S-ar putea să vă placă și

- American Diplomatic Noncitizen National Passport and MCO52418Document4 paginiAmerican Diplomatic Noncitizen National Passport and MCO52418NotarysTo Go100% (52)

- Fight Debt Collectors and Win: Win the Fight With Debt CollectorsDe la EverandFight Debt Collectors and Win: Win the Fight With Debt CollectorsEvaluare: 5 din 5 stele5/5 (12)

- How to Get Rid of Your Unwanted Debt: A Litigation Attorney Representing Homeowners, Credit Card Holders & OthersDe la EverandHow to Get Rid of Your Unwanted Debt: A Litigation Attorney Representing Homeowners, Credit Card Holders & OthersEvaluare: 3 din 5 stele3/5 (1)

- Affidavit of Loan Denial - FDCPADocument4 paginiAffidavit of Loan Denial - FDCPAPublic Knowledge98% (51)

- Have Fun With Debt CollectorsDocument3 paginiHave Fun With Debt CollectorsTitle IV-D Man with a plan94% (16)

- Consumer Law Cheatsheet 2Document3 paginiConsumer Law Cheatsheet 2Josh Campbell100% (11)

- Notice of Dispute - Proof of Claim - Debt Validation Template 8-10-10 Copy 3Document4 paginiNotice of Dispute - Proof of Claim - Debt Validation Template 8-10-10 Copy 3Nessie Jenkins95% (44)

- Truth in Lending - Affidavit - TemplateDocument12 paginiTruth in Lending - Affidavit - TemplateMarsha Maines100% (14)

- Credit Repair Letter To Send After Debt DischargeDocument6 paginiCredit Repair Letter To Send After Debt Dischargeamenelbey78% (9)

- Damages For FDCPA ViolationsDocument9 paginiDamages For FDCPA Violationscj100% (12)

- Stop! Illegal Predatory Lending: A Self-Help GuideDe la EverandStop! Illegal Predatory Lending: A Self-Help GuideÎncă nu există evaluări

- 15 U.S. Code 1635 - Right of Rescission As To Certain TransactionsDocument7 pagini15 U.S. Code 1635 - Right of Rescission As To Certain TransactionsHelpin Hand100% (5)

- Using RICO To Handle Debt CollectorsDocument19 paginiUsing RICO To Handle Debt CollectorsRandy Rosado100% (9)

- Sucessful Mortgage DischargeDocument48 paginiSucessful Mortgage DischargeAkil Bey83% (30)

- About Charge-Offs: Collection Agent Has The Right To Collect The Entire BalanceDocument4 paginiAbout Charge-Offs: Collection Agent Has The Right To Collect The Entire BalanceBhakta Prakash75% (4)

- Prove A Creditor Is in Violation - Automatic Win For $1000Document7 paginiProve A Creditor Is in Violation - Automatic Win For $1000FreedomofMind100% (11)

- 15 Us Code Subchapter V Debt Collection Practices Very Basic Version With Keywords in Red 05012017Document9 pagini15 Us Code Subchapter V Debt Collection Practices Very Basic Version With Keywords in Red 05012017api-356589607100% (5)

- Debt Cleanse: How To Settle Your Unaffordable Debts for Pennies on the Dollar (And Not Pay Some At All)De la EverandDebt Cleanse: How To Settle Your Unaffordable Debts for Pennies on the Dollar (And Not Pay Some At All)Evaluare: 3 din 5 stele3/5 (1)

- FDCPA FraudDocument44 paginiFDCPA FraudJeff Wilner92% (26)

- The Ultimate Weapon in Debt Elimination: Unlocking the Secrets in Debt EliminationDe la EverandThe Ultimate Weapon in Debt Elimination: Unlocking the Secrets in Debt EliminationEvaluare: 5 din 5 stele5/5 (1)

- Sample Notice of Rescission Under Truth in Lending ActDocument2 paginiSample Notice of Rescission Under Truth in Lending ActStan Burman100% (12)

- Mortgage......... Debt Validation Letter - NoticeDocument28 paginiMortgage......... Debt Validation Letter - Noticevsoskil80% (10)

- Unsecured DebtDocument14 paginiUnsecured Debtapi-374440893% (15)

- CFPB Fair Credit Reporting Act Fcra ProceduresDocument86 paginiCFPB Fair Credit Reporting Act Fcra ProceduresJustin BurgessÎncă nu există evaluări

