory, and Culture of DenmarkRina ApriliaÎncă nu există evaluări

- Group 1 - MM - Vanca Digital StrategyDocument10 paginiGroup 1 - MM - Vanca Digital StrategyAashna Duggal100% (1)

- RAS MARKAZ CRUDE OIL PARK SITE INSPECTION PROCEDUREDocument1 paginăRAS MARKAZ CRUDE OIL PARK SITE INSPECTION PROCEDUREANIL PLAMOOTTILÎncă nu există evaluări

- KSDL RameshDocument10 paginiKSDL RameshRamesh KumarÎncă nu există evaluări

- ECC Ruling on Permanent Disability Benefits OverturnedDocument2 paginiECC Ruling on Permanent Disability Benefits OverturnedmeymeyÎncă nu există evaluări

- History-Complete Study NoteDocument48 paginiHistory-Complete Study NoteRahul PandeyÎncă nu există evaluări

- Pudri RekpungDocument1 paginăPudri Rekpungpz.pzzzzÎncă nu există evaluări

- Gender, Race, and Semicolonialism: Liu Na'ou's Urban Shanghai LandscapeDocument24 paginiGender, Race, and Semicolonialism: Liu Na'ou's Urban Shanghai Landscapebaiqian liuÎncă nu există evaluări

- Public-International-Law Reviewer Isagani Cruz - Scribd 2013 Public International Law (Finals) - Arellano ..Document1 paginăPublic-International-Law Reviewer Isagani Cruz - Scribd 2013 Public International Law (Finals) - Arellano ..Lylanie Alexandria Yan GalaÎncă nu există evaluări

- Agreement For Consulting Services Template SampleDocument6 paginiAgreement For Consulting Services Template SampleLegal ZebraÎncă nu există evaluări

- Senate Hearing, 110TH Congress - The Employee Free Choice Act: Restoring Economic Opportunity For Working FamiliesDocument83 paginiSenate Hearing, 110TH Congress - The Employee Free Choice Act: Restoring Economic Opportunity For Working FamiliesScribd Government DocsÎncă nu există evaluări

- Engineering Utilities 2: Engr. Ervin John D. Melendres InstructorDocument24 paginiEngineering Utilities 2: Engr. Ervin John D. Melendres InstructorStephanie CanibanÎncă nu există evaluări

- AN ORDINANCE ESTABLISHING THE BARANGAY SPECIAL BENEFIT AND SERVICE IMPROVEMENT SYSTEMDocument7 paginiAN ORDINANCE ESTABLISHING THE BARANGAY SPECIAL BENEFIT AND SERVICE IMPROVEMENT SYSTEMRomel VillanuevaÎncă nu există evaluări

- AACCSA Journal of Trade and Business V.1 No. 1Document90 paginiAACCSA Journal of Trade and Business V.1 No. 1Peter MuigaiÎncă nu există evaluări

- Engineering Economy 2ed Edition: January 2018Document12 paginiEngineering Economy 2ed Edition: January 2018anup chauhanÎncă nu există evaluări

- Su Xiaomi's spring arrives in unexpected formDocument4 paginiSu Xiaomi's spring arrives in unexpected formDonald BuchwalterÎncă nu există evaluări

- The Meaning of Life Without Parole - Rough Draft 1Document4 paginiThe Meaning of Life Without Parole - Rough Draft 1api-504422093Încă nu există evaluări

- Fs 6 Learning-EpisodesDocument11 paginiFs 6 Learning-EpisodesMichelleÎncă nu există evaluări

- The Basketball Diaries by Jim CarollDocument22 paginiThe Basketball Diaries by Jim CarollEricvv64% (25)

- IPR and Outer Spaces Activities FinalDocument25 paginiIPR and Outer Spaces Activities FinalKarthickÎncă nu există evaluări

- Important PIC'sDocument1 paginăImportant PIC'sAbhijit SahaÎncă nu există evaluări

- Value: The Four Cornerstones of Corporate FinanceDe la EverandValue: The Four Cornerstones of Corporate FinanceEvaluare: 4.5 din 5 stele4.5/5 (18)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelDe la Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelÎncă nu există evaluări

- Joy of Agility: How to Solve Problems and Succeed SoonerDe la EverandJoy of Agility: How to Solve Problems and Succeed SoonerEvaluare: 4 din 5 stele4/5 (1)

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000De la EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Evaluare: 4.5 din 5 stele4.5/5 (86)

- Finance Basics (HBR 20-Minute Manager Series)De la EverandFinance Basics (HBR 20-Minute Manager Series)Evaluare: 4.5 din 5 stele4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDe la EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaEvaluare: 4.5 din 5 stele4.5/5 (14)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistDe la EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistEvaluare: 4.5 din 5 stele4.5/5 (73)

- Product-Led Growth: How to Build a Product That Sells ItselfDe la EverandProduct-Led Growth: How to Build a Product That Sells ItselfEvaluare: 5 din 5 stele5/5 (1)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanDe la EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanEvaluare: 4.5 din 5 stele4.5/5 (79)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsDe la EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsÎncă nu există evaluări

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisDe la EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisEvaluare: 5 din 5 stele5/5 (6)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)De la EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Evaluare: 4.5 din 5 stele4.5/5 (4)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialDe la EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialÎncă nu există evaluări

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityDe la EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityEvaluare: 4.5 din 5 stele4.5/5 (4)

- Note Brokering for Profit: Your Complete Work At Home Success ManualDe la EverandNote Brokering for Profit: Your Complete Work At Home Success ManualÎncă nu există evaluări

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursDe la EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursEvaluare: 4.5 din 5 stele4.5/5 (34)

- Connected Planning: A Playbook for Agile Decision MakingDe la EverandConnected Planning: A Playbook for Agile Decision MakingÎncă nu există evaluări

- Financial Risk Management: A Simple IntroductionDe la EverandFinancial Risk Management: A Simple IntroductionEvaluare: 4.5 din 5 stele4.5/5 (7)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNDe la Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNEvaluare: 4.5 din 5 stele4.5/5 (3)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDe la EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaEvaluare: 3.5 din 5 stele3.5/5 (8)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthDe la EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthÎncă nu există evaluări

- Strategic Value Chain Analysis for Investors and ManagersDe la EverandStrategic Value Chain Analysis for Investors and ManagersÎncă nu există evaluări

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorDe la EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorÎncă nu există evaluări

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingDe la EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingEvaluare: 4.5 din 5 stele4.5/5 (17)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionDe la EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionEvaluare: 5 din 5 stele5/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialDe la EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialEvaluare: 4.5 din 5 stele4.5/5 (32)