S-ar putea să vă placă și

- Fear The Ninja: Demystifying Cryptocurrency TradingDe la EverandFear The Ninja: Demystifying Cryptocurrency TradingÎncă nu există evaluări

- Inve$t & Grow: Different Forms of Investment Explained - A Beginner's GuideDe la EverandInve$t & Grow: Different Forms of Investment Explained - A Beginner's GuideÎncă nu există evaluări

- 20.9.2019 DSK IBF7712 Financial InclusionDocument88 pagini20.9.2019 DSK IBF7712 Financial InclusionIsnan Hari MardikaÎncă nu există evaluări

- Chapter 10Document73 paginiChapter 10Melissa Mclean73% (11)

- Houston Fearless 76 Sales Incentive AnalysisDocument3 paginiHouston Fearless 76 Sales Incentive Analysisdachlevie rizaÎncă nu există evaluări

- Passware Kit User GuideDocument262 paginiPassware Kit User GuideTuấn Minh PhùngÎncă nu există evaluări

- Middle WareDocument8 paginiMiddle WareNaresh SÎncă nu există evaluări

- Deadalnix's Den: Schnorr Signatures For DummiesDocument5 paginiDeadalnix's Den: Schnorr Signatures For DummiesakuumbakkumÎncă nu există evaluări

- FIN268 Analysis 6Document5 paginiFIN268 Analysis 6Joseph SibiÎncă nu există evaluări

- Analysis of Fuel Pump Skimming DevicesDocument6 paginiAnalysis of Fuel Pump Skimming DevicesmarcelloperrathaisÎncă nu există evaluări

- Handout 2 - Introduction To SQL ServerDocument6 paginiHandout 2 - Introduction To SQL Serverabdi100% (1)

- Dave Banking Direct Deposit Enrollment FormDocument1 paginăDave Banking Direct Deposit Enrollment FormDavid HannaganÎncă nu există evaluări

- Palm Serials 2Document34 paginiPalm Serials 2Eric ChambersÎncă nu există evaluări

- Prags - Theory Part 123Document6 paginiPrags - Theory Part 123Trần HuyềnÎncă nu există evaluări

- 13 Steps to Investing WiselyDocument33 pagini13 Steps to Investing WiselyadikesaÎncă nu există evaluări

- 7700 Hard Spellrex Puzzles Nurture Your IQDocument573 pagini7700 Hard Spellrex Puzzles Nurture Your IQTomhÎncă nu există evaluări

- e-ChipTHTTT 211 Tech24.vnDocument47 paginie-ChipTHTTT 211 Tech24.vnthanhlinh9191Încă nu există evaluări

- Manage finances and track transactions easilyDocument4 paginiManage finances and track transactions easilyNarayanan KrishnamurthiÎncă nu există evaluări

- NETELLER UserGuide EnglishDocument94 paginiNETELLER UserGuide EnglishAnindita AndriatiÎncă nu există evaluări

- New Product Test Results and Chip ChartDocument158 paginiNew Product Test Results and Chip ChartomanfastsolutionÎncă nu există evaluări

- Yetubit Exchange: Whitepaper V 1.1Document22 paginiYetubit Exchange: Whitepaper V 1.1CRYPTO BEGINNERSÎncă nu există evaluări

- Baby Talk: New Evidence Challenges Traditional Views of Early Language DevelopmentDocument3 paginiBaby Talk: New Evidence Challenges Traditional Views of Early Language DevelopmentAndreea CiotÎncă nu există evaluări

- 1992 World Scientists' Warning To HumanityDocument4 pagini1992 World Scientists' Warning To Humanityjuggle333Încă nu există evaluări

- Computer Crime: Professional PracticesDocument45 paginiComputer Crime: Professional PracticesHaseeb AslamÎncă nu există evaluări

- 2014 Buick Encore Propeller Shaft Replacement GuideDocument16 pagini2014 Buick Encore Propeller Shaft Replacement Guidealberto navasÎncă nu există evaluări

- 10 Steps To Invest in Social Trading Like A ProDocument18 pagini10 Steps To Invest in Social Trading Like A ProInvestingoalÎncă nu există evaluări

- State of Crvpto: DisclaimerDocument35 paginiState of Crvpto: DisclaimerilhamÎncă nu există evaluări

- Crypto For BeginnersDocument15 paginiCrypto For BeginnersVlad VladutÎncă nu există evaluări

- How Bitcoin Casinos WorkDocument2 paginiHow Bitcoin Casinos WorkAnonymous Bitcoin CasinosÎncă nu există evaluări

- SoundcardDocument46 paginiSoundcardgetÎncă nu există evaluări

- Questions G 1Document9 paginiQuestions G 1Haressa ArumpacÎncă nu există evaluări

