S-ar putea să vă placă și

- Important Insurance Abbreviations Cheat SheetDocument36 paginiImportant Insurance Abbreviations Cheat SheetATUL CHAUHANÎncă nu există evaluări

- IB Math Applications Syllabus Sample Problems PDFDocument267 paginiIB Math Applications Syllabus Sample Problems PDFD FlynnÎncă nu există evaluări

- Khosh Mohammad Coordinate GeometryDocument148 paginiKhosh Mohammad Coordinate GeometryShuvajit Dutta100% (5)

- Profiles: Autocad Civil 3D 2010 Education Curriculum Unit 3: Land DevelopmentDocument31 paginiProfiles: Autocad Civil 3D 2010 Education Curriculum Unit 3: Land Developmentozcapoeira2000Încă nu există evaluări

- Calculus IIDocument386 paginiCalculus IILuizPedroÎncă nu există evaluări

- BezierCurveProof PDFDocument10 paginiBezierCurveProof PDFinderÎncă nu există evaluări

- Bezier CurveDocument14 paginiBezier CurveSarthak SharmaÎncă nu există evaluări

- Solution Manual for an Introduction to Equilibrium ThermodynamicsDe la EverandSolution Manual for an Introduction to Equilibrium ThermodynamicsÎncă nu există evaluări

- CG QnaDocument13 paginiCG QnaabcÎncă nu există evaluări

- De Casteljau algorithm for Bezier curvesDocument6 paginiDe Casteljau algorithm for Bezier curvesIvek RupaÎncă nu există evaluări

- Approximating Cycloids Using Bézier CurvesDocument30 paginiApproximating Cycloids Using Bézier CurvesHarsh ShrivÎncă nu există evaluări

- Bsplines UniDocument3 paginiBsplines Uninitimishra111Încă nu există evaluări

- MATH 4330 HW 2 CorrectedDocument4 paginiMATH 4330 HW 2 Corrected10802117Încă nu există evaluări

- MIT Computational Geometry Problem Set 2 on Spline CurvesDocument3 paginiMIT Computational Geometry Problem Set 2 on Spline Curvesbaoke renÎncă nu există evaluări

- Bezier Curves and SurfacesDocument10 paginiBezier Curves and SurfacesAniruddho RayÎncă nu există evaluări

- Bezier Curves and B-Splines, Blossoming: New York UniversityDocument8 paginiBezier Curves and B-Splines, Blossoming: New York UniversityBalbirÎncă nu există evaluări

- Bezier Curve 1 PDFDocument4 paginiBezier Curve 1 PDFAnsuman MahantyÎncă nu există evaluări

- CurvesAndSurfaces2018 2 PDFDocument4 paginiCurvesAndSurfaces2018 2 PDFParas RastogiÎncă nu există evaluări

- Bezier PDFDocument20 paginiBezier PDFAntonio TankosicÎncă nu există evaluări

- CJC Mathematics Department Explores Parametric EquationsDocument13 paginiCJC Mathematics Department Explores Parametric Equationscoyite8695Încă nu există evaluări

- Properties of Blending FunctionsDocument8 paginiProperties of Blending Functionsayu7kajiÎncă nu există evaluări

- Rational Cubic Implicitization: M. S. FloaterDocument9 paginiRational Cubic Implicitization: M. S. FloaterapoclyteÎncă nu există evaluări

- B Splines 04 PDFDocument16 paginiB Splines 04 PDFShawn PetersenÎncă nu există evaluări

- (Winter 2021) : CS231A: Computer Vision, From 3D Reconstruction To Recognition Homework #2 Due: Friday, Februrary 12Document5 pagini(Winter 2021) : CS231A: Computer Vision, From 3D Reconstruction To Recognition Homework #2 Due: Friday, Februrary 12Nono NonoÎncă nu există evaluări

- 2 Parametric CurvesDocument10 pagini2 Parametric CurvesPhenias ManyashaÎncă nu există evaluări

- La LN10Document9 paginiLa LN10Hi2 HiÎncă nu există evaluări

- Chapter 5 ReviewDocument6 paginiChapter 5 ReviewUp ToyouÎncă nu există evaluări

- Exercises7 SolDocument2 paginiExercises7 SolSichzeugÎncă nu există evaluări

- Derivatives of Rational B Ezier CurvesDocument16 paginiDerivatives of Rational B Ezier Curvestomica06031969Încă nu există evaluări

- LECTURE 4: Linear Least Squares Problem, Normal Equation and QR FactorizationDocument74 paginiLECTURE 4: Linear Least Squares Problem, Normal Equation and QR FactorizationBilal AlderbashiÎncă nu există evaluări

- Problem Solutions - 6Document17 paginiProblem Solutions - 6daglarduman510Încă nu există evaluări