- Tila Right of Rescission and ConsequencesDocument7 paginiTila Right of Rescission and Consequencesboss4him100% (9)

- Right of Recission ReportDocument15 paginiRight of Recission Reportwebuyhouses4782100% (3)

- Title Iv. - Consumer Credit TransactionDocument24 paginiTitle Iv. - Consumer Credit TransactionALIAHDAYNE POLIDARIOÎncă nu există evaluări

- Truth in Lending - Act PDF BookDocument91 paginiTruth in Lending - Act PDF BookBOSSKING DESIGNS100% (2)

- Find Respa, Tila Fdcpa Fcra Violation CaselawDocument14 paginiFind Respa, Tila Fdcpa Fcra Violation CaselawDeon Thomas100% (1)

- Arkansas Statury Law UnlawfulDocument13 paginiArkansas Statury Law UnlawfulRonnie LongÎncă nu există evaluări

- Violations of The Fair Debt Collection Practices Act (Fdcpa)Document7 paginiViolations of The Fair Debt Collection Practices Act (Fdcpa)sawasinc100% (3)

- Consumer Laws That Protect Your MoneyDocument2 paginiConsumer Laws That Protect Your MoneyDunne Law Offices, P.C.100% (2)

- How To Cancel A MortgageDocument23 paginiHow To Cancel A MortgageCairo Anubiss100% (1)

- Truth in Lending Affidavit 02 07 12Document8 paginiTruth in Lending Affidavit 02 07 12xfritz100% (13)

- TILA Mortgage RescissionDocument3 paginiTILA Mortgage Rescissionklg_consultant868850% (2)

- Affidavit of Fact - No LoanDocument4 paginiAffidavit of Fact - No Loanmusodude100% (16)

- Using The FDCPA To Beat Foreclosure 11-12-13 NOTESDocument15 paginiUsing The FDCPA To Beat Foreclosure 11-12-13 NOTESTRISTARUSA96% (25)

- 15 USC 1635 - Right of Rescission As To Certain TransactionsDocument4 pagini15 USC 1635 - Right of Rescission As To Certain TransactionslostvikingÎncă nu există evaluări

- Adverse Action LettersDocument7 paginiAdverse Action LettersRobat Kooc100% (2)

- How To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionDe la EverandHow To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionÎncă nu există evaluări

- Dealing With Credit Card StatementsDocument3 paginiDealing With Credit Card Statementsjpes100% (6)

- Credit Validation EXDocument6 paginiCredit Validation EXAndyJackson100% (9)

- Fcra and FdcpaDocument4 paginiFcra and FdcpaFreedomofMind100% (1)

- DEBT COLLECTOR VIOLATIONS (1692g)Document9 paginiDEBT COLLECTOR VIOLATIONS (1692g)SLAVEFATHER100% (1)

- Debtor Remedies For WrongsDocument55 paginiDebtor Remedies For WrongsEzekiel Kobina100% (1)

- Truth in Lending Complaint SampleDocument3 paginiTruth in Lending Complaint SampleCarrieonic100% (3)

- Debtors Remedies For Creditors WrongsDocument173 paginiDebtors Remedies For Creditors Wrongscyrusdh100% (4)

- Notice of Cancelation of LoanDocument7 paginiNotice of Cancelation of LoanJulie Hatcher-Julie Munoz Jackson100% (9)

- Debt Elimination StatementDocument2 paginiDebt Elimination StatementKeith Kauhi100% (6)

- TILA Rescission Success Without Tender - HENRY BOTELHO, Plaintiff, V. U.S. BANK, N.a., As Trustee For The LXS 2007-4N Trust, DefendantDocument6 paginiTILA Rescission Success Without Tender - HENRY BOTELHO, Plaintiff, V. U.S. BANK, N.a., As Trustee For The LXS 2007-4N Trust, DefendantForeclosure Fraud100% (4)

- Rule 114 BailDocument22 paginiRule 114 BaildaybarbaÎncă nu există evaluări

- Tila Disclosure Req Viol RemediesDocument15 paginiTila Disclosure Req Viol RemediesCarrieonic100% (9)

- Step 1. Notice of Right To CancelDocument3 paginiStep 1. Notice of Right To Cancellabellaby100% (5)

- Notice of RescissionDocument1 paginăNotice of RescissionArmond Trakarian100% (1)

- Reg ZDocument62 paginiReg ZYolanda Lewis100% (1)