- NanoByte - Full Whitepaper - 21 Feb 22Document20 paginiNanoByte - Full Whitepaper - 21 Feb 22tuyul polosÎncă nu există evaluări

- Tweetattacks Manual2 PDFDocument62 paginiTweetattacks Manual2 PDFFadlan HumaidiÎncă nu există evaluări

- 10-04-05 Top 10 Alleged Violations of Human Rights by The United States - Notice To The UN Hight Commissioner: Efforts To Undermine The 2010 Universal Periodic ReviewDocument9 pagini10-04-05 Top 10 Alleged Violations of Human Rights by The United States - Notice To The UN Hight Commissioner: Efforts To Undermine The 2010 Universal Periodic ReviewHuman Rights Alert - NGO (RA)Încă nu există evaluări

- Bitcoin: A Peer-to-Peer Electronic Cash System PresentationDocument14 paginiBitcoin: A Peer-to-Peer Electronic Cash System PresentationSahethiÎncă nu există evaluări

- How Encryption Protects Online Banking CommunicationsDocument14 paginiHow Encryption Protects Online Banking Communications思恩Încă nu există evaluări

- Oracle® Ireceivables: Implementation Guide Release 12Document76 paginiOracle® Ireceivables: Implementation Guide Release 12Sravan DilseÎncă nu există evaluări

- How To Turn $100 Into $1,000,000Document2 paginiHow To Turn $100 Into $1,000,000no-reply0% (1)

- Evolution of PayPalDocument9 paginiEvolution of PayPalFlaviub23Încă nu există evaluări

- Money Pad: The Future WalletDocument15 paginiMoney Pad: The Future WalletAnvita_Jain_2921Încă nu există evaluări

- Polkadot ResearchDocument3 paginiPolkadot ResearchChrisLCampbellÎncă nu există evaluări

- Very Cheap Car InsuranceDocument1 paginăVery Cheap Car Insurancepapi7000Încă nu există evaluări

- Zeeshan UPDATEDDocument4 paginiZeeshan UPDATEDsiddharth.dubeyÎncă nu există evaluări

- Ebook-16 v6Document50 paginiEbook-16 v6José Luis Pérez RodríguezÎncă nu există evaluări

- OP - Modern Monetary Theory - Day 1Document15 paginiOP - Modern Monetary Theory - Day 1tarogiosdrakÎncă nu există evaluări

- 10-Minute Options Trading and ETF Investing - Rapidly Build Wealth, Retire Early, and Live Free From The Worry of Market Crashes (Passive Stock Options Trading Book 2)Document127 pagini10-Minute Options Trading and ETF Investing - Rapidly Build Wealth, Retire Early, and Live Free From The Worry of Market Crashes (Passive Stock Options Trading Book 2)PauloÎncă nu există evaluări

- Apple Pay FaqDocument7 paginiApple Pay FaqTHENNARASU A/L PANIR CHELVAM KPM-GuruÎncă nu există evaluări

- The Doge of Wall Street: Detecting Pump and Dump Cryptocurrency ManipulationsDocument32 paginiThe Doge of Wall Street: Detecting Pump and Dump Cryptocurrency ManipulationsSofari HidayatÎncă nu există evaluări

- Chatbot Web Application Using DIETDocument9 paginiChatbot Web Application Using DIETIJRASETPublicationsÎncă nu există evaluări

- PrintBoss Standard-Enterprise ManualDocument218 paginiPrintBoss Standard-Enterprise ManualWellspringSoftwareÎncă nu există evaluări

- Cincinnati LaserNst PDFDocument204 paginiCincinnati LaserNst PDFedrf sswedÎncă nu există evaluări

- BlockEye - Hunting For DeFi Attacks On Blockchain, B. Wang Et Al.Document4 paginiBlockEye - Hunting For DeFi Attacks On Blockchain, B. Wang Et Al.Ismael MedeirosÎncă nu există evaluări

- The BlueprintDocument11 paginiThe BlueprintCIO White PapersÎncă nu există evaluări

- Customer Perception Towards Plastic Money PDF FreeDocument65 paginiCustomer Perception Towards Plastic Money PDF FreeAmit bailwalÎncă nu există evaluări

- Also Read:: ERC20 Tether Transactions Flip Their Omni EquivalentDocument5 paginiAlso Read:: ERC20 Tether Transactions Flip Their Omni Equivalentong0625Încă nu există evaluări

- Stable Money: What we can learn from Bitcoin, Libra, and Co.De la EverandStable Money: What we can learn from Bitcoin, Libra, and Co.Încă nu există evaluări

- Cryptocurrency: Beginners Bible - How You Can Make Money Trading and Investing in CryptocurrencyDe la EverandCryptocurrency: Beginners Bible - How You Can Make Money Trading and Investing in CryptocurrencyÎncă nu există evaluări

- Methods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeDe la EverandMethods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeÎncă nu există evaluări

