S-ar putea să vă placă și

- Obama’S Wonder Years: 8 Years of Lower Unemployment & Rising Stock MarketsDe la EverandObama’S Wonder Years: 8 Years of Lower Unemployment & Rising Stock MarketsÎncă nu există evaluări

- CEP Presentation - May 2018Document40 paginiCEP Presentation - May 2018TPPFÎncă nu există evaluări

- Socioeconomic Stratification: A Case Study on Sustainable Growth in a Declining PopulationDe la EverandSocioeconomic Stratification: A Case Study on Sustainable Growth in a Declining PopulationÎncă nu există evaluări

- CEP Presentation (October 2017)Document35 paginiCEP Presentation (October 2017)TPPFÎncă nu există evaluări

- Macro Economics: A Simplified Detailed Edition for Students Understanding Fundamentals of MacroeconomicsDe la EverandMacro Economics: A Simplified Detailed Edition for Students Understanding Fundamentals of MacroeconomicsÎncă nu există evaluări

- CEP Presentation - March 2018Document38 paginiCEP Presentation - March 2018TPPFÎncă nu există evaluări

- CEP PresentationDocument35 paginiCEP PresentationTPPFÎncă nu există evaluări

- CEP Presentation - April 2018Document38 paginiCEP Presentation - April 2018TPPFÎncă nu există evaluări

- August CFP PresentationDocument33 paginiAugust CFP PresentationTPPFÎncă nu există evaluări

- CFP PresentationDocument33 paginiCFP PresentationTPPFÎncă nu există evaluări

- CFP PresentationDocument33 paginiCFP PresentationTPPFÎncă nu există evaluări

- CEP Presentation - SeptemberDocument40 paginiCEP Presentation - SeptemberTPPFÎncă nu există evaluări

- Montgomery County Empower Montgomery ReportDocument7 paginiMontgomery County Empower Montgomery ReportAJ MetcalfÎncă nu există evaluări

- The Millionaires ClubDocument3 paginiThe Millionaires ClubEduardo Salas100% (1)

- Florida Unemployment Numbers June 2021Document17 paginiFlorida Unemployment Numbers June 2021RUELLE FLUDDÎncă nu există evaluări

- Texas Workforce: Texas Workforce Commission's Labor Market & Career InformationDocument54 paginiTexas Workforce: Texas Workforce Commission's Labor Market & Career InformationLisa FabianÎncă nu există evaluări

- Data Points Newsletter 2012 July FinalDocument2 paginiData Points Newsletter 2012 July FinalJOHNALEXANDERREESÎncă nu există evaluări

- Self Employed Tax ContributionDocument4 paginiSelf Employed Tax ContributionLe-Noi AndersonÎncă nu există evaluări

- EDB Economics Seminar On Population Ageing (19 Oct 2022)Document30 paginiEDB Economics Seminar On Population Ageing (19 Oct 2022)Ricky LIÎncă nu există evaluări

- Housing 17 Q 1Document13 paginiHousing 17 Q 1Dan LehrÎncă nu există evaluări

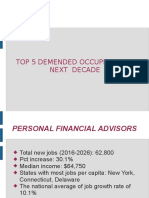

- Top 5 Occupation of FutureDocument7 paginiTop 5 Occupation of FutureEasyEnglishÎncă nu există evaluări

- Reward Work, Not Wealth: Methodology NoteDocument12 paginiReward Work, Not Wealth: Methodology NoteRaduÎncă nu există evaluări

- 2015 Child Welfare PresentationDocument42 pagini2015 Child Welfare PresentationRupak SapkotaÎncă nu există evaluări

- Research Memo and Labour Markets: Statistics 1Document6 paginiResearch Memo and Labour Markets: Statistics 1Nearby ClassicÎncă nu există evaluări

- Houston Economic Out LookDocument8 paginiHouston Economic Out LookKevin ParkerÎncă nu există evaluări

- Northeastern Region Vegetable Report: National Agricultural Statistics ServiceDocument2 paginiNortheastern Region Vegetable Report: National Agricultural Statistics ServiceGrowing AmericaÎncă nu există evaluări

- 01 01 08 Ada Misery IndexDocument1 pagină01 01 08 Ada Misery IndexMark WelkieÎncă nu există evaluări