- Homework 3Document5 paginiHomework 3Prakhar AgrawalÎncă nu există evaluări

- Assignment_4Document5 paginiAssignment_4Kalpit AgarwalÎncă nu există evaluări

- How Bezier Curve WorksDocument20 paginiHow Bezier Curve WorksHELL DOZERÎncă nu există evaluări

- Thermal physics model answersDocument4 paginiThermal physics model answersSl xtremeÎncă nu există evaluări

- Bezier Curve and Its Application: Dušan Páleš, Jozef RédlDocument7 paginiBezier Curve and Its Application: Dušan Páleš, Jozef Rédlrohit mittalÎncă nu există evaluări

- Chapter 10 - Fourier Analysis: J.R. Wilson January 7, 2018Document15 paginiChapter 10 - Fourier Analysis: J.R. Wilson January 7, 2018Roy VeseyÎncă nu există evaluări

- Spectrum Analyzer Lab ReportDocument16 paginiSpectrum Analyzer Lab ReportMohammed EllafiÎncă nu există evaluări

- Curve and Surface Construction Using Variable Degree Polynomial SplinesDocument28 paginiCurve and Surface Construction Using Variable Degree Polynomial SplinesLayla VuÎncă nu există evaluări

- Stress Verification Manual v4Document84 paginiStress Verification Manual v4Gilmar BastidasÎncă nu există evaluări

- Parametric CurveDocument28 paginiParametric Curveavi200894Încă nu există evaluări

- BeziercurveDocument13 paginiBeziercurveankit tyagiÎncă nu există evaluări

- Understanding Alternating CurrentDocument31 paginiUnderstanding Alternating CurrentDeepÎncă nu există evaluări

- Engineering Mechanics Dynamics 4th Edition Pytel Solutions ManualDocument83 paginiEngineering Mechanics Dynamics 4th Edition Pytel Solutions Manualfelixquan3x8ua2Încă nu există evaluări

- PHYSA Endler Gallas 2004 PDFDocument7 paginiPHYSA Endler Gallas 2004 PDFRodolfo AraújoÎncă nu există evaluări

- Report: Rotor On Flexible Supports: 1. Free Body Diagram of The SystemDocument3 paginiReport: Rotor On Flexible Supports: 1. Free Body Diagram of The SystemGiovanni LabriniÎncă nu există evaluări

- Picks TheoremDocument10 paginiPicks Theoremcbarraza77398100% (1)

- Curves: Parametric Cubic Splines for Smooth InterpolationDocument40 paginiCurves: Parametric Cubic Splines for Smooth InterpolationAgam SaxenaÎncă nu există evaluări

- Space Curves: B Spline Curves and Their ConstructionDocument28 paginiSpace Curves: B Spline Curves and Their ConstructionRubina HannureÎncă nu există evaluări

- Unit IiDocument39 paginiUnit IiAnbazhagan SelvanathanÎncă nu există evaluări

- Long Col.Document6 paginiLong Col.HAITHAM ALIÎncă nu există evaluări

- Graphical - Analysis PDFDocument4 paginiGraphical - Analysis PDFAiman FitryÎncă nu există evaluări

- Mikota J. (2000): Frequency tuning of a chain structure multi-body oscillator to place the natural frequencies at Omega1 and N-1 integer multiples Omega2 ... Omega N. GAMM 2000, Technical University of Göttingen, Germany.Document2 paginiMikota J. (2000): Frequency tuning of a chain structure multi-body oscillator to place the natural frequencies at Omega1 and N-1 integer multiples Omega2 ... Omega N. GAMM 2000, Technical University of Göttingen, Germany.J MikotaÎncă nu există evaluări

- Scientific Computing - LESSON 10: Polynomial Interpolation - Computational Methods 1Document4 paginiScientific Computing - LESSON 10: Polynomial Interpolation - Computational Methods 1Lee Hei LongÎncă nu există evaluări

- 361 DeCasteljau JohnDocument3 pagini361 DeCasteljau JohnMario PiazzioÎncă nu există evaluări

- Fourier SeriesDocument41 paginiFourier SeriesDeepakÎncă nu există evaluări

- L7 PDFDocument37 paginiL7 PDFDarsh MenonÎncă nu există evaluări

- M2-4-Geom Mod Syn Curv Bezier 230420210945Document67 paginiM2-4-Geom Mod Syn Curv Bezier 230420210945NANDULA GOUTHAM SAIÎncă nu există evaluări

- Manual PHY-103 Laboratory Final IISERDocument72 paginiManual PHY-103 Laboratory Final IISERGourav DasÎncă nu există evaluări

- FM-Frequency Modulation Bandwidth and The Proof of The BESSEL's Series-EnG+ITADocument12 paginiFM-Frequency Modulation Bandwidth and The Proof of The BESSEL's Series-EnG+ITALeonardo RubinoÎncă nu există evaluări

