S-ar putea să vă placă și

- Notes For The Teacher: Chapter 3: Money and CreditDocument16 paginiNotes For The Teacher: Chapter 3: Money and CreditEmil AbrahamÎncă nu există evaluări

- Screenshot 2023-11-26 at 10.21.47 PMDocument19 paginiScreenshot 2023-11-26 at 10.21.47 PM6c6yf87x2fÎncă nu există evaluări

- Money and Credit ExplainedDocument16 paginiMoney and Credit Explainedchaitanya200039Încă nu există evaluări

- 4 PDF Class XDocument20 pagini4 PDF Class XRanjana AnandÎncă nu există evaluări

- Class10 Economics Unit03 NCERT TextBook English EditionDocument16 paginiClass10 Economics Unit03 NCERT TextBook English EditionGarima BatraÎncă nu există evaluări

- NCERT Class 10 Economics Money and CreditDocument16 paginiNCERT Class 10 Economics Money and CreditChaitanya siriÎncă nu există evaluări

- Money & Credit SlideDocument64 paginiMoney & Credit SlideFREE FIRE SHORT VIDEO'SÎncă nu există evaluări

- Money and Banking Money and Banking Money and Banking Money and Banking Money and BankingDocument17 paginiMoney and Banking Money and Banking Money and Banking Money and Banking Money and BankingDhrUv GuptaÎncă nu există evaluări

- Ncert MacroecoDocument17 paginiNcert MacroecoDivya BadgujarÎncă nu există evaluări

- Exchanges Coincidence of WantsDocument17 paginiExchanges Coincidence of Wantsankit chauhanÎncă nu există evaluări

- Money and Banking: Functions and DemandDocument17 paginiMoney and Banking: Functions and Demandsudhanshu pandeyÎncă nu există evaluări

- Money and Credit Question and AnswersDocument12 paginiMoney and Credit Question and AnswersAashi Ranjan100% (1)

- Economics Le-3 Money and CreditDocument15 paginiEconomics Le-3 Money and CreditHema LathaÎncă nu există evaluări

- Unit 3 Microeconomics Chapter 17 Money and Banking Chapter 18 Workers Chapter 19 Trade UnionsDocument94 paginiUnit 3 Microeconomics Chapter 17 Money and Banking Chapter 18 Workers Chapter 19 Trade Unionseren parkÎncă nu există evaluări

- 9th EconomicsDocument70 pagini9th EconomicsDr. Mateen YousufÎncă nu există evaluări

- Evolution of MoneyDocument21 paginiEvolution of MoneyKunal100% (1)

- Notes - Money & Credit - Class X - EconomicsDocument4 paginiNotes - Money & Credit - Class X - EconomicsabhinavsinghbaliyanraghuvanshiÎncă nu există evaluări

- Functions and Evolution of MoneyDocument7 paginiFunctions and Evolution of MoneyLucela InocÎncă nu există evaluări

- Economics Chapter 3 Handwritten Notes Money and Credit EconomicsDocument11 paginiEconomics Chapter 3 Handwritten Notes Money and Credit EconomicsRenu Yadav100% (1)

- Oxford Public School, RanchiDocument7 paginiOxford Public School, RanchiRishav Singh RajputÎncă nu există evaluări

- Money and Banking: Chapter - 8Document36 paginiMoney and Banking: Chapter - 8Nihar NanyamÎncă nu există evaluări

- Money and BankingDocument9 paginiMoney and BankingAaryan MoreÎncă nu există evaluări

- Chapter 14Document7 paginiChapter 14ayandasmtsÎncă nu există evaluări

- Siddharth Menon WorkbookDocument69 paginiSiddharth Menon WorkbookNavneet YadavÎncă nu există evaluări

- I Defenition of Currency 2Document17 paginiI Defenition of Currency 2HAPSAH HARIANTIÎncă nu există evaluări

- MoneyDocument54 paginiMoneyTwinkle MehtaÎncă nu există evaluări

- Functions of MoneyDocument17 paginiFunctions of MoneyAnonymous ytZsBOVÎncă nu există evaluări

- CH 8 - Money MarketDocument60 paginiCH 8 - Money MarketSampreeth SampiÎncă nu există evaluări