- ENTIRE Fall 2016 Symposium Slide ShowDocument102 paginiENTIRE Fall 2016 Symposium Slide ShowLydia DePillisÎncă nu există evaluări

- Extract From 2013 Housing Needs AssessmentDocument8 paginiExtract From 2013 Housing Needs Assessment3x4 ArchitectureÎncă nu există evaluări

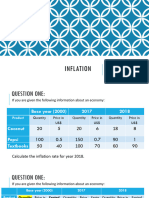

- 4.inflation QuesDocument18 pagini4.inflation QuesMahmoud IbrahimÎncă nu există evaluări

- The Big Squeeze ReportDocument42 paginiThe Big Squeeze ReportFOX 17 News Digital StaffÎncă nu există evaluări

- T E S - J 2017: Transmission of Material in This Release Is Embargoed Until 8:30 A.M. (EST) Friday, February 3, 2017Document42 paginiT E S - J 2017: Transmission of Material in This Release Is Embargoed Until 8:30 A.M. (EST) Friday, February 3, 2017mukeshÎncă nu există evaluări

- 2018 Progress Report Pepfar Hiv AidsDocument16 pagini2018 Progress Report Pepfar Hiv AidsThe Independent MagazineÎncă nu există evaluări

- EmpsitDocument42 paginiEmpsitPrathamesh GhargeÎncă nu există evaluări

- Budget Responses 04-03-2023Document6 paginiBudget Responses 04-03-2023Caitlyn FroloÎncă nu există evaluări

- End of Cheap Labor ChinaDocument18 paginiEnd of Cheap Labor Chinalouisecordeiro05Încă nu există evaluări

- Cwopa State Government Workforce Statistics 2011Document28 paginiCwopa State Government Workforce Statistics 2011EHÎncă nu există evaluări

- Data Points Newsletter March - FinalDocument2 paginiData Points Newsletter March - FinalJohn ReesÎncă nu există evaluări

- The Capital Area Council of Governments: Employment Update - JanuaryDocument3 paginiThe Capital Area Council of Governments: Employment Update - JanuaryJohn ReesÎncă nu există evaluări

- CFO Macro12 PPT 16Document29 paginiCFO Macro12 PPT 16Pedro ValdiviaÎncă nu există evaluări

- Climate Report - FEB 2010 FINALDocument20 paginiClimate Report - FEB 2010 FINALHouston ChronicleÎncă nu există evaluări

- EmpsitDocument42 paginiEmpsitGMG EditorialÎncă nu există evaluări

- Nonprofits in New York State 2019Document20 paginiNonprofits in New York State 2019ZacharyEJWilliamsÎncă nu există evaluări

- T E S - A 2023: Transmission of Material in This News Release Is Embargoed Until 8:30 A.M. (ET) Friday, September 1, 2023Document39 paginiT E S - A 2023: Transmission of Material in This News Release Is Embargoed Until 8:30 A.M. (ET) Friday, September 1, 2023iliana tinocoÎncă nu există evaluări

- City of Hoboken CY 2017 Introduced BudgetDocument13 paginiCity of Hoboken CY 2017 Introduced BudgetGrafixAvengerÎncă nu există evaluări

- Sizing Up The Executive Branch - 1Document9 paginiSizing Up The Executive Branch - 1Edison BreggerÎncă nu există evaluări

- December 2021 Jobs ReportDocument43 paginiDecember 2021 Jobs ReportStephen LoiaconiÎncă nu există evaluări

- MGEA06 Midterm Answer Key Winter 2017Document11 paginiMGEA06 Midterm Answer Key Winter 2017Krish AhluwaliaÎncă nu există evaluări

- Wisconsin April Unemployment NumbersDocument4 paginiWisconsin April Unemployment Numbersrobertmentzer4853Încă nu există evaluări

- T E S - M 2015: Transmission of Material in This Release Is Embargoed Until 8:30 A.M. (EDT) Friday, June 5, 2015Document38 paginiT E S - M 2015: Transmission of Material in This Release Is Embargoed Until 8:30 A.M. (EDT) Friday, June 5, 2015yasahswi91Încă nu există evaluări