- Blockchain and Retail BankingDocument9 paginiBlockchain and Retail BankingMilinbhadeÎncă nu există evaluări

- The Impact of Blockchain For GovernmentDocument41 paginiThe Impact of Blockchain For GovernmentKaren L YoungÎncă nu există evaluări

- Us Fsi 2018 Global Blockchain Survey ReportDocument48 paginiUs Fsi 2018 Global Blockchain Survey ReportTamoghnaÎncă nu există evaluări

- Accenture Where Fintech Lending Will Land PDFDocument12 paginiAccenture Where Fintech Lending Will Land PDFKaren L YoungÎncă nu există evaluări

- FINRA Regulatory-Notice-18-20 Regarding Digital AssetsDocument4 paginiFINRA Regulatory-Notice-18-20 Regarding Digital AssetsCrowdfundInsiderÎncă nu există evaluări

- A Financial System That Creates Economic Opportunities Nonbank Financials, Fintech, and InnovationDocument4 paginiA Financial System That Creates Economic Opportunities Nonbank Financials, Fintech, and InnovationKaren L YoungÎncă nu există evaluări

- The Changing Landscape of Disruptive TechnologiesDocument42 paginiThe Changing Landscape of Disruptive TechnologiesKaren L YoungÎncă nu există evaluări

- Crypto-Assets: Report To The G20 On The Work of The FSB and Standard-Setting BodiesDocument10 paginiCrypto-Assets: Report To The G20 On The Work of The FSB and Standard-Setting BodiesAnonymous tyKXPuÎncă nu există evaluări

- WEF New Physics of Financial ServicesDocument167 paginiWEF New Physics of Financial ServicesKaren L YoungÎncă nu există evaluări

- Competition Issues in Teh Area of Financial TechnologyDocument136 paginiCompetition Issues in Teh Area of Financial TechnologyKaren L YoungÎncă nu există evaluări

- Accenture Open Platform Banking New EraDocument12 paginiAccenture Open Platform Banking New EraKaren L YoungÎncă nu există evaluări

- Driving New Modes of IoT-Facilitated Citzen/User EngagementDocument116 paginiDriving New Modes of IoT-Facilitated Citzen/User EngagementKaren L Young100% (1)

- BCG The First All Blockchain Insurer June 2018 Tcm9 194260Document7 paginiBCG The First All Blockchain Insurer June 2018 Tcm9 194260Karen L YoungÎncă nu există evaluări

- Ar 2018 e 5Document24 paginiAr 2018 e 5TBP_Think_TankÎncă nu există evaluări

- Digital Currencies Pros and Cons New Zeland Central BankDocument21 paginiDigital Currencies Pros and Cons New Zeland Central BankKaren L YoungÎncă nu există evaluări

- Summary Report of White House AI SummitDocument15 paginiSummary Report of White House AI SummitKaren L YoungÎncă nu există evaluări

- Us MFG Advanced Manufacturing Technologies ReportDocument64 paginiUs MFG Advanced Manufacturing Technologies ReportKaren L YoungÎncă nu există evaluări

- Accenture Technology Vision Oracle 2018Document32 paginiAccenture Technology Vision Oracle 2018Karen L YoungÎncă nu există evaluări

- Ar 2018 e 5Document24 paginiAr 2018 e 5TBP_Think_TankÎncă nu există evaluări

- Es 20180416 Digitalcurrencies PDFDocument52 paginiEs 20180416 Digitalcurrencies PDFKaren L YoungÎncă nu există evaluări

- Call For Rule-Making On ICO Proposal by ICO Business Research GroupDocument7 paginiCall For Rule-Making On ICO Proposal by ICO Business Research GroupKaren L YoungÎncă nu există evaluări

- Big Risks in ICO MarketDocument1 paginăBig Risks in ICO MarketKaren L YoungÎncă nu există evaluări

- Secure Military Mobile Voting SolutionDocument5 paginiSecure Military Mobile Voting SolutionKaren L YoungÎncă nu există evaluări

- March - April - 2016 - Disruption - Report PDFDocument33 paginiMarch - April - 2016 - Disruption - Report PDFKaren L YoungÎncă nu există evaluări

- Central Bank Digital CurrenciesDocument3 paginiCentral Bank Digital CurrenciesKaren L YoungÎncă nu există evaluări

- Top 10 AI Trends For 2018Document1 paginăTop 10 AI Trends For 2018Karen L YoungÎncă nu există evaluări

- Quantitative Easing & The Housing MarketDocument21 paginiQuantitative Easing & The Housing MarketKaren L YoungÎncă nu există evaluări

- Bitcoin Money or Financial Investment SEDocument6 paginiBitcoin Money or Financial Investment SEKaren L YoungÎncă nu există evaluări