- Chapter 8 Unit 1 - UnlockedDocument21 paginiChapter 8 Unit 1 - UnlockedSanay ShahÎncă nu există evaluări

- Financial System, Market & ManagementDocument62 paginiFinancial System, Market & ManagementVer Dnad JacobeÎncă nu există evaluări

- Discuss How Money Removed The Problems of Barter SystemDocument10 paginiDiscuss How Money Removed The Problems of Barter SystemChinedu chibuzoÎncă nu există evaluări

- Money and CreditDocument2 paginiMoney and CreditChris JudeÎncă nu există evaluări

- My Booklet About MoneyDocument9 paginiMy Booklet About MoneyNovilee MartinezÎncă nu există evaluări

- Amity Law School, Noida: Importance, Functions, Classification and Its TheoryDocument13 paginiAmity Law School, Noida: Importance, Functions, Classification and Its TheorySimran Kaur KhuranaÎncă nu există evaluări

- Nature of The Business NewDocument16 paginiNature of The Business Newshantol wedderburnÎncă nu există evaluări

- AssignmentDocument19 paginiAssignmentPham LinhÎncă nu există evaluări

- Module 1-The Concept and Development of MoneyDocument20 paginiModule 1-The Concept and Development of MoneyRoliane LJ RugaÎncă nu există evaluări

- Money and Currency Are Closely ConnectedDocument1 paginăMoney and Currency Are Closely ConnectedTricia SalvaniÎncă nu există evaluări

- Introduction To MoneyDocument10 paginiIntroduction To MoneyHassan IjazÎncă nu există evaluări

- Money and Banking: Module - 11Document14 paginiMoney and Banking: Module - 11Sarthak PithoriyaÎncă nu există evaluări

- FINANCIAL MARKETS REVIEWER. CH 3&4docxDocument29 paginiFINANCIAL MARKETS REVIEWER. CH 3&4docxChristine RepuldaÎncă nu există evaluări

- 1lmd - Test 01 - Money - 2nd VersionDocument6 pagini1lmd - Test 01 - Money - 2nd Versionimen DEBBAÎncă nu există evaluări

- Money and Its EvolutionDocument7 paginiMoney and Its EvolutionCANDA Jennyrose A.Încă nu există evaluări

- Money and BankingDocument47 paginiMoney and BankingYoacel FancyÎncă nu există evaluări

- Money and Banking NotesDocument13 paginiMoney and Banking NotesYash ShrivastavaÎncă nu există evaluări

- MoneyDocument14 paginiMoneyKarthik SanthoshÎncă nu există evaluări

- CBSE Class 10 EconomicsDocument4 paginiCBSE Class 10 EconomicsVishal DeyÎncă nu există evaluări

- Money and Banking, IG - 1Document26 paginiMoney and Banking, IG - 1ANSHIKA CHAUHAN100% (1)

- What Is MoneyDocument7 paginiWhat Is Moneyshrudiya100% (1)

- Education Group 6 Managerial Economics IiDocument9 paginiEducation Group 6 Managerial Economics Iimvodani98Încă nu există evaluări

- Chapter 1 ShairaDocument15 paginiChapter 1 ShairaIrish Dianne TulodÎncă nu există evaluări

- Money, Inflation and Interest RatesDocument19 paginiMoney, Inflation and Interest Rateswakemeup143Încă nu există evaluări

- U5 Lesson 1 2024Document3 paginiU5 Lesson 1 2024Mouh ZerÎncă nu există evaluări

- What is Money and How is it Created in 40 CharactersDocument7 paginiWhat is Money and How is it Created in 40 CharactersHassan NisarÎncă nu există evaluări

- Week 4 - History of MoneyDocument4 paginiWeek 4 - History of MoneyAmrita GangaramÎncă nu există evaluări

- Lesson 2 Introducing Money and Interest RatesDocument10 paginiLesson 2 Introducing Money and Interest RatesRovelyn SeñoÎncă nu există evaluări

- Economics ChapDocument8 paginiEconomics ChapJose J OlickalÎncă nu există evaluări