- August 2018 Jobs ReportDocument39 paginiAugust 2018 Jobs ReportStephen LoiaconiÎncă nu există evaluări

- T E S - A 2020: HE Mployment Ituation UgustDocument42 paginiT E S - A 2020: HE Mployment Ituation UgustOwnown StuffstuffÎncă nu există evaluări

- DATAPOINTS NEWSLETTER March - FINALDocument2 paginiDATAPOINTS NEWSLETTER March - FINALJohn ReesÎncă nu există evaluări

- EmpsitDocument40 paginiEmpsitReneÎncă nu există evaluări

- Corpus Christi Housing Condition Outlook March 2018Document15 paginiCorpus Christi Housing Condition Outlook March 2018callertimes100% (2)

- T E S - A 2022: HE Mployment Ituation PrilDocument40 paginiT E S - A 2022: HE Mployment Ituation PrilDiksha yadavÎncă nu există evaluări

- Slaughter: U.S. Commercial Red Meat Production Down SlightlyDocument2 paginiSlaughter: U.S. Commercial Red Meat Production Down SlightlyGrowing AmericaÎncă nu există evaluări

- Development of China: - An Economy in TransitionDocument23 paginiDevelopment of China: - An Economy in TransitionHsu MeeÎncă nu există evaluări

- For Release 10:00 A.M. (EDT) Tuesday, October 24, 2017: Chart 1. Ten Fastest Growing Occupations, Projected 2016-26Document7 paginiFor Release 10:00 A.M. (EDT) Tuesday, October 24, 2017: Chart 1. Ten Fastest Growing Occupations, Projected 2016-26avik124Încă nu există evaluări

- Job Ads December 2009Document10 paginiJob Ads December 2009peter_martin9335Încă nu există evaluări

- 2018 08 Testimony Deregulating Occupational Licensing CEP GinnDocument1 pagină2018 08 Testimony Deregulating Occupational Licensing CEP GinnTPPFÎncă nu există evaluări

- TPPF Judicial Confirmation Letter 08-16-18Document3 paginiTPPF Judicial Confirmation Letter 08-16-18TPPFÎncă nu există evaluări

- CEP Presentation - SeptemberDocument40 paginiCEP Presentation - SeptemberTPPFÎncă nu există evaluări

- Slavery HexagonsDocument17 paginiSlavery HexagonsTPPFÎncă nu există evaluări

- 2018-08-Testimony - HouseCommittee On Public Education - CIE - SassDocument2 pagini2018-08-Testimony - HouseCommittee On Public Education - CIE - SassTPPFÎncă nu există evaluări

- 2018 07 RR A College Degree in Three Years CIE LindsayDocument12 pagini2018 07 RR A College Degree in Three Years CIE LindsayTPPFÎncă nu există evaluări

- CEP PresentationDocument43 paginiCEP PresentationTPPFÎncă nu există evaluări

- A-F Accountability BrochureDocument4 paginiA-F Accountability BrochureTPPFÎncă nu există evaluări

- 2018 06 RR Robin Hood School Property Tax BelewSassPeacockDocument12 pagini2018 06 RR Robin Hood School Property Tax BelewSassPeacockTPPF100% (1)

- Employer HandbookDocument28 paginiEmployer HandbookTPPFÎncă nu există evaluări

- 2018-07-Testimony-Testimony Before The Matagorda Co Commissioners Ct-ACEE-GonzalezDocument1 pagină2018-07-Testimony-Testimony Before The Matagorda Co Commissioners Ct-ACEE-GonzalezTPPFÎncă nu există evaluări

- 2018 04 RR TexasWindPowerStoryPart1 ACEE LisaLinowesDocument20 pagini2018 04 RR TexasWindPowerStoryPart1 ACEE LisaLinowesTPPFÎncă nu există evaluări

- CEP PresentationDocument43 paginiCEP PresentationTPPFÎncă nu există evaluări

- 2018-07-Testimony-Testimony Before The Concho County Hospital District-A...Document1 pagină2018-07-Testimony-Testimony Before The Concho County Hospital District-A...TPPFÎncă nu există evaluări

- CEP Presentation - June 2018Document40 paginiCEP Presentation - June 2018TPPFÎncă nu există evaluări