- The Truth Shall Set You Free: Explaining Judicial Hostility To The Truth in Lending Act's Right To Rescind A Mortgage LoanDocument50 paginiThe Truth Shall Set You Free: Explaining Judicial Hostility To The Truth in Lending Act's Right To Rescind A Mortgage LoanRepublic Records BureauÎncă nu există evaluări

- Notice of (Cancellation), (Revocation of Power of Attorney), and (Removal of Trustee and Beneficiary)Document2 paginiNotice of (Cancellation), (Revocation of Power of Attorney), and (Removal of Trustee and Beneficiary)hramcorp100% (7)

- All Debts Are Prepaid PDFDocument7 paginiAll Debts Are Prepaid PDFNat Williams100% (1)

- Outline Foreclosure Defense - Tila & RespaDocument13 paginiOutline Foreclosure Defense - Tila & RespaEdward BrownÎncă nu există evaluări

- RescissionNotice Fin Charge COMPLAINTDocument23 paginiRescissionNotice Fin Charge COMPLAINTLoanClosingAuditors100% (1)

- Desistance Ra PEDocument5 paginiDesistance Ra PEJAYAR MENDZ100% (2)

- Rule 60 CasesDocument28 paginiRule 60 CasesMaria Cristina MartinezÎncă nu există evaluări

- Tila Rescission - Rights and ConsequencesDocument8 paginiTila Rescission - Rights and ConsequencesTA WebsterÎncă nu există evaluări

- Contract of Lease - HouseDocument3 paginiContract of Lease - HouseMae Sntg Ora100% (3)

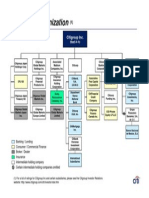

- Bloomberg Markets Magazine - Citifraud July 2012Document10 paginiBloomberg Markets Magazine - Citifraud July 2012CarrieonicÎncă nu există evaluări

- De Zuzuarregui vs. Hon VillarosaDocument3 paginiDe Zuzuarregui vs. Hon VillarosabusinessmanÎncă nu există evaluări

- Republic vs. Rosario, G.R. No. 186635, January 27, 2016 (Stare Decisis)Document2 paginiRepublic vs. Rosario, G.R. No. 186635, January 27, 2016 (Stare Decisis)Charmila Siplon100% (3)

- Class V III ProspectusDocument209 paginiClass V III ProspectusCarrieonicÎncă nu există evaluări

- Consti Reviewer For PrelimsDocument25 paginiConsti Reviewer For PrelimsfaithÎncă nu există evaluări

- 4 Zacarias vs. AnacayDocument1 pagină4 Zacarias vs. AnacaySarah GantoÎncă nu există evaluări

- World Bank Insider Blows Whistle On Corruption - Federal Reserve May 2013Document8 paginiWorld Bank Insider Blows Whistle On Corruption - Federal Reserve May 2013CarrieonicÎncă nu există evaluări

- Fannie Mae Term Sheet For The Citigroup - New Century Mortgage Deal 2006-09-07 Cmlti 2006-NC2Document50 paginiFannie Mae Term Sheet For The Citigroup - New Century Mortgage Deal 2006-09-07 Cmlti 2006-NC283jjmackÎncă nu există evaluări

- SEC Vs Citigroup CDOs RMBS and Class V III Funding Comp-Pr2011-214Document21 paginiSEC Vs Citigroup CDOs RMBS and Class V III Funding Comp-Pr2011-214CarrieonicÎncă nu există evaluări

- In RE CitiGroup Inc Securities Litigation 1Document547 paginiIn RE CitiGroup Inc Securities Litigation 1CarrieonicÎncă nu există evaluări

- FCA Citi Mortgage Complaint-In-InterventionDocument36 paginiFCA Citi Mortgage Complaint-In-InterventionjodiebrittÎncă nu există evaluări

- Citigroup Whistle-Blower Says Bank's Brute Force' Hid Bad Loans From U.SDocument5 paginiCitigroup Whistle-Blower Says Bank's Brute Force' Hid Bad Loans From U.SCarrieonicÎncă nu există evaluări

- r01c 079901Document522 paginir01c 079901CarrieonicÎncă nu există evaluări

- Subsidiarys of Citigroup Inc. 2009 Exhibit21-01Document5 paginiSubsidiarys of Citigroup Inc. 2009 Exhibit21-01CarrieonicÎncă nu există evaluări