- Bitcoin: The Simplified Guide to Understanding Bitcoin Currency, Mining & ExchangeDe la EverandBitcoin: The Simplified Guide to Understanding Bitcoin Currency, Mining & ExchangeEvaluare: 4 din 5 stele4/5 (22)

- March 2018 CA EnglishDocument87 paginiMarch 2018 CA EnglishferozbabuÎncă nu există evaluări

- January 2018 CA EnglishDocument82 paginiJanuary 2018 CA EnglishAnkit RajputÎncă nu există evaluări

- GS IvDocument24 paginiGS IvsaqibÎncă nu există evaluări

- BHEL Tender ClarificationDocument133 paginiBHEL Tender Clarificationelangorenga0% (1)

- GS IiDocument102 paginiGS IiThejeswarÎncă nu există evaluări

- GS-III Dec 2017Document64 paginiGS-III Dec 2017ferozbabuÎncă nu există evaluări

- GS-II Dec 2017Document85 paginiGS-II Dec 2017ferozbabuÎncă nu există evaluări

- Secure Synopsis: InsightsonindiaDocument36 paginiSecure Synopsis: InsightsonindiasaqibÎncă nu există evaluări

- Secure Synopsis: InsightsonindiaDocument36 paginiSecure Synopsis: InsightsonindiasaqibÎncă nu există evaluări

- Secure Synopsis: InsightsonindiaDocument36 paginiSecure Synopsis: InsightsonindiasaqibÎncă nu există evaluări

- GS IiDocument102 paginiGS IiThejeswarÎncă nu există evaluări

- GS IiiDocument75 paginiGS IiiferozbabuÎncă nu există evaluări

- Insights PT 2018 Exclusive: PolityDocument55 paginiInsights PT 2018 Exclusive: PolityThejeswarÎncă nu există evaluări

- GS IiDocument90 paginiGS IiferozbabuÎncă nu există evaluări

- GS-I Jan 2018Document48 paginiGS-I Jan 2018ferozbabuÎncă nu există evaluări

- Insights Daily Current Events June 2017 PDFDocument87 paginiInsights Daily Current Events June 2017 PDFAmir Danish UmarÎncă nu există evaluări

- GS IiiDocument62 paginiGS IiiferozbabuÎncă nu există evaluări

- GS IDocument33 paginiGS IferozbabuÎncă nu există evaluări

- Jess 201Document16 paginiJess 201KarthikPrakashÎncă nu există evaluări

- Insights PT 2018 Exclusive International RelationsDocument84 paginiInsights PT 2018 Exclusive International RelationsferozbabuÎncă nu există evaluări

- Jess 2 PsDocument13 paginiJess 2 PsArjun BiswasÎncă nu există evaluări

- Insights PT 2018 Exclusive Art and Culture 1Document44 paginiInsights PT 2018 Exclusive Art and Culture 1ferozbabuÎncă nu există evaluări

- Jess204 PDFDocument20 paginiJess204 PDFVamshi Krishna AllamuneniÎncă nu există evaluări

- Insights IAS Summary of Economic Survey 2017 2018Document35 paginiInsights IAS Summary of Economic Survey 2017 2018ashishÎncă nu există evaluări

- Indian Economy Sectors GuideDocument20 paginiIndian Economy Sectors GuideBabul Kumar BhartiyaÎncă nu există evaluări

- Pdms 12.0 TutorialDocument136 paginiPdms 12.0 Tutorialferozbabu0% (1)

- Thermal InsulationDocument28 paginiThermal Insulationferozbabu100% (2)

- Statutory RegulationDocument19 paginiStatutory RegulationferozbabuÎncă nu există evaluări

- Learn About SCDL Student HandbookDocument11 paginiLearn About SCDL Student HandbookDaxa TrivediÎncă nu există evaluări

- Internet BookshopDocument19 paginiInternet Bookshopamitpatil777Încă nu există evaluări

- On May 31 2017 Reber Company Had A Cash BalanceDocument1 paginăOn May 31 2017 Reber Company Had A Cash BalanceAmit PandeyÎncă nu există evaluări

- Utility Powertech Limited: Notice Inviting E-TenderDocument3 paginiUtility Powertech Limited: Notice Inviting E-Tenderashishntpc1309Încă nu există evaluări

