S-ar putea să vă placă și

- Competing Digital PlatformDocument4 paginiCompeting Digital PlatformChristian AsoreyÎncă nu există evaluări

- An Outlook of Platform Theory Research in Business Studies: Tatsuyuki Negoro and Satoshi AjiroDocument29 paginiAn Outlook of Platform Theory Research in Business Studies: Tatsuyuki Negoro and Satoshi AjiroChristian AsoreyÎncă nu există evaluări

- Digital Platform Regulation What Are The Proposals Across EuropeDocument5 paginiDigital Platform Regulation What Are The Proposals Across EuropeChristian AsoreyÎncă nu există evaluări

- Brand Finance Global 500 2020 PreviewDocument27 paginiBrand Finance Global 500 2020 PreviewChristian AsoreyÎncă nu există evaluări

- The Application of Strategic Models To Non-Life Insurance MarketsDocument53 paginiThe Application of Strategic Models To Non-Life Insurance MarketsChristian AsoreyÎncă nu există evaluări

- Articulo - Forbes - How Executives Around The World View Industry 4.0Document4 paginiArticulo - Forbes - How Executives Around The World View Industry 4.0Christian AsoreyÎncă nu există evaluări

- Eiu Accenture Pega Digital EvolutionDocument30 paginiEiu Accenture Pega Digital EvolutionChristian AsoreyÎncă nu există evaluări

- A Smart City Initiative: The Case of BarcelonaDocument15 paginiA Smart City Initiative: The Case of BarcelonaGourav GuptaÎncă nu există evaluări

- Mobile InsuranceDocument9 paginiMobile InsuranceChristian AsoreyÎncă nu există evaluări

- Artículo - 27.a. Digital Business Transformation - WadeDocument4 paginiArtículo - 27.a. Digital Business Transformation - WadeChristian AsoreyÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Normal Consistency of Hydraulic CementDocument15 paginiNormal Consistency of Hydraulic CementApril Lyn SantosÎncă nu există evaluări

- IJISRT23JUL645Document11 paginiIJISRT23JUL645International Journal of Innovative Science and Research TechnologyÎncă nu există evaluări

- Python Cheat Sheet-1Document8 paginiPython Cheat Sheet-1RevathyÎncă nu există evaluări

- (Database Management Systems) : Biag, Marvin, B. BSIT - 202 September 6 2019Document7 pagini(Database Management Systems) : Biag, Marvin, B. BSIT - 202 September 6 2019Marcos JeremyÎncă nu există evaluări

- The Ins and Outs Indirect OrvinuDocument8 paginiThe Ins and Outs Indirect OrvinusatishÎncă nu există evaluări

- Ojt Evaluation Forms (Supervised Industry Training) SampleDocument5 paginiOjt Evaluation Forms (Supervised Industry Training) SampleJayJay Jimenez100% (3)

- Grade 6 q2 Mathematics LasDocument151 paginiGrade 6 q2 Mathematics LasERIC VALLE80% (5)

- d10 Sandra Darby FinalDocument3 paginid10 Sandra Darby FinalFirstCitizen1773Încă nu există evaluări

- Modicon PLC CPUS Technical Details.Document218 paginiModicon PLC CPUS Technical Details.TrbvmÎncă nu există evaluări

- DocsDocument4 paginiDocsSwastika SharmaÎncă nu există evaluări

- SUNGLAO - TM PortfolioDocument60 paginiSUNGLAO - TM PortfolioGIZELLE SUNGLAOÎncă nu există evaluări

- Directorate of Technical Education, Maharashtra State, MumbaiDocument57 paginiDirectorate of Technical Education, Maharashtra State, MumbaiShubham DahatondeÎncă nu există evaluări

- Datasheet 6A8 FusívelDocument3 paginiDatasheet 6A8 FusívelMluz LuzÎncă nu există evaluări

- Cognitive-Behavioral Interventions For PTSDDocument20 paginiCognitive-Behavioral Interventions For PTSDBusyMindsÎncă nu există evaluări

- BGP PDFDocument100 paginiBGP PDFJeya ChandranÎncă nu există evaluări

- Miata Wiring NA8 DiagramDocument65 paginiMiata Wiring NA8 DiagramseanÎncă nu există evaluări

- CH 2 PDFDocument85 paginiCH 2 PDFSajidÎncă nu există evaluări

- Asian Paints Final v1Document20 paginiAsian Paints Final v1Mukul MundleÎncă nu există evaluări

- Shot Blasting Machine ApplicationsDocument7 paginiShot Blasting Machine ApplicationsBhavin DesaiÎncă nu există evaluări

- Ccie R&s Expanded-BlueprintDocument12 paginiCcie R&s Expanded-BlueprintAftab AlamÎncă nu există evaluări

- Exam TimetableDocument16 paginiExam Timetablenyarko_eÎncă nu există evaluări

- Datasheet - HK ml7012-04 3364913Document22 paginiDatasheet - HK ml7012-04 3364913kami samaÎncă nu există evaluări

- SPWM Vs SVMDocument11 paginiSPWM Vs SVMpmbalajibtechÎncă nu există evaluări

- Amberjet™ 1500 H: Industrial Grade Strong Acid Cation ExchangerDocument2 paginiAmberjet™ 1500 H: Industrial Grade Strong Acid Cation ExchangerJaime SalazarÎncă nu există evaluări

- Tripura 04092012Document48 paginiTripura 04092012ARTHARSHI GARGÎncă nu există evaluări

- Iot Based Garbage and Street Light Monitoring SystemDocument3 paginiIot Based Garbage and Street Light Monitoring SystemHarini VenkatÎncă nu există evaluări

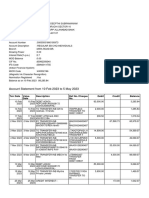

- Feb-May SBI StatementDocument2 paginiFeb-May SBI StatementAshutosh PandeyÎncă nu există evaluări

- CBLM - Interpreting Technical DrawingDocument18 paginiCBLM - Interpreting Technical DrawingGlenn F. Salandanan89% (45)

- General Mathematics SS3 2ND Term SchemeDocument2 paginiGeneral Mathematics SS3 2ND Term Schemesam kaluÎncă nu există evaluări

- Cable Schedule - Instrument - Surfin - Malanpur-R0Document3 paginiCable Schedule - Instrument - Surfin - Malanpur-R0arunpandey1686Încă nu există evaluări