- Citi Subsidiarys 2010 Exhibit 21-01Document4 paginiCiti Subsidiarys 2010 Exhibit 21-01CarrieonicÎncă nu există evaluări

- FHFA V Citigroup Inc. (09-02-11)Document95 paginiFHFA V Citigroup Inc. (09-02-11)Master ChiefÎncă nu există evaluări

- Citi V SMITH WDocument4 paginiCiti V SMITH WCarrieonicÎncă nu există evaluări

- Corp Struct CitigroupDocument1 paginăCorp Struct CitigroupCarrieonicÎncă nu există evaluări

- Citi Portfolio CorpDocument2 paginiCiti Portfolio CorpCarrieonicÎncă nu există evaluări

- Company Law 2Document12 paginiCompany Law 2MAHI8888Încă nu există evaluări

- #4 Fieldsman Vs Vda de SongcoDocument2 pagini#4 Fieldsman Vs Vda de SongcoDon SumiogÎncă nu există evaluări

- (Day 48) (Final) The International Finance Corporation (Status, Immunities, and Privileges) Act, 1958Document2 pagini(Day 48) (Final) The International Finance Corporation (Status, Immunities, and Privileges) Act, 1958Deb DasÎncă nu există evaluări

- Curriculum VitaeDocument4 paginiCurriculum VitaeThiam-Jin ChuÎncă nu există evaluări

- Special Court of Review in Re Etta MullinDocument29 paginiSpecial Court of Review in Re Etta MullinMichael Lowe, Attorney at LawÎncă nu există evaluări

- Semblante Vs CADocument2 paginiSemblante Vs CALyka Lim PascuaÎncă nu există evaluări

- Discount Records LTD V Barclays Bank LTD and AnotherDocument6 paginiDiscount Records LTD V Barclays Bank LTD and AnotherLina Zainal100% (1)

- United States v. Brian James Bronson, 4th Cir. (2013)Document3 paginiUnited States v. Brian James Bronson, 4th Cir. (2013)Scribd Government DocsÎncă nu există evaluări

- Criminal Procedure For Atty. GSA (Case Doctrines)Document17 paginiCriminal Procedure For Atty. GSA (Case Doctrines)ERIN CANDICE CANCEKOÎncă nu există evaluări

- Francisco V People, G.R. No. 177720, February 18, 2009Document3 paginiFrancisco V People, G.R. No. 177720, February 18, 2009Hemsley Battikin Gup-ayÎncă nu există evaluări

- A. Case Title B. Reason For Inclusion C. Pertinent Facts D. ExcerptDocument4 paginiA. Case Title B. Reason For Inclusion C. Pertinent Facts D. ExcerptAlex VitasaÎncă nu există evaluări

- Memorial Reprint PDFDocument15 paginiMemorial Reprint PDFSinghÎncă nu există evaluări

- Spouses Oliveros v. Presiding JudgeDocument3 paginiSpouses Oliveros v. Presiding JudgeKobe Lawrence Veneracion0% (1)

- Real Estate: Business Law Project ReportDocument8 paginiReal Estate: Business Law Project ReportChahat ShahÎncă nu există evaluări

- Anti-Hazing Law (Philippines)Document3 paginiAnti-Hazing Law (Philippines)Alvin Cabaltera100% (2)

- HRM 390 ReportDocument8 paginiHRM 390 ReportAmi SakilÎncă nu există evaluări

- Shining Tailors Vs Industrial Tribunal II, U. P., ... On 25 August, 1983Document2 paginiShining Tailors Vs Industrial Tribunal II, U. P., ... On 25 August, 1983vishalbalechaÎncă nu există evaluări

- Avelino G.R. No. L-2821 March 4, 1949 - JOSE AVELINO v. MARIANO J PDFDocument24 paginiAvelino G.R. No. L-2821 March 4, 1949 - JOSE AVELINO v. MARIANO J PDFBeboy Paylangco EvardoÎncă nu există evaluări

- United States v. Damon Stradwick, United States of America v. Daryl Smith, United States of America v. Personne Elrico McGhee, 46 F.3d 1129, 4th Cir. (1995)Document8 paginiUnited States v. Damon Stradwick, United States of America v. Daryl Smith, United States of America v. Personne Elrico McGhee, 46 F.3d 1129, 4th Cir. (1995)Scribd Government DocsÎncă nu există evaluări

- Regional Trial Court: BranchDocument3 paginiRegional Trial Court: BranchBettina BarrionÎncă nu există evaluări