- Refugee LoanDocument1 paginăRefugee LoanKSTPTV100% (1)

- Standard Tender Document For Sale of Disposable Stores and EquipmentDocument43 paginiStandard Tender Document For Sale of Disposable Stores and EquipmentAccess to Government Procurement OpportunitiesÎncă nu există evaluări

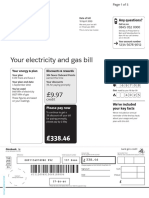

- Customer's annual statement bill analyzedDocument3 paginiCustomer's annual statement bill analyzedmohamed elmakhzniÎncă nu există evaluări

- Two Column Cash BookDocument24 paginiTwo Column Cash BookDarshans dadÎncă nu există evaluări

- Checklist For Secretarial Audit & Com - CertDocument42 paginiChecklist For Secretarial Audit & Com - CertCA Shobhit GuptaÎncă nu există evaluări

- The Seven C's of Effective Business CommunicationDocument102 paginiThe Seven C's of Effective Business CommunicationKainat BaigÎncă nu există evaluări

- Cambridge Exam Fees 2022 1 1Document1 paginăCambridge Exam Fees 2022 1 1Saeed Ul HassanÎncă nu există evaluări

- San Mateo not proven guilty of BP 22 violation despite delay in paymentDocument3 paginiSan Mateo not proven guilty of BP 22 violation despite delay in paymentMadsSalazarÎncă nu există evaluări

- Pdfcaie Igcse Accounting 0452 Theory v2 PDFDocument24 paginiPdfcaie Igcse Accounting 0452 Theory v2 PDFrumaisaaltaf287Încă nu există evaluări

- Everything You Need to Know About Plastic MoneyDocument23 paginiEverything You Need to Know About Plastic Moneyharsh1717Încă nu există evaluări

- Equitable Banking CorporationDocument2 paginiEquitable Banking CorporationChammyÎncă nu există evaluări

- FIDE Rating Chess Tournament 2016Document3 paginiFIDE Rating Chess Tournament 2016Mahesh ChÎncă nu există evaluări

- MBA Review Questions CH 8 & CH 10 Princ. Acc. IIDocument5 paginiMBA Review Questions CH 8 & CH 10 Princ. Acc. IIMirna Kassar100% (1)

- Commercial Banks and NBFIsDocument17 paginiCommercial Banks and NBFIsAbhishek kumarÎncă nu există evaluări

- How To Read Your MT4 Trading StatementDocument7 paginiHow To Read Your MT4 Trading StatementwanfaroukÎncă nu există evaluări

- 2017 DOJ Free Bar Notes in Criminal LawDocument7 pagini2017 DOJ Free Bar Notes in Criminal LawMarcelino CasilÎncă nu există evaluări

- Commerce Green BookDocument95 paginiCommerce Green Bookchenu sumaniÎncă nu există evaluări

- AnnexuresDocument47 paginiAnnexuresRajneesh JadhavÎncă nu există evaluări

- Proof of CashDocument2 paginiProof of Cashmjc24100% (2)

- Chapter7 Cash and EquivalentsDocument6 paginiChapter7 Cash and EquivalentsTamayo PaulaÎncă nu există evaluări

- FBI Summary About Alleged Flight 77 Hijacker Khalid AlmihdharDocument24 paginiFBI Summary About Alleged Flight 77 Hijacker Khalid Almihdhar9/11 Document ArchiveÎncă nu există evaluări

- Housing Service Committee: ProblemsDocument13 paginiHousing Service Committee: ProblemsKimberly Marie SousaÎncă nu există evaluări

- NCERT SolutionsDocument55 paginiNCERT SolutionsArif ShaikhÎncă nu există evaluări

- IT Audit CH 9Document19 paginiIT Audit CH 9Venice Mae Geronimo AvilaÎncă nu există evaluări

- Negotiable Instruments QuestionsDocument17 paginiNegotiable Instruments QuestionsAashish TiwariÎncă nu există evaluări

- Revision Questions and Answers Law Past PapersDocument106 paginiRevision Questions and Answers Law Past PapersRobin Thiru100% (1)