- 2018 08 PP Cautionary Tale of Wind Energy ACEE McConnell 1 1Document8 pagini2018 08 PP Cautionary Tale of Wind Energy ACEE McConnell 1 1TPPFÎncă nu există evaluări

- 2018-07-Testimony-Testimony Before The Concho County Commissioners Court-ACEE-GonzalezDocument1 pagină2018-07-Testimony-Testimony Before The Concho County Commissioners Court-ACEE-GonzalezTPPFÎncă nu există evaluări

- 2018 06 RR TexasWindPowerStoryPart2 ACEE LisaLinowesDocument20 pagini2018 06 RR TexasWindPowerStoryPart2 ACEE LisaLinowesTPPFÎncă nu există evaluări

- ACEE - Testimony Matagorda CampaignDocument1 paginăACEE - Testimony Matagorda CampaignTPPFÎncă nu există evaluări

- 2018 06 Charter Paper CIE ExcelInEdDocument24 pagini2018 06 Charter Paper CIE ExcelInEdTPPFÎncă nu există evaluări

- 2018 06 Charter Paper CIE ExcelInEdDocument24 pagini2018 06 Charter Paper CIE ExcelInEdTPPFÎncă nu există evaluări

- STAAR Report Card HandoutDocument4 paginiSTAAR Report Card HandoutTPPFÎncă nu există evaluări

- 2018-6-1-Testimony - A-F Academic School District and Campus Accountability System-CIE-BelewDocument4 pagini2018-6-1-Testimony - A-F Academic School District and Campus Accountability System-CIE-BelewTPPFÎncă nu există evaluări

- 2018 03 RR Purdue University's Cost Cutting CHE LindsayDocument24 pagini2018 03 RR Purdue University's Cost Cutting CHE LindsayTPPFÎncă nu există evaluări

- 2018 06 Charter Paper CIE ExcelInEdDocument24 pagini2018 06 Charter Paper CIE ExcelInEdTPPFÎncă nu există evaluări

- ACEE - Resource Bank Peacock PresentationDocument14 paginiACEE - Resource Bank Peacock PresentationTPPFÎncă nu există evaluări

- 2018 04 RR Rural Pretrial Incarceration CEJ Levin HaugenDocument44 pagini2018 04 RR Rural Pretrial Incarceration CEJ Levin HaugenTPPFÎncă nu există evaluări

- 2018 04 RR TexasWindPowerStoryPart1 ACEE LisaLinowesDocument20 pagini2018 04 RR TexasWindPowerStoryPart1 ACEE LisaLinowesTPPFÎncă nu există evaluări

- 2018 06 RR Robin Hood School Property Tax BelewSassPeacockDocument12 pagini2018 06 RR Robin Hood School Property Tax BelewSassPeacockTPPF100% (1)

- Chapter 5 Problems of The Third World CountriesDocument64 paginiChapter 5 Problems of The Third World CountriesFatima VillalobosÎncă nu există evaluări

- (32 34) +Great+Depression+and+New+Deal+Cornell+NotesDocument8 pagini(32 34) +Great+Depression+and+New+Deal+Cornell+NotesOlivia LardizabalÎncă nu există evaluări

- Forum 4 EcoDocument12 paginiForum 4 EcoSHIVANI CHOUDHARYÎncă nu există evaluări

- Macro Economics KLE Law College NotesDocument193 paginiMacro Economics KLE Law College Noteslakshmipriyats1532Încă nu există evaluări

- Education Mismatch-Issues and Problems in Philippine Educational System-PHILIP OMAR FAMULARCANODocument5 paginiEducation Mismatch-Issues and Problems in Philippine Educational System-PHILIP OMAR FAMULARCANOPHILIP OMAR FAMULARCANO100% (1)

- 2019 H1 Economics A-Level CSQ 1 PDFDocument5 pagini2019 H1 Economics A-Level CSQ 1 PDF19S53 LIAN ZHIJUNÎncă nu există evaluări

- Microeconomics 19th Edition Samuelson Solutions ManualDocument5 paginiMicroeconomics 19th Edition Samuelson Solutions ManualLaurenThompsonnfcqy100% (15)