- 3 Abonus BDocument3 pagini3 Abonus BJAyÎncă nu există evaluări

- Parametric Curves SurfacesDocument24 paginiParametric Curves Surfacesben2099Încă nu există evaluări

- PH 203 Quantum Mechanics I - Assignment 4Document5 paginiPH 203 Quantum Mechanics I - Assignment 4NANDEESH KUMAR K MÎncă nu există evaluări

- 2203BPS - Final Exam2009 - Solutions (1) 2Document7 pagini2203BPS - Final Exam2009 - Solutions (1) 2samÎncă nu există evaluări

- GATE 2015 Question Papers With Answers For ME - Mechanical Engineering PDFDocument23 paginiGATE 2015 Question Papers With Answers For ME - Mechanical Engineering PDFATUL CHAUHANÎncă nu există evaluări

- Important Gardens in IndiaDocument3 paginiImportant Gardens in IndiaATUL CHAUHANÎncă nu există evaluări

- Pi 2015 WWW - Questionpaperz.inDocument22 paginiPi 2015 WWW - Questionpaperz.inATUL CHAUHANÎncă nu există evaluări

- GATE 2015 Question Papers With Answers For ME - Mechanical Engineering PDFDocument23 paginiGATE 2015 Question Papers With Answers For ME - Mechanical Engineering PDFATUL CHAUHANÎncă nu există evaluări

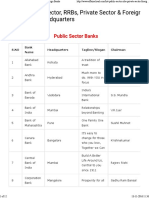

- Banks at GalanceDocument12 paginiBanks at GalanceATUL CHAUHANÎncă nu există evaluări

- Clausius InequalityDocument53 paginiClausius InequalityNandhanÎncă nu există evaluări

- Second Law of ThermodynamicsDocument40 paginiSecond Law of ThermodynamicscaptainhassÎncă nu există evaluări

- GATE 2015 Question Papers With Answers For MA - MathematicsDocument19 paginiGATE 2015 Question Papers With Answers For MA - MathematicsATUL CHAUHANÎncă nu există evaluări

- GATE 2015 Question Papers With Answers For in - Instrumentation EngineeringDocument26 paginiGATE 2015 Question Papers With Answers For in - Instrumentation EngineeringATUL CHAUHANÎncă nu există evaluări

- Top Museums in India: A State-by-State GuideDocument12 paginiTop Museums in India: A State-by-State GuideATUL CHAUHANÎncă nu există evaluări

- Basic ThermoDocument12 paginiBasic ThermoATUL CHAUHANÎncă nu există evaluări

- FC Basics Technology TypesDocument2 paginiFC Basics Technology TypesATUL CHAUHANÎncă nu există evaluări

- Module 8Document12 paginiModule 8Vallapureddy VenkateshÎncă nu există evaluări

- Pure SubstancesDocument42 paginiPure SubstancesATUL CHAUHANÎncă nu există evaluări

- Highest Mountain Peaks StatewiseDocument3 paginiHighest Mountain Peaks StatewiseATUL CHAUHANÎncă nu există evaluări

- MMEMD 103 CAD in ManufacturingDocument3 paginiMMEMD 103 CAD in ManufacturingRaghuÎncă nu există evaluări

- List of PhobiasDocument8 paginiList of PhobiasATUL CHAUHANÎncă nu există evaluări

- 8a CurvesDocument67 pagini8a CurvesMady MathurÎncă nu există evaluări

- Geometric Modelling2Document287 paginiGeometric Modelling2ATUL CHAUHANÎncă nu există evaluări

- Approx Solution of Differential Equations - Variation Principles and Weighted Residual ApproachDocument17 paginiApprox Solution of Differential Equations - Variation Principles and Weighted Residual ApproachATUL CHAUHANÎncă nu există evaluări

- Discretization of Convection-Diffusion Equation - Afinite Volume Approach - 5Document19 paginiDiscretization of Convection-Diffusion Equation - Afinite Volume Approach - 5ATUL CHAUHANÎncă nu există evaluări

- Conservation Equation PDFDocument32 paginiConservation Equation PDFATUL CHAUHANÎncă nu există evaluări

- Chapter 3 InterpolationDocument35 paginiChapter 3 InterpolationATUL CHAUHAN100% (1)

- Cubic SplineDocument29 paginiCubic SplineATUL CHAUHANÎncă nu există evaluări

- L-04 BSplines NURBS.6Document10 paginiL-04 BSplines NURBS.6ATUL CHAUHANÎncă nu există evaluări

- CFD Lecture1Document25 paginiCFD Lecture1GCVishnuKumar100% (1)

- Cubic Hermite Spline Interpolation IIDocument6 paginiCubic Hermite Spline Interpolation IIATUL CHAUHANÎncă nu există evaluări