- Easing at The Zero Bound - Beyond QE & The "Foolproof Way" by James RickardsDocument25 paginiEasing at The Zero Bound - Beyond QE & The "Foolproof Way" by James RickardsKaren L YoungÎncă nu există evaluări

- Mortgage Lending in 2014 What Are The Drivers BrinkmannDocument14 paginiMortgage Lending in 2014 What Are The Drivers BrinkmannKaren L YoungÎncă nu există evaluări

- Delhi Bank 2Document56 paginiDelhi Bank 2doon devbhoomi realtorsÎncă nu există evaluări

- Theory of Value - A Study of Pre-Classical, Classical andDocument11 paginiTheory of Value - A Study of Pre-Classical, Classical andARKA DATTAÎncă nu există evaluări

- CH 07Document50 paginiCH 07Anonymous fb7C3tcÎncă nu există evaluări

- Analisis Cost Volume Profit Sebagai Alat Perencanaan Laba (Studi Kasus Pada Umkm Dendeng Sapi Di Banda Aceh)Document25 paginiAnalisis Cost Volume Profit Sebagai Alat Perencanaan Laba (Studi Kasus Pada Umkm Dendeng Sapi Di Banda Aceh)Fauzan C LahÎncă nu există evaluări

- Banglalink (Final)Document42 paginiBanglalink (Final)Zaki Ahmad100% (1)

- Global Marketing Test Bank ReviewDocument31 paginiGlobal Marketing Test Bank ReviewbabykintexÎncă nu există evaluări

- Green Supply Chain Management PDFDocument18 paginiGreen Supply Chain Management PDFMaazÎncă nu există evaluări

- Managing Capability Nandos Executive Summary Marketing EssayDocument7 paginiManaging Capability Nandos Executive Summary Marketing Essaypitoro2006Încă nu există evaluări

- Assignment 2 - IPhonesDocument6 paginiAssignment 2 - IPhonesLa FlâneurÎncă nu există evaluări

- UWTSD BABS 5 ENT SBLC6001 Assignment and Case Study Apr-Jul 2019Document16 paginiUWTSD BABS 5 ENT SBLC6001 Assignment and Case Study Apr-Jul 2019Hafsa IqbalÎncă nu există evaluări

- 0 AngelList LA ReportDocument18 pagini0 AngelList LA ReportAndrés Mora PrinceÎncă nu există evaluări

- Titan Case StudyDocument14 paginiTitan Case StudySaurabh SinghÎncă nu există evaluări

- Accountancy Answer Key Class XII PreboardDocument8 paginiAccountancy Answer Key Class XII PreboardGHOST FFÎncă nu există evaluări

- Griffin Chap 11Document34 paginiGriffin Chap 11Spil_vv_IJmuidenÎncă nu există evaluări

- Case Study 1Document9 paginiCase Study 1kalpana0210Încă nu există evaluări

- Client Reacceptance Checklist - DR - FagihDocument1 paginăClient Reacceptance Checklist - DR - FagihAlizer AbidÎncă nu există evaluări

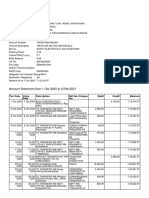

- Account StatementDocument46 paginiAccount Statementogagz ogagzÎncă nu există evaluări

- Expertise in trade finance sales and distributionDocument4 paginiExpertise in trade finance sales and distributionGabriella Njoto WidjajaÎncă nu există evaluări

- G.R. No. 161759, July 02, 2014Document9 paginiG.R. No. 161759, July 02, 2014Elaine Villafuerte AchayÎncă nu există evaluări

- PEA144Document4 paginiPEA144coffeepathÎncă nu există evaluări

- Cagayan de Oro Revenue Code of 2015Document134 paginiCagayan de Oro Revenue Code of 2015Jazz Adaza67% (6)

- JDA Demand - Focus 2012Document43 paginiJDA Demand - Focus 2012Abbas Ali Shirazi100% (1)

- Suzuki Project NewDocument98 paginiSuzuki Project NewRohan Somanna67% (3)

- Injection Molding Part CostingDocument4 paginiInjection Molding Part CostingfantinnoÎncă nu există evaluări

- Sage Pastel Partner Courses...Document9 paginiSage Pastel Partner Courses...Tanaka MpofuÎncă nu există evaluări

- Commodities CompaniesDocument30 paginiCommodities Companiesabhi000_mnittÎncă nu există evaluări

- Figure 26.1 The Directional Policy Matrix (DPM)Document2 paginiFigure 26.1 The Directional Policy Matrix (DPM)Abdela TuleÎncă nu există evaluări

- SMDDocument2 paginiSMDKhalil Ur RehmanÎncă nu există evaluări

- Moneyback and EndowmentDocument14 paginiMoneyback and EndowmentSheetal IyerÎncă nu există evaluări

- Internship PresentationDocument3 paginiInternship Presentationapi-242871239Încă nu există evaluări