- Aqa Econ4 QP Jan13Document8 paginiAqa Econ4 QP Jan13api-247036342Încă nu există evaluări

- Unemployment Problem in JakartaDocument3 paginiUnemployment Problem in JakartabudimagÎncă nu există evaluări

- Career Counseling Economically DisadvantagedDocument12 paginiCareer Counseling Economically DisadvantagedAbhishek Upadhyay100% (1)

- Qns Sec 222Document8 paginiQns Sec 222Haggai SimbayaÎncă nu există evaluări

- Study Guide APUSHDocument18 paginiStudy Guide APUSHmialee595Încă nu există evaluări

- Kater Michael - The Twisted Muse - Musicians and Their Music in The Third ReichDocument344 paginiKater Michael - The Twisted Muse - Musicians and Their Music in The Third ReichEsculapio JonesÎncă nu există evaluări

- Main Street November 2013Document40 paginiMain Street November 2013Anne SecorÎncă nu există evaluări

- Adjudication Center 500 East Third Street Carson City, NV 89713-0035 Tel (775) 684-0302 Fax (775) 684-0338 Tel (702) 486-7999 Fax (702) 486-7987Document1 paginăAdjudication Center 500 East Third Street Carson City, NV 89713-0035 Tel (775) 684-0302 Fax (775) 684-0338 Tel (702) 486-7999 Fax (702) 486-7987Don YoungÎncă nu există evaluări

- Bahcesehir Universitesi Yeterlilik Sinavı Soru Ve CevaplariDocument16 paginiBahcesehir Universitesi Yeterlilik Sinavı Soru Ve CevaplariIzZet BeyÎncă nu există evaluări

- Ramesh Singh Indian Economy Class 11Document42 paginiRamesh Singh Indian Economy Class 11Abhijit NathÎncă nu există evaluări

- Final Exam Study GuideDocument9 paginiFinal Exam Study GuideDognimin Aboudramane KonateÎncă nu există evaluări

- IRS w4v PDFDocument2 paginiIRS w4v PDFMikeDouglas50% (2)

- Macroeconomics: Dr. Ahmed Said AhmedDocument25 paginiMacroeconomics: Dr. Ahmed Said AhmedNorhan SamyÎncă nu există evaluări

- Circular Flow QuestionsDocument2 paginiCircular Flow QuestionssilÎncă nu există evaluări

- List of Idioms and PhrasesDocument22 paginiList of Idioms and PhrasesVũ Tâm MinhÎncă nu există evaluări

- Term Paper On Current Scenerio of Entrepreneur in BDDocument14 paginiTerm Paper On Current Scenerio of Entrepreneur in BDAshikur Rahman0% (1)

- Macro AssignmentDocument28 paginiMacro AssignmentSabin SadafÎncă nu există evaluări

- Band 8 IELTS Essay SampleDocument3 paginiBand 8 IELTS Essay SampleBibo MovaÎncă nu există evaluări

- Pyramid ModelDocument20 paginiPyramid Modelimre lengyel100% (1)

- Macro Chapter 4Document44 paginiMacro Chapter 4Siddharth Jain100% (1)

- Pestle of Dairy Industry in UsaDocument5 paginiPestle of Dairy Industry in UsaQuyên NguyễnÎncă nu există evaluări

- Business Plan (Sweet-Tastic)Document12 paginiBusiness Plan (Sweet-Tastic)ChichiÎncă nu există evaluări

- Impact of CovidDocument6 paginiImpact of CovidRãjû LãmâÎncă nu există evaluări

- The Great Displacement: Climate Change and the Next American MigrationDe la EverandThe Great Displacement: Climate Change and the Next American MigrationEvaluare: 4.5 din 5 stele4.5/5 (32)

- Workin' Our Way Home: The Incredible True Story of a Homeless Ex-Con and a Grieving Millionaire Thrown Together to Save Each OtherDe la EverandWorkin' Our Way Home: The Incredible True Story of a Homeless Ex-Con and a Grieving Millionaire Thrown Together to Save Each OtherÎncă nu există evaluări

- When Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfDe la EverandWhen Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfEvaluare: 5 din 5 stele5/5 (36)