- CurvesDocument4 paginiCurvesKannan SreenivasanÎncă nu există evaluări

- Cubic Hermite Spline Interpolation IIDocument6 paginiCubic Hermite Spline Interpolation IIATUL CHAUHANÎncă nu există evaluări

- Syllabus2301108 Distribute PDFDocument2 paginiSyllabus2301108 Distribute PDFSupakorn SuttiruangÎncă nu există evaluări

- Multi-Variable Vector Calculus Free EbookDocument205 paginiMulti-Variable Vector Calculus Free Ebookcatclub22Încă nu există evaluări

- 05 CAD Finals Coverage (Week 7-8) Part1Document46 pagini05 CAD Finals Coverage (Week 7-8) Part1glockenspiel9971Încă nu există evaluări

- 3DDocument35 pagini3Dgaurav gargÎncă nu există evaluări

- Topics in Finite Element AnalysisDocument9 paginiTopics in Finite Element Analysischeung ka lungÎncă nu există evaluări

- TrinityDocument55 paginiTrinitystephenÎncă nu există evaluări

- Getting Started With DIAdemDocument51 paginiGetting Started With DIAdemluchotevesÎncă nu există evaluări

- JEE MAINS Marked Syllabus 2024Document21 paginiJEE MAINS Marked Syllabus 2024Anant M NÎncă nu există evaluări

- ATENA Engineering 3D TutorialDocument97 paginiATENA Engineering 3D Tutorialahmad.zaki84Încă nu există evaluări

- Vector CalculusDocument222 paginiVector CalculusTall GeoÎncă nu există evaluări

- Mathematics Online WWW - Mathematicsonline.co - in Three Dimensional Coordinate Assignment 3Document5 paginiMathematics Online WWW - Mathematicsonline.co - in Three Dimensional Coordinate Assignment 3Karm VeerÎncă nu există evaluări

- Solid Edge Fundamentals PDFDocument1.539 paginiSolid Edge Fundamentals PDFOtto Heinrich Wehmann100% (1)

- Chapter I GameprogrammingDocument7 paginiChapter I Gameprogrammingabp007Încă nu există evaluări

- At Struct RefDocument463 paginiAt Struct Refsultan.amirÎncă nu există evaluări

- A New Approach Using The Viterbi Algorithm in Stereo Correspondence ProblemDocument6 paginiA New Approach Using The Viterbi Algorithm in Stereo Correspondence ProblemJeremy ChangÎncă nu există evaluări

- Analytic Solutions for Thermoelastic Analysis of a Cylindrically Anisotropic TubeDocument16 paginiAnalytic Solutions for Thermoelastic Analysis of a Cylindrically Anisotropic Tuberosen95713Încă nu există evaluări

- André Clement, Alain Riviere, Philippe Serre (Auth.), Fred Van Houten, Hubert Kals (Eds.) - Global Consistency of Tolerances - Proceedings of The 6 TH CIRP International Seminar On Computer-AidDocument447 paginiAndré Clement, Alain Riviere, Philippe Serre (Auth.), Fred Van Houten, Hubert Kals (Eds.) - Global Consistency of Tolerances - Proceedings of The 6 TH CIRP International Seminar On Computer-AidEssayas HaileÎncă nu există evaluări

- Great Circle Distance Methode For Improving OperatDocument16 paginiGreat Circle Distance Methode For Improving OperatKunal PawaleÎncă nu există evaluări

- Tensors in Cartesian CoordinatesDocument24 paginiTensors in Cartesian Coordinatesnithree0% (1)

- Challenge 20 Vectors 3 Dimensional Geometry Linear Programming ProblemsDocument1 paginăChallenge 20 Vectors 3 Dimensional Geometry Linear Programming Problemsjitender8Încă nu există evaluări

- Vector Calculus - Cápitulo 1-28-58Document31 paginiVector Calculus - Cápitulo 1-28-58Mario Alberto Loret RosetteÎncă nu există evaluări

- 12th Board Math Lecture PlannerDocument2 pagini12th Board Math Lecture PlannerAditya Singh PatelÎncă nu există evaluări

- Centroid of VolumeDocument10 paginiCentroid of VolumeDianne VillanuevaÎncă nu există evaluări

- Force Vectors: Magnitude: Characterized by Size in Some Units, E.G. 34 N Represented by Length of TheDocument26 paginiForce Vectors: Magnitude: Characterized by Size in Some Units, E.G. 34 N Represented by Length of TheErikÎncă nu există evaluări

- Empirical Design MethodsDocument16 paginiEmpirical Design MethodsyoniÎncă nu există evaluări

- Computer Graphics2-KpDocument166 paginiComputer Graphics2-KpVishnu Viraat AKÎncă nu există evaluări