- The Meth Lunches: Food and Longing in an American CityDe la EverandThe Meth Lunches: Food and Longing in an American CityEvaluare: 5 din 5 stele5/5 (5)

- Heartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthDe la EverandHeartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthEvaluare: 4 din 5 stele4/5 (188)

- Not a Crime to Be Poor: The Criminalization of Poverty in AmericaDe la EverandNot a Crime to Be Poor: The Criminalization of Poverty in AmericaEvaluare: 4.5 din 5 stele4.5/5 (37)

- Life at the Bottom: The Worldview That Makes the UnderclassDe la EverandLife at the Bottom: The Worldview That Makes the UnderclassEvaluare: 5 din 5 stele5/5 (30)

- High-Risers: Cabrini-Green and the Fate of American Public HousingDe la EverandHigh-Risers: Cabrini-Green and the Fate of American Public HousingÎncă nu există evaluări

- Nickel and Dimed: On (Not) Getting By in AmericaDe la EverandNickel and Dimed: On (Not) Getting By in AmericaEvaluare: 3.5 din 5 stele3.5/5 (197)

- The Great Displacement: Climate Change and the Next American MigrationDe la EverandThe Great Displacement: Climate Change and the Next American MigrationEvaluare: 4 din 5 stele4/5 (21)

- Same Kind of Different As Me Movie Edition: A Modern-Day Slave, an International Art Dealer, and the Unlikely Woman Who Bound Them TogetherDe la EverandSame Kind of Different As Me Movie Edition: A Modern-Day Slave, an International Art Dealer, and the Unlikely Woman Who Bound Them TogetherEvaluare: 4 din 5 stele4/5 (686)

- When Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfDe la EverandWhen Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfEvaluare: 4 din 5 stele4/5 (126)

- Hillbilly Elegy: A Memoir of a Family and Culture in CrisisDe la EverandHillbilly Elegy: A Memoir of a Family and Culture in CrisisEvaluare: 4 din 5 stele4/5 (4284)

- Poor Economics: A Radical Rethinking of the Way to Fight Global PovertyDe la EverandPoor Economics: A Radical Rethinking of the Way to Fight Global PovertyEvaluare: 4.5 din 5 stele4.5/5 (263)

- Fucked at Birth: Recalibrating the American Dream for the 2020sDe la EverandFucked at Birth: Recalibrating the American Dream for the 2020sEvaluare: 4 din 5 stele4/5 (173)

- Heartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthDe la EverandHeartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthEvaluare: 4 din 5 stele4/5 (269)

- This Is Ohio: The Overdose Crisis and the Front Lines of a New AmericaDe la EverandThis Is Ohio: The Overdose Crisis and the Front Lines of a New AmericaEvaluare: 4 din 5 stele4/5 (37)

- Nickel and Dimed: On (Not) Getting By in AmericaDe la EverandNickel and Dimed: On (Not) Getting By in AmericaEvaluare: 4 din 5 stele4/5 (186)

- Same Kind of Different As Me Movie Edition: A Modern-Day Slave, an International Art Dealer, and the Unlikely Woman Who Bound Them TogetherDe la EverandSame Kind of Different As Me Movie Edition: A Modern-Day Slave, an International Art Dealer, and the Unlikely Woman Who Bound Them TogetherEvaluare: 4 din 5 stele4/5 (645)

- Dark Days, Bright Nights: Surviving the Las Vegas Storm DrainsDe la EverandDark Days, Bright Nights: Surviving the Las Vegas Storm DrainsÎncă nu există evaluări

- How the Poor Can Save Capitalism: Rebuilding the Path to the Middle ClassDe la EverandHow the Poor Can Save Capitalism: Rebuilding the Path to the Middle ClassEvaluare: 5 din 5 stele5/5 (6)

- Walking the Bowl: A True Story of Murder and Survival Among the Street Children of LusakaDe la EverandWalking the Bowl: A True Story of Murder and Survival Among the Street Children of LusakaEvaluare: 4.5 din 5 stele4.5/5 (2)

- What Difference Do It Make?: Stories of Hope and HealingDe la EverandWhat Difference Do It Make?: Stories of Hope and HealingEvaluare: 4 din 5 stele4/5 (31)